Local: Understanding Risk and Investment Management

Lesson Learning Objectives:

Introduction:

This section focuses on understanding risk and investment management, highlighting the relationship between risk and reward, diversification as a strategy, comparing different investment risks, sustainability factors, the role of insurance, and the use of credit. By grasping these principles, users can build a balanced financial strategy that aligns with their risk tolerance and financial goals.

Understand the Relationship Between Risk and Reward: Learn how different investments balance risk and potential return, helping users decide how much risk is acceptable based on personal goals and financial comfort levels. This knowledge is useful for making informed investment choices.

Comprehend Diversification as a Risk Management Strategy: Explore how diversification helps reduce risk by spreading investments across various asset classes, ensuring that losses in one area may be offset by gains in another. This strategy stabilizes returns over time and enhances long-term financial growth.

Evaluate Different Investment Risks: Compare the risk and reward of different investment options, from low-risk bonds to high-risk stocks. Understanding these differences allows users to choose investments that align with their financial objectives, whether focusing on growth or stability.

Incorporate Sustainability Factors and Insurance in Financial Planning: Understand how environmental, social, and governance (ESG) factors affect investment risks and returns. Learn how insurance products help protect against major financial losses, ensuring users are better prepared for unexpected events.

Introduction

Risk management is an essential component of financial planning, and insurance plays a key role in protecting individuals and businesses from unforeseen financial losses. This chapter delves into the relationship between risk and reward, the importance of diversification, and how insurance helps manage risks associated with health, life, property, and more. It also explores how external factors such as government policies, economic changes, and emerging technologies impact investment risk. By understanding the types of insurance available and implementing effective risk management strategies, individuals can safeguard their financial future while making informed decisions about how to handle potential risks.

Relationship Between Risk and Reward

One of the most fundamental principles in both investing and risk management is understanding the relationship between risk and potential reward. Generally, investments with the potential for high returns also carry higher risks, meaning there’s a greater chance of losing money. For example, investing in volatile stock markets or speculative assets, such as startups or cryptocurrencies, may lead to significant returns, but there’s also a high likelihood of sharp losses. Conversely, low-risk investments, such as government bonds or savings accounts, tend to offer lower returns but are more secure.

When making financial decisions, it’s important to evaluate how much risk is acceptable based on personal risk tolerance, financial goals, and investment horizon.

Figure: An illustration of a hand offering an umbrella to protect a dollar symbol, representing the concept of financial security and insurance. The image conveys the idea of safeguarding assets and investments.

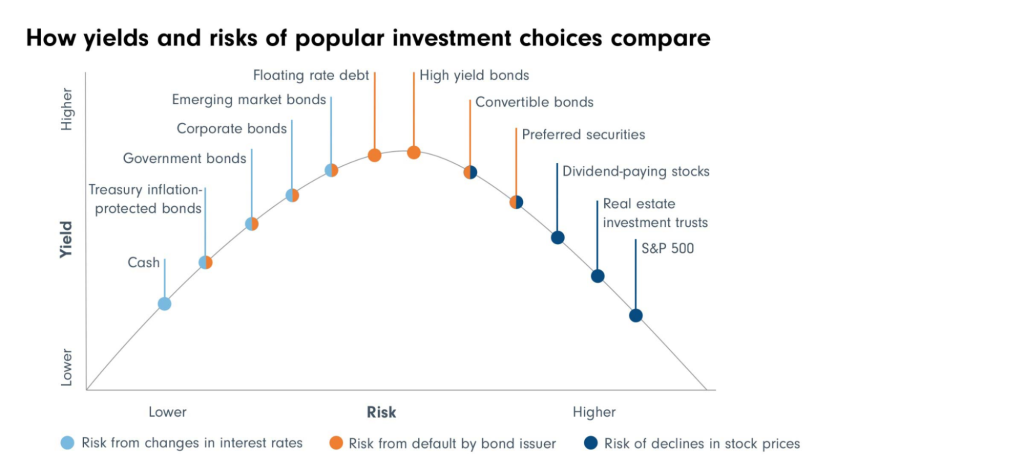

Figure: How yields and risks of popular investment choices compare

Description:

The graph compares various investment options by illustrating their relative yields and associated risks. It plots different types of investments, such as cash, bonds, and stocks, showing how each can be affected by factors like changes in interest rates, bond defaults, or stock price declines. Investments are positioned from low yield/low risk to high yield/high risk, helping users understand where each asset class stands in terms of risk and return.

Key Takeaways:

Low-risk, low-yield investments include cash and government bonds, typically seen as safe but with modest returns.

Moderate-risk investments like corporate and emerging market bonds offer higher yields but come with greater risks.

