Lokal: Einführung in Konjunkturzyklen und Anlageklassen

Lernziele der Lektion:

Understand the business cycle: Recognize the phases of expansion, peak, contraction, and recession, and how they influence investment decisions.

Identify different asset classes: Erfahren Sie mehr über stocks, bonds, real estate, Und Rohstoffe, and their performance across business cycle stages.

Apply diversification strategies: Grasp the importance of diversifying investments across different asset classes to mitigate risks and enhance portfolio resilience.

Interpret sector performance: Analyze how different sectors like technology, real estate, Und financials perform during various phases of the business cycle.

Utilize economic indicators: Utilize figures and data to understand sector behavior and Wirtschaftsindikatoren over decades, aiding in strategic investment planning.

6.5.1 Introduction to Business Cycles and Asset Classes

Der Konjunkturzyklus in Europe, like elsewhere, goes through phases of Erweiterung, Gipfel, Kontraktion, Und recession. Different asset classes—Aktien, Anleihen, Immobilie, Und Rohstoffe—perform differently across these stages, driven by factors such as ECB policies, Zinssätze, Und economic growth. Understanding these phases is crucial for European investors who want to optimize their portfolios based on where the economy is in the cycle.

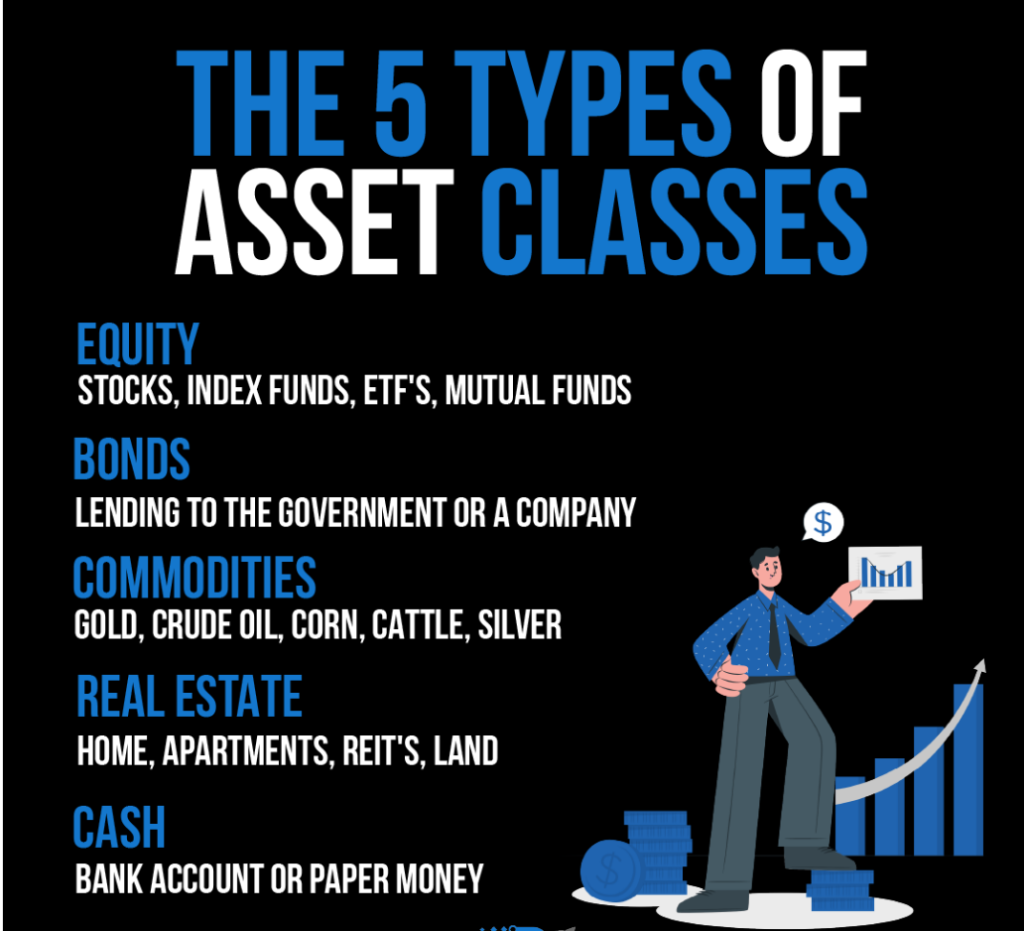

Figure: The infographic provides a clear breakdown of the five primary types of asset classes. It categorizes them into Equity, Bonds, Commodities, Real Estate, and Cash. Each category is further elaborated with examples. For instance, under Equity, it lists stocks, index funds, ETFs, and mutual funds. This visual guide is essential for beginners in finance and investment to understand the diverse avenues available for investment. Advice: When considering investments, it's crucial to diversify across different asset classes to mitigate risks. Each asset class has its own set of advantages and potential risks, so understanding them can help in making informed investment decisions. Source: Custom Infographic

