Local: analyzing European companies

Στόχοι Μαθήματος:

- Learn about the income statement under IFRS. You will understand how revenues, έξοδα, και net income are reported, along with the inclusion of other comprehensive income (OCI). This helps investors assess a company’s profitability and financial performance.

- Understand the balance sheet under IFRS. The balance sheet provides a snapshot of a company’s assets, liabilities, και equity, offering insights into the company’s financial position. Learn about the distinctions between current and non-current items and how they reflect a company’s liquidity and solvency.

- Explore the cash flow statement under IFRS. The cash flow statement outlines how cash is generated and used across operating, investing, και financing activities. You will learn how this statement helps assess a company’s liquidity and its ability to generate cash to fund operations and investments.

- Gain insights into the overall structure and application of IFRS in European financial reporting. Understanding IFRS helps ensure transparency and comparability, making it easier to analyze financial statements and make informed investment decisions across borders.

Εισαγωγή

Understanding the core financial concepts is essential for any investor. Financial statements provide critical insights into a company’s financial health and performance, helping investors evaluate profitability, liquidity, and growth potential. This section will introduce the fundamental financial statements—κατάσταση αποτελεσμάτων, ισολογισμός, και cash flow statement—and explain how to analyze these documents. We will also discuss key financial data points that investors use to assess a company’s performance.

22.1 Financial Statements

When analyzing European companies, it’s essential to understand that their financial statements are typically prepared according to the International Financial Reporting Standards (IFRS), a global accounting framework that ensures transparency and comparability across borders. In Europe, IFRS is mandatory for all publicly listed companies, providing investors with consistent and clear financial information. This section introduces how financial statements in Europe adhere to IFRS, ensuring high-quality reporting.

IFRS and Income Statement

Under IFRS, the κατάσταση αποτελεσμάτων (also called the statement of comprehensive income) follows a structured approach, similar to financial statements globally, but with some unique European nuances. The income statement provides detailed insight into a company’s revenues, costs, and overall profitability.

- Revenue Recognition: Under IFRS, revenue is recognized when control of a product or service is transferred to the customer. European companies must adhere to these rules, ensuring that revenues are reported accurately based on performance obligations, not just when payments are received.

- Εξοδα λειτουργίας: Expenses are classified by either their nature (e.g., wages, materials) or their function (e.g., cost of sales, administrative expenses). This flexibility allows European companies to present their income statements in a way that best reflects their operational structure.

- Other Comprehensive Income: IFRS emphasizes the importance of other comprehensive income (OCI), which includes gains or losses not reflected in the net income, such as foreign exchange differences or revaluation of financial instruments. This is particularly relevant for European companies operating in multiple currencies.

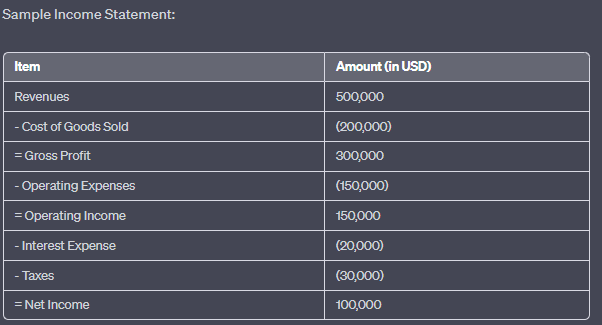

Εικόνα: Δείγμα Κατάστασης Αποτελεσμάτων

Περιγραφή:

The image presents a sample income statement, breaking down the financial performance of a company over a specific period. It starts with the total revenues and subtracts various expenses to arrive at the net income. The statement showcases the following items:

Έσοδα: $500.000

Κόστος Πωληθέντων Αγαθών: $ (200.000)

Μικτό Κέρδος: $300.000

Λειτουργικά Έξοδα: $ (450.000)

Λειτουργικά Έσοδα: $150.000

Έξοδα τόκων: $(20.000)

Φόροι: $(30.000)

Καθαρό Κέρδος: $100.000

Βασικά συμπεράσματα:

- Έσοδα: Το συνολικό χρηματικό ποσό που εισπράττει η εταιρεία πριν από τυχόν έξοδα.

- Κόστος Πωληθέντων Αγαθών (ΚΠΑΓ): Τα άμεσα κόστη που αποδίδονται στην παραγωγή των πωληθέντων αγαθών.

- Μικτό κέρδος: Το κέρδος που έχει μια εταιρεία μετά την αφαίρεση των ΚΠΓ από τα συνολικά έσοδά της.

