Local: Understanding Financial Products and Integrating Sustainability Preferences

Lesson Learning Objectives:

Introduction:

This section explores financial products available in the EU and emphasizes integrating sustainability into financial decisions. By understanding these products and aligning them with personal values, consumers can achieve both financial goals et ethical standards.

- Identify Different Financial Products: Renseignez-vous sur le various financial products and services offered in the EU, from traditional banking to modern digital financial solutions. This understanding helps consumers make informed choices based on their financial goals and needs.

- Understand the Role of Sustainability in Finance: Discover how sustainable financial products like green bonds et ESG funds align with personal values. Integrating sustainability into financial decisions enables consumers to support ethical practices while working toward financial stability.

- Regularly Reassess Financial Products: Understand why it’s important to periodically review and adjust financial products. This helps maintain relevance to changing personal circumstances, financial goals, and market conditions.

- Balance Financial and Ethical Goals: Learn how to use disclosure documents, sustainability labels, and standards to align financial choices with both ethical considerations and financial returns. This knowledge ensures informed decisions that support long-term sustainability.

Introduction

In today’s financial landscape, consumers in the European Union (EU) have access to a wide range of financial products and services designed to meet diverse needs. As the market evolves, there is a growing demand for financial solutions that not only deliver returns but also align with personal values, particularly in the realm of sustainability. This chapter explores the types of financial products available across the EU, the role of personal preferences in selecting them, and the increasing importance of integrating sustainability into financial decision-making.

Sustainability is no longer a peripheral consideration in finance; it has become central to both personal and institutional financial strategies. From green bonds to eco-friendly insurance options, financial products are now being tailored to meet the growing consumer demand for Environmental, Social, and Governance (ESG) standards. This chapter highlights how individuals can navigate these choices, balance financial goals with personal values, and ensure their financial products support long-term sustainability objectives. Additionally, it provides insights into how consumers can periodically reassess their financial choices to ensure that their portfolios continue to meet both financial and ethical standards as personal circumstances and market conditions evolve.

Understanding the available financial products and how sustainability plays a role in their development empowers consumers to make informed decisions that align with both their financial goals and their commitment to environmental and social responsibility.

Types of Financial Products and Services

Financial consumers in the EU have access to a wide range of financial products and services, from traditional banking and insurance products to modern digital solutions. These products can vary significantly across different regions and Member States, offering unique features based on local regulations, economic factors, and consumer needs.

- Digital Financial Services: With the rise of FinTech, many financial services are now available digitally, offering convenience and efficiency. These include online savings accounts, digital wallets, et mobile investment platforms. However, some financial products are still only available in certain regions or through traditional financial institutions.

- Example: A consumer in France might access savings accounts through traditional banks, while consumers in the Netherlands may have additional digital options through FinTech platforms like bunq.

- Example: A consumer in France might access savings accounts through traditional banks, while consumers in the Netherlands may have additional digital options through FinTech platforms like bunq.

- Key Features to Consider: When choosing financial products, consumers should consider several important features, such as fees, taux d'intérêt, risk levels, liquidity, et sustainability. Each product’s characteristics will determine its suitability based on individual and household financial goals.

- Example: A consumer comparing pension plans may prioritize low fees, high returns, and investment in sustainable funds, depending on their long-term goals and preferences.

- Example: A consumer comparing pension plans may prioritize low fees, high returns, and investment in sustainable funds, depending on their long-term goals and preferences.

