الفصل 13: التخطيط للتقاعد (الولايات المتحدة الأمريكية)

أهداف تعلم الدرس:

لوريم إيبسوم دولور سيت أميت، consectetur adipiscing إيليت. Ut elit Tellus، luctus nec ullamcorper mattis، pulvinar dapibus leo.

يتضمن التخطيط للتقاعد في الولايات المتحدة فهم المصادر المتعددة الجوانب للدخل التقاعدي ودور الضمان الاجتماعي في التخطيط للتقاعد. فيما يلي استكشاف للجوانب الرئيسية المتعلقة بالتخطيط للتقاعد في الولايات المتحدة، بما في ذلك الضمان الاجتماعي ومصادر الدخل الأخرى.

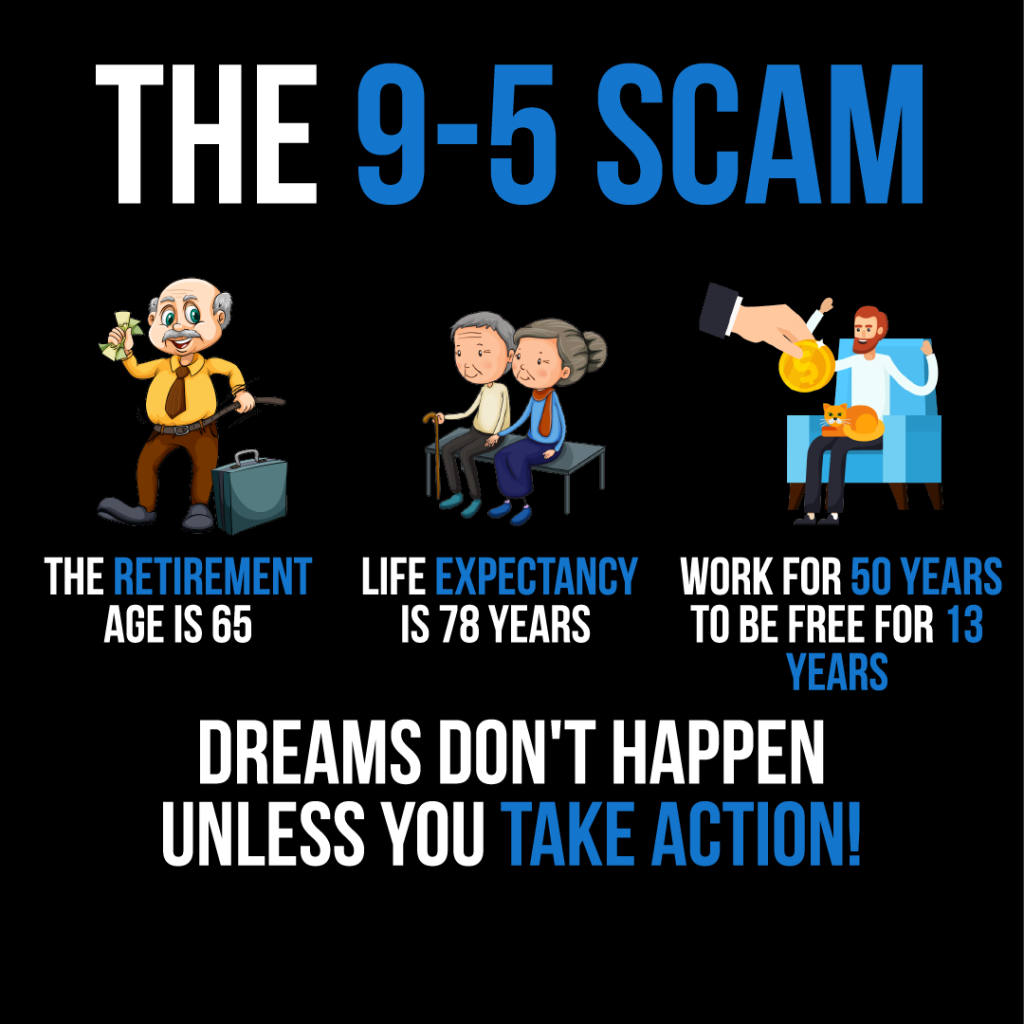

Figure: The infographic titled "The 9-5 Scam" presents a critical view of traditional work life. It points out that with a life expectancy of 78 years and a retirement age of 65, one would work for 50 years only to be free for 13 years. The message "Dreams don't happen unless you take action!" suggests that relying solely on a 9-5 job may not be the most effective path to fulfilling one's dreams. This visual is a call to action for individuals to take proactive steps towards their goals, possibly implying the pursuit of alternative income streams or early retirement strategies. For practical use, users should consider their long-term life and financial goals and explore various ways to achieve them beyond the conventional employment paradigm. Source: Custom Infographic

13.1 Understanding Social Security

تمويل الضمان الاجتماعي: Social Security is funded through payroll taxes collected under the Federal Insurance Contributions Act (FICA). Both employees and employers contribute to this fund, which then provides benefits to retirees, disabled individuals, and survivors of deceased workers. Each paycheck has a deduction (typically 6.2% from the employee and 6.2% from the employer) funding future benefits. Understanding the funding method is crucial because changes in the workforce or tax rates could affect Social Security’s long-term sustainability.

