الفصل السابع: الادخار وصناديق الطوارئ

أهداف تعلم الدرس:

لوريم إيبسوم دولور سيت أميت، consectetur adipiscing إيليت. Ut elit Tellus، luctus nec ullamcorper mattis، pulvinar dapibus leo.

مقدمة عن منتجات الادخار والمنتجات المالية

إن فهم المنتجات المالية المختلفة وأهمية الادخار أمر بالغ الأهمية في إدارة التمويل الشخصي. ويتناول هذا الفصل أنواعًا مختلفة من الحسابات المصرفية، وأهمية أموال الطوارئ، وكيف يؤثر التضخم وأسعار الفائدة على المدخرات. بالإضافة إلى ذلك، يغطي أساسيات المؤسسات المالية وكيفية إدارة وتنمية التمويل الشخصي بشكل فعال.

7.1 Types of Accounts and Financial Services

تقدم المؤسسات المالية مجموعة من الحسابات والخدمات، كل منها مصممة لتلبية احتياجات مالية محددة:

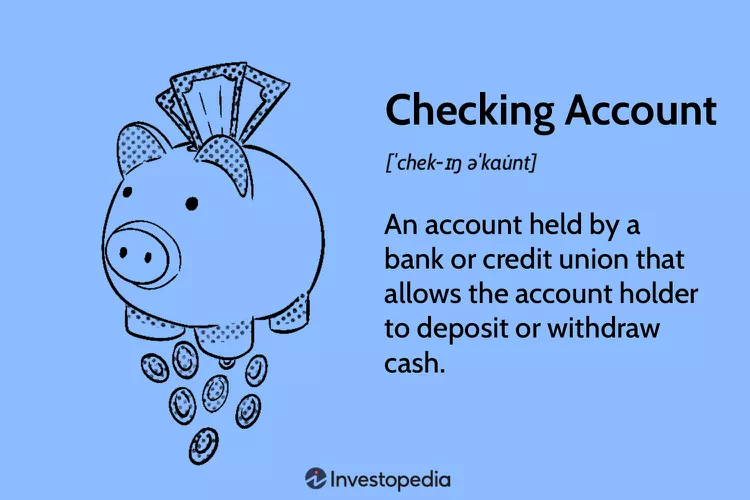

حسابات جارية:

يستخدم للمعاملات اليومية. عادة ما تأتي مع بطاقة خصم و تقديم إيداعات وسحوبات غير محدودة.

- المزايا: سهولة الوصول إلى الأموال، والوصول إلى بطاقة الخصم، ودفع الفواتير عبر الإنترنت.

- العيوب: عادة ما تكون الفائدة المكتسبة منخفضة أو معدومة.

حسابات التوفير:

Aimed at short-term savings over time. Offer interest on the stored funds.

- المزايا: كسب الفائدة، والمخاطر المنخفضة.

- السلبيات: عمليات سحب محدودة، وأسعار فائدة منخفضة محتملة مقارنة بمنتجات الادخار الأخرى.

حسابات سوق النقد (MMAs):

مزيج من حسابات الجاري وحسابات التوفير، وعادة ما تكون معدلات الفائدة فيها أعلى ومتطلبات الحد الأدنى للرصيد أعلى.

- المزايا: أسعار فائدة أعلى، وامتيازات كتابة الشيكات.

- العيوب: متطلبات الحد الأدنى للرصيد عالية، معاملات محدودة.

شهادات الإيداع:

Fixed-term savings account with a guaranteed interest rate.

- المزايا: أسعار فائدة أعلى مقارنة بحسابات التوفير، وعوائد ثابتة.

- السلبيات: غرامات على السحب المبكر، وعدم إمكانية الوصول إلى الأموال إلا بعد انتهاء المدة.

Figure: What is a Checking Account?

وصف:

This image visually defines a checking account, which is a primary tool for managing day-to-day finances. It highlights the main features of the account, such as a debit card and paper checks, which are used to make purchases and pay bills. The graphic serves as a simple introduction to one of the most basic and essential products in personal finance.

الماخذ الرئيسية:

- أ checking account is a type of bank account that provides easy access to your money for daily transactions.

- It is designed for high liquidity, meaning you can withdraw or spend your money quickly using tools like a debit card, ATM, or online transfers.

- The main purpose of this account is for spending and bill payments, not for earning interest; most checking accounts offer little to no interest on your balance.

- Keeping track of your transactions through a bank statement or online portal is crucial for الميزانية and avoiding overdrafts.