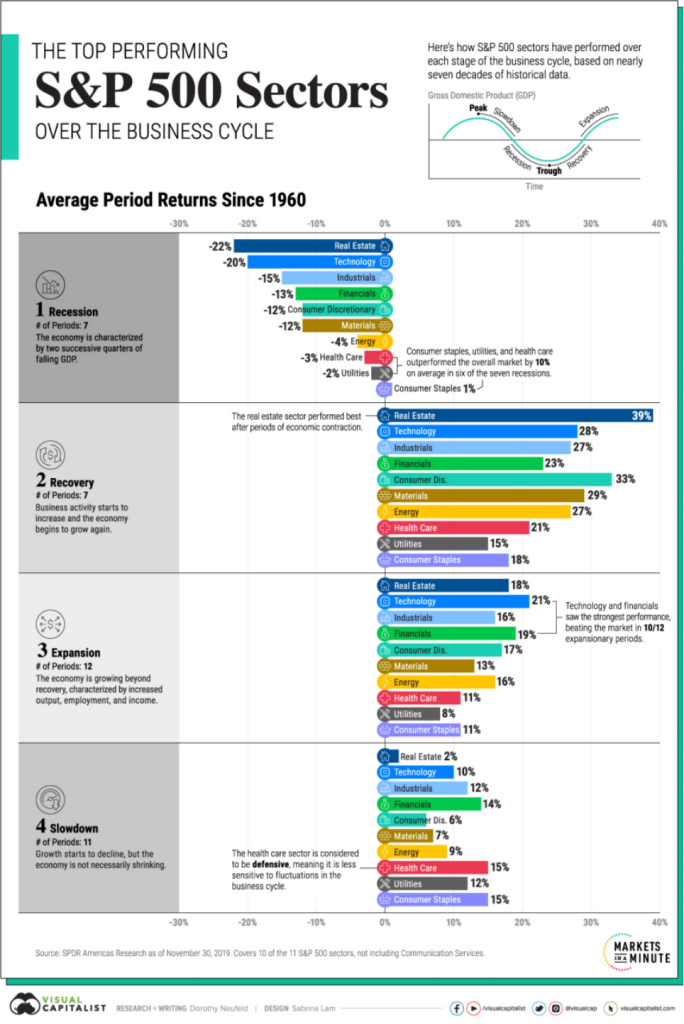

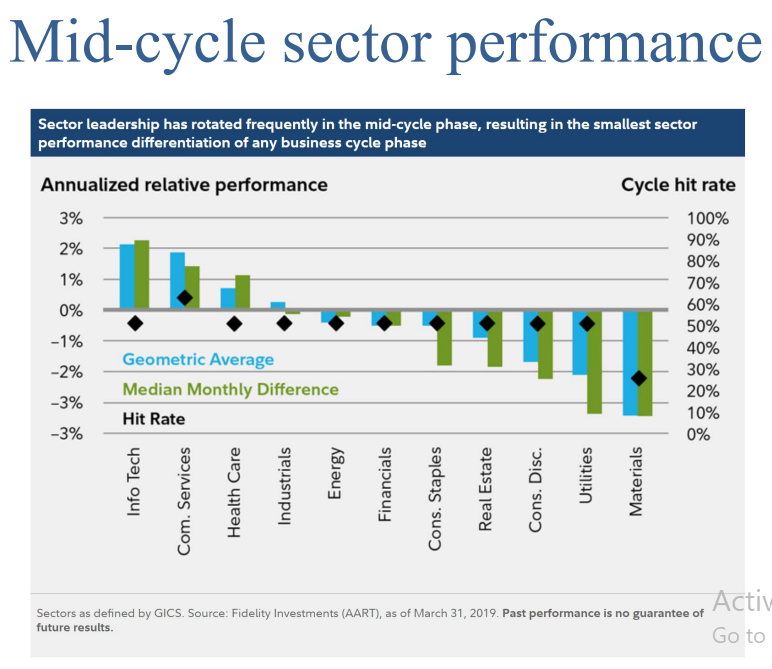

Figur: Wertentwicklung der S&P 500-Sektoren im Konjunkturzyklus

Beschreibung:

The figure shows the average period returns of S&P 500 sectors over different phases of the business cycle since 1960, including Recession, Recovery, Expansion, Und Slowdown. Each phase highlights how sectors perform during distinct economic conditions. For example, Immobilie performs best during recovery, während Technologie Und Financials excel during Erweiterung. The figure provides insights into sector behavior across seven decades, helping users understand which sectors may outperform in specific economic phases.

Wichtige Erkenntnisse:

Immobilie generally outperforms during recovery, with an average return of 39%.

Technologie Und Financials lead during Erweiterung, with returns of 28% and 23%, respectively.

During slowdowns, Health Care is considered a defensive sector, offering more stable returns.

Consumer Staples, Versorgungsunternehmen, Und Health Care outperform during recessions, being less sensitive to economic downturns.

Anwendung der Informationen:

Investors can use this data to optimize portfolio allocations based on expected economic phases. By identifying which sectors perform best during specific economic cycles, investors can strategically adjust their sector exposure to enhance returns and manage risks. Understanding sector performance across cycles can also help with Diversifizierung and improve decision-making during market volatility.

6.5.2 Stocks, Bonds, and Cash: A Primer

Aktien: European stocks tend to perform well during periods of expansion when corporate earnings are rising. Sectors such as automotive, pharmaceuticals, Und financial services benefit most from GDP growth and increased consumer spending.

Anleihen: European bonds, particularly sovereign bonds wie German Bunds, are viewed as safe investments, especially during the contraction phase when interest rates are low. Corporate bonds from large European companies also perform well in early expansion phases.

Cash: Cash and equivalents, such as short-term government bonds oder money market funds, are typically favored in recessionary periods as they provide liquidity and protection against volatility.

