Chapter 11: Tax Planning and Strategies (CAD)

Objetivos de aprendizaje de la lección:

Introducción: This section introduces essential tax planning strategies in Canada, focusing on taxpayer rights, understanding different types of taxes, and advanced tax planning techniques to optimize financial outcomes.

- Understand Taxpayer Rights and Responsibilities: Gain knowledge of the Taxpayer Bill of Rights and the responsibilities of Canadian taxpayers, ensuring fair treatment and awareness of entitlements.

- Comprehend Various Types of Taxes: Learn about different taxes applicable in Canada, including income tax, sales tax, property tax, y custom duties, and their implications on personal finances.

- Apply Advanced Tax Strategies: Explore strategic tax planning techniques, including timing income and deductions, investment tax optimization, y estate tax planning to enhance financial benefits.

A. Tax Basics

A1. Taxpayer Rights and Responsibilities

Canadian taxpayers have rights outlined in the Taxpayer Bill of Rights. For instance, you have the right to receive entitlements and to pay no more and no less than what is required by law. Example: If a taxpayer believes they’ve been overcharged, they can file an objection, which the Canada Revenue Agency (CRA) must address promptly and professionally.

A2. Understanding Taxes and Contributions

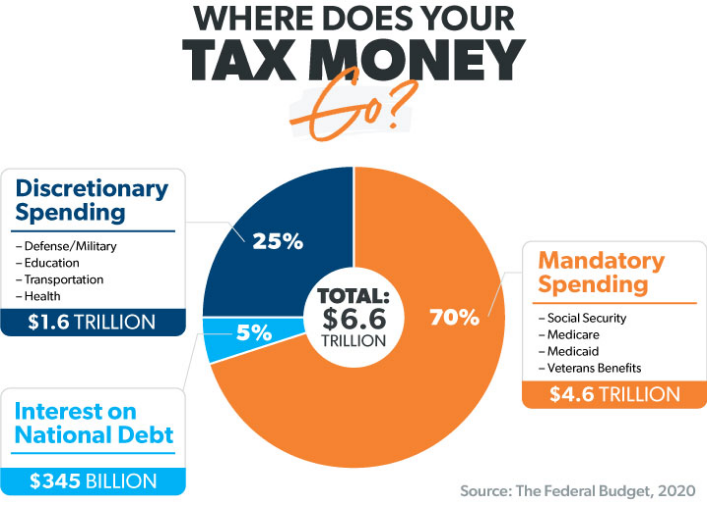

Título de la figura: ¿A dónde va el dinero de sus impuestos?

Fuente: Soluciones Ramsey

Descripción: El artículo de Ramsey Solutions desglosa la asignación de impuestos federales recaudados por el IRS, que ascendió a alrededor de $4,9 billones en 2022. Explica la distribución del dinero de los impuestos entre diversos gastos gubernamentales, incluidos los intereses de la deuda pública, el gasto obligatorio en derechos programas como beneficios del Seguro Social, Medicare, Medicaid y Asuntos de Veteranos, así como gastos discrecionales, que cubren defensa nacional, transporte, educación, salud y más.

Conclusiones clave:

- Una parte del dinero de los impuestos se utiliza para pagar intereses de la deuda nacional.

- Gasto obligatorio Incluye importantes programas de derechos como el Seguro Social, Medicare y Medicaid.

Gastos discrecionales Implica asignaciones presupuestarias que el Congreso debate anualmente, incluidas defensa, transporte, educación y salud.

Solicitud: Para las personas que aprenden sobre finanzas personales, este desglose proporciona información sobre cómo funciona el presupuesto gubernamental y la importancia de comprender dónde se gasta el dinero de los impuestos. Puede informar decisiones sobre el compromiso político y la responsabilidad fiscal. Para los inversores, conocer las áreas de gasto público puede orientar las estrategias de inversión, ya que los sectores que reciben una financiación significativa pueden presentar oportunidades de inversión. Comprender estas asignaciones también ayuda a los contribuyentes a ver el impacto de sus contribuciones en las prioridades y servicios nacionales.

Different taxes apply to various aspects of life in Canada:

- Income Taxes: Earnings are taxed at federal and provincial levels. Example: A software developer in Ontario pays federal tax and a provincial tax.

- Sales Taxes: Goods and Services Tax (GST) is a federal tax, while the Harmonized Sales Tax (HST) combines GST with provincial sales tax in some provinces. Example: When purchasing a laptop in British Columbia, you pay 5% GST and an additional 7% PST.

- Property Taxes: Homeowners pay property taxes based on assessed property value. Example: A homeowner in Vancouver pays property tax to the City, which funds local services.

- Custom Duties and Excise Taxes: Special taxes on certain imports like cars or alcohol. Example: Importing a car from the US might incur excise taxes if it doesn’t meet Canadian standards.