تطبيق المعلومات:

- أ checking account is the foundation of personal financial management, acting as the operational center for your income and expenses.

- Learning to manage a checking account is a critical first step in creating a budget, tracking your spending, and building good financial habits.

- For anyone new to finance, this account is an essential tool for safely storing money, paying bills efficiently, and participating in the modern economy.

فتح وإدارة الحساب:

يتطلب فتح حساب مصرفي عادةً تقديم إثبات هوية شخصي ورقم الضمان الاجتماعي وإيداع أولي. تتضمن إدارة الحساب مراقبة الأرصدة وإجراء الإيداعات والسحوبات وفهم الرسوم مثل متطلبات الحد الأدنى للرصيد ورسوم السحب على المكشوف.

مكونات الحساب:

رقم الحساب يحدد حسابك بشكل فريد، بينما يحدد رقم التوجيه البنك الخاص بك - وهو أمر بالغ الأهمية للإيداعات المباشرة وإعداد المدفوعات التلقائية.

اتحادات الإئتمان مقابل البنوك التجارية:

Credit unions typically offer lower fees and better interest rates but might have fewer branches and services. Commercial banks offer a broader range of services but may charge higher fees.

تقييم المنتجات المالية للطلاب

ينبغي على الطلاب أن يأخذوا في الاعتبار حسابات جارية وحسابات توفير مع رسوم منخفضة، وسهولة الوصول إلى الأموال، والموارد التعليمية للمساعدة في إدارة شؤونهم المالية. مزايا تتضمن تعلم إدارة الأموال وكسب الفائدة على المدخرات. العيوب قد يتضمن ذلك إدارة متطلبات الحد الأدنى للرصيد أو التعامل مع الرسوم المحتملة.

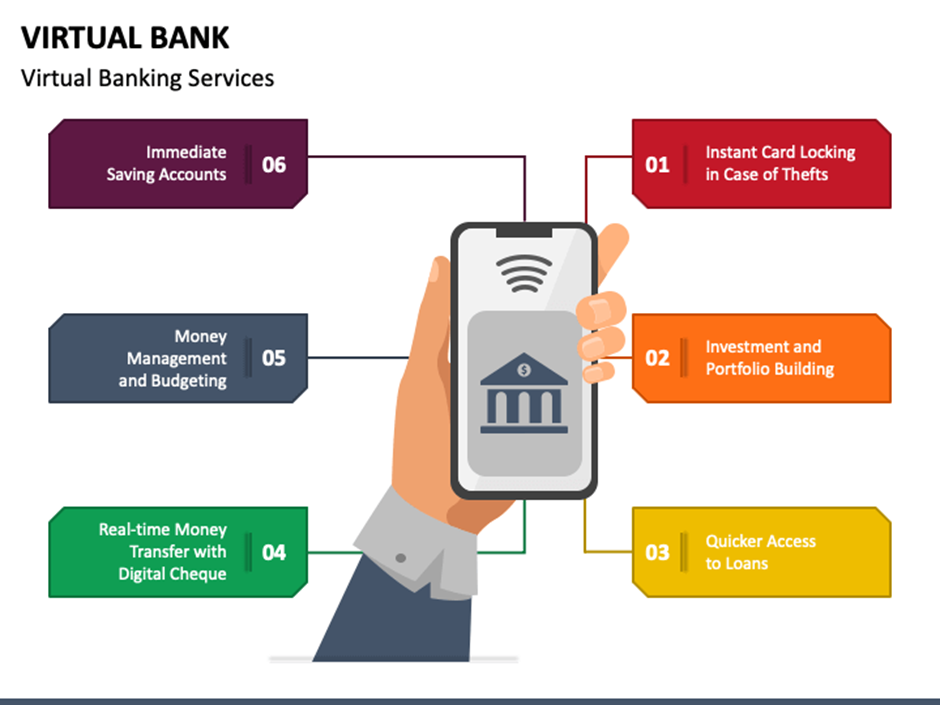

7.2 Online Banking and Account Management

توفر الخدمات المصرفية عبر الإنترنت إمكانية الوصول بسهولة إلى الخدمات المالية، بما في ذلك فتح الحسابات والتحقق من الرصيد وتحويل الأموال. وتتضمن المكونات الرئيسية فهم متطلبات الحد الأدنى للرصيد والرسوم الشهرية وعقوبات السحب على المكشوف وأسعار الفائدة. ومن الضروري تتبع وإدارة الأموال بانتظام لضمان تغطية الحسابات للمعاملات وتجنب الرسوم.

