Lokal: Anlagekonzepte und Risikomanagement verstehen

Lernziele der Lektion:

Einführung:

This section focuses on building an understanding of fundamental investment concepts and the importance of risk management. By exploring different types of investments, liquidity, and the impact of external factors, learners will be better equipped to make informed financial decisions and achieve long-term goals.

- Understand the Difference Between Saving and Investing: Learn how saving preserves capital for short-term needs, while investing aims to grow wealth over time through different asset classes, like stocks and bonds. This knowledge helps you decide when to save and when to invest based on your financial goals.

- Distinguish Between Debt and Equity Investments: Gain insight into how debt investments (e.g., bonds) involve lending money for interest returns, while equity investments (e.g., stocks) represent ownership with potential for higher returns but more risk. This distinction guides better investment choices according to your risk tolerance and expected returns.

- Learn the Impact of Liquidity and Investment Value Fluctuations: Discover how liquidity affects the ease of converting investments into cash without losing value, and how market changes can lead to unrealized or realized gains and losses. This helps you evaluate investments based on accessibility and stability.

- Explore the Role of Fees and External Factors in Investment Performance: Understand how fees, inflation, interest rates, and exchange rates impact returns. This knowledge helps you manage costs and adapt strategies according to economic conditions.

- Recognize the Importance of Diversification and Sustainable Investing: Understand how spreading investments across different asset classes reduces risk, while sustainable investing aligns financial choices with ethical values. This promotes both financial growth and responsible investing.

Einführung

Investing is an essential component of long-term financial planning, offering opportunities to grow wealth and achieve financial goals. However, investing carries risks that must be understood and managed carefully. This chapter introduces fundamental investment concepts, such as the difference between saving and investing, the risks and rewards of different investment types, and the importance of diversification. It also covers key considerations like liquidity, fees, and external factors that affect investments. By understanding the principles of risk tolerance, investment horizons, and sustainable investing, individuals can make informed decisions that align with their financial goals and risk appetite.

Difference Between Saving and Investing, and Debt vs. Equity

It’s important to distinguish between saving Und Investieren. Saving typically involves placing money in a low-risk account, such as a savings account, with the goal of preserving capital while earning modest interest. Investing, on the other hand, involves purchasing assets (such as stocks or bonds) with the potential for higher returns, but with greater risk.

Understanding the difference between debt Und equity is also crucial. Debt investments, like bonds, involve lending money to an entity that promises to repay with interest. Eigenkapital investments, like stocks, represent ownership in a company and offer potential returns through dividends and capital appreciation. Equity investments tend to carry more risk but can also offer higher returns than debt investments.

:max_bytes(150000):strip_icc():format(webp)/TheDifferencesBetweenSavingandInvesting-bc50bd28537e4fb7b2d696047bee33eb.jpg)

Figure: The Differences Between Saving and Investing

Beschreibung:

The figure outlines key differences between saving and investing. Saving involves setting aside money in safe and liquid accounts, such as checking accounts, savings accounts, U.S. Treasury bills, and money market accounts. Investing, on the other hand, is about allocating capital to assets like stocks, bonds, and real estate with the goal of earning returns. While saving ensures funds are readily available, investing aims to increase capital over time.

Wichtige Erkenntnisse:

- Saving is about keeping money in safe, liquid accounts to ensure it is easily accessible.

- Investing involves purchasing assets with the potential for growth, such as stocks, bonds, or real estate.

- Sparkonten are typically used for short-term needs, while Investitionen focus on long-term gains.

- Risk levels differ, with saving being low-risk and investing carrying higher risk but offering higher potential returns.

Anwendung der Informationen:

Understanding the differences between saving and investing is crucial for personal finance planning. Saving is ideal for Notfallfonds or short-term goals, while investing can help grow wealth over time for long-term objectives like retirement. Knowing when to save and when to invest allows individuals to balance risk and return effectively.