- Εξοδα λειτουργίας: Το κόστος που σχετίζεται με την καθημερινή λειτουργία της επιχείρησης.

- Λειτουργικά Έσοδα: Το κέρδος από επιχειρηματικές δραστηριότητες (προ φόρων και τόκων).

- Έξοδα τόκων: Το κόστος δανεισμού κεφαλαίων.

- Φόροι: Το ποσό που καταβάλλεται στην κυβέρνηση με βάση το φορολογητέο εισόδημα της εταιρείας.

- Καθαρά έσοδα: Το συνολικό κέρδος της εταιρείας μετά την αφαίρεση όλων των εξόδων από τα έσοδα.

Εφαρμογή πληροφοριών:

Η κατάσταση αποτελεσμάτων χρήσης είναι ένα θεμελιώδες οικονομικό έγγραφο που παρέχει στους επενδυτές και τα ενδιαφερόμενα μέρη πληροφορίες σχετικά με την κερδοφορία μιας εταιρείας σε μια συγκεκριμένη περίοδο. Αναλύοντας την κατάσταση αποτελεσμάτων χρήσης, μπορεί κανείς να κατανοήσει τις ροές εσόδων της εταιρείας, τη δομή κόστους και τη συνολική οικονομική της υγεία. Αυτά τα δεδομένα είναι ζωτικής σημασίας για τη λήψη τεκμηριωμένων επενδυτικών αποφάσεων και την αξιολόγηση της λειτουργικής αποτελεσματικότητας της εταιρείας.

22.2 IFRS and Balance Sheet (Statement of Financial Position)

ο ισολογισμός, known under IFRS as the statement of financial position, provides a snapshot of a company’s assets, liabilities, and equity. IFRS requires companies to clearly differentiate between current and non-current items to offer a transparent view of a company’s financial health.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

- Υποχρεώσεις: Under IFRS, liabilities are also divided into ρεύμα (due within a year) and non-current. European companies must report their obligations, including debt, leases, and pensions, in this format, providing clear insights into their short-term and long-term obligations.

- Shareholders’ Equity: The shareholders’ equity section under IFRS is structured to show both contributed capital (from shareholders) and retained earnings (profits that have been reinvested into the business). European firms must also disclose other reserves, including revaluation reserves and foreign currency translation adjustments.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

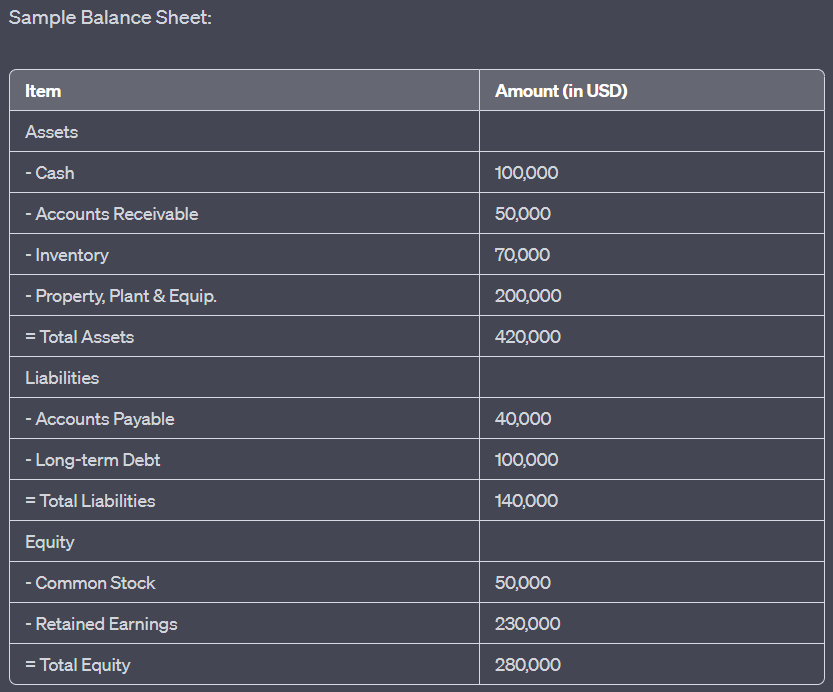

Εικόνα: Sample Balance Sheet

Περιγραφή:

The image displays a sample balance sheet, which provides a snapshot of a company’s financial position at a specific point in time. It categorizes the company’s resources (assets) and the claims against those resources (liabilities and equity). The balance sheet showcases the following items:

- Ακίνητη περιουσία: Σύνολο $420.000, συμπεριλαμβανομένων μετρητών ($400.000), εισπρακτέων λογαριασμών ($50.000), αποθεμάτων ($70.000) και ενσώματων παγίων ($200.000).