شكل: Key Benefits of Online Banking

وصف:

This graphic illustrates the main advantages of using online banking for managing personal or business finances. It visually highlights key features such as 24/7 account access from any device, the ease of making digital payments, and real-time transaction monitoring. The overall message is that online banking offers a more convenient, efficient, and powerful way to handle financial tasks.

الماخذ الرئيسية:

- Constant Accessibility: A major benefit of online banking is 24/7 access to your accounts from anywhere with an internet connection, eliminating the need to visit a physical bank.

- Efficiency and Cost Savings: It saves significant time by allowing you to automate bill payments and transfer funds instantly, and it often comes with lower fees than traditional banking services.

- Enhanced Financial Control: Online banking provides real-time visibility into your transactions and account balances, which is crucial for accurate budgeting and managing cash flow.

- Simplified Record-Keeping: Many platforms can integrate with accounting software, which automates bookkeeping and makes financial reporting much easier for individuals and businesses.

تطبيق المعلومات:

- Adopting online banking is a foundational step for modern and efficient money management.

- It provides the tools to actively track your spending, automate your savings contributions, and maintain a clear, up-to-the-minute picture of your financial health.

- By leveraging these digital tools, you can reduce time spent on financial administration and focus more energy on achieving your primary goals, like investing for the future or growing a business.

أسعار الفائدة والادخار

عندما يزداد الطلب على القروض، قد تقدم البنوك أسعار فائدة أعلى على الودائع لجذب المزيد من المدخرين، وتزويدهم بالأموال اللازمة للإقراض. وعلى العكس من ذلك، في سوق القروض المشبعة أو الركود الاقتصادي، ينخفض الطلب على الاقتراض، وقد تخفض البنوك أسعار الفائدة على حسابات التوفير.

حسابات الدفع عبر الهاتف المحمول مقابل الخدمات المصرفية التقليدية

توفر حسابات الدفع عبر الهاتف المحمول الراحة وسهولة الاستخدام ولكنها تفتقر عادةً إلى أرباح الفائدة، مما يقلل من إمكانية نمو المدخرات مقارنة بالحسابات التقليدية حسابات التوفير، والتي تقدم الفائدة. حسابات العملات المشفرة وتوفر هذه الصناديق تقلبات عالية وعوائد محتملة ولكنها تفتقر إلى التأمين الفيدرالي، على النقيض من الأمان وإمكانات النمو المطرد التي توفرها حسابات التوفير المؤمنة فيدرالياً.

7.3 Comparing Mobile Payment Accounts, Cryptocurrency Accounts, and Traditional Bank Accounts

While mobile payment platforms like Venmo or Cash App and cryptocurrency wallets offer convenience and fast transactions, they typically do not provide interest earnings or federal insurance protections (like FDIC or NCUA insurance). Traditional savings and checking accounts offer lower risk, provide interest (even if modest), and are protected against institutional failures up to certain limits.

Feature | Mobile Payments | حسابات العملات المشفرة | Traditional Bank Accounts |

تأمين | No federal insurance | No federal insurance | FDIC/NCUA insured |

Interest Earnings | None | Very rare | Common (low to moderate) |

إمكانية الوصول | High (instant transfer) | High (global access) | High (ATM, online banking) |

Risk Level | Medium to high | High (market volatility) | Low |

7.4 Why Certificates of Deposit (CDs) Typically Pay Higher Interest Rates

Certificates of Deposit (CDs) generally offer higher interest rates than regular savings accounts or interest-bearing checking accounts because they require depositors to commit their money for a specific period. This commitment gives banks more certainty about the availability of funds for lending and investments. In exchange for giving up liquidity (easy access to their funds), depositors are rewarded with higher rates. Early withdrawal often results in penalties, reinforcing the importance of keeping funds deposited for the full term.

مثال:

A savings account might offer a 1% interest rate, while a 12-month CD could offer 4% during the same period.

الايجابيات:

- Higher guaranteed returns over the term.

- Safe and predictable growth.

سلبيات:

- Funds are locked until maturity.

- Penalties for early withdrawal.

7.5 Impact of Loan Demand on Deposit Interest Rates

When the demand for loans rises, banks often need additional funds to meet the demand. To attract more deposits (which they use to fund new loans), they may offer higher interest rates on savings accounts, CDs, and other deposit products. Essentially, banks are willing to pay more to bring in money they can lend out profitably.