Higher-risk investments such as high-yield bonds and dividend-paying stocks can provide substantial returns but are more susceptible to market volatility.

Investment risk can stem from various factors, including interest rate changes, defaults, or fluctuations in stock prices.

Application of Information:

Investors can use this information to balance their portfolios based on risk tolerance and desired returns. Understanding the risk-yield relationship helps in choosing appropriate assets, whether prioritizing safety or aiming for higher potential gains. This comparison is useful for creating diversified investment strategies that align with specific financial goals.

Diversification as a Risk Management Strategy

Investment diversification is a strategy used to reduce risk by spreading investments across a variety of asset classes (e.g., stocks, bonds, real estate, commodities) and sectors. Diversification ensures that poor performance in one area is balanced by better performance in another, thereby reducing the overall impact on a portfolio.

Figure: An illustration of a businessman holding a coin, standing next to a pie chart depicting various investment categories such as stocks, bonds, crypto, commodities, and mutual funds. The image represents the concept of diversification in investment portfolios.

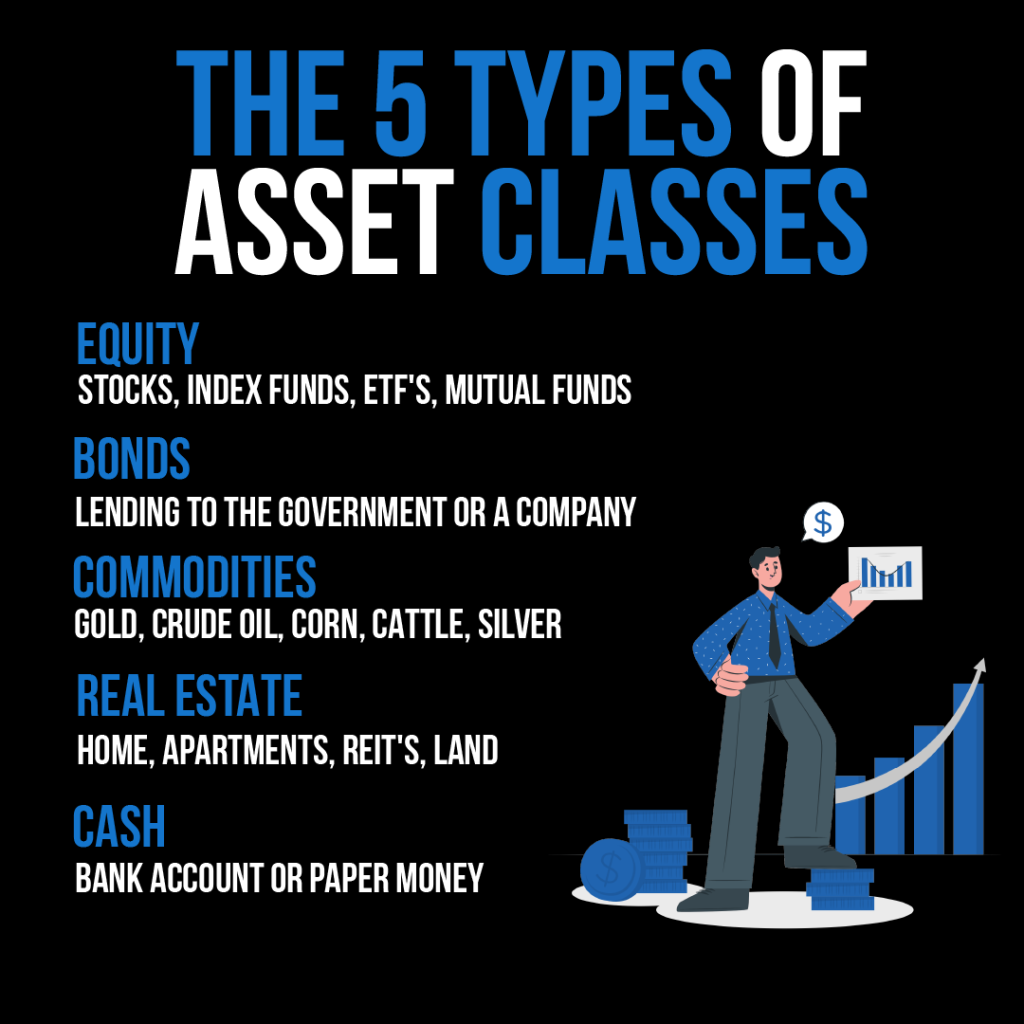

Figure: The infographic outlines "The 5 Types of Asset Classes" that are commonly included in an investment portfolio. These are: Equity: This includes stocks, index funds, exchange-traded funds (ETFs), and mutual funds. Bonds: This represents lending to the government or a company. Commodities: Examples are gold, crude oil, corn, cattle, and silver. Real Estate: This can be a home, apartments, Real Estate Investment Trusts (REITs), or land. Cash: This refers to money in bank accounts or physical paper money. The infographic serves as an educational tool for individuals looking to understand the different types of assets they can invest in. For practical use, investors should consider diversifying their portfolios across these asset classes to spread risk and potential for return, in line with their investment goals and risk tolerance.