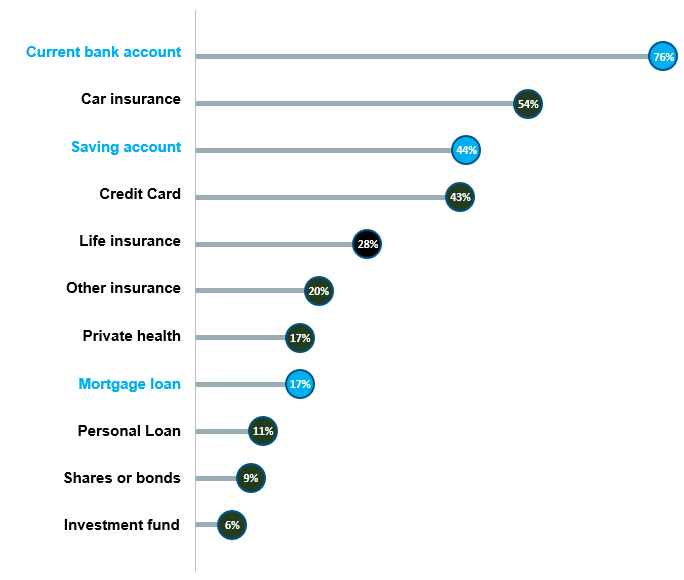

Figure: Prevalence of Selected Financial Products in the EU

Description:

The figure displays the percentage of the population aged 15 and above in the EU who use various financial products. The most commonly used product is a current bank account (76%), followed by car insurance (54%) and saving accounts (44%). Other products such as credit cards (43%), life insurance (28%), and private health insurance (17%) show varying levels of usage. Financial products like shares or bonds et investment funds are the least prevalent, with only a small segment of the population engaging in them.

Points clés à retenir:

- Current bank accounts are the most widely held financial product in the EU, showing the basic need for banking services.

- Insurance products, including car, life, and health insurance, are also quite prevalent, indicating a focus on risk management.

- Savings accounts et credit cards are common, reflecting a blend of saving and credit usage among individuals.

- Investment products such as shares, bonds, and funds have low participation, suggesting limited engagement in investment markets by the general population.

Application des informations :

Understanding the prevalence of financial products can help financial institutions target their services effectively. For investors, it highlights areas where financial literacy can be improved, especially concerning investment products. It also indicates trends that may affect demand for various financial services across the EU.

Personal Preferences and Financial Products

When selecting financial products, individuals must account for personal and household factors, including economic, sustainability, and cultural preferences. Each person’s financial goals and values will affect the types of products that are most appropriate.

- Economic and Cultural Preferences: Some financial products are designed to meet specific economic or cultural preferences, such as Islamic finance products that comply with Sharia law or community-based lending circles. Consumers should choose products that align with their personal and cultural beliefs while also supporting their financial goals.

- Example: A consumer in Germany may opt for an ethical investment fund that avoids industries like tobacco or weapons manufacturing due to personal values.

- Example: A consumer in Germany may opt for an ethical investment fund that avoids industries like tobacco or weapons manufacturing due to personal values.

- Sustainability Preferences: Increasingly, financial products are integrating sustainability factors, including environmental, social, and governance (ESG) criteria. Individuals who prioritize sustainability can choose products that align with these preferences, such as green bonds, sustainable pensions, or eco-friendly insurance options.

- Example: A consumer may prefer a pension fund that invests in companies committed to reducing their carbon footprint, contributing to climate goals while securing their financial future.

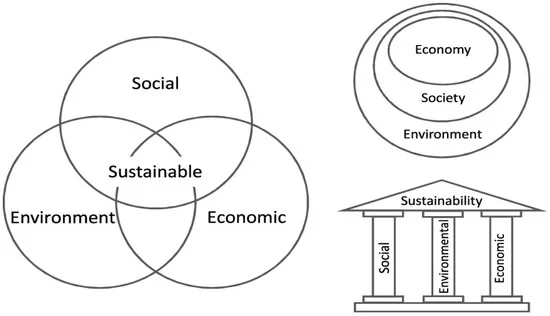

Chiffre: Sustainability Frameworks

Description:

The image illustrates three different representations of the concept of sustainability, highlighting the social, environmental, et economic dimensions. The Venn diagram shows how these three areas intersect to form a central area of “Sustainable,” indicating that true sustainability occurs when all three aspects are balanced. The concentric circles suggest a layered approach, where the économie exists within society, and both are dependent on the environment. The pillar diagram depicts sustainability as a structure supported equally by social, environmental, and economic pillars, emphasizing that all are essential to maintain stability.

