अध्याय 14: रियल एस्टेट और गृह स्वामित्व

पाठ सीखने के उद्देश्य:

लोरेम इप्सुम डोलर सिट अमेट, कॉन्सेक्टूर एडिपिसिंग एलिट। उत एलीट टेलुस, लक्टस नेक उल्लमकोर्पर मैटिस, पुल्विनार डेपिबस लियो।

रियल एस्टेट और घर के स्वामित्व में अनुबंधों को समझना, आवास निर्णयों पर आर्थिक स्थितियों का प्रभाव और किराए पर लेने बनाम खरीदने के वित्तीय निहितार्थ शामिल हैं। रियल एस्टेट निर्णयों की जटिलताओं के माध्यम से व्यक्तियों का मार्गदर्शन करने के लिए यहां इन पहलुओं की खोज की गई है।

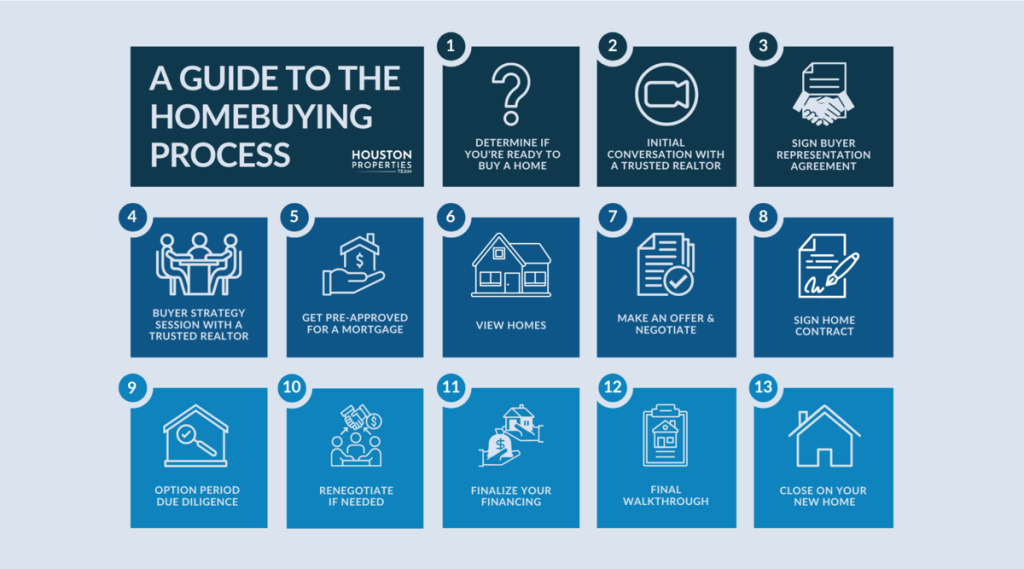

आकृति: A Guide to the Homebuying Process

विवरण:

This infographic provides a step-by-step visual guide to the homebuying process, outlining the journey from the initial thought of buying to finally receiving the keys. It breaks down the complex process into manageable stages, such as financial preparation, house hunting, and the final closing. The purpose is to demystify the experience for potential homebuyers so they know what to expect.

चाबी छीनना:

- The homebuying process starts long before you look at houses; the first step is financial preparation, which includes getting pre-approved for a mortgage to set your budget.

- A crucial phase after finding a home and having an offer accepted is the यथोचित परिश्रम period, which involves a home inspection to assess the property’s condition.

- The process involves several key professionals, including a real estate agent, a loan officer, and an inspector, who guide you through the various stages.

- The final step is the closing, where all legal documents are signed, funds are transferred, and ownership of the property officially passes to you.

सूचना का अनुप्रयोग:

- This guide acts as a valuable checklist for prospective homebuyers, helping you understand each step and stay organized throughout the purchasing journey.

- By knowing what’s coming next, you can proactively prepare your finances and documents, leading to a smoother and less stressful transaction.

- This knowledge empowers you to make more confident and informed financial decisions at every stage, from choosing the right loan to negotiating the final sale price.

