عالميًا: استراتيجيات رئيسية للثقافة المالية واتخاذ القرارات المستنيرة

أهداف تعلم الدرس:

مقدمة:

This section covers the strategies needed to enhance financial literacy and make informed decisions. Understanding how to stay updated on financial trends, use digital tools, and collaborate with financial professionals is crucial for effective personal finance management.

- Stay Informed About Personal Finance: Learn how to regularly access reliable financial news, follow economic indicators, and participate in financial education programs. Staying informed allows individuals to understand how economic changes, tax policies, and new financial tools can affect their personal finances and decision-making.

- Use Financial Tools and Software: Discover the benefits of using digital tools like budgeting apps, منصات الاستثمار، و tax software to manage personal finances. By using these tools, individuals can plan their budgets, monitor investments, and handle tax filing efficiently, leading to better financial outcomes.

- Work with Financial Professionals: Explore when and why to seek guidance from financial professionals, such as المستشارين الماليين, investment specialists, ، أو tax experts. This helps users make confident decisions in complex financial situations, such as retirement planning, investment diversification, or large purchases.

- Build Financial Confidence: Understand the importance of continuous learning and evaluation in financial decision-making. By combining insights from الأدوات الرقمية, تعليم، و professional advice, users can develop the skills needed to set realistic financial goals and achieve them.

A. Staying Informed About Personal Finance

Personal finance is a dynamic field, with new products, regulations, and trends emerging regularly. Staying informed is crucial for making sound financial decisions, whether related to saving, investing, or managing debt. Individuals must take proactive steps to keep up with financial news, economic trends, and changes in personal finance tools or government policies.

- Regularly Accessing Reliable Financial News: Keeping up with financial news from reliable sources is essential for understanding how economic shifts—such as interest rate changes or market trends—can impact personal finance. Reputable websites, news channels, and financial blogs provide up-to-date information on global markets, interest rates, inflation, and financial products.

- مثال: A consumer might regularly read financial publications like the Financial Times, The Wall Street Journal, ، أو Bloomberg to stay updated on global market trends and economic policies.

- مثال: A consumer might regularly read financial publications like the Financial Times, The Wall Street Journal, ، أو Bloomberg to stay updated on global market trends and economic policies.

- Following Economic Indicators: Being aware of key economic indicators, such as معدلات التضخم, unemployment figures، و الزيادة في الناتج المحلي, helps individuals understand the broader economic environment and how it could affect their personal finances.

- مثال: If inflation is rising, a consumer may adjust their budget to account for increasing costs of goods and services or explore investment opportunities that protect against inflation, such as السندات المرتبطة بالتضخم.

- مثال: If inflation is rising, a consumer may adjust their budget to account for increasing costs of goods and services or explore investment opportunities that protect against inflation, such as السندات المرتبطة بالتضخم.

- Participating in Financial Education Programs: Many organizations, government bodies, and non-profits offer financial education programs designed to help individuals improve their financial literacy. Participating in these programs allows individuals to deepen their understanding of personal finance and make more informed financial decisions.

- مثال: ال OECD International Network on Financial Education (INFE) offers global resources to improve financial education across countries.

