Mondial : Mesurer le risque et comprendre la volatilité

Objectifs d'apprentissage de la leçon :

- Understand the difference between risk and volatility. You’ll learn how risque relates to the chance of losing money and how volatilité reflects the ups and downs of asset prices over time.

- Learn how to measure risk using standard deviation and beta. These tools help you understand how much an investment’s price might change, and how it moves in relation to the market.

- Explore how personal risk tolerance affects investment decisions. You’ll see how age, goals, income, and emotional comfort with risk help shape a portfolio that feels right for you.

- Discover common tools for measuring portfolio risk. Techniques like Valeur à risque (VaR), Ratio de Sharpe, et analyse de scénarios help you understand possible outcomes and worst-case scenarios.

- Recognize different types of investment risks. You’ll learn about market risk, credit risk, liquidity risk, and more, and how knowing these risks helps you protect your money through better strategies.

A. Measuring Risk and Understanding Volatility

Risk and volatility are inherent parts of investing. While risk refers to the potential for losing part or all of an investment, volatility refers to the degree of price fluctuations over time. Measuring risk helps investors understand the likelihood of adverse outcomes, while understanding volatility helps them gauge the stability or instability of asset prices.

- Volatility as a Risk Indicator: Volatility is one of the most commonly used indicators of risk. High volatility means the price of a security can change dramatically over a short period, which may offer high rewards but also high risk. Conversely, low volatility suggests more stability in the asset’s price.

- Écart type: This is a key metric used to measure volatility. It calculates the variation in an asset’s returns from its average over time. Higher standard deviation means more volatility and, therefore, more risk.

- Bêta: Beta measures how a stock’s volatility compares to the market as a whole. A beta of 1 indicates that the stock moves with the market. A beta greater than 1 implies higher volatility, while a beta less than 1 suggests lower volatility.

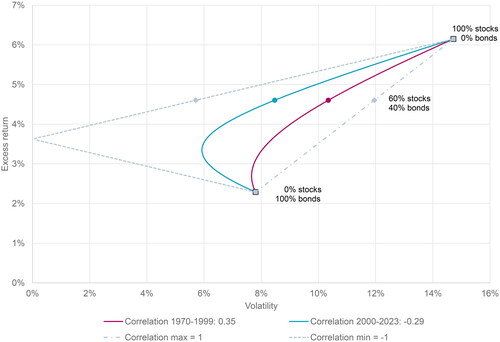

Chiffre: Correlation Between Stocks and Bonds: Historical vs. Recent (1970-2023)

Description:

The chart illustrates the relationship between excess return et volatilité of different portfolios composed of stocks and bonds over two distinct periods: 1970-1999 (represented in red) and 2000-2023 (represented in blue). The chart shows how changes in correlation between stocks and bonds affect the portfolio’s risk-return profile. The curved lines indicate the optimal portfolio mix for each period, with labeled points highlighting key combinations such as 100% stocks, 60% stocks/40% bonds, et 0% stocks/100% bonds. The dotted lines represent maximum and minimum correlations between stocks and bonds.

Points clés à retenir:

- From 1970 to 1999, the correlation between stocks and bonds was positive (0.35), indicating that stocks and bonds tended to move together.

- From 2000 to 2023, the correlation between stocks and bonds became negative (-0.29), suggesting that they often moved in opposite directions.

- Le negative correlation observed in recent years offers better diversification benefits, reducing portfolio volatility.

- The optimal 60/40 stocks-bonds portfolio provides a balanced risk-return trade-off, with lower volatility compared to an all-stock portfolio.

Application des informations :

Comprendre le changing correlation between stocks and bonds helps investors adjust their asset allocation strategies. During periods of negative correlation, a mix of stocks and bonds can enhance diversification du portefeuille, offrant risk reduction without significantly compromising returns. This insight is valuable for investors looking to build resilient portfolios that can adapt to varying market conditions and improve overall risk-adjusted performance.

B. Personal Risk Tolerance

Personal risk tolerance refers to the level of risk an individual is comfortable taking when investing. Understanding risk tolerance is crucial for creating a portfolio that aligns with an investor’s goals, financial situation, and emotional comfort with market fluctuations.

- Assessing Risk Tolerance: Risk tolerance varies from person to person, influenced by factors such as age, investment goals, income, and personal circumstances. Younger investors may have higher risk tolerance due to a longer time horizon, while retirees may prefer less risk and focus on capital preservation.