المزايا المقدمة: يوفر الضمان الاجتماعي شبكة أمان للمتقاعدين، حيث يوفر لهم دخلاً شهريًا يعتمد على أرباحهم خلال سنوات عملهم. ويعتمد مبلغ الاستحقاق على سن التقاعد وسجل أرباح الفرد.

ال average Social Security benefit for a retired worker in 2023 is approximately $1,827 per month, but this varies depending on lifetime earnings and the age at which benefits are claimed.

مثال للنشاط:صمم نشرة ترويجية تسلط الضوء على فوائد الضمان الاجتماعي. يمكن أن توضح النشرة كيف أن التقاعد المبكر عند سن 62 قد يؤدي إلى فوائد أقل مقارنة بفوائد سن التقاعد الكامل، وكيف أن تأخير الفوائد حتى سن 70 قد يؤدي إلى زيادة مبلغ الفائدة الشهرية. قم بتضمين صور أو مخططات لعرض الفرق في الفوائد لمستويات الدخل المختلفة.

13.2 Diversifying Retirement Income

مصادر مختلفة للدخل التقاعدي:

الضمان الاجتماعي: يعد هذا المصدر الأساسي للدخل بالنسبة للعديد من المتقاعدين، حيث يوفر لهم فوائد تعتمد على تاريخ أرباحهم.

خطط التقاعد التي يرعاها صاحب العمل: مثل خطط 401(ك) والمعاشات التقاعدية، والتي تعتبر ضرورية لبناء صندوق التقاعد.

الاستثمارات الشخصية: بما في ذلك حسابات التقاعد الفردية والأسهم والسندات وأدوات الاستثمار الأخرى.

استمرار أرباح التوظيف: إن العمل بدوام جزئي أو الاستشارات أثناء التقاعد قد يكون مكملاً للدخل.

Typical sources of retirement income also include annuities, real estate rental income, reverse mortgages, and health savings accounts (HSAs) for medical expenses.

مصادر الدخل المتعددة في التقاعد: Relying on a single source of retirement income, like Social Security may not be sufficient for a comfortable retirement. A diversified income strategy incorporating employer-sponsored plans and personal investments can offer a way to maintain financial security and flexibility during retirement.

خطط التقاعد التي يرعاها صاحب العمل: Participating in these plans is critical, like a 401(k). Many employers offer a match to your contributions, which is essentially free money for your retirement fund. Maximizing your contribution to receive the full employer match can significantly impact your retirement savings. Employees should strive to contribute at least enough to receive the full employer match — otherwise, they are leaving free money on the table.

حسابات التوفير الصحية (HSA) are another valuable tool for retirement planning. HSAs allow tax-free savings for medical expenses in retirement, reducing the financial burden of healthcare costs.

متوسط استحقاقات الضمان الاجتماعي: وفقًا للبيانات الحديثة، يبلغ متوسط استحقاقات الضمان الاجتماعي الشهرية للعمال المتقاعدين حوالي $1,543. ومع ذلك، يختلف هذا المبلغ بناءً على سجل أرباحك والعمر الذي تبدأ فيه تحصيل الاستحقاقات.

شكل: استراتيجيات الادخار للتقاعد

وصف:

توضح الصورة استراتيجيات مختلفة للادخار للتقاعد:

وفر 15% سنويًا: تهدف إلى توفير ما لا يقل عن 15% من دخلك سنويًا.

توفير لأكبر النفقات: إعطاء الأولوية للادخار لتغطية النفقات الكبيرة التي ستحدث أثناء التقاعد.

وفر أكثر من 15% سنويًا: إذا أمكن، قم بتوفير أكثر من 15% الموصى به لبناء صندوق تقاعد أكبر.

تعظيم حسابات التقاعد الخاصة بك: استفد بشكل كامل من حسابات التقاعد مثل 401(k)s وIRAs.

استثمر على المدى الطويل الآن: ركز على الاستثمارات طويلة الأجل لتنمية مدخراتك التقاعدية.