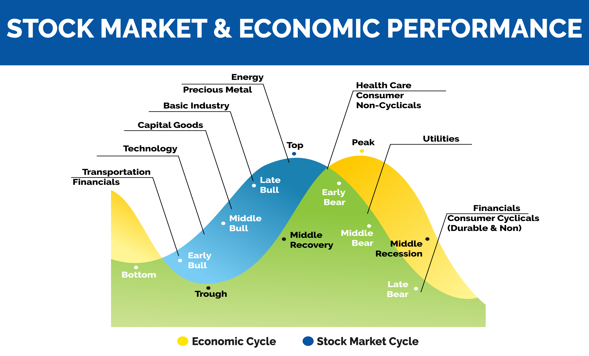

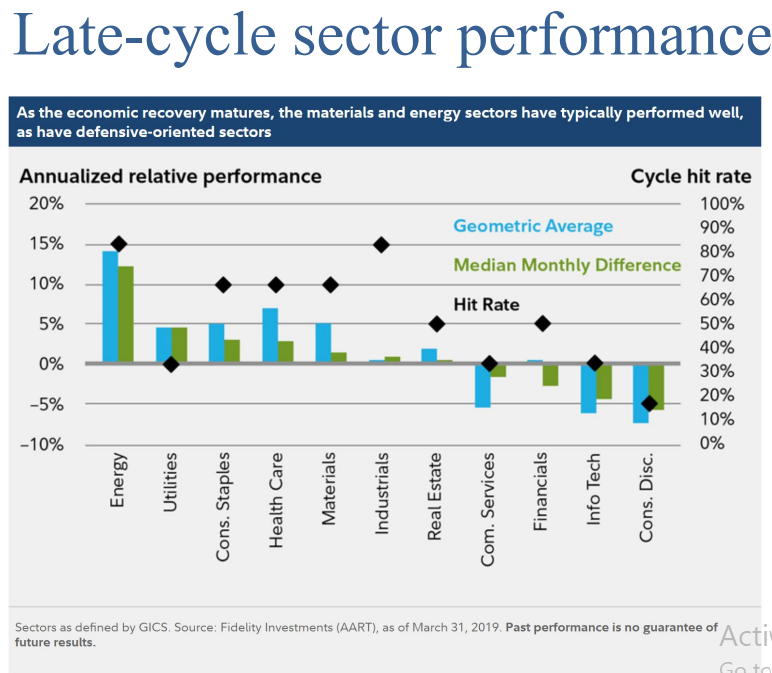

Figure: Stock Market & Economic Performance

Beschreibung:

The figure illustrates the relationship between the economic cycle und die stock market cycle. It depicts the different stages of each cycle, including phases like Early Bull, Middle Bull, Late Bull, Early Bear, Und Middle Recession. Key sectors such as Energie, Versorgungsunternehmen, Und Health Care are aligned with specific phases, indicating their performance during economic transitions.

Wichtige Erkenntnisse:

Der economic cycle Und stock market cycle have distinct but interconnected phases.

Sectors like Transport Und Financials perform well in the early bull phase, while Versorgungsunternehmen excel at the Gipfel.

Basic industries Und capital goods perform better in the middle bull phase, aligning with economic recovery.

Precious metals Und energy typically peak during the late bull phase.

Health Care Und Consumer Non-Cyclicals offer stability during recessions.

Anwendung der Informationen:

Understanding the correlation between the economic cycle Und stock market performance can help investors make informed decisions about sector allocation based on economic phases. By aligning investments with phases like recovery oder recession, users can optimize returns and manage risk effectively. This approach aids in strategic portfolio diversification across economic conditions.

6.5.3 Early Expansion Phase

During the early expansion phase in Europe, economic recovery begins with rising GDP, low interest rates, and growing investor confidence.

Aktien: European stocks, particularly in sectors like consumer discretionary Und technology, tend to perform well as the economy rebounds.

Anleihen: High-yield corporate bonds are attractive as companies recover and their credit risk decreases.

Cash: Cash is less attractive during this phase as investors seek higher returns in riskier asset classes.

