Global: El papel de los valores personales y sociales en el comportamiento financiero

Objetivos de aprendizaje de la lección:

Introducción:

This section focuses on how personal and societal values shape financial behavior, impacting decisions on spending, saving, and investing. Understanding these values can help you align your financial choices with your personal beliefs and societal norms.

- Understand Personal Values: Learn how your personal beliefs influence financial decisions, such as prioritizing sustainable investments or saving for family support. This knowledge will help you make financial choices that align with your personal ethics.

- Recognize Societal Influences: Discover how broader societal norms shape financial behavior. For example, in cultures that emphasize collectivism, financial decisions might focus on family support, while individualistic cultures may prioritize personal wealth.

- Identify Cognitive Biases: Gain awareness of common cognitive biases like anchoring y loss aversion, which can impact financial decision-making. Knowing these biases helps you avoid irrational choices and make more informed decisions.

- Navigate Financial Partnerships: Learn how to manage financial partnerships effectively, whether in business, family, or marriage, by emphasizing clear communication, transparency, and shared goals.

A. The Role of Personal and Societal Values

Personal and societal values play a significant role in shaping financial decisions. Personal values refer to an individual’s beliefs about money, spending, saving, and investing, while societal values influence broader financial norms and behaviors within a community or country. For example, in societies that emphasize collectivism, there may be a stronger focus on family support, shared wealth, or communal financial goals. In more individualistic societies, personal wealth accumulation and financial independence are often prioritized.

Understanding how values influence financial behavior helps individuals align their financial decisions with their moral or ethical beliefs. For instance, someone who values sustainability may choose to invest in green energy companies or purchase products from environmentally responsible brands.

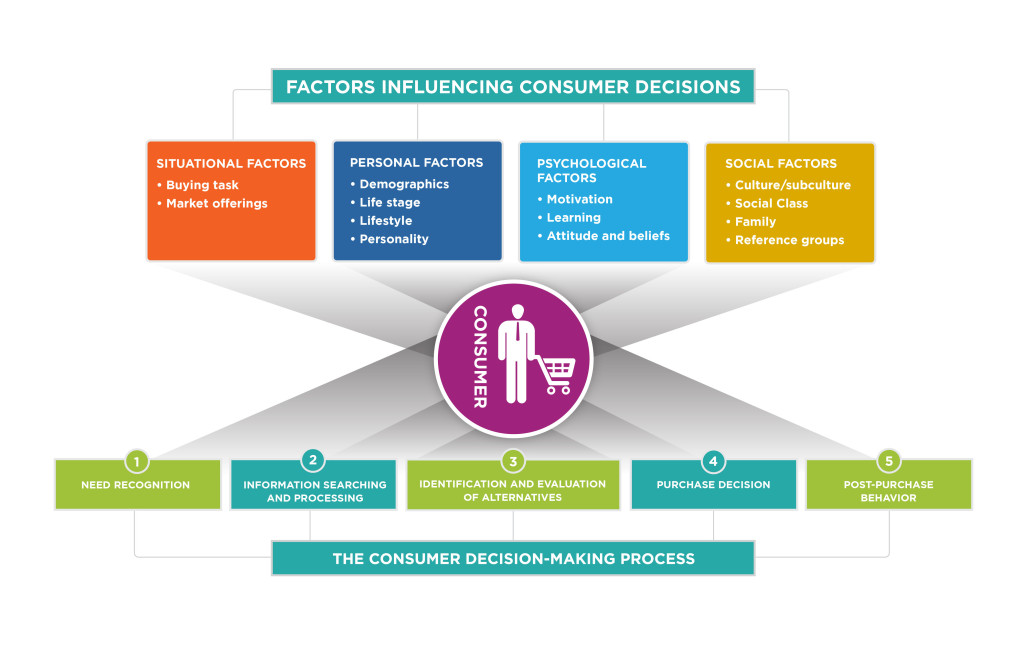

Cifra: Factors Influencing Consumer Decisions

Descripción:

This image shows the factors influencing consumer decisions, which include situational factors (like market offerings and buying tasks), personal factors (such as demographics and lifestyle), psychological factors (including motivation and beliefs), and social factors (like family and social class). At the center of these influences is the consumidor, who goes through a decision-making process with steps: need recognition, information searching and processing, identification of alternatives, purchase decision, y post-purchase behavior.