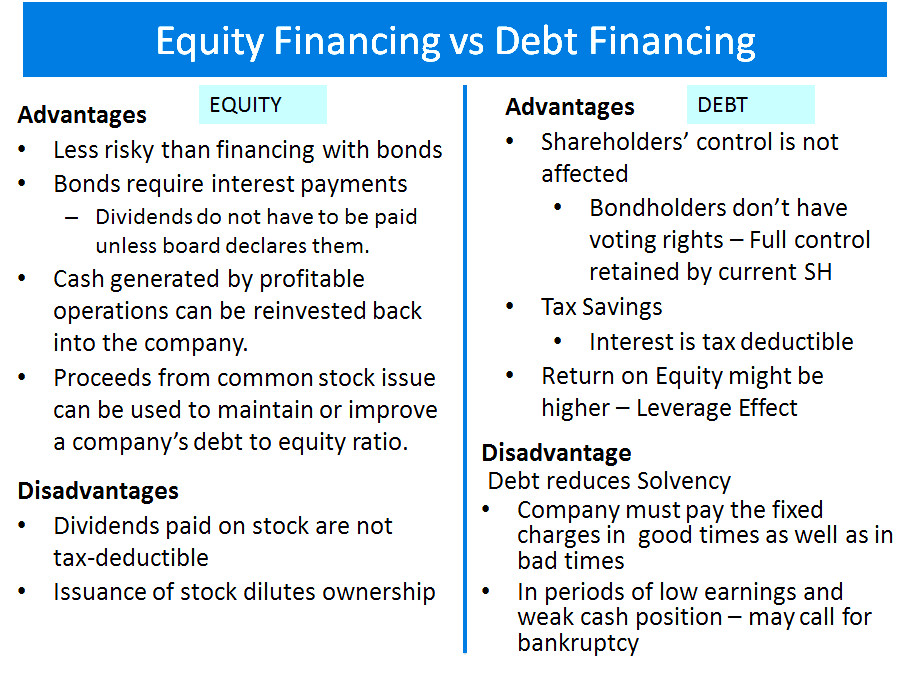

Figur: Equity Financing vs Debt Financing

Beschreibung:

The figure compares the advantages and disadvantages of equity financing Und debt financing. Equity financing involves issuing stock, which does not require regular payments but can dilute ownership. Debt financing, on the other hand, allows companies to retain full control, as creditors do not get voting rights. However, it requires regular interest payments, which are tax-deductible, making it beneficial for reducing taxable income.

Wichtige Erkenntnisse:

- Equity financing avoids regular payment obligations but may dilute ownership.

- Debt financing allows the retention of control but requires regular interest payments.

- Tax benefits from debt interest can make debt financing attractive despite repayment risks.

- Eigenkapital is less risky for the company’s cash flow as it does not involve fixed repayment schedules.

Anwendung der Informationen:

die Unterschiede verstehen zwischen equity and debt financing helps businesses decide how to raise funds. Eigenkapital might be better for companies looking to avoid fixed payments, while debt could be suitable for those needing to preserve ownership and leverage tax benefits. Investors can also use this knowledge to understand a company’s financial strategy and stability.

Liquidity and Investment Value Fluctuations

Not all investments are equally liquid, meaning they can’t all be converted to cash quickly without losing value. For instance, Aktien are generally more liquid than real estate, as they can be sold quickly in the stock market, while selling a property may take weeks or months.

Der value of an investment can fluctuate due to market conditions, economic changes, or company performance. Aktien, for example, may rise or fall based on market trends, while Anleihen are affected by Änderungen des Zinssatzes. Investors should be prepared for both unrealized gains and losses—which are paper gains or losses before selling—and realized gains and losses that occur when an investment is sold.

Example: A person who buys shares of a company at €50 per share may experience an unrealized gain if the share price rises to €60 but realizes this gain only upon selling the shares.

Impact of Fees, Charges, and External Factors on Investments

Investments often come with fees and charges that can significantly affect returns. These include one-time fees like trading commissions and ongoing fees like management fees for mutual funds or ETFs. These fees reduce the overall performance of an investment and must be carefully considered before making decisions.

External factors like Inflation, Zinssätze, Und Wechselkurse can also affect the long-term performance of investments. For example, rising inflation can erode the real value of returns, while changes in exchange rates can affect investments in foreign assets. Understanding these influences is key to making informed investment decisions.

Risk Tolerance, Investment Horizon, and Diversification

One of the most fundamental concepts in investing is risk tolerance—the amount of risk an investor is willing to take in exchange for potential rewards. Investment horizon refers to the amount of time an investor expects to hold an investment before needing the funds, with longer horizons allowing for more risk.