14.1 Understanding Contracts

मुख्य नियम एवं शर्तें:

- अनुबंधचाहे डिजिटल हो या कागज़, उसमें अवधि, समाप्ति खंड, भुगतान शर्तें और विवाद समाधान विधियाँ जैसी महत्वपूर्ण शर्तें शामिल होती हैं। अपने अधिकारों और जिम्मेदारियों की रक्षा के लिए इन शर्तों को समझना ज़रूरी है।

अनुबंधों में, चाहे वे रियल एस्टेट लेनदेन के लिए हों या वेब एप्लिकेशन समझौतों के लिए, कई प्रमुख शर्तें शामिल होती हैं जो इसमें शामिल सभी पक्षों के दायित्वों और अधिकारों को निर्धारित करती हैं। यहाँ एक विस्तृत विवरण दिया गया है:

1. Duration

Definition: Specifies how long the contract remains valid. It includes the start and end dates, and may outline renewal conditions (automatic or optional).

उदाहरण:

A cell phone contract might state: “This agreement begins on January 1, 2025, and remains in effect until December 31, 2026. The contract will automatically renew for another 12 months unless canceled in writing 30 days prior to the expiration date.”

2. Termination

Definition: Outlines how and when either party may end the agreement before the official end date, including any penalties or notice requirements.

उदाहरण:

In a rental lease agreement: “The tenant may terminate the lease with 60 days’ written notice and payment of a $500 early termination fee. The landlord may terminate for non-payment of rent or lease violations with 30 days’ notice.”

3. Payment Terms

Definition: Describes the amounts owed, when payments are due, acceptable payment methods, and consequences for late or missed payments.

उदाहरण:

A freelance graphic designer contract might read: “The client agrees to pay $2,000 in two installments: 50% upfront, and 50% upon project completion. Late payments incur a 5% penalty after 10 business days.”

4. Dispute Resolution

Definition: Identifies the process to follow if disagreements arise, such as mediation, arbitration, or litigation, and the location where disputes will be settled.

उदाहरण:

A software subscription agreement may state: “Any disputes arising from this agreement will be resolved through binding arbitration in the state of California. The parties waive their right to a jury trial.”

5. Privacy and Sharing of Personal Information

Definition: Explains how your personal data is collected, used, stored, and whether it’s shared with third parties. Must comply with data protection laws like GDPR (EU) or CCPA (California).

उदाहरण:

A budgeting app’s privacy policy might say: “We collect your name, email address, and banking data to provide our services. We do not sell your information to third parties. You can request data deletion under the CCPA.”

⚠️ Tip: Always read these clauses before agreeing, especially in digital contracts like signing up for apps or services. Your data may be shared with partners for marketing or analytics purposes.

6. Privacy Policies and Data Sharing Terms

Definition: These terms clarify how a company collects, stores, uses, and potentially shares personal information. They often reference compliance with regulations like the General Data Protection Regulation (GDPR) in Europe or the California Consumer Privacy Act (CCPA) in the U.S.

उदाहरण:

When signing up for a social media app, you might see:

“By using our services, you agree to our privacy policy. We collect data such as your location, browsing history, and contacts. This data may be shared with advertisers to personalize your experience. You may opt out of data sharing in your settings, and request deletion of your data at any time.”

वास्तविक जीवन परिदृश्यकिसी लोकप्रिय बजट ऐप को डाउनलोड करने से पहले, जेमी नियम और शर्तों को अच्छी तरह से पढ़ती हैं, तथा गोपनीयता नीति पर ध्यान केंद्रित करती हैं, ताकि यह सुनिश्चित हो सके कि व्यक्तिगत वित्तीय डेटा सुरक्षित रहे।

14.2 Economic and Labor Market Conditions

आवास संबंधी निर्णयों पर प्रभाव:

- आर्थिक मंदी और श्रम बाजार में बदलाव आय स्थिरता को काफी हद तक प्रभावित कर सकते हैं, जिससे यह प्रभावित होता है कि व्यक्ति किराए पर रहना पसंद करते हैं या खरीदना। नौकरी की सुरक्षा एक महत्वपूर्ण विचार बन जाती है।

- तकनीकी उन्नति से नए कैरियर के अवसर पैदा हो सकते हैं और कुछ नौकरियां अप्रचलित हो सकती हैं, जिससे दीर्घकालिक आवास संबंधी निर्णय प्रभावित हो सकते हैं।

- आर्थिक मंदी व्यक्तियों को उनकी शिक्षा, अनुभव, रोजगार के प्रकार, जातीयता और लिंग के आधार पर असमान रूप से प्रभावित करती है।

- कम शिक्षा और अनुभव वाले लोग, अस्थायी या गिग श्रमिक, तथा कुछ जातीय समूहों को उच्च बेरोजगारी दर का सामना करना पड़ सकता है।