مثال:

If mortgage applications rise sharply, banks may raise deposit rates from 1.5% to 2% to attract savers and balance their funding needs.

7.6 Market Conditions Leading to Lower Savings Rates

In times of economic slowdown or when consumers and businesses are not borrowing as much, banks don’t need as many deposits. As a result, they may lower the interest rates paid on savings accounts. This often occurs during recessions or when central banks lower benchmark interest rates to stimulate the economy.

مثال:

During a recession, banks may drop savings account interest rates from 2% down to 0.5%, reflecting lower loan demand and economic conditions.

7.7 Impact of Spending vs. Saving

إن الاختيار بين الإنفاق الفوري والادخار للمستقبل يشكل معضلة شائعة. فالإشباع الفوري قد يؤدي إلى الندم إذا منع تحقيق أهداف مالية أكثر أهمية، مثل شراء منزل أو تأمين تقاعد مريح.

السيناريو 1:

قررت إيميلي شراء كمبيوتر محمول عالي الجودة بدافع الاندفاع، منجذبة إلى ميزاته المتقدمة. وبعد أشهر، ندمت على عدم توفير هذا المال للحصول على شهادة مهنية كان من الممكن أن تساعدها في تطوير حياتها المهنية، وهو ما يسلط الضوء على أهمية إعطاء الأولوية للأهداف المالية طويلة الأجل على الإشباع الفوري.

السيناريو 2:

بعد حصوله على المكافأة، حجز جيك على الفور إجازة باهظة الثمن. ورغم أنها كانت ممتعة، إلا أنه تمنى لاحقًا لو كان قد وفر جزءًا من المال لصندوق الطوارئ عندما احتاجت سيارته إلى إصلاحات غير متوقعة، مؤكدًا على التوازن بين الاستمتاع بالحاضر والاستعداد للمستقبل.

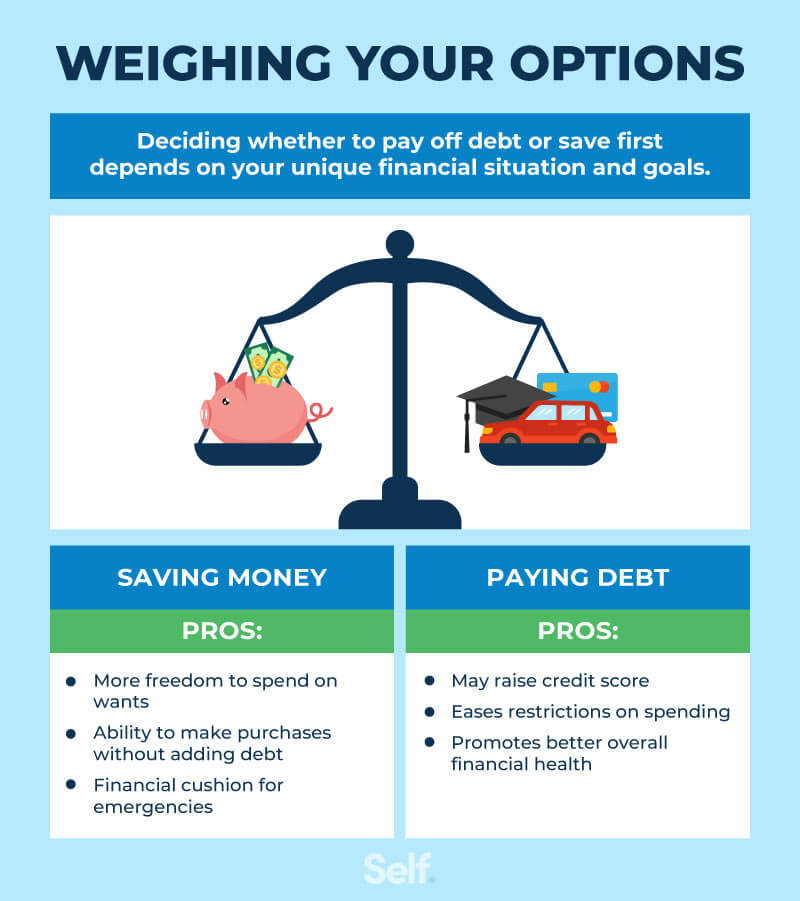

شكل: Pay Off Debt vs. Save Money: Which Comes First?