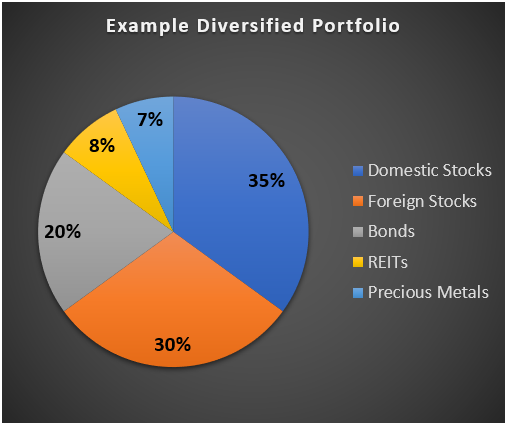

Investors should also be aware of the importance of Diversifizierung—spreading investments across different asset classes (such as stocks, bonds, and real estate) to reduce risk. A diversified portfolio is less likely to suffer significant losses because different asset classes may perform differently under various market conditions.

Example: An investor in France may create a diversified portfolio that includes French government bonds, European stocks, and real estate. By doing so, they reduce the risk associated with putting all their money into one asset class.

Figur: Example Diversified Portfolio

Beschreibung:

The figure illustrates a diversified investment portfolio, dividing assets into five categories: Domestic Stocks (35%), Foreign Stocks (30%), Bonds (20%), REITs (8%), Und Precious Metals (7%). Each segment of the pie chart represents the percentage of the portfolio allocated to each asset class, showing how diversification can spread investment risk across different sectors.

Wichtige Erkenntnisse:

- Diversifizierung involves spreading investments across various asset classes.

- Domestic and foreign stocks make up the largest portions, showing a focus on equities.

- Anleihen provide stability, accounting for 20% of the portfolio.

- REITs Und precious metals add further diversification, reducing overall risk.

- A well-diversified portfolio can mitigate risks associated with market volatility.

Anwendung der Informationen:

Investors can use this data to understand how to balance risk by allocating funds across different types of assets. This approach helps in reducing the impact of any single investment’s poor performance, thus preserving overall portfolio value. Diversification is crucial for long-term stability in an investment strategy.

Sustainable Investing and ESG Factors

In recent years, there has been a growing interest in sustainable investing, where investors consider Environmental, Social, and Governance (ESG) factors when selecting investment products. ESG investing involves choosing companies that meet certain criteria for environmental sustainability, social responsibility, and corporate governance. Investors may also choose to divest from sectors or companies that do not align with their values, such as fossil fuels or tobacco, or to engage with companies to encourage better practices.

In the Eurozone, many sustainable investment products are available, and these products often have ESG ratings or labels that indicate how well they align with sustainability goals. For example, a mutual fund might have an ESG rating based on the sustainability of the companies it invests in.

Figure: VP Bank Sustainability Approach

Beschreibung:

The figure illustrates VP Bank’s sustainability investment strategy, dividing it into three categories: VP Bank Standard, Sustainable Plus, Und Philanthropy. It highlights the criteria used for ESG (Environmental, Social, and Governance) ratings, assessments of business practices, and alignment with UN goals. The Sustainable Plus category includes thematic and impact investments, with a focus on generating positive social and environmental outcomes. Philanthropy emphasizes creating positive impacts without expecting financial returns.

Wichtige Erkenntnisse:

- ESG ratings are essential for evaluating sustainability, with standards ensuring minimal environmental impact.

- Business practices assessment ensures no undesirable activities and promotes responsible business.

- Sustainable Plus investments focus on specific themes, such as demographics and the environment, while impact investments target measurable positive outcomes.

- Philanthropy focuses on generating social good without financial gains.

- Alignment with UN Sustainable Development Goals (SDGs) is a key aspect of the approach.

Anwendung der Informationen:

Investors can use this approach to understand how to make sustainable and responsible investment decisions. By incorporating thematic and impact investments, they can align their portfolios with global sustainability goals. This helps in not only gaining returns but also contributing to positive environmental and social impacts.

Managing Emotional and Cognitive Biases in Investing

Human emotions and cognitive biases can greatly affect investment decisions. For instance, fear of missing out (FOMO) can lead investors to chase trends or invest in overvalued assets, while loss aversion can cause them to sell investments prematurely during market downturns. Being aware of these biases is important in maintaining a rational, long-term investment strategy.

Investors must take steps to control their emotional responses and rely on informed decision-making, rather than letting emotions drive their actions. This can be done through regular monitoring of the market, sticking to an investment plan, and avoiding decisions based solely on short-term market fluctuations or media hype.

Example: During a market downturn, an investor might be tempted to sell off stocks to avoid further losses, but holding onto these investments could lead to greater gains in the future when the market recovers.