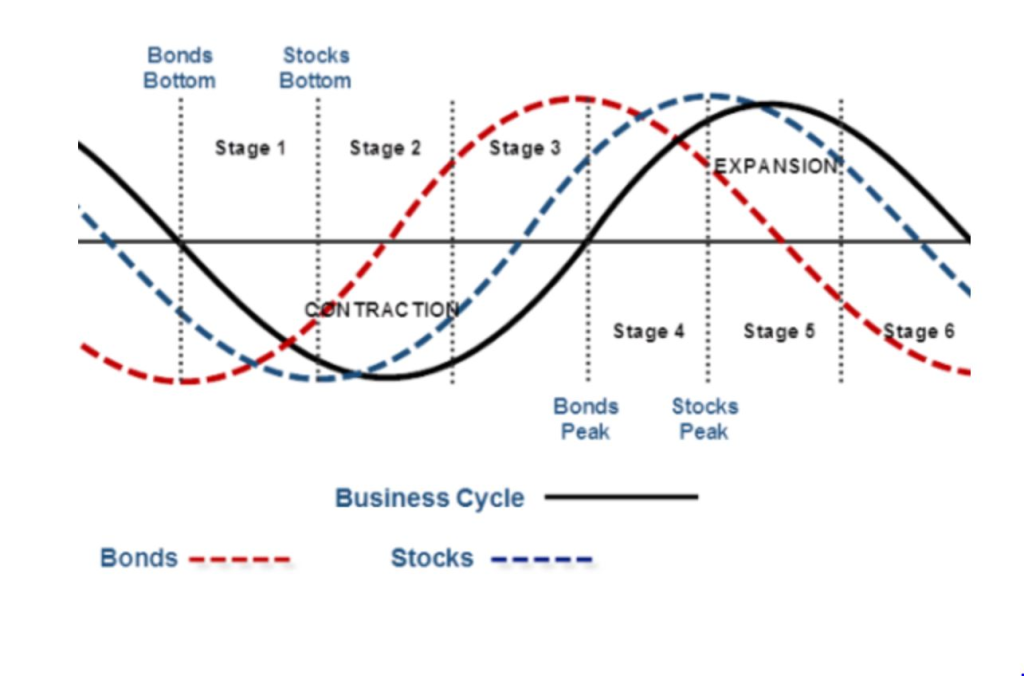

Figur: Business Cycle and Market Phases

Beschreibung:

The figure shows the relationship between the business cycle and the performance of bonds and stocks over six distinct stages. It demonstrates that Anleihen tend to perform well during early stages of economic contraction, reaching their lowest point earlier than stocks. As the business cycle progresses towards economic expansion, stocks begin to recover and outperform bonds, peaking at later stages of the expansion.

Wichtige Erkenntnisse:

Anleihen generally perform well during the early contraction phase of the business cycle, peaking sooner than stocks.

Aktien tend to bottom out after bonds and excel during the later expansion phase.

The cycle demonstrates distinct stages where different asset classes show stronger performance.

Understanding the timing of bonds’ and stocks’ peaks and bottoms can be crucial for effective portfolio management.

Anwendung der Informationen:

Investors can use this information to align their Anlagestrategien with the business cycle, focusing more on Anleihen during contraction and shifting towards Aktien as the economy expands. This helps optimize returns by timing Vermögensallokation according to the specific phases of the business cycle.

6.5.4 Mid Expansion Phase

Der mid expansion phase in Europe brings stable growth and moderate inflation.

Aktien: Sectors such as financial services Und industrial goods perform strongly.

Anleihen: Corporate bonds remain attractive, but rising interest rates make government bonds less appealing.

Cash: Cash is still not a favored option, though it may be used by investors seeking to hedge against future volatility.

Figur:

Beschreibung:

Wichtige Erkenntnisse:

Anwendung der Informationen:

6.5.5 Late Expansion Phase

In the late expansion phase in Europe, the economy begins to overheat, with rising inflation and tightening labor markets.

Aktien: Defensive sectors like utilities Und healthcare start to outperform.

Anleihen: Government bonds become attractive again as investors seek safety amid rising interest rates.

Cash: Cash becomes a more attractive asset class as the economy nears a potential downturn.

Figur:

Beschreibung:

Wichtige Erkenntnisse:

Anwendung der Informationen:

6.5.6 Recession

During a recession in Europe, economic activity contracts, and unemployment rises.

Aktien: European stocks typically suffer significant losses, with cyclical sectors such as automotive Und consumer discretionary being the hardest hit.

Anleihen: Government bonds, especially from stable economies like Germany, outperform as investors seek safety.