وصف:

This image tackles the common financial dilemma of whether to focus on paying off debt أو building savings. It presents a clear, step-by-step guide to help you decide where to direct your money first. The framework helps you create a balanced strategy that allows you to build a financial safety net while efficiently eliminating debt.

الماخذ الرئيسية:

- The first priority for almost everyone should be to build a starter صندوق الطوارئ of at least $500 to $1,000. This prevents small emergencies from forcing you into more debt.

- After establishing a small emergency fund, you should aggressively pay down any high-interest debt, like credit card balances, as the interest charged is often very high.

- If your employer offers a retirement plan with a company match, contribute enough to get the full match, as this is essentially a 100% return on your investment and a top priority.

- Once high-interest debt is gone, you can adopt a balanced approach by simultaneously building your full 3-6 month emergency fund and saving for other long-term goals.

تطبيق المعلومات:

- This model provides a clear roadmap to help you make smart decisions and reduce financial stress when you have competing financial priorities.

- You can use this framework to create an effective cash flow plan, ensuring your money is allocated in the most impactful way.

- By following these steps—starter صندوق الطوارئ, attacking high-interest debt, and securing an employer match—you can build a strong financial foundation for future wealth creation.

7.8 Inflation and Interest Rates

يؤدي التضخم إلى تقليص قيمة النقود بمرور الوقت، مما يقلل من القدرة الشرائية للمدخرات. ولا يأخذ سعر الفائدة الاسمي في الاعتبار التضخم، في حين يشير سعر الفائدة الحقيقي (سعر الفائدة الاسمي مطروحًا منه معدل التضخم) إلى النمو الفعلي للمدخرات. وينبغي للمدخرين أن يسعوا إلى سعر فائدة اسمي يفوق التضخم للحفاظ على قيمة مدخراتهم.

سعر الفائدة = الفائدة الاسمية – معدل التضخم

مثال:

إذا كان سعر الفائدة الاسمي على حساب التوفير 3% وكان معدل التضخم 2%، فإن سعر الفائدة الحقيقي هو فعليًا 1%. على مدار عام واحد، تنمو القوة الشرائية للأموال في هذا الحساب بمقدار 1% فقط عند تعديلها وفقًا للتضخم، مما يؤكد أهمية البحث عن خيارات الادخار أو الاستثمار التي تتفوق على التضخم لتنمية الثروة بشكل حقيقي بمرور الوقت.

7.9 Inflation Protection and I Bonds

تم تصميم السندات للحماية من التضخم، حيث تتكيف أسعار فائدتها مع التضخم. عندما يرتفع التضخم، يرتفع سعر الفائدة على السندات، مما يضمن احتفاظ المدخرات بقوتها الشرائية بمرور الوقت، على عكس شهادات الإيداع التقليدية، حيث قد تؤدي أسعار الفائدة الثابتة إلى عوائد حقيقية سلبية في بيئات التضخم المرتفع.

القيمة المستقبلية والخصم

شكل: Calculating the Future Value of a Single Cash Flow

وصف:

The infographic likely demonstrates the formula for calculating the future value of a single cash flow, which is a fundamental concept in finance. This formula helps in understanding how much an investment made today will grow to at a future date, considering a specific rate of interest. The formula is typically represented as FV = PV(1 + r)^n, where FV is the future value, PV is the present value, r is the interest rate, and n is the number of periods.

الماخذ الرئيسية:

- تعتبر صيغة القيمة المستقبلية (FV) ضرورية لحساب مدى نمو الاستثمارات بمرور الوقت.

- إن فهم هذه الصيغة يسمح للمستثمرين بتقدير قيمة الاستثمارات في المستقبل.

- تتضمن المتغيرات في الصيغة القيمة الحالية (PV)، ومعدل الفائدة (r)، وعدد الفترات (n)، حيث يلعب كل منها دورًا حاسمًا في الحساب.

تطبيق المعلومات:

This concept is essential for anyone involved in financial planning, investment analysis, or saving for future goals. By applying this formula, individuals can make informed decisions about their investments, understanding how different rates of interest and time periods affect the growth of their money. It encourages strategic investment and helps in setting realistic expectations for investment returns, which is fundamental for long-term financial planning and wealth accumulation.

