Real Estate Financing and Mortgages

पाठ सीखने के उद्देश्य:

परिचय: This section provides a comprehensive guide to real estate financing and mortgages. Understanding these concepts is essential for making informed decisions when buying, renting, or investing in property. Learning about mortgages and the financing process helps ensure that you choose the best option for your financial situation and long-term goals.

- Understand Mortgage Basics: You will learn what a mortgage is, how it works, and the importance of amortization schedules. This knowledge will help you plan your finances effectively and understand the long-term impact of mortgage payments on your budget.

- Explore Different Types of Mortgages: You will become familiar with primary and secondary mortgages, including the roles of traditional banks, private lenders, and the secondary mortgage market. Understanding these options will allow you to choose the most suitable financing method for your property purchase or investment.

- Grasp Key Mortgage Concepts: You will learn about fixed-rate and variable-rate mortgages, the impact of interest rates, and the pros and cons of different mortgage types. This will enable you to make informed decisions about which mortgage suits your financial needs and risk tolerance.

- Consider Legal and Affordability Factors: You will gain insights into the legal aspects of mortgage agreements, the importance of budgeting, and strategies for negotiating favorable mortgage terms. This knowledge will empower you to manage your real estate finances wisely and avoid common pitfalls.

Introduction to Real Estate Financing

Real estate financing is a critical component for anyone looking to buy, rent, or invest in property. Understanding the various financing options and how they impact your overall budget is essential for making informed decisions. In this chapter, we will explore the different ways to finance real estate, how mortgages work, and key considerations for affordability when buying or renting property.

Section 1: Understanding Mortgages

What is a Mortgage?

A mortgage is a loan specifically designed for purchasing real estate. It involves borrowing money from a lender, which is then paid back over time with interest. The property itself serves as collateral for the loan. Mortgages are essential for most homebuyers because they allow individuals to purchase property without needing the full amount upfront.

आकृति: A young man using a calculator to check financial figures. The image highlights the process of financial planning and calculation.

स्रोत: iStockफोटो

:max_bytes(150000):strip_icc():format(webp)/dotdash_Final_Amortized_Loan_Oct_2020-01-3a606fa9285943098248ac92e8d03b40.jpg)

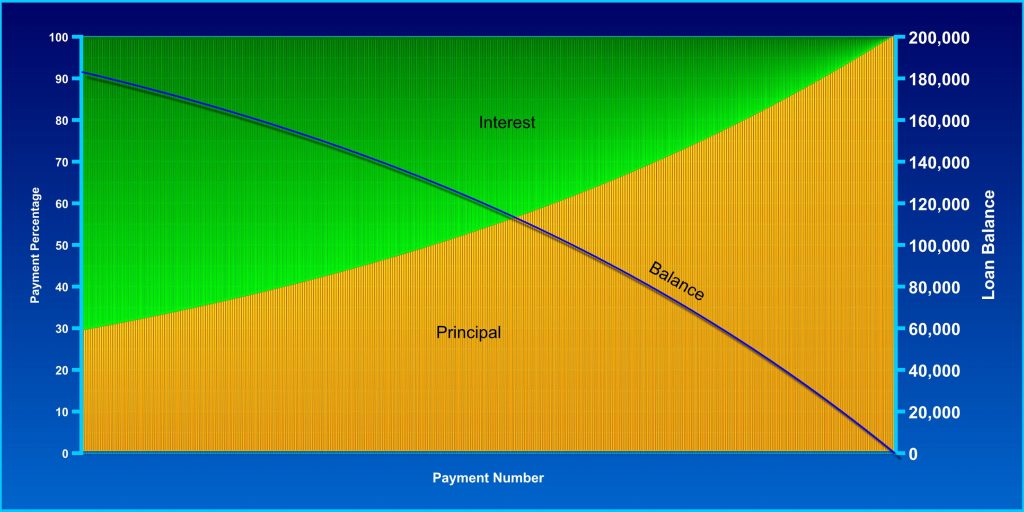

आकृति: Amortized Loan Payment Breakdown

स्रोत: Investopedia

विवरण:

The figure shows the breakdown of an amortized loan over time. It illustrates how each loan payment is divided between interest and principal repayment. In the early stages of the loan, a larger portion of each payment goes towards paying interest, while in the later stages, more of each payment goes towards repaying the principal. The graph typically shows a declining interest portion and an increasing principal portion over time.