Cash: Cash becomes the safest investment as market volatility increases.

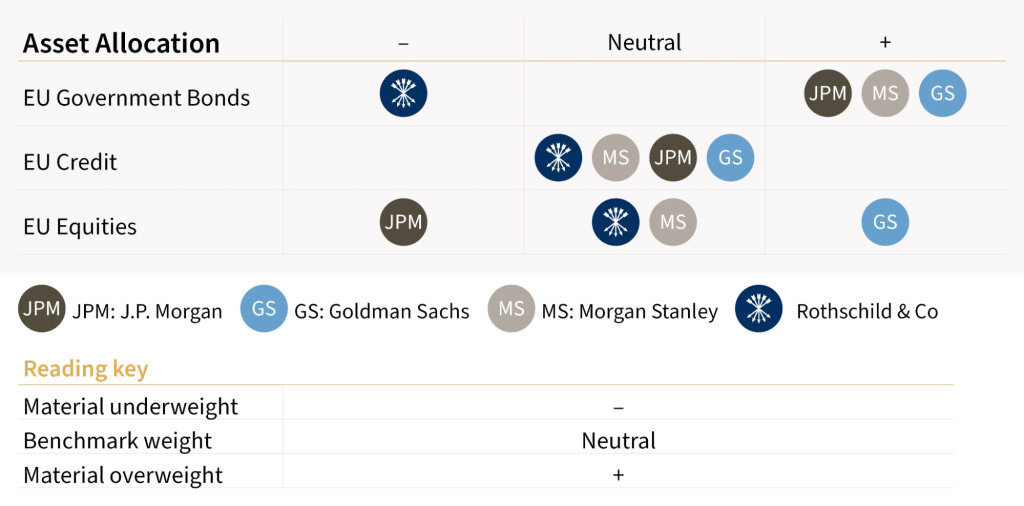

Figur: Asset Allocation by Major BanksAsset Allocation by Major Banks

Beschreibung:

This figure presents the asset allocation preferences of four major banks—J.P. Morgan (JPM), Goldman Sachs (GS), Morgan Stanley (MS), Und Rothschild & Co.—across three categories: EU Government Bonds, EU Credit, Und EU Equities. The positions are classified as material underweight (-), benchmark weight (neutral), oder material overweight (+), indicating each bank’s level of exposure or preference for these assets.

Wichtige Erkenntnisse:

J.P. Morgan is materially overweight on EU Equities while being neutral on EU Government Bonds Und EU Credit.

Goldman Sachs shows a more balanced approach, favoring EU Credit Und EU Equities as overweight positions while remaining neutral on EU Government Bonds.

Morgan Stanley maintains a neutral position on EU Government Bonds Und EU Credit, with a slight overweight in EU Equities.

Rothschild & Co. adopts a material underweight stance in EU Government Bonds but a neutral stance on both EU Credit Und EU Equities.

Anwendung der Informationen:

Investors can use this information to understand the asset allocation preferences of major banks, which can guide their own Anlagestrategien. By observing how financial institutions position themselves in different asset classes, investors can make informed decisions about portfolio diversification and potential market opportunities.

6.5.7 Real Estate and Commodities: An Overview

Immobilie: Real estate in Europe is influenced by local economic conditions, particularly interest rates and consumer demand. During expansion phases, commercial Und residential real estate tends to perform well, while in recessions, property values may decline.

Rohstoffe: Commodities like oil Und natural gas are key to Europe’s energy sector. Rising Rohstoffpreise benefit energy-exporting countries during the late expansion phase, while gold performs well during recessions as a safe-haven asset.

Figur: Gold vs. a Single-Family Home

Beschreibung:

The figure compares the year-over-year percentage difference in value between gold Und single-family homes from 2011 to 2019. It shows annual changes for each asset, with gold depicted in yellow and housing in blue. For five out of these nine years, single-family homes exhibited a higher percentage increase in value than gold. Notable differences include 2011, where gold increased significantly by 23.5%, and 2013, where it dropped by -18.1%.