- Emotional Comfort with Risk: It’s important to assess how comfortable an investor is with market volatility. Some may panic during downturns and sell investments at a loss, while others may be able to ride out market volatility for long-term gains.

- Balancing Risk and Reward: Higher-risk investments, such as stocks, offer the potential for higher returns but also greater potential for losses. Low-risk investments, such as bonds or cash equivalents, provide more stability but typically offer lower returns. Investors must find a balance between risk and reward that matches their risk tolerance.

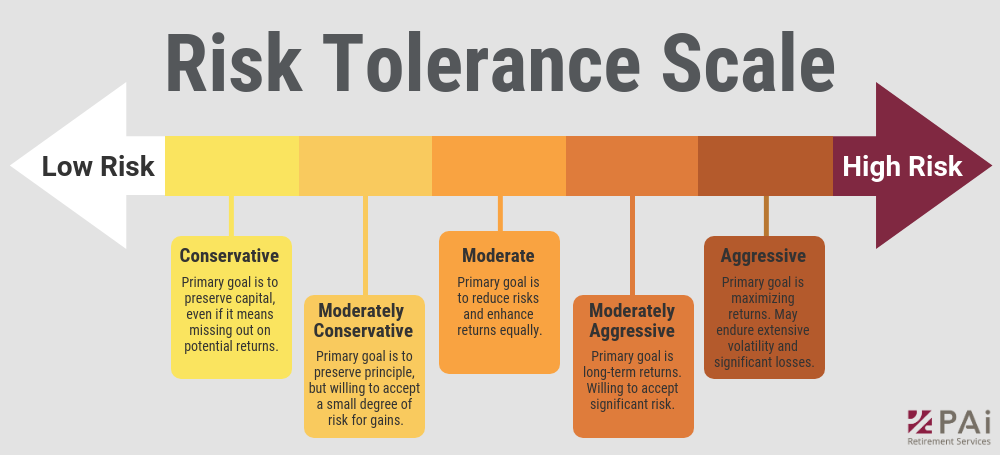

Chiffre: Risk Tolerance Scale

Description:

Cette figure représente un risk tolerance scale ranging from low risk à high risk, represented by an arrow that moves from left to right. The scale categorizes risk tolerance into five levels: Conservative, Moderately Conservative, Moderate, Moderately Aggressive, et Aggressive. Each level includes a brief description of the primary investment goal and willingness to accept risk vs. return. The conservative side focuses on preserving capital, while the aggressive side aims for maximizing returns, with a willingness to endure higher volatility.

Points clés à retenir:

- investisseurs conservateurs prioritize capital preservation and are less concerned with returns.

- Moderately conservative investors seek to preserve capital while accepting limited risk for small gains.

- Moderate investors balance risk and returns equally.

- Moderately aggressive investors focus on long-term growth, accepting significant risk.

- Investisseurs agressifs aim for maximum returns, willing to face extensive volatility and potential losses.

Application des informations :

Understanding your tolérance au risque helps determine an appropriate stratégie d'investissement. It is crucial to align your portfolio with your objectifs financiers, time horizon, et comfort level regarding potential losses. This framework can guide decisions, helping to create a well-balanced portfolio tailored to personal preferences and financial objectives.

C. Risk Measurement Techniques

Risk measurement techniques help investors quantify and manage the risks in their portfolios. Here are some of the most commonly used techniques:

- Valeur à risque (VaR): VaR estimates the potential loss in an investment portfolio over a given period for a certain level of confidence. For example, a 5% VaR of $1 million means there is a 5% chance the portfolio will lose more than $1 million over the specified period.

- Ratio de Sharpe: Le Rapport de netteté measures the risk-adjusted return of an investment by comparing its excess return over a risk-free asset to the investment’s volatility. A higher Sharpe ratio indicates better risk-adjusted performance.

- Maximum Drawdown: This measures the largest drop from a peak to a trough in the value of a portfolio. Understanding the maximum drawdown helps investors gauge the potential worst-case scenario for their portfolio.

- Scenario Analysis and Stress Testing: These techniques evaluate how a portfolio might perform under different hypothetical scenarios, such as economic downturns, rising interest rates, or geopolitical crises.