وباستخدام جدول بيانات، نحسب أن طفلاً يبلغ من العمر 10 أعوام يحتاج إلى ادخار $200 دولار أميركي شهرياً بمعدل فائدة سنوي 5% لتغطية تكاليف سنة دراسية جامعية، والتي تقدر بنحو 1TP42000 دولار أميركي بعد ثماني سنوات من الآن. ويوضح هذا المثال خصم القيمة المستقبلية للمال، مع مراعاة الفائدة لتحديد المبلغ الذي يتعين ادخاره اليوم لتحقيق الأهداف المالية المستقبلية.

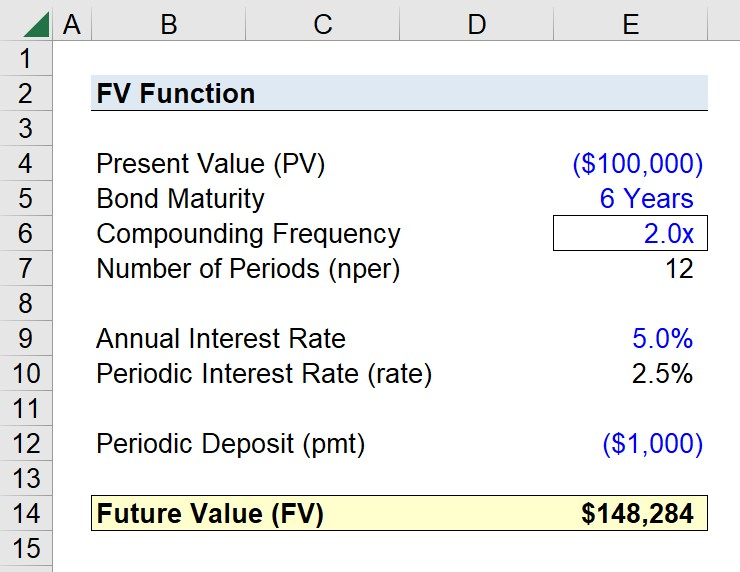

شكل: Using the FV Function in Excel to Calculate Future Value

وصف:

The infographic likely demonstrates how to use the FV function in Excel to calculate the future value of an investment, considering a constant interest rate over a number of periods. The FV function is a powerful tool in Excel for financial analysis, allowing users to input variables such as rate, number of periods, payments, present value, and type (whether payments are made at the beginning or end of periods) to compute the future value of an investment.

الماخذ الرئيسية:

- تعتبر وظيفة FV في Excel ضرورية لحساب القيمة المستقبلية للاستثمارات.

- تتضمن المدخلات الرئيسية لوظيفة القيمة المستقبلية سعر الفائدة وعدد الفترات والدفعات الدورية والقيمة الحالية وتوقيت الدفع.

- إن فهم كيفية استخدام وظيفة القيمة المالية (FV) يمكن أن يعزز بشكل كبير مهارات النمذجة المالية وتحليل الاستثمار.

تطبيق المعلومات:

This knowledge is crucial for finance students, financial analysts, and anyone involved in investment planning or analysis. By mastering the FV function, users can quickly assess the potential future value of investments, aiding in decision-making processes. It’s particularly useful for evaluating the growth of savings accounts, retirement funds, or any investment over time, providing a clear picture of financial futures.

7.10 Down Payments and Loans

يؤدي سداد دفعة أولى على قرض، مثل دفعة أولى 20% على منزل، إلى تقليل المبلغ الإجمالي المقترض، مما يؤدي إلى دفعات شهرية أقل ومعدلات فائدة أفضل في كثير من الأحيان. وهذا يجعل المقترض أكثر جاذبية للمقرضين ويمكن أن يقلل بشكل كبير من تكلفة القرض بمرور الوقت.