- आर्थिक लचीलापन अक्सर उच्च शिक्षा स्तर, विशिष्ट कौशल सेट और आर्थिक चक्रों के प्रति कम संवेदनशील उद्योगों से संबंधित होता है।

वास्तविक जीवन परिदृश्य: एक प्रमुख प्रौद्योगिकी कंपनी द्वारा छंटनी की घोषणा के बाद, एलेक्स ने अग्रिम भुगतान के लिए पर्याप्त बचत करने के बावजूद किराए पर रहना जारी रखने का फैसला किया, अनिश्चित नौकरी की संभावनाओं के बीच गृह स्वामित्व की तुलना में वित्तीय लचीलेपन को प्राथमिकता दी।

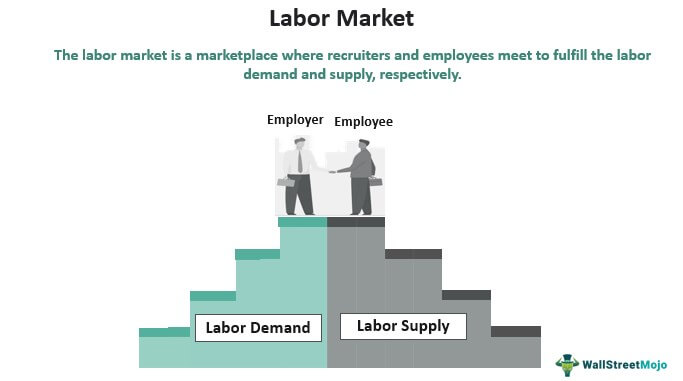

आकृति: Understanding the Labor Market

विवरण:

This image provides a clear and simple definition of the labor market, the system where employment and wages are determined. It visually represents the two core components: the supply of labor, which comes from individuals seeking work, and the demand for labor, which comes from businesses looking to hire. The graphic explains that the interaction between these two forces sets the price of labor, which is the wage level.

चाबी छीनना:

- The labor market is the broad term for the interaction between workers (supply) and employers (demand).

- The “price” of labor is the wage, which tends to increase when demand for workers is high and the supply of qualified workers is low.

- Key metrics used to analyze the health of the labor market include the बेरोजगारी की दर और यह labor force participation rate.

- A “tight” labor market, where there are more job openings than available workers, generally gives more bargaining power to employees.

सूचना का अनुप्रयोग:

- The health of the labor market is a critical indicator of the overall health of the economy, making it essential information for investors and policymakers.

- As an individual, understanding labor market trends can help you make informed career choices by identifying industries and skills that are in high demand.

- For investors, positive labor market news, such as strong job growth, often signals a growing economy, which can be beneficial for corporate profits and the शेयर बाजार.

14.3 Renting vs. Buying

वित्तीय और व्यक्तिगत विचार:

- युवा वयस्क किराये पर रहना पसंद कर सकते हैं, क्योंकि इससे उन्हें लचीलापन मिलता है, तथा वे घर के स्वामित्व के कारण दीर्घकालिक वित्तीय प्रतिबद्धता और रखरखाव की जिम्मेदारियों से बच जाते हैं।

- किराये पर लेने और खरीदने की लागत और लाभ की तुलना करने में मासिक भुगतान, घर की संभावित कीमत और व्यक्तिगत जीवनशैली संबंधी प्राथमिकताओं का विश्लेषण करना शामिल है।

किराए पर घर लेने या खरीदने का फैसला वित्तीय स्थिति, जीवनशैली संबंधी प्राथमिकताओं और दीर्घकालिक योजनाओं से प्रभावित होता है। यहाँ बताया गया है कि इनकी तुलना कैसे की जाती है:

- किराये पर लेने की अल्पकालिक लागत और लाभ:

- कम अग्रिम लागत (सुरक्षा जमा बनाम अग्रिम भुगतान)।

- चलने-फिरने में लचीलापन.

- कोई रखरखाव लागत नहीं.