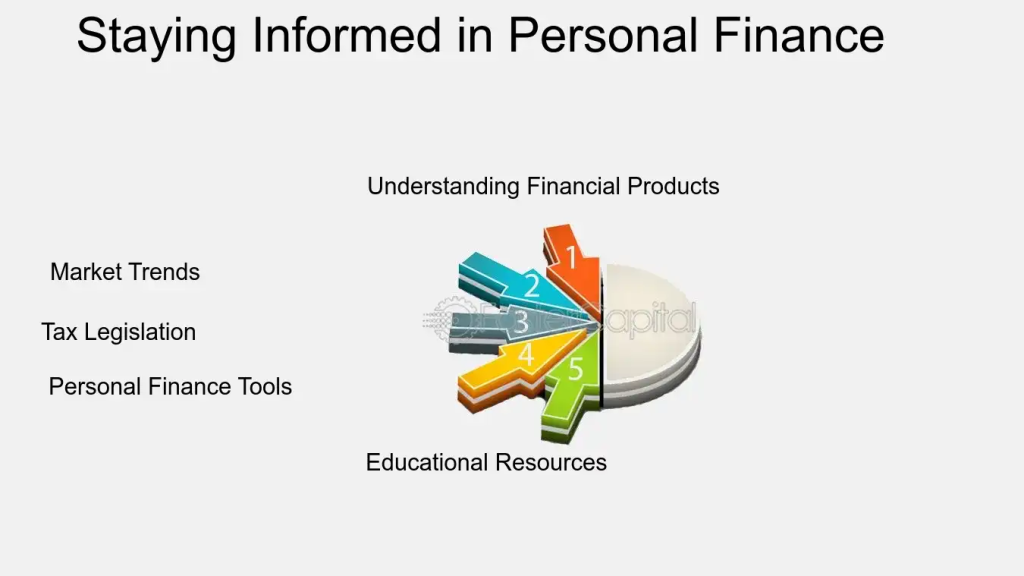

شكل: Staying Informed in Personal Finance

وصف:

The figure highlights key aspects that are essential for staying informed in the field of personal finance. It includes Market Trends, Tax Legislation, Personal Finance Tools, Educational Resources, و Understanding Financial Products. Each component plays a role in helping individuals manage their finances effectively by ensuring they have access to the latest information, tools, and resources.

الماخذ الرئيسية:

- اتجاهات السوق provide insights into the direction of the economy, helping people make informed financial decisions.

- Tax Legislation knowledge is critical for understanding how different financial actions affect taxes.

- Personal Finance Tools offer practical assistance in budgeting, saving, and managing investments.

- Educational Resources enhance understanding and keep users informed of new financial products and strategies.

- Understanding Financial Products enables individuals to choose the best options for their financial goals.

تطبيق المعلومات:

Staying informed in التمويل الشخصي helps individuals make better financial decisions by understanding the impact of external factors like taxes and market trends. Regularly using finance tools and resources ensures continuous learning and adaptation to financial changes.

ب. استخدام الأدوات والبرمجيات المالية

In today’s digital world, numerous الأدوات والبرمجيات المالية are available to help individuals manage their finances more effectively. These tools assist with budgeting, saving, investing, and tracking expenses, making it easier to make informed financial decisions.

- Budgeting Tools: Digital budgeting tools, such as النعناع, YNAB (You Need a Budget)، و PocketGuard, help individuals track their income, expenses, and savings goals. By visualizing spending patterns, users can make adjustments to their budgets to achieve financial goals like reducing debt or increasing savings.

- مثال: A user of النعناع can link their bank accounts and credit cards to the app, which then categorizes their spending automatically, helping them identify areas where they can cut back and save more.

2. Investment Platforms and Calculators: Online platforms like E*TRADE, Robinhood، و Vanguard make investing accessible to individuals, while investment calculators help users understand potential returns based on investment amounts, interest rates, and time horizons. These tools are essential for إدارة المحافظ and long-term financial planning.

- مثال: A user of Vanguard can use the platform’s investment tools to simulate different retirement scenarios, adjusting variables like the amount saved, investment returns, and retirement age.

- مثال: A user of Vanguard can use the platform’s investment tools to simulate different retirement scenarios, adjusting variables like the amount saved, investment returns, and retirement age.

3. Debt Management Tools: For individuals managing debt, tools like Debt Payoff Planner و Tally help track debt repayment schedules, calculate interest, and offer strategies for paying off loans faster. These tools can also provide reminders for upcoming payments to avoid late fees.

4. Tax Software: Platforms such as TurboTax, H&R Block، و TaxSlayer help individuals navigate the complexities of tax filing, allowing them to calculate deductions, credits, and refunds. Using tax software ensures accuracy and maximizes tax savings.

مثال: A freelancer might use TurboTax to file taxes efficiently by tracking deductions and expenses related to their business, maximizing potential tax refunds

5. Robo-Advisors: المستشارون الروبوتيون، مثل Betterment, Wealthfront، و Schwab Intelligent Portfolios, use algorithms to provide automated financial advice and portfolio management. These tools are ideal for individuals who want to invest without needing to manually manage their portfolios.