Conclusiones clave:

- Consumer decisions are influenced by a mix of situational, personal, psychological, and social factors.

- El decision-making process begins with recognizing a need and ends with post-purchase behavior.

- Motivation, beliefs, and lifestyle play a crucial role in shaping consumer preference

- Market offerings and the buying task directly impact situational decision-making.

Solicitud de información:

Understanding the factors influencing consumer decisions is crucial for investors and businesses in predicting market trends and consumer behavior. Analyzing consumer motivations and preferences can help create more targeted marketing strategies and improve product offerings to meet consumer needs at different stages of the decision-making process.

B. Cognitive Biases and Financial Decision-Making

Cognitive biases are systematic patterns of deviation from rational decision-making, and they can heavily influence how people manage their finances. Some of the most common biases include:

- Anchoring Bias: The tendency to rely heavily on the first piece of information encountered (e.g., focusing on the initial price of an item without considering discounts or promotions).

- Herd Mentality: Following the financial behaviors of others, such as making investment decisions based on what friends or family are doing, without conducting personal research.

- Loss Aversion: The tendency to prefer avoiding losses over acquiring gains. For example, people may hold onto underperforming investments to avoid realizing a loss, even when selling could free up funds for better opportunities.

By recognizing these biases, individuals can take steps to mitigate their effects and make more informed financial decisions. This can include seeking out diverse sources of information, using financial planning tools, or consulting professionals before making major financial decisions.