- खरीदने की दीर्घकालिक लागत और लाभ:

- संपत्ति के मूल्य में वृद्धि की संभावना।

- समय के साथ इक्विटी का निर्माण होता है।

- बंधक ब्याज पर संभावित कर कटौती

वास्तविक जीवन परिदृश्य: सारा अपने शहर में किराए पर रहने और खरीदने की तुलना करती है। वह गणना करती है कि भले ही उसका मासिक बंधक भुगतान किराए से अधिक हो, लेकिन घर की इक्विटी वृद्धि की संभावना उसे वित्तीय रूप से एक दीर्घकालिक निर्णय बनाती है।

In some cases, individuals may encounter rent-to-own agreements, especially for homes or furniture. While renting-to-own offers flexibility and the chance to eventually own the property or item, it often results in paying significantly more over time compared to buying outright.

Buying a home directly builds equity and may lead to long-term financial stability, while renting (or rent-to-own) provides short-term flexibility but little or no ownership benefits until all payments are made.

प्रमुख किराया अनुबंध शब्दावली

1. Lease Term: Duration of the rental agreement

- परिभाषा: Specifies the length of time the tenant agrees to rent the property.

- उदाहरण:

A lease agreement states: “This lease shall begin on August 1, 2025, and end on July 31, 2026.”

This indicates a 12-month lease term during which both the landlord and tenant are bound by the lease conditions.

2. Security Deposit: Funds held by the landlord as insurance against damage or unpaid rent

- परिभाषा: A refundable amount paid upfront to cover potential property damage or lease violations.

- उदाहरण:

Upon signing a lease, John pays $1,200 as a security deposit in addition to his first month’s rent. When he moves out, the landlord inspects the apartment. Because John left a hole in the wall and didn’t clean the carpets, the landlord keeps $300 to cover the repairs and refunds the remaining $900.

3. Grace Period: Time allowed after the due date for rent payments without penalty

- परिभाषा: A short period during which late payments are accepted without a fee.

- उदाहरण:

A lease states: “Rent is due on the 1st of each month. A 5-day grace period is provided before late fees are applied.”

If Maria pays her rent on the 4th, she avoids a penalty; if she pays on the 6th, she owes a $50 late fee.

4. Eviction: Legal process by which a tenant is removed for violating lease terms

- परिभाषा: The formal removal of a tenant from the rental property due to non-payment or other breaches.

- उदाहरण:

After failing to pay rent for two months and ignoring multiple notices, David receives an official eviction notice from the landlord. The court sets a hearing, and eventually David is legally required to vacate the property within 10 days.