Points clés à retenir:

- Sustainability requires a balance of social, economic, and environmental factors.

- Le Venn diagram shows that sustainability lies at the intersection of all three aspects.

- Le concentric circles highlight the dependence of the economy and society on the environment.

- Le pillar model emphasizes that weakening one pillar can destabilize the entire sustainability structure.

Application des informations :

Understanding the three dimensions of sustainability helps investors and businesses prioritize projects that do not harm social, environmental, or economic aspects. It is crucial for making long-term investment decisions that promote responsible growth. This framework is also useful for evaluating companies’ sustainability initiatives, guiding investment in firms that contribute positively to social responsibility, environmental health, and economic development.

Reassessing Financial Products Over Time

Financial services and products evolve, and so do personal circumstances. Periodically reassessing the suitability of financial products is essential for ensuring that they continue to meet individual needs and preferences.

- Reviewing Product Suitability: Financial products such as pensions, investissements, et savings accounts should be reviewed periodically, especially in response to changes in personal circumstances (e.g., job changes, marriage, or economic downturns). Adjustments may be necessary to account for changing financial goals or risk tolerance.

- Example: A consumer might shift from a high-risk investment fund to a more conservative option as they approach retirement.

- Example: A consumer might shift from a high-risk investment fund to a more conservative option as they approach retirement.

- Evaluating Costs and Provider Performance: Consumers should also review the costs associated with financial products and the quality of service provided. If fees become uncompetitive or service declines, it may be time to consider switching providers.

- Example: A consumer might decide to switch from a high-fee mutual fund to a low-fee index fund to improve long-term returns.

- Example: A consumer might decide to switch from a high-fee mutual fund to a low-fee index fund to improve long-term returns.

- Changing Providers: If a product no longer meets expectations or market conditions change, consumers should feel confident to change providers or negotiate better terms. Financial service providers can often improve conditions when faced with competition.

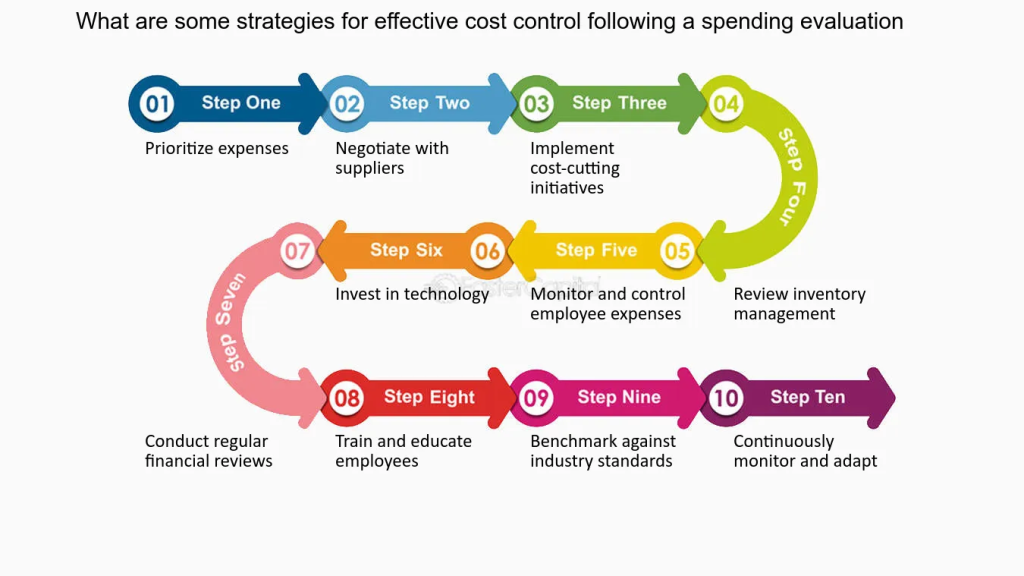

Figure: Strategies for Effective Cost Control

Description:

The image outlines a ten-step strategy for managing and controlling costs following a spending evaluation. Each step provides a clear and systematic approach, starting from prioritizing expenses and negotiating with suppliers, to investing in technology, conducting financial reviews, and continuously adapting strategies. It highlights a comprehensive cycle of actions designed to maintain financial health within an organization.