चाबी छीनना:

- Amortization: The process by which loan payments are structured to include both interest and principal repayment.

- Interest and Principal Allocation: Early payments primarily cover interest, while later payments mostly reduce the principal.

- Payment Structure: Understanding how payments are allocated helps in planning finances and predicting future loan balances.

- Loan Term Impact: The length of the loan term affects how quickly the principal is paid down.

- वित्तीय योजना: Knowing the breakdown helps borrowers anticipate changes in their equity and outstanding loan balance.

सूचना का अनुप्रयोग:

Understanding the amortization schedule of a loan is crucial for effective financial planning. निवेशकों और उधारकर्ताओं can use this information to predict how much of each payment goes towards interest versus reducing the principal. This helps in making informed decisions about loan refinancing, budgeting, and long-term financial planning. For those learning about investing और finance, grasping the concept of amortized loans is essential for comprehending how loans impact cash flow and debt management strategies.

आकृति: Mortgage Amortization Schedule

स्रोत: Loanatik

विवरण:

The figure displays a mortgage amortization schedule, illustrating how monthly payments are split between principal and interest over the life of a loan. In the beginning, a larger portion of each payment goes towards interest, while over time, the portion applied to the principal increases. The schedule helps borrowers understand how their loan balance decreases gradually and how much interest they will pay over the loan term.

चाबी छीनना:

- Monthly Payments Breakdown: Shows the distribution of each payment into interest and principal.

- Interest Portion: Higher at the start of the loan and decreases over time.

- Principal Portion: Increases over time, leading to a gradual reduction in the loan balance.

- कुल भुगतान किया गया ब्याज: The schedule helps in understanding the total interest paid over the loan term.

- Financial Planning Tool: Useful for borrowers to plan and manage their finances better.

सूचना का अनुप्रयोग:

Understanding a mortgage amortization schedule is essential for homeowners और निवेशकों to manage their loans effectively. It allows them to see how payments affect the loan balance and the total interest paid. This information is valuable for making decisions about refinancing, planning for prepayments, and evaluating the cost of borrowing. For those learning about finance, mastering amortization schedules provides insights into debt management and long-term financial planning.

Secondary Mortgage

A secondary mortgage, also known as a second mortgage or home equity loan, is an additional loan taken out against the equity in the property. This can be used for various purposes, such as home improvements or consolidating debt. It is subordinate to the primary mortgage, meaning the primary mortgage must be paid off first in case of default.