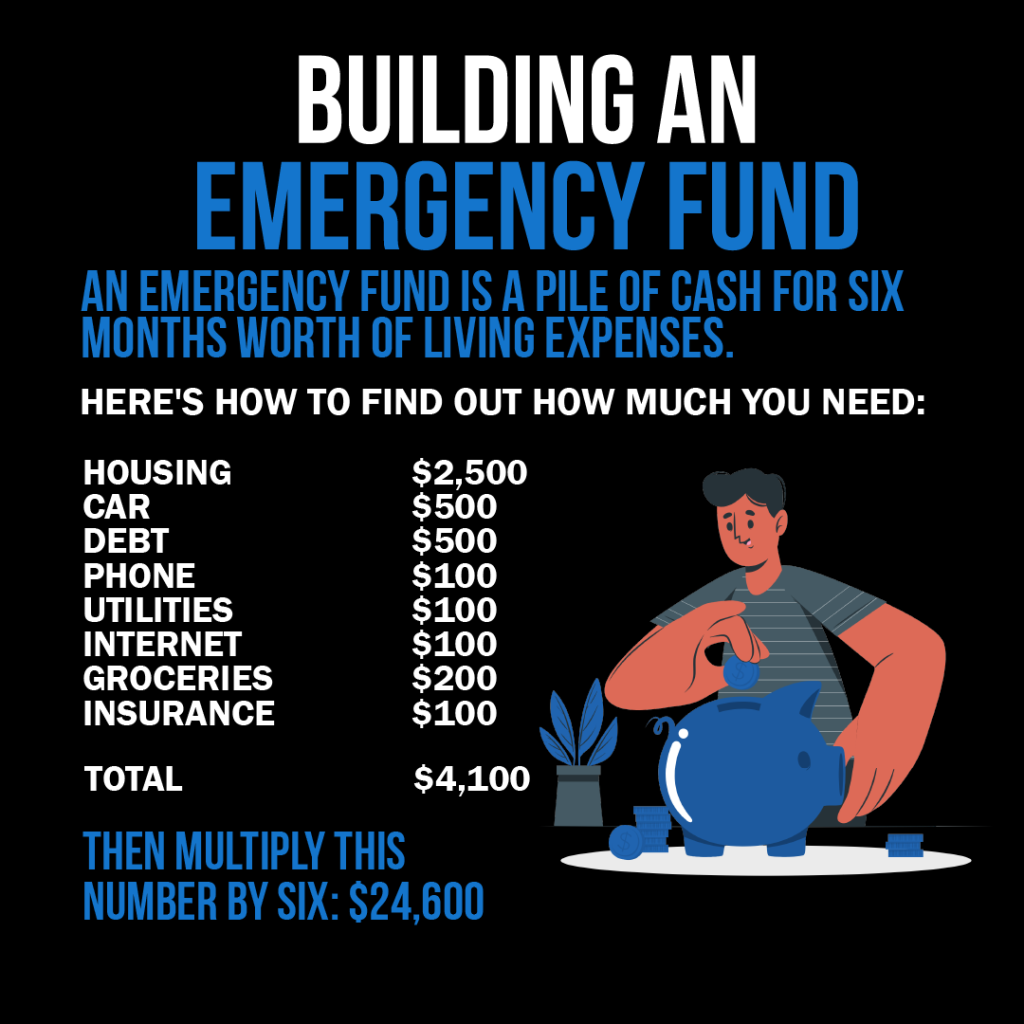

7.11 Emergency Funds and Financial Planning

يعد صندوق الطوارئ أمرًا بالغ الأهمية للاستقرار المالي، حيث يوفر شبكة أمان للنفقات غير المتوقعة. إن إنشاء ميزانية والحفاظ عليها تتضمن مخصصات للادخار على المدى القصير والطويل يضمن الاستعداد لمواجهة عدم اليقين في الحياة والتقدم نحو الأهداف المالية.

مثال:

تعطلت سيارة ماريا، مما يتطلب إصلاحات باهظة الثمن. قامت بمراجعة ميزانيتها لتقليل الإنفاق التقديري وإعادة تخصيص الأموال من فئات الترفيه وتناول الطعام بالخارج لتغطية تكاليف الإصلاح، في حين قللت مؤقتًا من المساهمات في حساب التوفير الخاص بها.

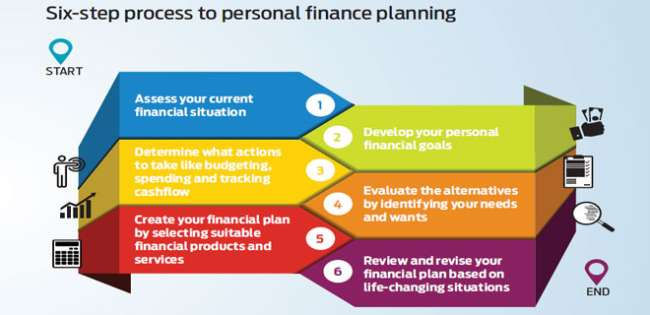

شكل:عملية من ست خطوات لتخطيط التمويل الشخصي

وصف:

تقدم الصورة عملية من ست خطوات لتخطيط التمويل الشخصي. ويبدأ بتقييم الوضع المالي الحالي للفرد، بما في ذلك الأصول والخصوم، ويستمر من خلال تحديد الأهداف المالية، وإنشاء خطة عمل، وتقييم خيارات الاستثمار، وتنفيذ الخطة، ومراجعة الإستراتيجية وتنقيحها بانتظام.