Figur: Cognitive Biases in Investment Decisions

Beschreibung:

The figure lists common cognitive biases that affect investment decisions, including Overconfidence Bias, Bestätigungsfehler, Anchoring Bias, Verlustaversion, Und Herdenmentalität. Each bias is defined, showing how it impacts investment behaviors and decisions. The figure also provides mitigation strategies for each bias, helping investors make more rational and informed choices.

Wichtige Erkenntnisse:

- Overconfidence Bias leads to excessive trading and unnecessary risk-taking. Mitigation involves acknowledging the limits of knowledge.

- Bestätigungsfehler can cause poor investment decisions by ignoring contradictory evidence. Seek diverse perspectives to counter this.

- Anchoring Bias results in reliance on initial information, ignoring new data. Focus on a broad range of information to avoid this.

- Verlustaversion leads to overly conservative strategies, missing potential opportunities. Adopting a long-term view can help.

- Herdenmentalität involves following crowd behavior, which can result in market bubbles or crashes. Develop a strategy based on individual financial goals.

Anwendung der Informationen:

diese verstehen cognitive biases helps investors make more informed and rational decisions. By recognizing and countering biases, investors can avoid common pitfalls, maintain a balanced approach, and achieve long-term investment goals.

Crypto-Assets and Emerging Technologies

The rise of crypto-assets like Bitcoin and Ethereum has introduced new investment opportunities, but also higher risks due to their volatility and the lack of regulation. Investors must understand the risks associated with using crypto-assets for payment or investment purposes, and the technological or regulatory issues that can affect the performance of these assets.

In the Eurozone and globally, there have been increasing instances of scams related to crypto-assets, often promising high returns to attract potential victims. Investors must be aware of these risks and take steps to ensure that they use trusted platforms for any crypto transactions.

Insurance and Financial Safety Nets

In addition to investing, building a financial safety net through rainy day savings and insurance is essential to managing risk. A safety net provides protection in case of unexpected expenses, such as medical emergencies, job loss, or car repairs. The goal is to save enough to cover at least three months of living expenses.

Additionally, insurance products such as life insurance, health insurance, Und property insurance help protect against high-cost, low-probability events that could otherwise deplete savings or investments. Understanding which insurance products are necessary and how they complement a long-term investment strategy is key to overall financial security.

Example: A person in Italy might save three months of income in a high-yield savings account for emergencies, while also purchasing health insurance to cover potential medical costs.

Figure: Building a Financial Safety Net

Beschreibung:

The figure illustrates five key steps to creating a financial safety net: setting up an emergency fund, automating savings, diversifying income streams, obtaining insurance coverage, Und reducing unnecessary expenses. Each step is essential to building financial security, providing strategies to manage unexpected costs and financial challenges effectively.

Wichtige Erkenntnisse:

- Setting up an emergency fund ensures that unexpected expenses can be covered without stress.

- Automating your savings helps in consistently building a financial cushion.

- Diversifying income streams provides additional security in case one source of income is disrupted.

- Insurance coverage protects against significant financial risks and uncertainties.

- Reducing unnecessary expenses allows more funds to be allocated to savings and investments.

Anwendung der Informationen:

Understanding these strategies allows users to create a reliable financial safety net, preparing them for emergencies and unforeseen expenses. This approach encourages consistent saving habits, financial planning, and strategic spending, which are essential for achieving long-term financial stability.

Wichtige Unterrichtsinformationen:

Schlusserklärung:

Understanding investment concepts and risk management lays the foundation for successful financial planning. This section covers key principles like saving vs. investing, liquidity, and diversification, all of which help in making informed decisions that align with personal goals and risk preferences.

- Saving vs. Investing: Saving focuses on safety and liquidity, making it suitable for short-term needs, while investing targets long-term growth with higher risk. Knowing when to save and when to invest is essential for effective financial planning.

- Debt vs. Equity Investments: Debt investments provide steady interest income, while equity investments offer ownership and potential for higher returns but come with more risk. This distinction helps tailor your portfolio according to risk tolerance and goals.

- Liquidity and Value Fluctuations: Not all investments can be quickly converted to cash without a loss in value. Be prepared for both unrealized and realized gains or losses, especially with assets like stocks or real estate that fluctuate with market conditions.

- Fees, Inflation, and External Factors: High fees reduce investment returns, while inflation and interest rate changes can alter the real value of gains. Keeping these factors in mind helps manage investment costs and adapt strategies to changing economic conditions.

- Diversification and Sustainable Investing: Spreading investments across asset classes minimizes risk, while sustainable investing allows you to support ethical causes alongside financial growth. This approach builds a balanced, responsible portfolio for long-term success.