Points clés à retenir:

- Prioritize expenses to focus on essential spending.

- Negotiate with suppliers to reduce costs without compromising quality.

- Monitor and control employee expenses to prevent unnecessary expenditures.

- Invest in technology for efficient and cost-effective solutions.

- Regularly review and benchmark against industry standards to ensure competitiveness.

Application des informations :

Implementing these cost-control strategies helps organizations maintain financial stability by identifying and minimizing unnecessary expenses. For investors, understanding how companies manage costs provides insight into their operational efficiency et long-term profitability, which can guide décisions d'investissement.

Sustainable Finance and Accountability

Sustainability is becoming a critical factor in the financial industry, with consumers increasingly demanding sustainable financial products that reflect their values. The EU has introduced regulations and standards to ensure transparency and accountability in sustainable finance.

- Sustainable Product Standards and Labels: The EU has developed a taxonomy for sustainable economic activities, which classifies environmentally sustainable activities and sets standards for financial products. Consumers can look for these labels when selecting products like green bonds ou sustainable investment funds.

- Example: A consumer looking to invest in green bonds can check if the product meets the EU’s taxonomy for environmentally sustainable activities.

- Example: A consumer looking to invest in green bonds can check if the product meets the EU’s taxonomy for environmentally sustainable activities.

- Disclosure Requirements: Financial service providers must comply with sustainability-related disclosure requirements, ensuring that consumers have access to clear and reliable information about the sustainability of financial products. This transparency helps consumers make informed decisions in line with their sustainability preferences.

- Monitoring Performance and Accountability: Consumers can hold funds accountable for their sustainability commitments by reviewing voting records and engagement efforts at annual general shareholder meetings. Monitoring the performance of ESG funds and ensuring that they align with sustainability goals is essential for maintaining trust in sustainable finance.

- Example: A consumer invested in a sustainable fund might review the fund’s annual reports to ensure it continues to meet its environmental and social objectives.

- Example: A consumer invested in a sustainable fund might review the fund’s annual reports to ensure it continues to meet its environmental and social objectives.

Figure: Environmental Objectives

Description:

The figure presents six key environmental objectives designed to promote sustainability. It includes climate change mitigation and adaptation, sustainable use of water resources, and the transition to a circular economy. It also emphasizes pollution control and the protection of healthy ecosystems, indicating a holistic approach to addressing environmental concerns.

Points clés à retenir:

- Climate change mitigation et adaptation are crucial for reducing greenhouse gas emissions and preparing for climate-related impacts.

- Sustainable water usage ensures the responsible management of marine resources.

- Transitioning to a circular economy can minimize waste and promote recycling.

- Pollution prevention is essential for maintaining clean air, water, and soil.

- Protecting ecosystems helps maintain biodiversity and natural balance.

Application des informations :

These environmental objectives can guide businesses and investors in adopting sustainable practices. Understanding these goals can help investors identify eco-friendly companies et sustainable projects that align with global environmental standards, supporting long-term growth and ethical investments.

Making Informed Decisions in Sustainable Finance

To align financial decisions with personal values, particularly in terms of sustainability, individuals should use reliable standards et disclosure information to guide their choices.

- Accessing Disclosure Documents: Investors can access disclosure documents that provide detailed information on the sustainability aspects of financial products. These documents are essential for understanding how investments align with ESG criteria and the broader sustainability goals of the fund or company.

- Researching Sustainability Standards: Financial products come with various sustainability labels and standards. Consumers should research these labels and understand their significance to ensure the products they choose meet their sustainability expectations.

- Balancing Risk and Sustainability Preferences: Consumers need to make informed decisions that balance their risk tolerance with their sustainability preferences. Some sustainable products may offer lower returns but align with ethical or environmental goals, while others might carry higher risks.