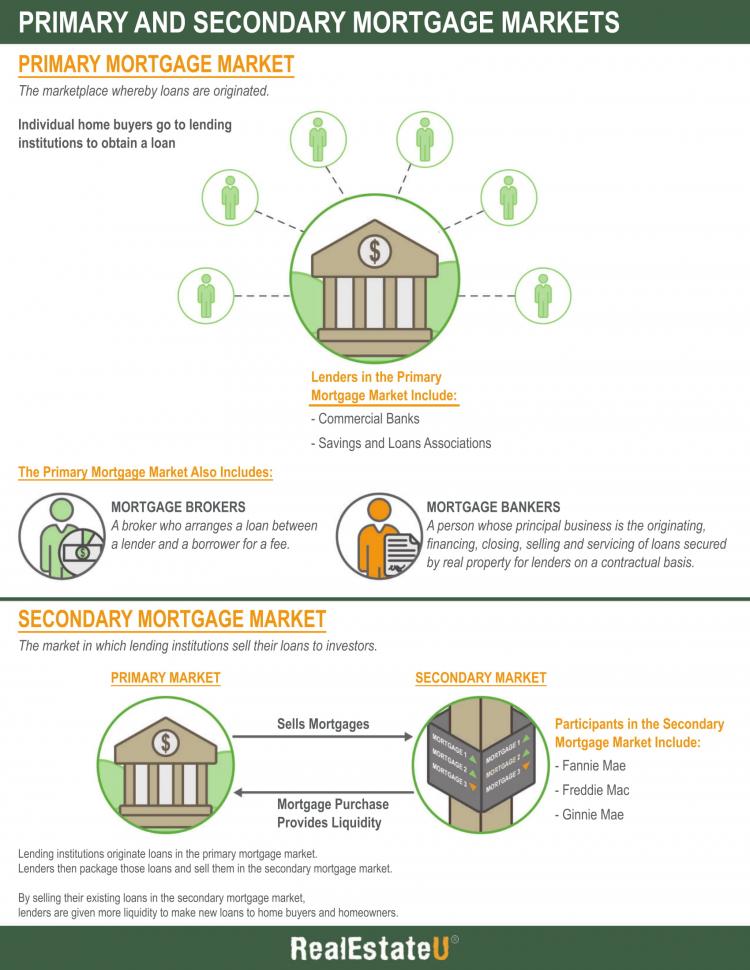

आकृति: Primary and Secondary Mortgage Markets Infographic

स्रोत: RealEstateU

विवरण:

The infographic explains the differences and functions of the primary and secondary mortgage markets. The primary mortgage market is where borrowers and lenders originate mortgage loans, while the secondary mortgage market involves the buying and selling of existing mortgages. The infographic highlights key players in each market, such as banks and credit unions in the primary market, and entities like Fannie Mae and Freddie Mac in the secondary market. It also shows how mortgages are bundled and sold as mortgage-backed securities (MBS) to investors.

चाबी छीनना:

- Primary Mortgage Market: Where mortgages are originated; key players include banks and credit unions.

- Secondary Mortgage Market: Where existing mortgages are bought and sold; involves entities like Fannie Mae and Freddie Mac.

- Mortgage-Backed Securities (MBS): Mortgages are bundled and sold to investors, providing liquidity to the primary market.

- Role of Investors: Investors in MBS provide funds that are used to originate new loans in the primary market.

- Market Functions: Both markets work together to ensure the availability and affordability of mortgage financing.

सूचना का अनुप्रयोग:

समझना primary and secondary mortgage markets is crucial for those involved in रियल एस्टेट और finance. It helps explain how mortgage loans are originated, funded, and sold, affecting interest rates and loan availability. For निवेशकों, knowledge of these markets provides insights into how mortgage-backed securities work and their impact on the broader financial system. This understanding aids in making informed decisions about real estate investments and evaluating the risks and returns associated with mortgage-backed securities.

आकृति: Customers agreeing to buy a house with a real estate agent, captured during the contract signing process. The image illustrates the formal agreement and transaction in real estate.

स्रोत: iStockफोटो

Section 2: Types of Lenders

Traditional Banks

Traditional banks are a common source of financing for real estate. They offer various mortgage products and often have strict lending criteria. These banks typically provide competitive interest rates and comprehensive customer service.

Private Lenders

Private lenders can be individuals or companies that offer loans outside of the traditional banking system. They might offer more flexible terms but often at higher interest rates. Private lending can be a good option for those who do not qualify for traditional bank loans.

द्वितीयक बाज़ार

The secondary market involves investors purchasing existing mortgages from primary lenders. This can provide liquidity to lenders and create more financing opportunities for borrowers. In this market, mortgage-backed securities are often sold to investors.

Section 3: Key Mortgage Concepts

ब्याज दर

The interest rate on a mortgage significantly impacts the total cost of the loan. It’s essential to compare rates from different lenders to find the most favorable terms. Interest rates can be fixed or variable.

Fixed-Rate Mortgages

Fixed-rate mortgages have a consistent interest rate throughout the loan term, providing stability in monthly payments. This is advantageous for budgeting, as your payments remain the same regardless of market fluctuations.