- Tariffs: Taxes on imported goods. Example: A business importing electronics from China pays tariffs calculated as a percentage of their value.

- Duties and Fees: Specific types of taxes on goods like tobacco or services like legal document processing. Example: Importing a vintage wine collection may attract a customs duty.

- CPP (Canada Pension Plan): A mandatory pension plan to which employees and employers contribute. Example: An employee earning CAD 55,000 annually might contribute CAD 2,544.30 to CPP.

- Health Services Taxes: Additional taxes in some provinces for health care funding. Example: In Ontario, a high-income earner pays a health premium with their taxes.

- Motor Vehicle Licenses: Annual fees for the licensing of vehicles, varying by province and vehicle type. Example: Renewing the license for a mid-sized car in Alberta may cost about CAD 93 annually.

Natural Gas Taxes: Levied on the consumption of natural gas. Example: A household in Quebec may see a tax on their monthly natural gas utility bill.

B. Income Tax Essentials

B1. Who Charges Income Tax

Both the federal government and your provincial/territorial government charge income tax, and you must file tax returns separately for each. Example: A teacher in Quebec files a federal return with the CRA and a provincial return with Revenu Québec.

B2. Types and Groups of Income

Income includes money from employment, businesses, and investments. Example: A freelance graphic designer reports income from client payments, interest from savings accounts, and dividends from Canadian stocks.

B3. Tax Brackets and Rates

Canada’s progressive tax system means higher earnings are taxed at higher rates. Example: A doctor earning CAD 250,000 pays a higher marginal tax rate on income above CAD 150,000.

- Average Federal Tax Rate: The percentage of income that goes to federal tax. Example: If a person earns CAD 100,000 and pays CAD 18,000 in tax, their average tax rate is 18%.

- Marginal Federal Tax Rate: The tax rate paid on the last dollar earned, often the highest rate. Example: If the same person earns an additional CAD 10,000, it may be taxed at 29%, which is their marginal rate.

Here’s an illustrative table showcasing hypothetical tax rates:

Income Range (CAD) | Tax Rate (%) |

0 – 48,535 | 15 |

48,536 – 97,069 | 20.5 |

97,070 – 150,473 | 26 |

150,474 – 214,368 | 29 |

Above 214,368 | 33 |

*Note: These numbers are illustrative and not based on current tax brackets.

B4. Provincial/Territorial Income Tax

Provincial/territorial taxes vary and can significantly affect your take-home pay. Example: An engineer might consider the lower personal income tax rate when deciding to move from Nova Scotia to Alberta.

C. Reducing Taxable Income

C1. Tax Deductions

You can lower your taxable income with deductions for RRSP contributions, childcare expenses, and more. Example: A parent may claim CAD 8,000 in childcare expenses, reducing their taxable income from CAD 70,000 to CAD 62,000.

C2. RRSP Contributions

Contributions to an RRSP reduce your current taxable income and grow tax-deferred until withdrawal. Example: A contribution of CAD 5,000 to an RRSP may save you approximately CAD 1,500 in taxes if you’re in a 30% tax bracket.

C3. Other Registered Savings Plans

- TFSA contributions are made with after-tax dollars, but earnings and withdrawals are tax-free. Example: If you invest CAD 5,000 in a TFSA and it grows to CAD 7,000, the CAD 2,000 gain is not taxed

- Clawback: Refers to the government reclaiming benefits if your income exceeds a certain threshold. Example: Old Age Security payments may be subject to clawback for high-income seniors.

- RESPs (Registered Education Savings Plans): Allow savings for education to grow tax-free until the beneficiary withdraws for educational purposes. Example: Parents contribute to an RESP for their child’s future tuition, and the investment grows without being taxed with a percentage contribution matched by government grants and bonds.

- RDSPs (Registered Disability Savings Plans): Long-term savings plans to help Canadians with disabilities and their families save for the future. Example: The family of a child with a disability invests in an RDSP to secure their financial future, with contributions matched by government grants and bonds.

.

C4. Tax Credits

Credits like the Disability Tax Credit or the Canada Child Benefit can directly reduce the tax payable. Example: A family with a child with a disability might receive a non-refundable credit that reduces their tax bill by CAD 2,500.

C5. Tax Refunds

If tax deductions and credits lower your taxes paid below what was withheld by employers, you’re due a refund. Example: An overpayment of CAD 2,000 in income tax due to excessive payroll deductions would result in a CAD 2,000 refund.

C6. Taxes in Everyday Life

Understanding taxation allows for informed decisions about spending, saving, and investing. Example: A consumer decides to buy a fuel-efficient car partly because of the eco-friendly rebate and the reduced fuel taxes compared to a gas-guzzling model.