- Υποχρεώσεις: Σύνολο $140.000, που περιλαμβάνει Πληρωτέους Λογαριασμούς ($40.000) και Μακροπρόθεσμο Χρέος ($400.000).

- Δικαιοσύνη: Σύνολο $280.000, με κοινές μετοχές ($50.000) και παρακρατηθέντα κέρδη ($230.000).

Βασικά συμπεράσματα:

- Ακίνητη περιουσία: Πόροι που ανήκουν στην εταιρεία και έχουν οικονομική αξία.

- ΥποχρεώσειςΥποχρεώσεις της εταιρείας προς εξωτερικούς φορείς.

- Δικαιοσύνη: Αντιπροσωπεύει το ιδιοκτησιακό συμφέρον στην εταιρεία, συμπεριλαμβανομένων των κεφαλαίων που έχουν επενδυθεί από τους μετόχους και των συσσωρευμένων κερδών.

- Η θεμελιώδης λογιστική εξίσωση: Ενεργητικό = Υποχρεώσεις + Ίδια Κεφάλαια.

\(\textbf{Accounting Equation:}\)

\[ \displaystyle \text{Assets} = \text{Liabilities} + \text{Equity} \]

\(\textbf{Legend:}\)

\(\text{Assets}\) = Total assets

\(\text{Liabilities}\) = Total liabilities

\(\text{Equity}\) = Total equity

Εφαρμογή πληροφοριών:

A balance sheet is a foundational financial statement that offers insights into a company’s financial health. By analyzing the balance sheet, stakeholders can assess the company’s liquidity, solvency, and overall financial stability. This information is vital for investors, creditors, and other stakeholders to make informed decisions related to the company’s financial position

22.3 IFRS and Cash Flow Statement

ο cash flow statement under IFRS follows a similar structure to other global standards but places particular emphasis on transparency in how cash is generated and used by the company. European companies use this statement to report cash flows from operating, investing, and financing activities.

- Λειτουργικές Δραστηριότητες: IFRS allows for flexibility in reporting cash flows from operating activities, either through the direct method (showing cash receipts and payments) or the indirect method (starting with net income and adjusting for non-cash items). Most European companies opt for the indirect method.

- Investing and Financing Activities: Cash flows related to investments in assets or securities and activities such as issuing shares or repaying debt are reported here. European companies must clearly distinguish these transactions to show how they are funding their growth and managing their financial obligations.

- Foreign Exchange Impacts: Given that many European companies operate across multiple countries and currencies, IFRS requires the inclusion of cash flow impacts due to changes in foreign exchange rates, providing investors with a clearer understanding of how currency movements affect a company’s cash position.

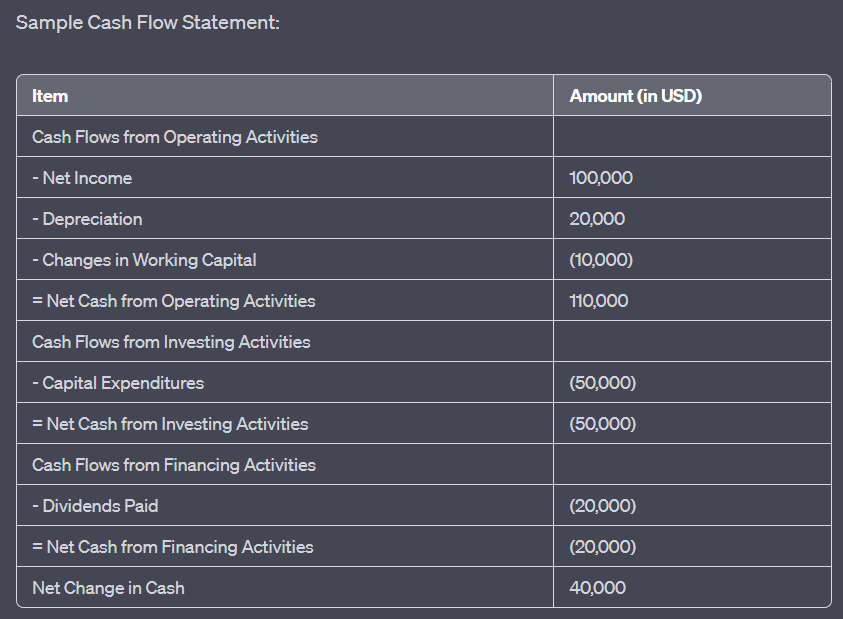

Εικόνα: Sample Cash Flow Statement

Περιγραφή:

