Global : Comprendre les options de crédit et de prêt

Objectifs d'apprentissage de la leçon :

Introduction:

This section covers credit and loan options, focusing on how to manage them effectively. By understanding different credit products, their costs, and risks, users will be able to make informed borrowing decisions that align with their financial goals.

- Understand credit card usage and its costs: Learn about credit card benefits, interest rates, and fees. This will help users make responsible choices, avoid high-interest debt, and build good credit.

- Identify factors affecting borrowing costs: Discover how interest rates, loan terms, credit scores, and inflation influence borrowing costs. This will guide users in selecting appropriate loan options and managing debt more effectively.

- Compare secured and unsecured loans: Learn the differences between secured and unsecured loans, including collateral requirements, interest rates, and risks. Users will gain the knowledge needed to choose the best loan type based on their needs.

- Apply financial knowledge to real-life scenarios: Use insights about credit cards and loans to manage debt wisely, plan purchases, and make sound financial decisions.

A. Credit Cards: Costs and Benefits

Credit cards are a convenient financial tool that offers flexibility in spending and managing short-term cash flow, but they come with both frais et avantages. Credit cards allow users to borrow money for purchases and repay it later, often with a grace period before interest is charged. However, credit cards often come with high-interest rates on unpaid balances, making them an expensive form of borrowing if not managed responsibly.

- Costs: The primary cost associated with credit cards is the taux d'intérêt on unpaid balances. Most credit cards charge annual percentage rates (APR) that can range from 10% to 25%, depending on the card issuer, the user’s credit score, and the country of issuance. In the Eurozone, credit card interest rates are regulated but can still be high, particularly for consumers with low credit scores. Other costs may include annual fees, late payment fees, cash advance fees, et foreign transaction fees for purchases made outside the Eurozone.

- Avantages: Credit cards provide convenience, protection des consommateurs, and opportunities to build or improve scores de crédit. Some cards offer rewards programs like cashback, points, or travel miles. Additionally, in the Eurozone and globally, consumers benefit from fraud protection laws that limit liability in cases of unauthorized transactions. Credit cards can also serve as a short-term credit option when used responsibly, allowing users to make larger purchases and spread payments over time.

Example: If a consumer in France uses a credit card for a €1,000 purchase and pays it off in full before the due date, no interest will be charged. However, if the consumer only pays the minimum monthly amount, interest could accumulate at 20%, leading to significant costs over time.