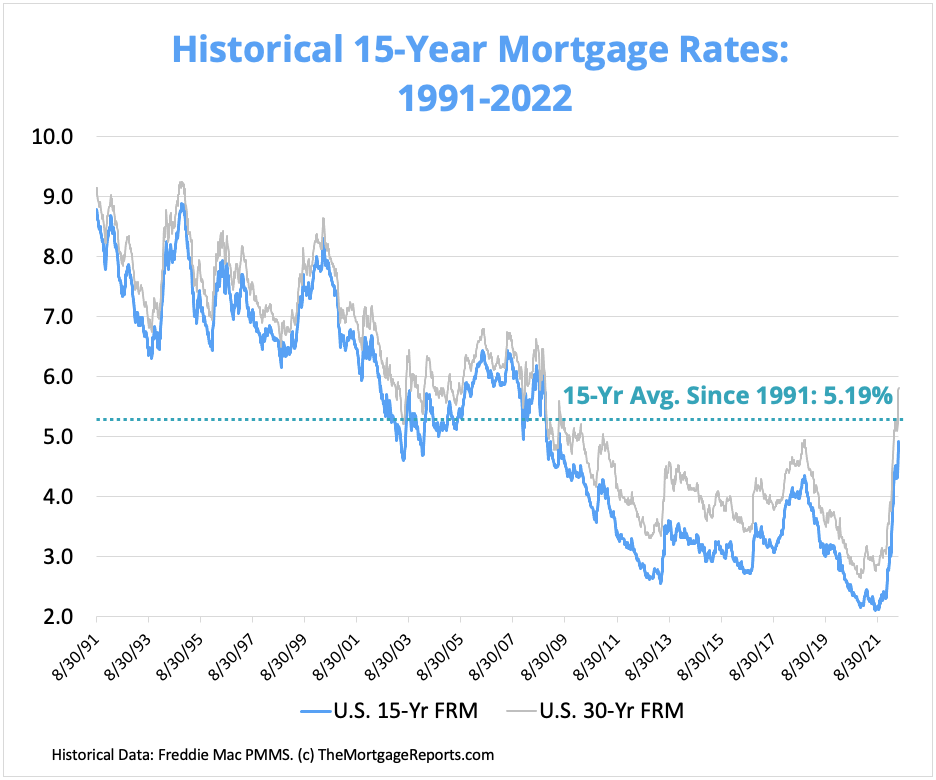

आकृति: Historical 15-Year Mortgage Rates Chart (1991 to June 2022)

स्रोत: The Mortgage Reports

विवरण:

The figure shows the historical 15-year mortgage rates from 1991 to June 2022. The chart provides a visual representation of how mortgage rates have fluctuated over the past three decades. It highlights significant peaks and troughs, reflecting changes in economic conditions, monetary policies, and market demand. The x-axis represents the years from 1991 to 2022, while the y-axis shows the mortgage rates in percentage. The trend line helps viewers understand the overall movement of interest rates over the given period.

चाबी छीनना:

- Historical Trends: Mortgage rates have experienced both high and low periods over the past 30 years.

- Economic Influence: Rates reflect broader economic conditions and monetary policy changes.

- Rate Peaks: Significant peaks can be associated with economic events or policy shifts.

- Rate Troughs: Lower rates often indicate favorable borrowing conditions and economic stability.

- Long-Term View: Understanding long-term trends helps in forecasting future rate movements and making informed borrowing decisions.

सूचना का अनुप्रयोग:

This data is useful for homebuyers और निवेशकों to understand historical mortgage rate trends, aiding in timing their real estate purchases or refinancing decisions. Financial analysts can use this information to predict future rate movements based on past trends. For those learning about finance and real estate, this chart provides a clear example of how external factors impact mortgage rates, highlighting the importance of staying informed about economic conditions and monetary policies. Understanding these trends helps in making strategic decisions about borrowing और investing.

Variable-Rate Mortgages (ARM)

Variable-rate mortgages, also known as Adjustable-Rate Mortgages (ARM), have interest rates that can change over time, which might result in fluctuating monthly payments. ARMs typically offer lower initial interest rates compared to fixed-rate mortgages, but the rates can increase over time based on market conditions.