الاستفادة من مساهمات اللحاق بالركب: إذا كان عمرك 50 عامًا أو أكثر، فقم بتقديم مساهمات تعويضية إلى حسابات التقاعد الخاصة بك.

ميزانية التقاعد الطويل: خطط لمدخراتك مع الأخذ في الاعتبار فترة التقاعد الطويلة.

احصل على مساعدة في التخطيط للتقاعد: اطلب المشورة المهنية للتأكد من أنك على الطريق الصحيح نحو تقاعد آمن.

الماخذ الرئيسية:

يعد توفير جزء كبير من دخلك سنويًا أمرًا بالغ الأهمية لتقاعد مريح.

الاستثمار طويل الأجل وتعظيم مساهمات حساب التقاعد يمكن أن يؤدي إلى نمو صندوق التقاعد الخاص بك بشكل كبير.

إن وضع ميزانية للتقاعد الطويل والحصول على مشورة مهنية بشأن التخطيط للتقاعد يمكن أن يساعد في ضمان الأمن المالي أثناء التقاعد.

تطبيق المعلومات:

توفر هذه الاستراتيجيات نهجا منظما نحو الادخار للتقاعد. باتباع هذه الإرشادات، يمكن للأفراد العمل على بناء صندوق تقاعد كبير يدعمهم خلال سنوات تقاعدهم. من الضروري البدء في الادخار والاستثمار مبكرًا، والاستفادة من حسابات التقاعد، والتفكير في طلب المشورة المهنية لضمان تقاعد جيد التخطيط وآمن ماليًا.

13.3 Planning for Retirement

لضمان تقاعد مريح، من الضروري:

ابدأ بالادخار مبكرًا للاستفادة من الفائدة المركبة.

قم بتنويع مصادر دخلك التقاعدي لتقليل المخاطر وزيادة الأمان المالي.

فهم فوائد وقيود الضمان الاجتماعي والتخطيط وفقًا لذلك لتحقيق أقصى استفادة من فوائده.

الاشتراك في خطط التقاعد التي يرعاها صاحب العمل والسعي إلى المساهمة بما يكفي للحصول على المساهمة الكاملة من صاحب العمل.

خذ في الاعتبار الاستثمارات الشخصية وخطط الادخار مثل حسابات التقاعد الفردية لبناء مدخرات تقاعدية إضافية.

Taxable vs Tax-Deferred vs Tax-Advantaged Accounts:

Taxable accounts (like brokerage accounts) do not offer any upfront tax benefits.

Tax-deferred accounts (like Traditional IRAs and 401(k)s) allow contributions to grow tax-free until retirement when withdrawals are taxed as income.

Tax-advantaged accounts (like Roth IRAs) involve paying taxes upfront, but earnings and qualified withdrawals are tax-free.”

Retirement vs Estate Planning:

Retirement planning focuses on ensuring financial independence during retirement by building savings through Social Security, employer plans, and personal investments.

تخطيط العقارات addresses how your assets will be distributed after your death and includes tools like wills, trusts, and beneficiary designations.

13.4 Estate Planning Tools:

الشكل: تمثيل رمزي لمدخرات التقاعد مع بيضة ذهبية موضوعة بشكل آمن، مما يشير إلى أهمية بناء عش مالي بيضة للمستقبل.

سوف: Legal document directing asset distribution after death.

الوصية الحية: Outlines healthcare wishes if incapacitated.

Trust: Allows assets to be managed and distributed without going through probate court.

Annuities and Pensions: Can provide income streams to support heirs. Understanding these tools ensures your wishes are honored and can reduce taxes or legal fees for your heirs

خاتمة

يجب أن يتضمن التخطيط للتقاعد في الولايات المتحدة استراتيجية شاملة تجمع بين الضمان الاجتماعي، والخطط التي ترعاها جهة العمل، والاستثمارات الشخصية، وربما استمرار المكاسب الوظيفية. إن فهم كيفية تمويل الضمان الاجتماعي والفوائد التي يوفرها أمر بالغ الأهمية، وكذلك أهمية تنويع دخل التقاعد لضمان الاستقرار المالي في سنواتك الذهبية.

يساعدك وجود خطة تقاعد مدروسة جيدًا على بناء بيضة عش توفر لك الأمان المالي وراحة البال خلال سنوات التقاعد.

معلومات الدرس الرئيسية:

لوريم إيبسوم دولور سيت أميت، consectetur adipiscing إيليت. Ut elit Tellus، luctus nec ullamcorper mattis، pulvinar dapibus leo.