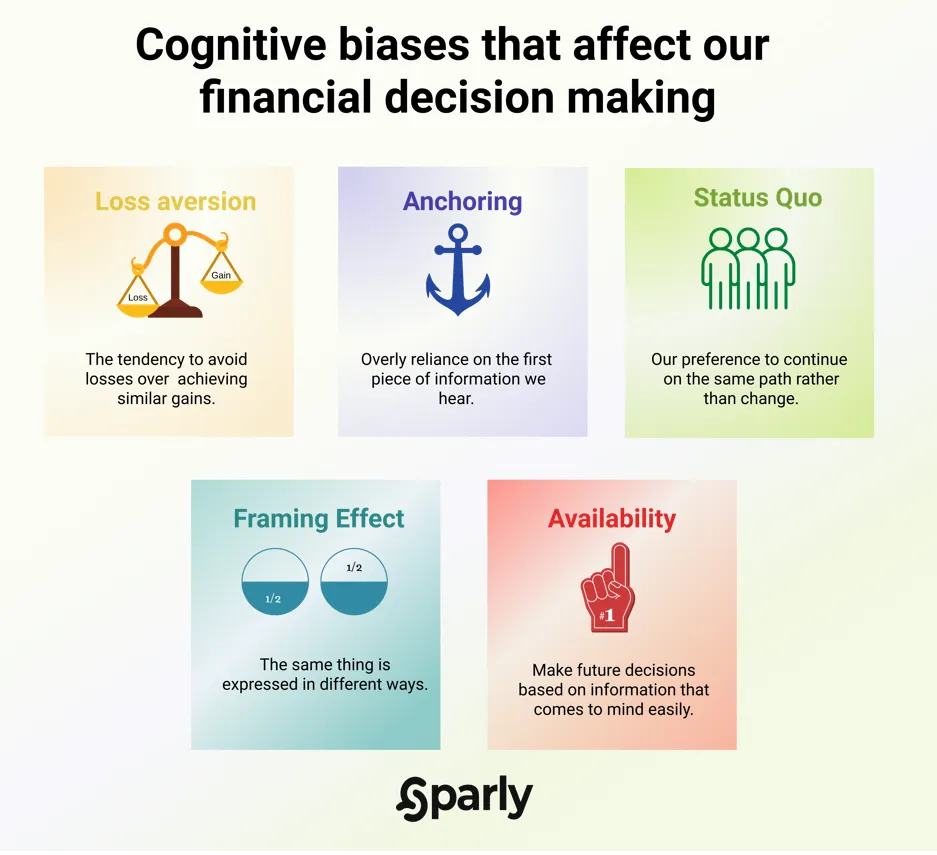

Cifra: Cognitive biases that affect our financial decision making

Descripción:

This image illustrates five common cognitive biases that can influence how individuals make financial decisions. These biases include Loss Aversion, where people tend to prioritize avoiding losses over achieving similar gains; Anchoring, which refers to relying too heavily on the first piece of information provided when making decisions; Status Quo, highlighting the preference to stick with familiar options rather than choosing change; Framing Effect, where different ways of presenting the same information can lead to different decisions; and Availability, where people make decisions based on information that is readily available or easily recalled.

Conclusiones clave:

- Loss Aversion: People prefer avoiding losses more than gaining equivalent rewards.

- Anchoring: Initial information provided can disproportionately influence decisions.

- Status Quo: There is a tendency to favor familiar, known options rather than changes.

- Framing Effect: The way information is presented can lead to different choices, even when the facts are the same.

- Availability: Decisions are often based on what comes to mind most easily, not necessarily on all relevant information.

Solicitud de información:

Understanding these biases can help inversores make more rational financial decisions by recognizing when they might be influenced by emotions or faulty thinking. For instance, being aware of loss aversion might encourage someone to take calculated risks in investing, while recognizing the framing effect can help in evaluating financial products more objectively.

C. Navigating Financial Partnerships

Whether in business, marriage, or family life, financial partnerships are a key aspect of managing personal finances. Successful financial partnerships require clear communication, mutual trust, and an understanding of each partner’s financial goals and values.

- Joint decision-making: Partners need to establish shared financial goals and make decisions together, whether it’s about buying a home, investing, or saving for future expenses.

- Transparency: Open and honest communication about income, expenses, debt, and financial challenges is crucial to avoid misunderstandings.

- Managing differences: Partners may have different approaches to spending and saving, which can create conflicts. Recognizing and respecting these differences while finding common ground is key to a healthy financial relationship.

In the case of business partnerships, it’s important to outline each party’s financial responsibilities, define clear roles, and have legal contracts in place to avoid potential disputes. Seeking professional advice when entering into financial partnerships can help ensure that all parties are protected.

D. Familial and Cultural Influences

Family and cultural background heavily influence how individuals view and manage money. In many cultures, there is a strong emphasis on intergenerational wealth y supporting extended family. For example, in some countries, younger generations are expected to contribute financially to support aging parents, while in other cultures, parents may prioritize saving for their children’s education or future.

Cultural influences can also shape attitudes toward debt, saving, and investment. In cultures where saving is highly valued, individuals may be more cautious about borrowing or taking financial risks. In contrast, societies that embrace entrepreneurship may encourage taking calculated risks to achieve financial success.

Understanding these familial and cultural influences helps individuals navigate their financial decisions while respecting their background. At the same time, it’s important to balance these influences with personal financial goals to ensure long-term financial security.