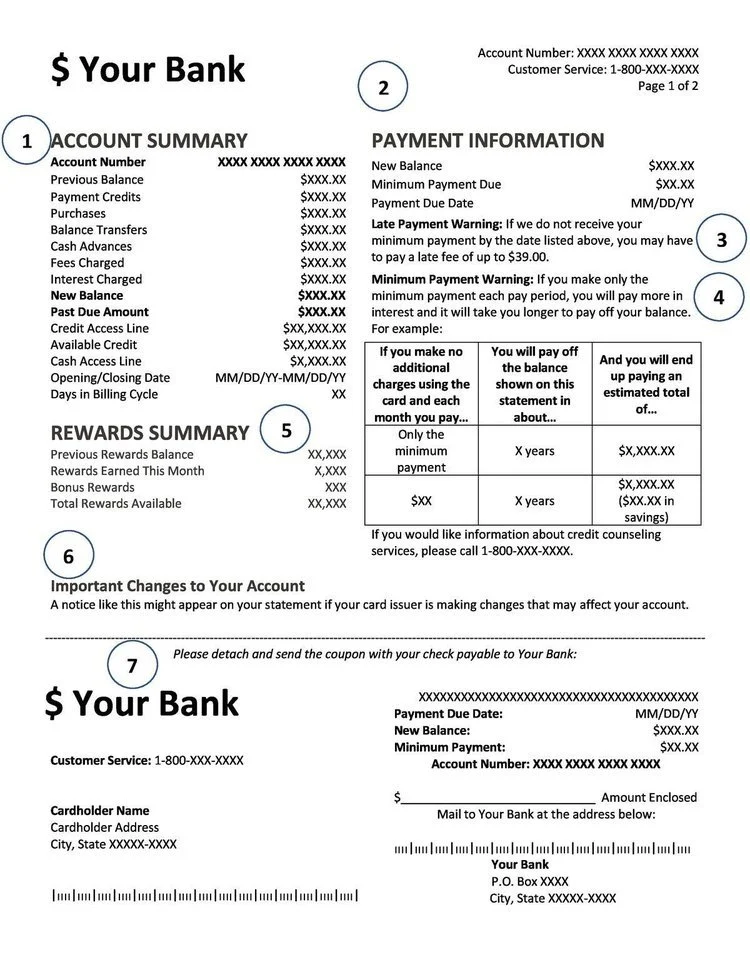

Chiffre: Credit Card Statement Overview

Description:

The figure shows a standard credit card statement layout, detailing important sections such as account summary, payment information, and rewards summary. It highlights key information including the new balance, minimum payment due, payment due date, and a breakdown of charges, credits, and available credit. Additionally, the statement warns users about late payment fees and provides instructions for making payments by mail.

Points clés à retenir:

- Account summary provides a snapshot of your credit card activity, showing new balances and any past due amounts.

- Payment information highlights the minimum payment required and the due date to avoid late fees.

- Late payment warnings alert cardholders about potential fees if the minimum payment is not made on time.

- Rewards summary informs users of rewards earned, including any bonus rewards and total rewards available.

- Important changes section informs users of updates to their account or cardholder agreement.

Application des informations :

Understanding a credit card statement helps users manage their finances effectively by tracking spending, staying aware of due dates, and avoiding unnecessary fees. It is also useful for budgétisation and ensuring that credit usage remains within limits, which can help maintain a good cote de crédit.

B. Factors Influencing Borrowing Costs

Le coût de l'emprunt varies depending on several factors, including the taux d'intérêt, le term of the loan, and the borrower’s creditworthiness. Understanding these factors helps consumers make more informed decisions about when and how to borrow.

- Taux d'intérêt: Interest rates are the primary cost of borrowing and can be either fixé ou variable. In the Eurozone, interest rates on loans are influenced by the Banque centrale européenne (BCE), which sets base rates that affect borrowing costs across the region. A low ECB rate can lead to cheaper loans, while high base rates can increase borrowing costs.

- Loan Term: The length of time over which a loan is repaid also affects its total cost. Longer loan terms typically mean lower monthly payments, but they result in higher total interest payments over time.

- Creditworthiness: A borrower’s cote de crédit significantly influences the interest rate they receive. Borrowers with higher credit scores typically qualify for lower interest rates because they represent a lower risk to lenders. In the Eurozone, credit scores are assessed based on past borrowing and repayment behavior, similar to global standards, but the systems used to calculate credit scores may vary by country.

- Inflation: Taux d'inflation can affect the real cost of borrowing. In periods of high inflation, the value of borrowed money decreases over time, benefiting borrowers with fixed-rate loans. However, during periods of low inflation or deflation, the opposite may occur, making debt more costly in real terms.

Example: If inflation rises in Germany while a borrower has a fixed-rate mortgage, the real value of their loan payments decreases over time, making it easier to repay.