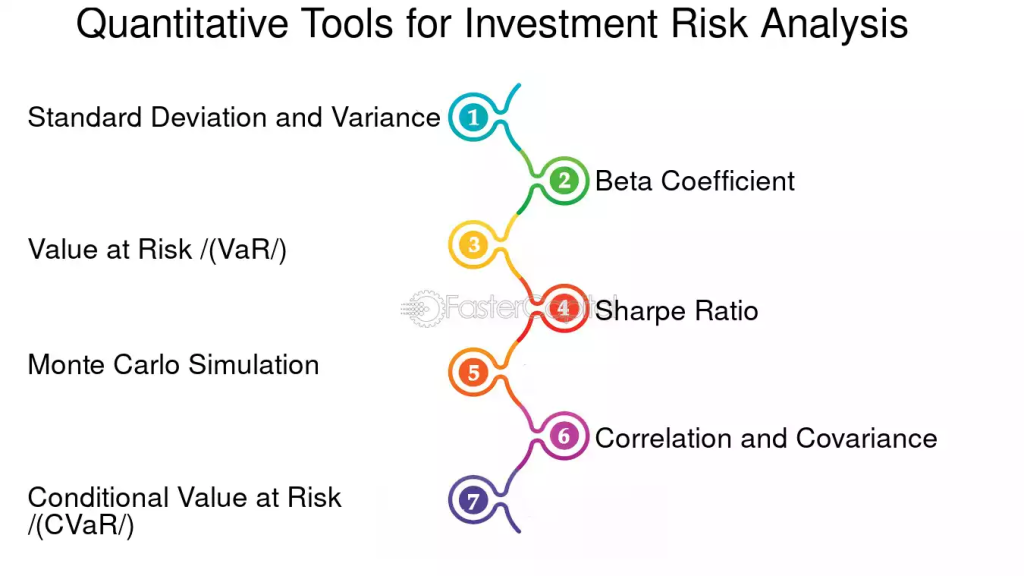

Chiffre: Quantitative Tools for Investment Risk Analysis

Description:

This diagram presents seven key tools used to measure and analyze investment risk. The tools include Standard Deviation and Variance, which assess the spread of returns; the Beta Coefficient, which measures an asset’s sensitivity to market movements; Valeur à risque (VaR), estimating potential losses in adverse conditions; and the Ratio de Sharpe, which evaluates risk-adjusted returns. Other tools include Monte Carlo Simulation for modeling potential outcomes, Correlation and Covariance for examining asset relationships, and Conditional Value at Risk (CVaR) for analyzing extreme loss scenarios.

Points clés à retenir:

- Standard Deviation and Variance provide insights into the volatility of returns.

- Le Beta Coefficient helps measure an investment’s responsiveness to overall market risk.

- Valeur à risque (VaR) et Conditional Value at Risk (CVaR) are essential for understanding potential losses during extreme market movements.

- Le Ratio de Sharpe is a valuable tool for assessing the return an investor receives per unit of risk.

- Monte Carlo Simulation et Correlation/Covariance aid in understanding potential outcomes and relationships between assets.

Application des informations :

Investors can use these tools to better understand and manage risques d'investissement by applying them to analyze the volatilité, correlation, et potential losses of their portfolios. These tools provide a foundation for making informed decisions, optimizing portfolios, and tailoring strategies based on tolérance au risque et conditions du marché.

D. Risk Categories

Investors face different types of risk, each requiring a different approach for management. Understanding the various risk categories allows investors to make informed decisions and build resilient portfolios.

- Market Risk: The risk that the value of investments will fluctuate due to market-wide factors, such as economic changes, political events, or changes in interest rates. Stocks are highly susceptible to market risk.

- Credit Risk: The risk that a bond issuer or borrower may default on its debt obligations. This is particularly relevant for bondholders and lenders. Credit risk increases with bonds issued by lower-rated companies or countries.

- Liquidity Risk: The risk that an investor will not be able to buy or sell an investment quickly enough without affecting its price. Small-cap stocks or real estate are often more affected by liquidity risk.

- Interest Rate Risk: The risk that changes in interest rates will affect the value of bonds or other fixed-income investments. Rising interest rates tend to lower the value of existing bonds, while falling rates increase bond prices.

- Inflation Risk: The risk that inflation will erode the purchasing power of investment returns. Inflation affects cash and fixed-income investments the most, as they may not keep pace with rising prices.