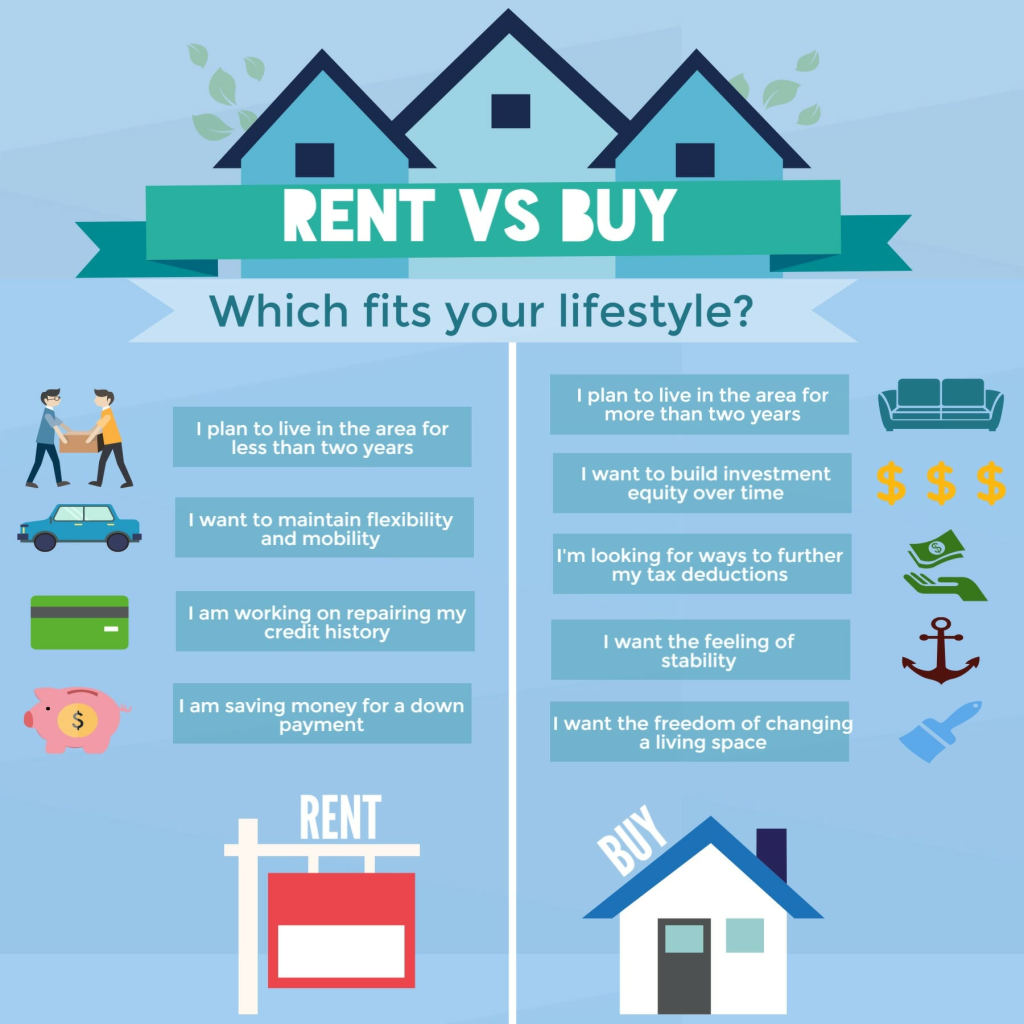

आकृति: Renting vs. Buying a Home: A Comparison

विवरण:

This image provides a side-by-side comparison of the pros and cons of renting versus buying a home. It breaks down the key differences between the two choices, focusing on factors like cost, responsibility, and financial benefits. The goal is to provide a balanced overview to help individuals make an informed decision that suits their lifestyle and financial situation.

चाबी छीनना:

- The main advantage of renting is flexibility, as it’s easier to move, and you are not responsible for maintenance costs or property taxes.

- The primary benefit of buying a home is building equity, which is a form of forced savings that helps you grow your net worth over time.

- Homeownership comes with significant additional costs beyond the mortgage payment, including repairs, insurance, and property taxes.

- The “rent vs. buy” decision is not purely financial; it is also a major lifestyle choice that depends on your long-term goals, career stability, and personal preferences.

सूचना का अनुप्रयोग:

- This framework provides a clear checklist of factors to consider when you are making the major financial decision of whether to rent or buy.

- It encourages you to analyze your complete financial picture, including your savings for a down payment and your ability to cover unexpected maintenance costs.

- By weighing these pros and cons against your personal goals and financial stability, you can make a choice that best supports your long-term financial well-being.

14.4 Mortgage Basics

सुरक्षित ऋण और बंधक:

- बंधक ये सुरक्षित ऋण हैं, जिसमें खरीदा गया घर संपार्श्विक के रूप में काम आता है। भुगतान न करने पर ऋण जब्त हो सकता है, जबकि क्रेडिट कार्ड ऋण जैसे असुरक्षित ऋण में ऐसा नहीं होता है।

- बंधक शर्तों को समझना महत्वपूर्ण है, जैसे कि फिक्स्ड-रेट बनाम एडजस्टेबल-रेट बंधक (ARMs), फिक्स्ड-रेट बंधक पूर्वानुमानित भुगतान प्रदान करते हैं, जबकि ARMs कम प्रारंभिक दरें प्रदान कर सकते हैं, लेकिन भविष्य में भुगतान बढ़ने का जोखिम पैदा करते हैं।

- खरीदी जा रही संपत्ति आम तौर पर निम्न प्रकार से कार्य करती है संपार्श्विक बंधक ऋण के लिए। इसका मतलब है कि अगर उधारकर्ता भुगतान करने में विफल रहता है, तो ऋणदाता को ऋण राशि वसूलने के लिए संपत्ति पर कब्ज़ा करने का अधिकार है।

Real-Life Scenario: Considering a stable job and a preference for predictable payments, Chris opts for a 30-year fixed-rate mortgage over an ARM when purchasing a first home, valuing long-term financial stability.