Wichtige Erkenntnisse:

Gold had a significant spike in 2011, while housing showed more stable growth over the period.

Einfamilienhäuser outperformed gold in terms of annual percentage increase for five of the nine years.

In 2013, gold experienced its largest decline, contrasting with a modest increase in housing.

Der housing market showed consistent growth from 2012 to 2019, suggesting more stable returns compared to gold.

Anwendung der Informationen:

Investors can use this comparison to understand the relative stability of the housing market compared to gold, which can be more volatile. This data helps in deciding asset allocation, suggesting that Immobilie may offer more consistent returns over time, while gold can act as a hedge during economic downturns.

6.5.8 Real Estate Across Business Cycle Stages

Early Expansion: Real estate begins to recover, with increased demand for housing and commercial properties.

Mid Expansion: Real estate thrives, with strong growth in both residential and commercial sectors.

Late Expansion: Rising interest rates slow real estate growth, particularly in over-leveraged markets.

Recession: Real estate values typically decline due to reduced demand and tighter credit conditions.

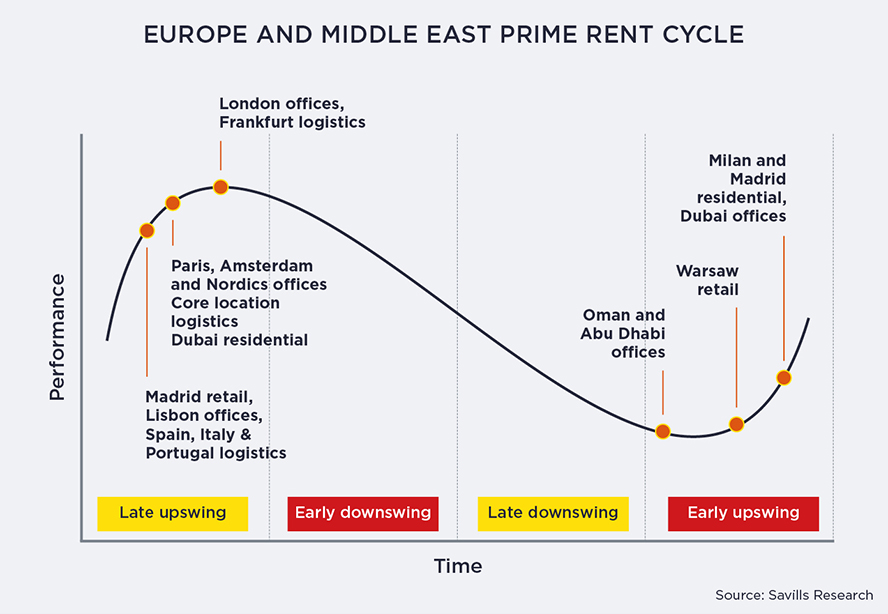

Figur: Europe and Middle East Prime Rent Cycle

Beschreibung:

The figure illustrates the prime rent cycle across various markets in Europe and the Middle East, highlighting different phases of performance over time. The cycle is divided into four stages: late upswing, early downswing, late downswing, Und early upswing. It showcases how prime rents in cities like London, Frankfurt, Paris, Amsterdam, and Warsaw evolve through these stages, with certain markets peaking during the upswing and others declining during the downswing.

Wichtige Erkenntnisse:

London offices Und Frankfurt logistics are at the peak of the late upswing phase.

Paris, Amsterdam, Und Dubai residential enter the early downswing phase, indicating declining prime rents.

Madrid retail Und Lisbon offices reach the late downswing phase, representing lower performance.

Markets like Warsaw retail Und Milan residential start to enter the early upswing, signaling potential recovery in prime rents.

Anwendung der Informationen:

Verstehen der prime rent cycle ist entscheidend für Immobilieninvestoren, as it helps identify the best entry and exit points in different markets. This knowledge can guide investment strategies, highlighting when to focus on growth markets during the early upswing or consider divestment during the downswing Phasen.