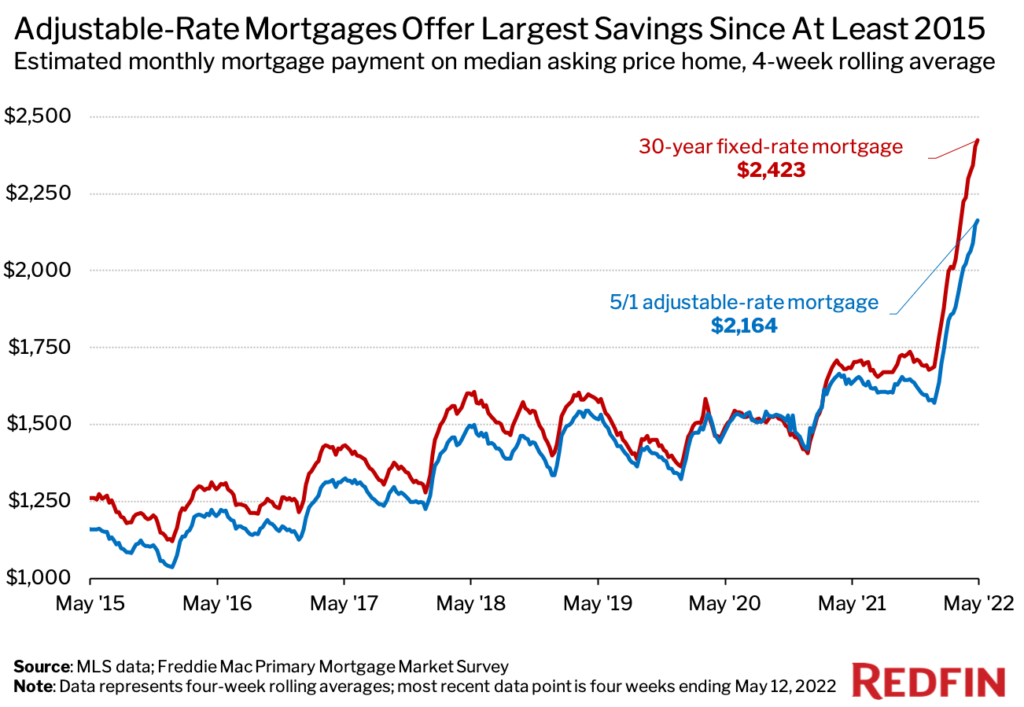

आकृति: Adjustable-Rate Mortgages (ARM) vs. Fixed-Rate Mortgages

स्रोत: Redfin

विवरण: The figure compares the interest rates and cost differences between Adjustable-Rate Mortgages (ARMs) and Fixed-Rate Mortgages from 2017 to 2022. It illustrates how the average rates for ARMs have generally been lower than those for fixed-rate mortgages during this period. The x-axis represents the years from 2017 to 2022, while the y-axis shows the interest rates. The chart provides insights into the cost-saving potential of ARMs compared to fixed-rate mortgages over time.

चाबी छीनना:

- Interest Rate Comparison: ARMs generally offer lower initial interest rates compared to fixed-rate mortgages.

- Cost Differences: The lower rates of ARMs can lead to significant cost savings, especially in the short term.

- Rate Stability: Fixed-rate mortgages provide rate stability and predictability over the loan term.

- बाजार के रुझान: The chart shows how interest rates for both types of mortgages have fluctuated over the years.

- Financial Strategy: Choosing between ARM and fixed-rate mortgages depends on individual financial situations and market conditions.

सूचना का अनुप्रयोग:

Understanding the differences between ARMs और fixed-rate mortgages is crucial for homebuyers और निवेशकों to make informed borrowing decisions. ARMs can be advantageous in a low-interest-rate environment, offering lower initial payments, while fixed-rate mortgages provide long-term stability, protecting against future rate increases. For those learning about mortgage financing, this chart highlights the importance of considering both short-term savings and long-term financial planning when choosing a mortgage type.

Section 4: Pros and Cons of Mortgages

पेशेवरों

- Homeownership: Allows individuals to own property without needing the full purchase price upfront.

- Equity Building: As you pay down your mortgage, you build equity in your home.

- Fixed Payments: Fixed-rate mortgages provide predictable monthly payments.

- कर लाभ: In some countries, mortgage interest payments can be tax-deductible.

Figure: The Pros and Cons of Mortgage Loans

स्रोत: फास्टरकैपिटल

विवरण:

The infographic outlines the pros and cons of mortgage loans for borrowers and lenders. It lists advantages such as tax benefits, fixed interest rates, and building equity, alongside disadvantages including long-term debt commitment, possible foreclosure, and interest rate variability. The infographic is divided into sections for clear understanding, making it easy to see the benefits and drawbacks for each party involved.