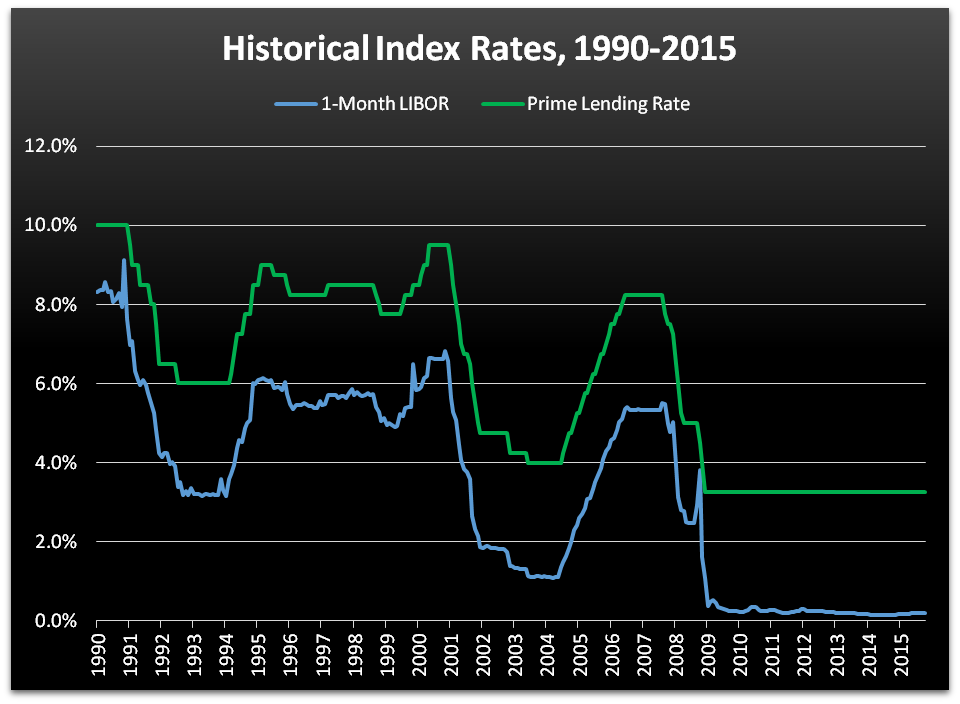

Chiffre: Historical Index Rates, 1990-2015

Description:

The graph shows a comparison between the 1-Month LIBOR (London Interbank Offered Rate) and the Prime Lending Rate from 1990 to 2015. It highlights how these two rates have fluctuated over time, with both experiencing significant declines, especially during the late 2000s financial crisis. The Prime Lending Rate generally remained higher than the LIBOR throughout the period, with noticeable drops during economic downturns.

Points clés à retenir:

- 1-Month LIBOR et Prime Lending Rate are key indicators of short-term borrowing costs.

- Both rates have shown a declining trend over time, especially during economic recessions.

- Le LIBOR rate is typically lower than the Prime Lending Rate, reflecting interbank lending rates.

- Significant drops, especially around 2008, indicate responses to the financial crisis and central bank interventions.

- Stabilité in rates can be seen after periods of economic recovery.

Application des informations :

Understanding historical index rates is useful for analyzing interest rate trends and how they affect loan products. Investors and borrowers can use this information to predict borrowing costs and make decisions regarding fixed vs. variable interest rates. It also helps in understanding the broader economic cycles and monetary policies influencing rates.

C. Secured vs. Unsecured Loans

Loans can be categorized as either secured ou unsecured, and each type has different implications for both the borrower and the lender.

- Secured Loans: A secured loan is backed by collateral, such as a house (in the case of a mortgage) or a car (for an auto loan). The lender has the right to seize the collateral if the borrower defaults on the loan. Secured loans typically offer taux d'intérêt plus bas because they present less risk to the lender. In the Eurozone, mortgages are a common form of secured loan, and the loan-to-value (LTV) ratio often determines the amount of collateral required.

Euro-Specific Item: In some Eurozone countries, green mortgages are available, which offer better rates for environmentally friendly homes. These products are gaining popularity due to the EU’s focus on sustainability. - Unsecured Loans: Unsecured loans do not require collateral and are typically granted based on the borrower’s cote de crédit et revenu. Because they carry more risk for the lender, they often come with taux d'intérêt plus élevés and stricter lending conditions. Prêts personnels et cartes de crédit are common types of unsecured loans. In both the Eurozone and globally, unsecured loans are widely used for smaller purchases or to consolidate debt.

Example: A borrower in Spain might take out a €20,000 secured loan to purchase a car. If they fail to make payments, the lender can repossess the vehicle. Conversely, if the borrower takes out a €5,000 unsecured personal loan for home improvements and defaults, the lender cannot seize any property but can pursue legal action to recover the debt.