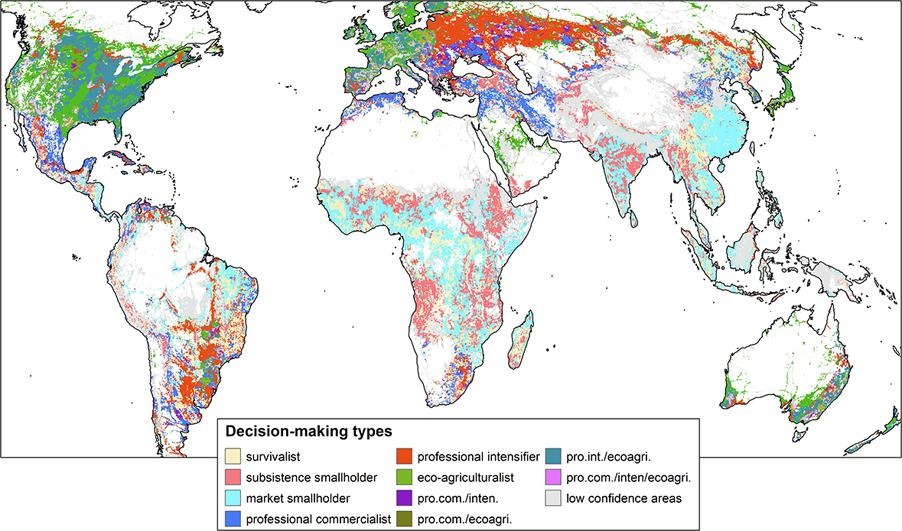

Cifra: Decision-Making Types in Agriculture

Descripción:

This map illustrates various agricultural decision-making types across the world. Each color on the map represents a different type of farmer or agricultural decision-maker, including categories like survivalist, subsistence smallholder, market smallholder, professional commercialist, professional intensifier, y eco-agriculturalist. The map also includes categories like professional intensifier with eco-agriculture and regions marked with low confidence areas. By examining these decision-making types, one can understand the diversity of farming practices and strategies across different geographic regions, based on factors like market orientation, sustainability, and professionalism.

Conclusiones clave:

- Survivalist farmers are focused on basic survival rather than market integration.

- Market smallholders engage in farming for commercial purposes but on a smaller scale.

- Professional commercialists focus on larger-scale, market-oriented farming.

- Eco-agriculturalists adopt practices focused on sustainability and environmental preservation.

- Professional intensifiers aim to increase productivity through modern techniques, sometimes combined with eco-friendly practices.

- Low confidence areas reflect regions with less certainty in the data due to various factors.

Solicitud de información:

Understanding the different agricultural decision-making types es crucial para inversores or policy-makers analyzing agricultural markets or supporting sustainable farming. Investors can identify regions with high potential for commercial agricultural investments, while sustainability advocates can target regions with existing eco-agricultural practices for further development and support.

Información clave de la lección:

- Personal Values influence financial choices by aligning spending, saving, and investing with ethical beliefs. For example, someone who values sustainability may invest in eco-friendly companies. Aligning financial decisions with personal ethics promotes satisfaction and confidence in financial outcomes.

- Societal Values impact financial behavior across different cultures. In collectivist societies, people may focus on shared wealth and family support, while in individualistic societies, the emphasis is often on personal wealth and financial independence. Recognizing these influences helps individuals understand the broader context of their financial behavior.

- Cognitive Biases como anchoring, herd mentality, y loss aversion can lead to suboptimal financial decisions. By identifying these biases, individuals can develop strategies to make more rational choices, such as conducting thorough research before investing or consulting with financial experts.

- Financial Partnerships require trust, transparency, and shared decision-making. Open communication about income, expenses, and goals can help avoid conflicts, whether in marriage, family, or business. Managing differences in financial habits is crucial for successful partnerships.

- Familial and Cultural Influences play a significant role in financial behavior. For example, some cultures emphasize saving for intergenerational wealth, while others encourage risk-taking for entrepreneurial success. Balancing these cultural influences with personal financial goals is essential for long-term stability.

Frase de cierre: Recognizing the role of personal and societal values, cognitive biases, and cultural influences can enhance financial decision-making. By aligning financial choices with values and managing biases, individuals can achieve greater satisfaction, build stronger partnerships, and navigate cultural expectations effectively.