चाबी छीनना:

- Pros for Borrowers: Tax benefits, fixed interest rates, building equity.

- Cons for Borrowers: Long-term debt commitment, risk of foreclosure, interest rate variability.

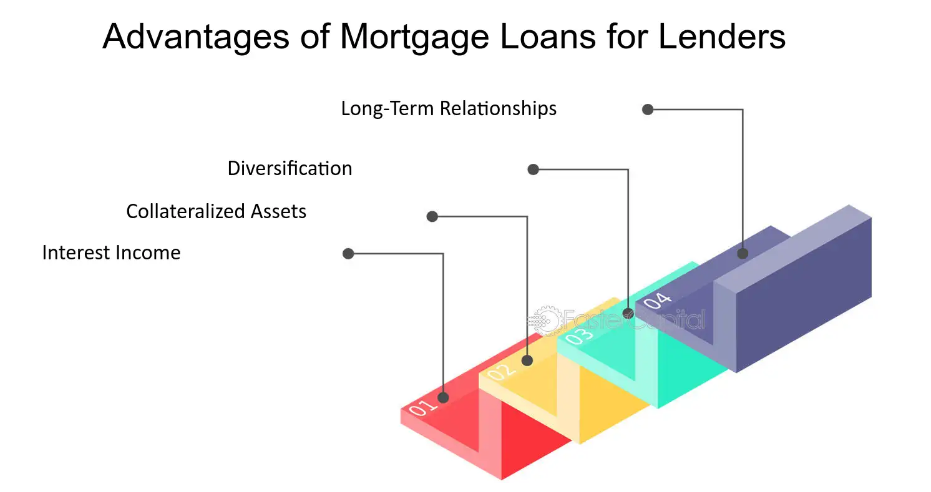

- Pros for Lenders: Secure investment, steady income stream, asset-backed loans.

- Cons for Lenders: Risk of borrower default, market interest rate fluctuations, foreclosure process costs.

- Balanced View: Understanding both sides helps in making informed decisions about mortgage loans.

सूचना का अनुप्रयोग:

Knowing the pros and cons of mortgage loans aids उधारकर्ताओं in evaluating whether taking a mortgage aligns with their financial goals and risk tolerance. For उधारदाताओं, understanding these factors helps in assessing the risk and return profile of their loan portfolios. This knowledge is useful for financial planners and those learning about real estate finance to provide balanced advice to clients and make strategic financial decisions.

Mention that tax deductibility depends on the country you are purchasing the real estate and in some countries it depends on if its a personal or investment property. Readers should refer to their specific countries policys

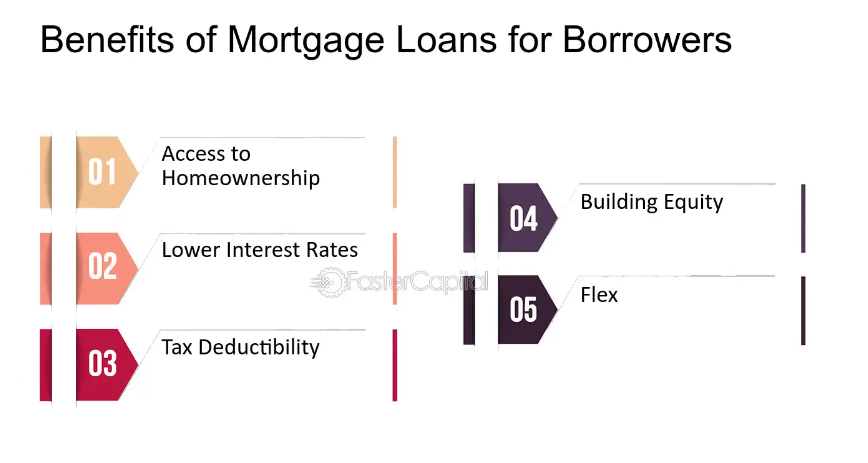

आकृति: Benefits of Mortgage Loans for Borrowers

स्रोत: फास्टरकैपिटल

विवरण:

The infographic illustrates the key benefits of mortgage loans for borrowers. It highlights how mortgage loans enable individuals to build equity, take advantage of tax benefits, enjoy fixed monthly payments, and achieve homeownership. It emphasizes the concept of financial leverage, where borrowers can purchase a home without paying the full amount upfront and benefit from potential property value appreciation over time.