D. Advanced Tax Strategies

D1. Strategic Tax Planning

Involves timing income and deductions for optimal tax outcomes. Example: A contractor defers invoicing for a big job to the next tax year when expecting to be in a lower tax bracket.

D2. Investment Tax

Understanding the tax implications of investments can optimize after-tax returns. Example: An investor chooses to hold dividend-paying stocks outside of a TFSA to take advantage of the dividend tax credit.

D3. Estate Tax Planning

Managing the tax implications of one’s estate can maximize the value passed to heirs. Example: An individual buys a life insurance policy to cover potential estate taxes, ensuring their heirs receive the intended inheritance without tax erosion.

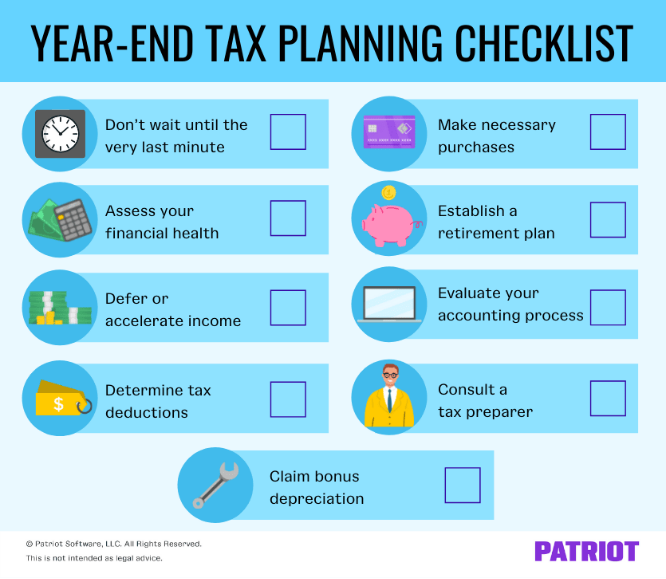

Título de la figura: Lista de verificación de planificación fiscal de fin de año

Fuente: Software patriota

Descripción:

La imagen proporciona una lista de verificación para la planificación fiscal de fin de año:

- No esperes hasta el último momento: Comience su planificación fiscal mucho antes de que termine el año.

- Evalúe su salud financiera: Revise sus estados financieros y comprenda su situación financiera.

- Aplazar o acelerar ingresos: Dependiendo de su situación fiscal, considere diferir o acelerar los ingresos.

- Determinar las deducciones fiscales: Identifique todas las posibles deducciones fiscales que pueda reclamar.

- Reclamar bonificación de depreciación: Si corresponde, reclame la depreciación adicional en su declaración de impuestos.

- Realizar las compras necesarias: Realice las compras comerciales necesarias antes de que finalice el año para reclamar deducciones.

- Establecer un plan de jubilación: Establece un plan de jubilación para ahorrar para el futuro y disfrutar de beneficios fiscales.

- Evalúe su proceso contable: Asegúrese de que su proceso contable sea eficiente y preciso.

Consulte a un preparador de impuestos: Busque asesoramiento profesional para asegurarse de maximizar sus ahorros fiscales.

Conclusiones clave:

- La planificación temprana y la evaluación de la salud financiera son cruciales para una planificación fiscal eficaz.

- Identificar las deducciones fiscales y realizar las compras necesarias puede ayudar a reducir la obligación tributaria.

- Consultar a un preparador de impuestos y evaluar el proceso contable garantiza una presentación de impuestos precisa.

Solicitud: Esta lista de verificación proporciona un enfoque estructurado para que los propietarios de pequeñas empresas planifiquen los impuestos de fin de año. Siguiendo estos pasos, los dueños de negocios pueden prepararse mejor para la temporada de impuestos, garantizar una presentación de impuestos precisa y potencialmente reducir su obligación tributaria. Es una guía útil para garantizar que todos los aspectos importantes de la planificación fiscal se consideren y aborden antes de que finalice el año.

Información clave de la lección:

Frase de cierre: Mastering tax planning and understanding various tax types and strategies are vital for financial optimization and compliance. This section equips you with the knowledge to navigate the Canadian tax system effectively and make informed financial decisions.

- Taxpayer Rights and Responsibilities: Entender el Taxpayer Bill of Rights, ensuring fair treatment and awareness of entitlements.

- Types of Taxes in Canada: Conozca más sobre income tax, sales tax, property tax, y custom duties, and their implications on personal finances.

- Income Tax Essentials: Comprehend how both federal and provincial/territorial governments charge income tax, and understand Canada’s progressive tax system with specific tax brackets y rates.

- Advanced Tax Strategies: Apply strategic tax planning techniques, including timing income and deductions, investment tax optimization, y estate tax planning.