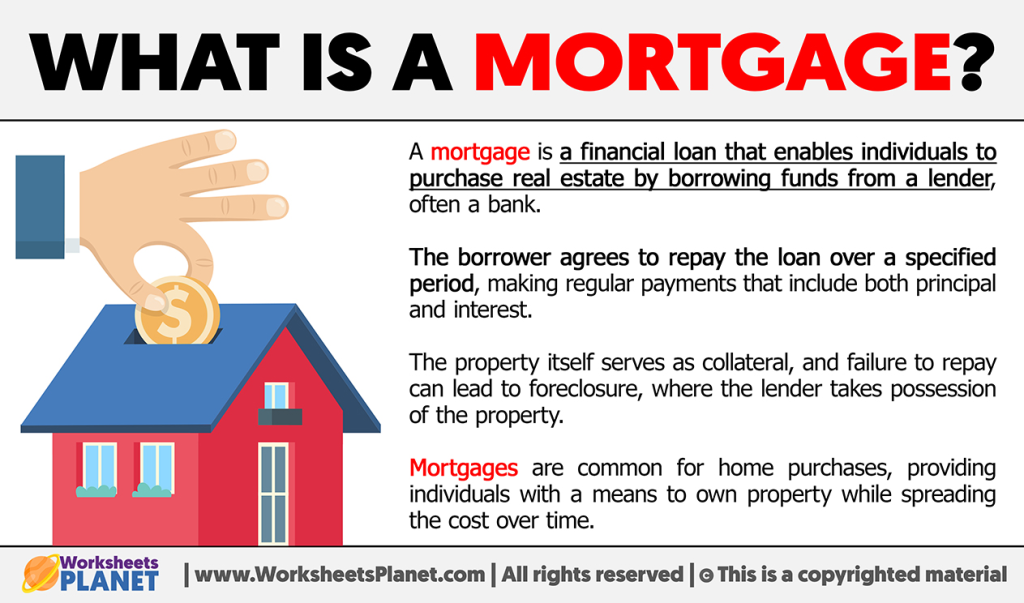

आकृति: What is a Mortgage?

विवरण:

This image provides a simple, educational overview of what a गिरवी रखना is, explaining it as a loan used to purchase a home. It likely illustrates the core relationship where a lender provides a large sum of money to a borrower, who then repays it in installments over many years. The goal is to define this fundamental financial concept in an easy-to-understand visual format.

चाबी छीनना:

- ए गिरवी रखना is a specific type of long-term loan from a bank or financial institution that helps you buy a house.

- The property you buy with the loan serves as संपार्श्विक, meaning the lender can take possession of the home if you fail to make your payments.

- Mortgages are typically repaid through regular monthly payments over a long period, commonly 15 to 30 years.

- Each monthly payment consists of two main parts: the principal (the original loan amount) and the दिलचस्पी (the cost of borrowing the money).

सूचना का अनुप्रयोग:

- Understanding the concept of a गिरवी रखना is the foundational first step for anyone aspiring to achieve homeownership.

- This knowledge is critical for assessing your financial readiness to buy a home and for comparing different loan options from various lenders.

- Grasping the long-term commitment of a mortgage helps you make a responsible and well-informed financial decision when purchasing what is likely your largest asset.

Key Mortgage Qualification Factors

When applying for a mortgage, two important financial ratios lenders consider are:

- Debt-to-Income (DTI) Ratio:

Measures how much of your monthly income goes toward debt payments.

उदाहरण: If your total debt payments are $1,800 and your monthly income is $5,000, your DTI = 36%.

Lenders typically prefer a DTI below 36%.

- Loan-to-Value (LTV) Ratio:

Compare the size of your mortgage to the home’s value.

उदाहरण: If you buy a $250,000 home with a $50,000 down payment, your loan is $200,000. Your LTV = 80%.

A lower LTV reduces lender risk and can help you avoid private mortgage insurance (PMI).

Understanding these ratios can improve your chances of qualifying for better mortgage terms.

14.5 Comparing Mortgage Payments

ऋण की अवधि | उधार ली गई राशि | ब्याज दर | मासिक भुगतान |

30 वर्ष | $250,000 | 4.0% | $1,193.54 |

15 वर्ष | $250,000 | 3.5% | $1,787.21 |

30 वर्ष | $350,000 | 4.5% | $1,773.40 |

15 वर्ष | $350,000 | 4.0% | $2,584.17 |

गणनाएँ उदाहरणात्मक हैं और निश्चित ब्याज दरों पर आधारित हैं। वास्तविक भुगतान विशिष्ट ऋण शर्तों और उतार-चढ़ाव वाली ब्याज दरों के आधार पर भिन्न हो सकते हैं।