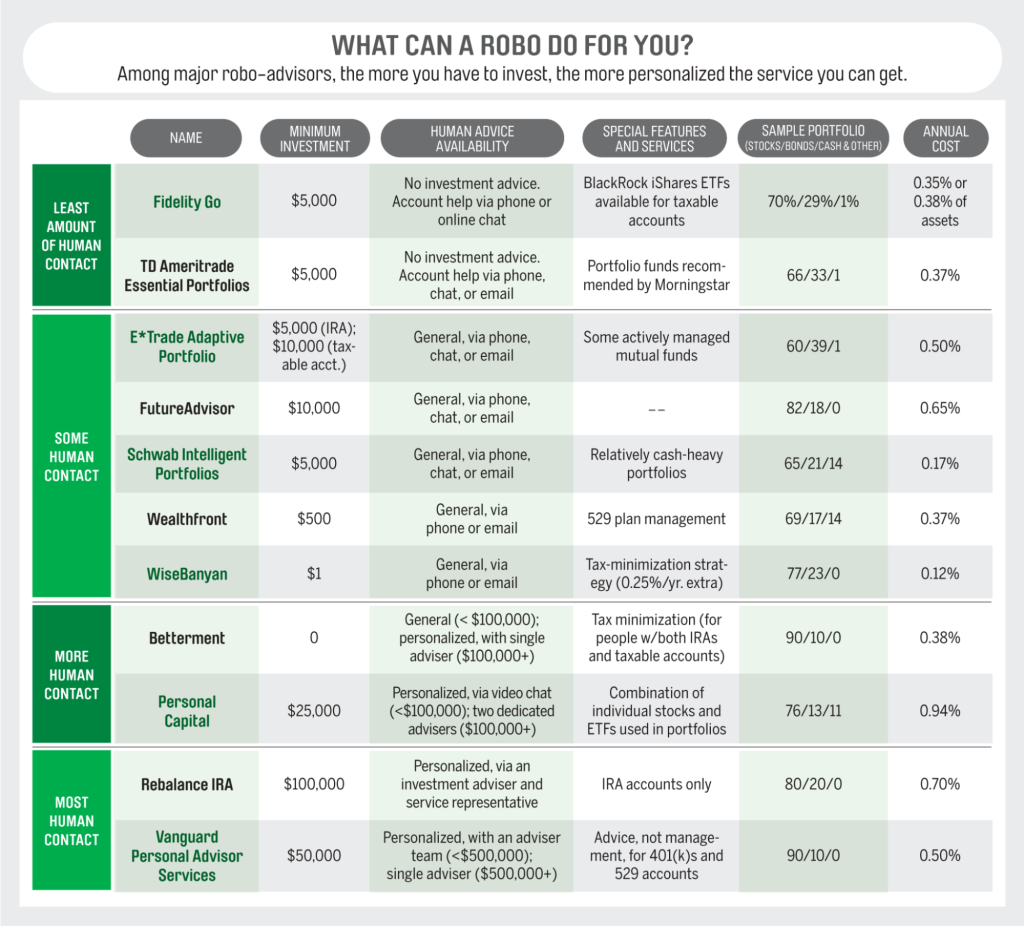

Figure: What Can a Robo Do For You?

وصف:

The figure compares various robo-advisors, detailing information about minimum investment, human advice availability, special features and services, sample portfolio allocation (stocks/bonds/cash & other), and annual cost. The list is categorized based on the level of human contact offered, ranging from the least to the most human interaction. Each row provides specific details about the services of well-known robo-advisors, helping users understand the differences in cost, investment strategies, and service features.

الماخذ الرئيسية:

- Robo-advisors vary in the level of human interaction they offer, from no contact to personalized advisory services.

- Minimum investments differ, with some platforms like WiseBanyan requiring as little as $1, while others need higher amounts, such as $100,000 for Rebalance IRA.

- Costs and features also vary, with annual fees ranging from 0.12% to 0.94%, depending on the services and portfolio management.

- Portfolio allocations indicate the focus on different asset classes, helping users choose based on risk tolerance and investment goals.

- Special features like tax-minimization strategies and IRA management help tailor investment plans to individual needs.

تطبيق المعلومات:

This information is helpful for المستثمرين to evaluate and compare different robo-advisors based on their أهداف الاستثمار و ميزانية. By understanding the differences in services, costs, and strategies, users can make informed decisions on selecting a platform that best suits their التخطيط المالي needs.

ج. العمل مع المتخصصين الماليين

While digital tools are useful, there are times when individuals should seek the guidance of المهنيين الماليين for more complex financial decisions, such as tax planning, investment strategies, and estate planning.

- When to Work with Financial Professionals: Financial professionals, such as المخططين الماليين, investment advisors، و tax advisors, offer tailored advice that can help individuals navigate significant life events like buying a home, saving for retirement, or managing a large inheritance.

- مثال: A financial planner can help a young couple develop a savings plan for their child’s education while also preparing for their own retirement by balancing short-term and long-term goals.

- مثال: A financial planner can help a young couple develop a savings plan for their child’s education while also preparing for their own retirement by balancing short-term and long-term goals.