6.5.9 Commodities Across Business Cycle Stages

Early Expansion: Commodities like industrial metals recover as production ramps up.

Mid Expansion: Commodities, particularly energy Und agriculture, perform well as consumption increases.

Late Expansion: Gold becomes attractive as an inflation hedge.

Recession: Commodities like oil decline due to reduced demand, but gold performs well as a safe-haven asset.

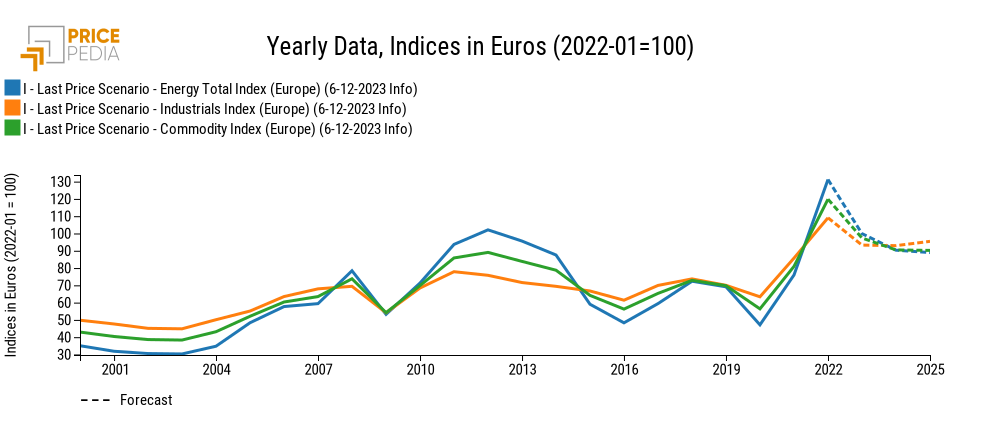

Figur: Yearly Data, Indices in Euros (2022-01=100)

Beschreibung:

The figure displays the yearly trends of three indices in Europe from 2000 to 2025, including the Energy Total Index, Industrials Index, Und Commodity Index. Each index starts from a base value of 100 in January 2022, reflecting how the indices have fluctuated over time. The forecast section, represented by dashed lines, shows the projected movement of these indices up to 2025.

Wichtige Erkenntnisse:

Der Energy Total Index has shown the highest volatility over time compared to the other indices.

There was a noticeable dip across all indices around 2009, coinciding with the global financial crisis.

The forecast indicates a gradual decline in all three indices, reflecting an anticipated economic slowdown in 2024 and 2025.

Der Industrials Index remains relatively stable compared to energy and commodity indices over the observed period.

Anwendung der Informationen:

This data helps investors understand the historical and projected price trends in energy, industrials, and commodities sectors in Europe. Investors can use this information to adjust their Anlagestrategien, anticipate potential risks, and make informed decisions regarding sector-specific allocations, especially considering projected declines.

Wichtige Unterrichtsinformationen:

Business cycles dictate asset performance: Asset classes such as real estate, technology, Und financials have distinct performances tied to economic phases like recovery Und Erweiterung.

Diversification is key: By diversifying across asset classes, investors can reduce risks and take advantage of growth opportunities in different economic conditions.

Sector-specific insights are valuable: Understanding which sectors outperform during specific business cycle phases can lead to more informed investment strategies.

Economic indicators are essential tools: Utilizing economic indicators and sector performance data helps in anticipating market conditions and aligning investments accordingly.

Strategic planning enhances returns: Aligning investment strategies with the Konjunkturzyklus phases facilitates better Risikomanagement and potential for higher returns.

Schlusserklärung

Mastering the dynamics of the business cycle and its impact on different asset classes equips investors with the knowledge to make informed, strategic decisions that optimize returns and manage risks effectively.