ये उदाहरण यह प्रदर्शित करने में मदद करते हैं कि ऋण की शर्तों, राशियों और ब्याज दरों में अंतर मासिक बंधक भुगतानों को कैसे महत्वपूर्ण रूप से प्रभावित कर सकता है। लंबी चुकौती अवधि के परिणामस्वरूप आम तौर पर मासिक भुगतान कम होता है लेकिन ऋण की अवधि के दौरान कुल ब्याज का भुगतान अधिक होता है।

14.6 Homeownership Costs

घर का मालिक होने के साथ-साथ कुछ लागतें भी आती हैं, जिन पर आपको घर खरीदने के लिए बजट बनाते समय विचार करना चाहिए। इन लागतों में शामिल हैं:

- सम्पत्ति कर: स्थानीय सरकारें आपकी संपत्ति के मूल्यांकित मूल्य के आधार पर संपत्ति कर लगाती हैं। कर की दरें आपके स्थान के आधार पर अलग-अलग होती हैं और समय के साथ बदल सकती हैं। संपत्ति कर आमतौर पर सालाना या अर्ध-वार्षिक रूप से चुकाए जाते हैं और अक्सर आपके मासिक बंधक भुगतान में शामिल होते हैं।

- घर के मालिक का बीमा: Homeowner’s insurance protects you from financial losses due to damage to your property or personal liability. The cost of homeowner’s insurance depends on factors such as your home’s value, location, and coverage limits. Shop around and compare quotes from multiple insurance providers to find the best policy for your needs. Homeowners’ insurance typically covers damages to the home from events like fire, storms, theft, and certain natural disasters. It also includes liability coverage if someone is injured on the property.

- Renters’ insurance, on the other hand, covers personal belongings inside a rented property, such as clothing, electronics, and furniture, but not the building structure itself.

Both types of insurance are important for protecting against unexpected losses.

- रखरखाव एवं मरम्मत: एक गृहस्वामी के रूप में, आप अपनी संपत्ति के रखरखाव और किसी भी आवश्यक मरम्मत को संबोधित करने के लिए जिम्मेदार हैं। लॉन की देखभाल, गटर की सफाई और HVAC सर्विसिंग जैसे नियमित रखरखाव कार्य समय के साथ बढ़ सकते हैं। इसके अतिरिक्त, अप्रत्याशित मरम्मत, जैसे कि छत को बदलना या प्लंबिंग की समस्याएँ, महंगी हो सकती हैं। इन चल रहे खर्चों के लिए बजट बनाना और अप्रत्याशित लागतों को कवर करने के लिए एक आपातकालीन निधि अलग रखना आवश्यक है।

रियल एस्टेट और घर के स्वामित्व के विभिन्न पहलुओं को समझने से आपको सूचित निर्णय लेने और घर खरीदने, वित्तपोषण करने और रखरखाव की जटिल दुनिया को नेविगेट करने में मदद मिल सकती है। सरल वित्तीय समुदाय आपकी वित्तीय यात्रा में आपका समर्थन करने के लिए यहाँ है, जो आपको अपने गृहस्वामी लक्ष्यों के लिए सर्वोत्तम विकल्प बनाने में मदद करने के लिए संसाधन और मार्गदर्शन प्रदान करता है।

14.7 Tenant and Landlord Rights and Responsibilities

Rental lease agreements outline important rights and obligations:

- Tenants have the right to a safe, habitable living environment and are responsible for timely rent payments and maintaining the property.

- Landlords have the right to collect rent and expect property upkeep, but must handle repairs and maintenance promptly.

Understanding these terms protects both parties and helps prevent legal disputes.

निष्कर्ष

रियल एस्टेट और घर के स्वामित्व को आगे बढ़ाने के लिए अनुबंधों, आर्थिक स्थितियों और व्यक्तिगत परिस्थितियों पर सावधानीपूर्वक विचार करने की आवश्यकता होती है। चाहे किराए पर लेना हो या खरीदना हो, बंधक विकल्पों को समझना हो और निवेश बेंचमार्क की तुलना करना हो, सूचित निर्णय रियल एस्टेट के क्षेत्र में अधिक संतुष्टि और वित्तीय कल्याण की ओर ले जा सकते हैं।

मुख्य पाठ जानकारी:

लोरेम इप्सुम डोलर सिट अमेट, कॉन्सेक्टूर एडिपिसिंग एलिट। उत एलीट टेलुस, लक्टस नेक उल्लमकोर्पर मैटिस, पुल्विनार डेपिबस लियो।