- Currency Risk: For international investors, currency risk arises when the value of the foreign currency in which an investment is denominated fluctuates relative to the investor’s home currency.

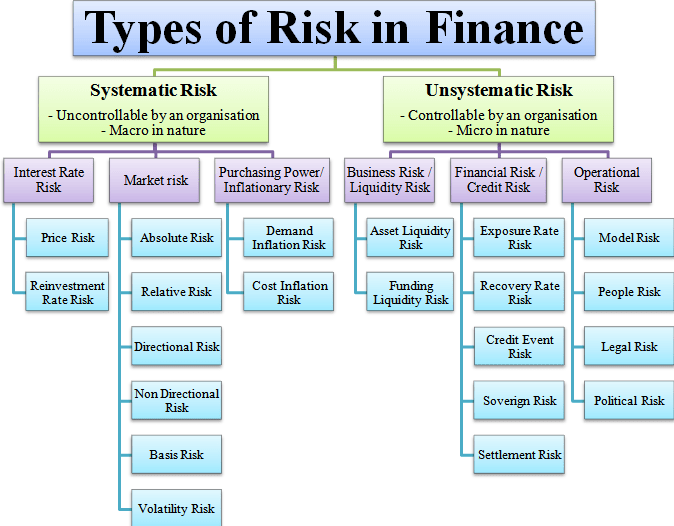

Chiffre: Types of Investment Risk: Systematic vs. Unsystematic

Description:

This diagram illustrates two primary categories of financial risk: Systematic Risk et Unsystematic Risk. Systematic Risk refers to macro-level risks that affect the entire market and are beyond the control of any organization. It includes factors like interest rate risk, market risk, et inflationary risk. On the other hand, Unsystematic Risk is specific to a company or industry and can be managed or reduced. This category includes risks such as business/liquidity risk, credit risk, et operational risk.

Points clés à retenir:

- Systematic Risk affects the entire market and cannot be eliminated by diversification.

- Interest rate risk, market risk, et inflationary risk are examples of systematic risks.

- Unsystematic Risk is specific to a company or industry and can be reduced through diversification.

- Business risk, credit risk, et operational risk fall under unsystematic risks.

- Understanding these risks helps investors in better gestion des risques et diversification du portefeuille.

Application des informations :

This information is useful for investors to differentiate between risks that can be controlled (unsystematic) and those that cannot (systematic). By knowing the types of risks, investors can develop stratégies de gestion des risques tel que diversification to mitigate unsystematic risks and enhance overall portfolio resilience.

Conclusion

Effective risk management is essential for building a strong, resilient investment portfolio. Understanding how to measure risk, assess personal risk tolerance, and apply different risk measurement techniques can help investors navigate market volatility and avoid unnecessary losses. By categorizing risks—such as market, credit, liquidity, and interest rate risks—investors can develop strategies to mitigate those risks and achieve long-term financial goals. Diversifying investments across asset classes and geographic regions remains one of the most effective ways to manage risk while maximizing returns.

Informations clés sur la leçon :

- Volatility is a key indicator of risk. High volatilité means an investment’s price moves a lot and can bring higher rewards or bigger losses. Tools like standard deviation et beta help measure how risky or stable an investment is.

- Personal risk tolerance shapes your investment choices. Some people are more comfortable with risk, while others prefer stability. Using a risk tolerance scale—from conservative to aggressive—helps match your investments to your comfort level and goals.

- Risk measurement tools help you plan for uncertainty. Valeur à risque (VaR) estimates possible losses in bad markets. The Ratio de Sharpe shows how much return you get for each unit of risk. Scenario analysis helps you see how your portfolio might perform in real-world events.

- Different risk categories need different strategies. Market risk affects all investments and can’t be avoided, but unsystematic risks, like credit or business risk, can be reduced through diversification. Knowing the difference helps you build a stronger portfolio.

- The relationship between stocks and bonds changes over time. From 2000 to 2023, stocks and bonds had a negative correlation, meaning when one dropped, the other often rose. This made a balanced 60/40 portfolio more effective for reducing volatility while maintaining good returns.

Déclaration finale :

Understanding how to measure and manage risk helps you stay in control of your investments. This section provides the tools and knowledge you need to make more confident and informed decisions in any market condition.