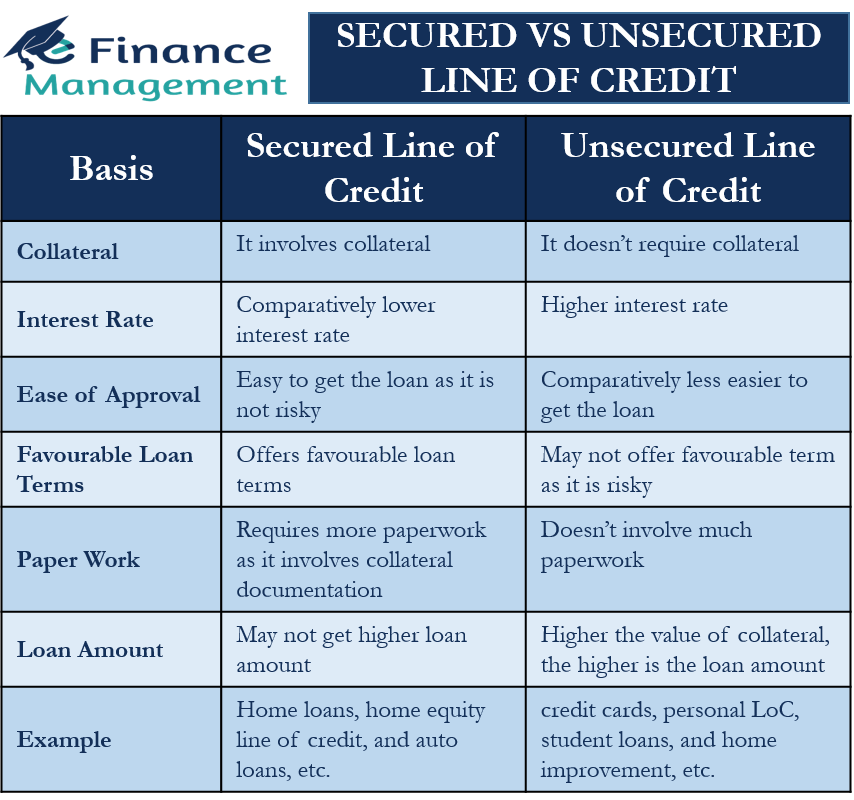

Figure: Secured vs Unsecured Line of Credit

Description:

The figure compares secured and unsecured lines of credit based on various factors such as collateral, interest rate, ease of approval, loan terms, paperwork, and loan amount. A secured line of credit requires collateral and generally offers lower interest rates, easier approval, and more favorable loan terms. In contrast, an unsecured line of credit does not require collateral but tends to have higher interest rates and may be harder to obtain due to the increased risk for the lender.

Points clés à retenir:

- Secured lines of credit require collateral, leading to taux d'intérêt plus bas and easier approval.

- Unsecured lines of credit avoir taux d'intérêt plus élevés due to the absence of collateral and involve less paperwork.

- Loan terms tend to be more favorable with secured options because they are less risky for lenders.

- Secured loans are more suitable for larger loan amounts, while unsecured loans may have lower limits.

- Examples include home loans for secured and cartes de crédit for unsecured lines of credit.

Application des informations :

Understanding the difference between secured and unsecured lines of credit helps individuals make informed decisions when choosing a loan. For large purchases or long-term financing, secured loans might be more cost-effective due to lower interest rates. On the other hand, unsecured loans can be beneficial for smaller, short-term financial needs where collateral is not available.

Informations clés sur la leçon :

- Credit card costs and benefits: Credit cards offer convenience and rewards but often come with high-interest rates if balances are not paid in full. Paying off the balance promptly can help users avoid unnecessary interest costs and maintain a good credit score.

- Factors that influence borrowing costs: Interest rates, loan terms, and credit scores all affect the cost of borrowing. Understanding these factors helps users find better loan deals and manage their debt efficiently.

- Secured vs. unsecured loans: Secured loans require collateral, usually resulting in lower interest rates, while unsecured loans do not require collateral but have higher interest rates. Choosing the right type of loan depends on the user’s financial situation and borrowing needs.

- Managing credit responsibly: By knowing how credit cards and loans work, users can budget better, control spending, and avoid excessive debt. Responsible credit use helps improve credit scores and offers more financial flexibility.

- Applying knowledge for better decisions: Understanding credit options and borrowing costs allows users to make smarter financial choices, manage debt effectively, and achieve long-term financial goals.