The image illustrates a sample cash flow statement, which provides a detailed account of the cash inflows and outflows for a company over a specific period. The statement is segmented into three main categories: Operating Activities, Investing Activities, and Financing Activities. The key items include:

Ταμειακές Ροές από Λειτουργικές Δραστηριότητες: Καθαρά Κέρδη ($100.000), Αποσβέσεις ($20.000) και Μεταβολές στο Κεφάλαιο Κίνησης (-$10.000), με αποτέλεσμα Καθαρά Ταμειακά Διαθέσιμα από Λειτουργικές Δραστηριότητες ύψους $110.000.

Ταμειακές Ροές από Επενδυτικές Δραστηριότητες: Κεφαλαιουχικές Δαπάνες (-$50.000), με αποτέλεσμα Καθαρά Μετρητά από Επενδυτικές Δραστηριότητες ύψους -$50.000.

Ταμειακές Ροές από Χρηματοδοτικές Δραστηριότητες: Καταβληθέντα μερίσματα (-$20.000), με αποτέλεσμα Καθαρά Ταμειακά Διαθέσιμα από Χρηματοδοτικές Δραστηριότητες ύψους -$20.000.

Η συνολική Καθαρή Αλλαγή σε Μετρητά είναι $40.000.

Βασικά συμπεράσματα:

- Λειτουργικές Δραστηριότητες: Αντικατοπτρίζει τα μετρητά που παράγονται ή χρησιμοποιούνται στις βασικές επιχειρηματικές δραστηριότητες.

- Επενδυτικές Δραστηριότητες: Αντιπροσωπεύει μετρητά που χρησιμοποιούνται για επενδύσεις σε περιουσιακά στοιχεία ή εισπράττονται από την πώληση περιουσιακών στοιχείων.

- Χρηματοδοτικές δραστηριότητεςΠαρουσιάζει τις ταμειακές ροές από ή προς εξωτερικές πηγές χρηματοδότησης, όπως δανειστές και μετόχους.

- Η Καθαρή Αλλαγή στα Μετρητά παρέχει μια στιγμιαία εικόνα της συνολικής αύξησης ή μείωσης της ταμειακής θέσης της εταιρείας κατά τη διάρκεια της περιόδου.

Εφαρμογή πληροφοριών:

The cash flow statement is an essential financial tool that offers insights into a company’s liquidity and its ability to generate and use cash effectively. By analyzing the cash flow statement, stakeholders can understand how a company manages its cash resources, which is crucial for assessing its financial health and making informed investment decisions.

συμπέρασμα

In Europe, financial statements are prepared according to IFRS, ensuring a high level of consistency, transparency, and comparability across countries and industries. The κατάσταση αποτελεσμάτων, ισολογισμός, και cash flow statement under IFRS provide investors with the detailed information needed to assess the financial health of European companies. IFRS’s global standards ensure that European companies’ financial reports meet international expectations, making it easier for investors to analyze and compare firms operating in different regions.

Βασικές πληροφορίες μαθήματος:

- The income statement shows a company’s profitability. The income statement provides a breakdown of a company’s revenues, cost of goods sold (COGS), operating expenses, και net income. By analyzing this statement, investors can evaluate how efficiently a company is generating profits and managing costs. Revenue recognition under IFRS ensures accurate reporting based on performance obligations.

- The balance sheet offers a snapshot of a company’s financial position. It categorizes a company’s assets, liabilities, και equity. By examining these elements, investors can assess a company’s liquidity (ability to meet short-term obligations), solvency (ability to meet long-term obligations), and financial health. The fundamental accounting equation του assets = liabilities + equity is key to understanding this statement.

- The cash flow statement tracks how cash is used. The statement divides cash flows into operating, investing, και financing activities. By analyzing this statement, investors can understand how the company generates cash from its operations, how it funds investments, and how it manages external financing. Positive cash flow from operating activities signals a strong cash position.

Τελική δήλωση:

Financial statements under IFRS provide essential insights into a company’s financial health and performance. By analyzing the κατάσταση αποτελεσμάτων, ισολογισμός, και cash flow statement, investors can make well-informed decisions based on transparency, consistency, and detailed reporting, helping them assess the company’s profitability, liquidity, and long-term sustainability.