- Choosing the Right Financial Professional: It’s important to choose a qualified and trustworthy financial professional. Consumers should verify credentials, such as Certified Financial Planner (CFP) أو Chartered Financial Analyst (CFA), and ensure that the professional’s services align with their financial needs.

- Independent vs. Non-Independent Advisors: Independent advisors are obligated to provide unbiased advice and act in their client’s best interest. Non-independent advisors may receive commissions for promoting specific financial products, which could influence their recommendations. Consumers should understand the difference and choose accordingly.

- مثال: A high-net-worth individual might choose to work with a CFA-certified investment advisor to diversify their portfolio and minimize tax liabilities across multiple jurisdictions.

- Independent vs. Non-Independent Advisors: Independent advisors are obligated to provide unbiased advice and act in their client’s best interest. Non-independent advisors may receive commissions for promoting specific financial products, which could influence their recommendations. Consumers should understand the difference and choose accordingly.

- Using Hybrid Financial Advice Models: In addition to traditional advisors, many individuals now turn to hybrid models that combine human advisors with digital tools. Platforms like Personal Capital أو Vanguard Personal Advisor Services offer a blend of automated portfolio management and personalized human advice, providing a more cost-effective solution for individuals seeking ongoing financial support.

- Discussing Financial Goals and Concerns: Whether working with a financial planner or an investment advisor, it is important for individuals to be clear about their financial goals, concerns, and risk tolerance. Open communication ensures that the advisor can provide the best advice tailored to the individual’s unique situation.

- مثال: A retiree working with a financial advisor may prioritize استقرار الدخل و الحفاظ على رأس المال over aggressive growth, and the advisor can design an investment portfolio accordingly.

- مثال: A retiree working with a financial advisor may prioritize استقرار الدخل و الحفاظ على رأس المال over aggressive growth, and the advisor can design an investment portfolio accordingly.

Figure: How to Choose the Right Financial Advisor for You

وصف:

The figure outlines eight key factors to consider when choosing a financial advisor. These include evaluating the advisor’s credentials and experience, تعويض structure, and investment philosophy. Other aspects to consider are the services offered, the advisor’s clientele, إمكانية الوصول, communication style، و personality. This comprehensive approach helps users make informed decisions when selecting a financial advisor.

الماخذ الرئيسية:

- Credentials and experience are crucial for assessing an advisor’s reliability and expertise.

- Compensation models (e.g., fee-only, commission-based) impact the cost and potential conflicts of interest.

- Investment philosophy should align with the investor’s financial goals and risk tolerance.

- Accessibility and communication style ensure smooth interactions and ease of reaching the advisor when needed.

- Considering the advisor’s clientele and personality can help determine if they are a good fit for one’s unique financial situation.

تطبيق المعلومات:

This guide helps investors assess and compare different advisors by focusing on factors that matter most to their financial goals. It allows users to make قرارات مبلغة about selecting an advisor who can provide suitable investment advice و personalized support, ensuring a good match between the investor’s needs and the advisor’s services.

معلومات الدرس الرئيسية:

- Staying Informed: Regularly accessing reliable financial news, ، التتبع economic indicators, and engaging in financial education programs helps individuals make informed financial decisions. Staying updated on market trends, tax changes, and economic shifts is essential for adapting financial plans accordingly.

- Using Digital Financial Tools: أدوات مثل النعناع, Vanguard، و TurboTax make managing personal finances easier by providing insights into spending, investments, and taxes. By regularly using these tools, individuals can improve budgeting, enhance investment strategies, and ensure accurate tax filing.

- العمل مع المتخصصين الماليين: Consulting with financial advisors for significant financial decisions, such as buying a home or planning for retirement, offers tailored guidance. Choosing between independent و non-independent advisors helps ensure objective advice, enhancing financial outcomes.

- Combining Digital and Human Advice: Hybrid models, such as Personal Capital أو Vanguard Personal Advisor Services, offer a mix of digital tools and human support, providing personalized and cost-effective financial management solutions. This approach combines automation with professional insights, helping users meet their financial goals.

- Building Financial Confidence: Using a mix of التعليم المالي, الأدوات الرقمية, and professional advice empowers individuals to manage their finances confidently. This combination supports informed decisions, effective goal-setting, and long-term financial growth.

كلمة الختام:

Applying these strategies to enhance financial literacy and decision-making enables users to manage personal finances with greater confidence. By staying informed, using digital tools, and seeking professional guidance, individuals can make well-informed financial choices and work towards achieving their financial goals.