الماخذ الرئيسية:

- تقييم المالية الحالية أمر بالغ الأهمية كنقطة انطلاق للتخطيط.

- تحديد الأهداف يتضمن تحديد القيمة والجداول الزمنية للتطلعات المالية القصيرة والمتوسطة والطويلة الأجل.

- ان خطة عمل يجب أن تأخذ في الاعتبار مدى تحمل الفرد للمخاطر ومواءمة خيارات الاستثمار وفقًا لذلك.

- خيارات الاستثمار وينبغي ربطها بأهداف محددة واختيارها على أساس الكفاءة الضريبية وملاءمتها.

- الاستثمار المنتظم يساهم في تكوين العادة وتحقيق الأهداف المالية بسلاسة.

- المراجعات الدورية التأكد من أن الاستثمارات تسير على الطريق الصحيح والسماح بإجراء التعديلات حسب الحاجة.

تطبيق المعلومات:

يعد البدء بتقييم الوضع المالي الحالي للفرد أمرًا أساسيًا في تخطيط التمويل الشخصي. من خلال فهم وضعك المالي، يمكنك وضع أهداف واقعية، وتحديد مجالات التحسين، وإنشاء خريطة طريق لتحقيق الاستقرار المالي والنمو. وتضمن هذه الخطوة أن يرتكز التخطيط اللاحق على الواقع وأن يكون مصممًا ليناسب الظروف المالية الفريدة للفرد.

Contingency Planning for Financial Emergencies

Contingency planning involves preparing for unexpected financial shocks by having backup savings or insurance. A good contingency plan can help cover emergency expenses such as car repairs, medical bills, sudden unemployment, or major household repairs without derailing long-term financial goals.

مثال:

- Backup Fund: Besides an emergency fund, maintain a small “contingency fund” specifically for very short-term needs.

- Insurance: Maintain adequate health, auto, and renters/homeowners insurance to mitigate major risks.

- Backup Budget: Create a reduced-spending version of your budget to activate if income drops suddenly.

فهم الأجور والخصومات

الأجر الإجمالي هو إجمالي أرباح الموظف قبل أي خصومات. صافي الأجرأو الراتب الصافي، هو ما يتبقى بعد الضرائب والرعاية الصحية وغيرها من الخصومات. وفهم الفرق بينهما أمر ضروري لإعداد الميزانية بدقة.

7.12 Financial Institutions and Services

تقدم المؤسسات المالية، بما في ذلك البنوك والاتحادات الائتمانية والمنصات عبر الإنترنت، منتجات متنوعة مثل الحسابات الجارية وحسابات التوفير وخدمات التخطيط المالي. يعد اختيار المؤسسة والخدمات المناسبة أمرًا حيويًا لإدارة الأموال بفعالية وتحقيق الأهداف المالية.

مثال على إدارة الحساب:

لإدارة حساب جارٍ بشكل فعّال، راجع المعاملات بانتظام وقارنها بالسجلات الشخصية لضمان الدقة. يمكن أن يؤدي استخدام تطبيقات الخدمات المصرفية عبر الهاتف المحمول إلى تبسيط عملية التتبع والمساعدة في تجنب رسوم السحب على المكشوف.

7.13 The Role of FDIC and NCUA Insurance

The Federal Deposit Insurance Corporation (FDIC) insures deposits at banks, while the National Credit Union Administration (NCUA) insures deposits at credit unions. Both agencies guarantee deposit accounts (up to $250,000 per depositor, per insured bank or credit union) in case the financial institution fails. This insurance provides consumers with peace of mind that their money is protected against institutional collapse.

مثال:

If your bank closes unexpectedly, the FDIC will reimburse your insured deposits up to the coverage limit.

خاتمة

Saving, managing financial products, preparing for inflation, and understanding the broader banking environment are essential skills for long-term financial success. By supplementing your knowledge with insights about CDs, market influences on interest rates, the differences between mobile/crypto accounts and traditional banks, federal insurance protections, and emergency contingency planning, you’ll be even better equipped to protect and grow your financial future.

معلومات الدرس الرئيسية:

لوريم إيبسوم دولور سيت أميت، consectetur adipiscing إيليت. Ut elit Tellus، luctus nec ullamcorper mattis، pulvinar dapibus leo.