For example, if someone holds a diversified portfolio with European stocks, government bonds, and real estate investments, a drop in the stock market may be offset by gains in the bond or real estate markets. This balance reduces the likelihood of a significant financial loss.

Diversification is particularly important in managing long-term financial risks, as it stabilizes returns and ensures steady asset growth over time.

Figure: Diversified Investment Portfolio

Description:

The image illustrates a diversified investment portfolio, displaying different asset classes like stocks, bonds, real estate, and gold. It visually represents how spreading investments across multiple assets can reduce risk. Each segment highlights a different type of investment, indicating that a balanced portfolio includes a variety of asset classes to achieve stability and growth.

Key Takeaways:

Diversification reduces risk by spreading investments across different assets.

Stocks and bonds are key components of many portfolios, offering a mix of growth and fixed income.

Real estate and gold can act as hedges, providing stability during market fluctuations.

Balanced portfolios can protect against losses in one asset class by gaining in another.

Application of Information:

Investors can use this strategy to protect their savings from unpredictable market movements. By including a variety of assets in their portfolios, they can achieve a balance between risk and return, ensuring long-term financial stability and growth. Diversification helps manage risk by not relying solely on a single investment.

Comparing the Risk and Reward of Different Investments

When making investment decisions, individuals must compare the risk and reward of different financial products. High-risk investments, such as venture capital or high-growth tech stocks, may offer substantial returns, but they come with the possibility of large losses. In contrast, lower-risk investments, such as bonds or certificates of deposit (CDs), provide more stable but modest returns.

Figure: Detailed vector diagram illustrating the risk management process, ideal for understanding corporate risk assessment and mitigation strategies.

Investors must assess whether their financial objectives—such as asset growth, financial security, or sustainability preferences—are best served by riskier investments or by taking a more conservative approach.

Example: An investor nearing retirement might prioritize financial security by investing in bonds and other low-risk assets, while a younger investor might prioritize asset growth by focusing on high-growth stocks.

Figure: Key Characteristics of Asset Classes

Description:

The table summarizes different asset classes by evaluating their return, risk, liquidity, transparency, holding period, and classification as defensive or growth assets. Each asset type, such as cash, equities, or hedge funds, is assessed based on factors like how risky they are, how liquid they are (ease of converting to cash), and the typical investment period required. This helps investors understand the trade-offs and typical characteristics of each asset class.

Key Takeaways:

Cash and gilts are low-risk, highly liquid assets but offer lower returns, classified as defensive.

Equities and private equity tend to have higher risk but can yield higher returns, categorized as growth assets.

Liquidity varies significantly, with assets like cash being more liquid compared to property or hedge funds.

Holding periods differ: defensive assets often have shorter holding periods, while growth assets may require longer commitments.

Application of Information:

Understanding the characteristics of each asset class can help investors balance risk and return in their portfolios. This table aids in determining which assets to prioritize based on investment goals, whether seeking stability (defensive) or growth. Investors can use this information to diversify effectively by including a mix of both defensive and growth assets, depending on their risk tolerance and investment horizon.

Sustainability Factors and Government Climate Policies

In recent years, sustainability factors—such as environmental, social, and governance (ESG) criteria—have become increasingly important in evaluating investment risks. Companies that fail to address environmental sustainability or social responsibility may face ESG risks that negatively impact their financial performance, such as reputational damage, regulatory fines, or declining market share.

Figure: A 3D isometric illustration showing financial charts, graphs, and analytics, symbolizing the concept of data-driven decision-making in investment and finance.

In the Eurozone and globally, government climate-related policies are affecting how companies operate and may influence the risk and return of investments. For example, companies that do not adapt to new environmental regulations may face higher costs, which could reduce profits and lower stock prices. Conversely, companies that embrace sustainability may benefit from favorable policies and consumer support, leading to better financial performance.

Investors should consider ESG risks when evaluating the long-term prospects of a company and be aware of how government policies on climate change could impact their investments.

Figure: The Environmental, Social, and Governance (ESG) Imperative and Its Impact on Organizations

Description:

The figure outlines the ESG program journey, highlighting eight key steps organizations can take to develop a comprehensive and effective ESG strategy. Starting with understanding ESG drivers, setting program goals, and assessing impacts, it guides through defining governance, identifying gaps, delivering goals, and continual monitoring. Each step emphasizes the role of stakeholders, and a circular diagram showcases the involvement of internal and external stakeholders in assessing ESG factors.