- Example: An individual with a low-risk tolerance may choose a sustainable pension fund with a moderate return that supports climate action, while someone with a higher risk tolerance might invest in renewable energy startups.

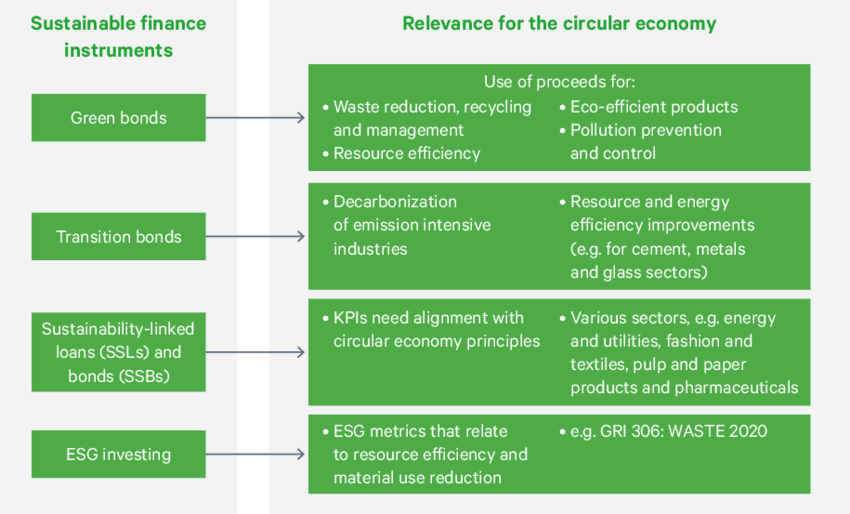

Chiffre: Sustainable Finance Instruments and Their Relevance for the Circular Economy

Description:

The figure outlines different sustainable finance instruments, such as green bonds, transition bonds, sustainability-linked loans, and ESG investing. It explains how each of these instruments contributes to the circular economy by promoting waste reduction, decarbonization, energy efficiency, and alignment with circular economy principles across various sectors.

Points clés à retenir:

- Green bonds support projects that focus on waste reduction, resource efficiency, and pollution control.

- Transition bonds help industries reduce carbon emissions and improve energy efficiency.

- Sustainability-linked loans require companies to meet KPIs that align with circular economy practices, covering diverse sectors.

- ESG investing focuses on metrics that promote resource efficiency and sustainable waste management.

Application des informations :

Understanding these instruments can help investors make sustainable investment choices that contribute to a circular economy. By recognizing how each instrument supports environmental goals, investors can identify eco-friendly projects and align their investments with sustainable development principles.

Informations clés sur la leçon :

- Variety of Financial Products in the EU: Consumers have access to a wide range of financial products, from traditional banking to digital FinTech solutions. Understanding their features, such as fees, risk, et sustainability, helps users make better financial decisions.

- Importance of Sustainability in Finance: Consumers increasingly seek sustainable financial products, tel que green bonds et eco-friendly insurance. Aligning investments with sustainability can achieve both financial returns and support for ethical standards.

- Reviewing Financial Products Regularly: It’s vital to periodically review and adjust financial products to ensure they meet evolving needs and circumstances. For example, changing from a high-risk investment fund to a safer option as retirement nears helps secure financial stability.

- Using Sustainability Labels and Standards: The EU’s sustainable finance standards provide transparency in financial products, allowing consumers to verify sustainability claims. This helps individuals select products that align with their values while managing potential risks.

- Balancing Returns and Ethics: Making informed choices in sustainable finance involves balancing risk tolerance with personal values. For instance, some sustainable products may offer lower returns but support ethical goals, while others might carry higher risks with potential for growth.

Déclaration finale :

By understanding the variety of financial products and integrating sustainability into decision-making, consumers can achieve a balance between financial growth and ethical values. Regular reassessment ensures that financial choices remain aligned with both personal circumstances and evolving market conditions, promoting long-term financial health and ethical investment.