Key Takeaways:

Understanding ESG drivers is crucial for setting a strong foundation for sustainability programs.

Defining clear governance structures ensures accountability and effective management of ESG initiatives.

Continual reporting and assessment help organizations stay adaptive and improve their ESG strategies over time.

Stakeholder involvement is a key factor in assessing and aligning ESG practices.

Identifying gaps and addressing them is essential for achieving desired sustainability outcomes.

Application of Information:

This data is useful for organizations and investors to build and evaluate ESG programs effectively. Understanding the steps in the ESG journey allows companies to improve their sustainability efforts, while investors can use this information to assess a company’s ESG performance and commitment.

Using Insurance for Risk Management

Insurance plays a critical role in risk management by providing protection against unforeseen financial losses. Common types of insurance include:

Health insurance: Covers medical expenses in case of illness or injury.

Life insurance: Provides financial support to beneficiaries in the event of the policyholder’s death.

Property insurance: Protects against damage to personal or commercial property due to disasters, theft, or accidents.

Disability insurance: Offers income replacement if the policyholder becomes unable to work due to injury or illness.

Each of these insurance types helps individuals and businesses manage specific financial risks, ensuring that they are protected from catastrophic financial events. The cost of insurance, in the form of premiums, should be weighed against the potential financial loss from unprotected risks.

Figure: Types of Insurance by DF/Risk Sharing Benefit

Description:

The figure categorizes different types of insurance based on their source and the type of risk-sharing benefits they offer. It divides insurance into those provided by the informal and formal economies. Informal sources include family, village, and informal businesses, focusing on basic personal needs, micro-enterprises, and mutual aid. Formal sources include cooperatives, commercial sectors, and government institutions, covering a wider range of insurance types such as loans, health, retirement, and social security.

Key Takeaways:

Informal economies provide basic and community-based insurance through personal loans and micro-business support.

Formal sectors offer structured insurance products like life, health, and mortgage insurance, typically through cooperatives, commercial firms, or government programs.

Cooperatives and credit unions play a role in providing group-based risk-sharing benefits and accessible financial products.

Government ensures social safety nets with programs like health insurance, unemployment benefits, and pensions.

Application of Information:

This data helps users understand the various sources of insurance and how they function within different economic systems. It is useful for individuals and investors to assess which type of insurance best suits their needs or to identify gaps in insurance coverage within markets, helping make informed decisions about risk management.

Understanding the Risks of Credit for Discretionary Spending

Using credit to finance discretionary spending, such as luxury goods or vacations, introduces significant financial risks. High-interest credit cards or loans can quickly accumulate debt, which may become difficult to repay, especially if personal finances take an unexpected hit. This can lead to long-term financial difficulties, including damage to credit scores and the potential for falling into debt traps.

It is essential to understand that while using credit can provide short-term financial flexibility, it should be done with careful consideration of the interest rates, repayment terms, and overall impact on long-term financial security.

Example: A consumer who uses a high-interest credit card to pay for a vacation may face steep monthly interest charges if they are unable to pay off the balance, ultimately increasing the total cost of the vacation.

Key Lesson Information:

Risk and Reward are directly related—higher potential returns come with higher risks, while lower-risk investments offer more stability but less growth. Users should align their investment choices with their comfort level and financial goals.

Diversification spreads investment risk across different asset types, such as stocks, bonds, real estate, and commodities. A diversified portfolio helps reduce overall risk, making it an essential part of long-term financial planning.

Investment Comparison helps users evaluate different options based on risk, return, and liquidity. For instance, low-risk investments like bonds offer more stable returns, while high-risk investments like stocks provide higher growth potential.

Sustainability Factors and ESG criteria are becoming increasingly important in investment decisions. Companies that embrace sustainability tend to perform better over the long term, while those that neglect it may face financial and reputational risks.

Insurance is a key element of risk management, providing protection against unforeseen events such as medical emergencies, property damage, or disability. Using insurance wisely can help users maintain financial security and avoid catastrophic losses.

Using Credit for Discretionary Spending involves significant risks. High-interest debt can lead to long-term financial challenges, such as damage to credit scores or debt traps. Users should approach credit usage carefully, considering the interest rates and repayment terms to avoid potential pitfalls.

Closing Statement:

Understanding these key concepts in risk and investment management helps users build a solid financial foundation. By applying strategies like diversification, considering ESG factors, using insurance effectively, and managing credit wisely, individuals can achieve both financial stability and growth.