चाबी छीनना:

- Building Equity: Mortgage payments increase the borrower’s ownership stake in the property over time.

- कर लाभ: Interest payments on mortgages can be tax-deductible, reducing the effective cost of borrowing.

- Fixed Monthly Payments: Provides predictability in financial planning with stable payment amounts.

- Home Ownership: Facilitates the purchase of a home, offering stability and potential appreciation in property value.

- Financial Leverage: Allows for the purchase of a home using borrowed funds, maximizing investment potential without immediate full payment.

सूचना का अनुप्रयोग:

Recognizing the benefits of mortgage loans is crucial for prospective homebuyers and those learning about व्यक्तिगत वित्त. Mortgage loans provide a path to homeownership, enhancing financial stability and growth through equity building और property appreciation. This knowledge is essential for making informed decisions about home financing, tax planning, and long-term financial strategy, enabling individuals to leverage these advantages for better financial outcomes.

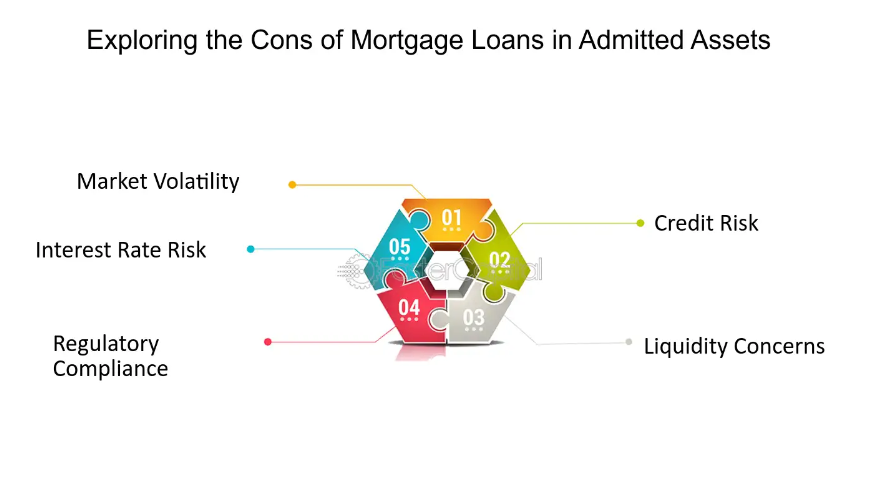

दोष

- Long-term Commitment: Mortgages are long-term financial commitments, typically lasting 15-30 years.

- Interest Costs: Over the life of the loan, you may pay a significant amount in interest.

- Risk of Foreclosure: Failure to meet payment obligations can result in the lender foreclosing on the property.

- Property Value Fluctuations: Property values can decrease, affecting your investment.

आकृति: Exploring the Cons of Mortgage Loans for Borrowers

स्रोत: फास्टरकैपिटल

विवरण:

The infographic outlines the potential drawbacks of mortgage loans for borrowers. It highlights issues such as the long-term commitment of debt, the risk of foreclosure if payments are not made, and the potential for fluctuating interest rates with adjustable-rate mortgages. It also touches on the impact of these factors on the borrower’s financial stability and long-term financial planning.

चाबी छीनना:

- Long-Term Debt Commitment: Borrowers are committed to a long-term financial obligation that can last 15-30 years.

- Foreclosure Risk: Failure to make timely payments can lead to losing the home through foreclosure.

- Interest Rate Variability: Adjustable-rate mortgages can lead to higher payments if interest rates increase.

- Financial Stability: Long-term debt can impact overall financial stability and limit financial flexibility.

- Cost of Borrowing: Over the loan term, borrowers may pay significantly more than the original loan amount due to interest.

सूचना का अनुप्रयोग:

समझना cons of mortgage loans is essential for borrowers to make informed decisions. Recognizing the risks of long-term debt और foreclosure helps in evaluating whether a mortgage is the right choice for one’s financial situation. For those learning about finance, grasping these drawbacks provides a balanced perspective on borrowing and emphasizes the importance of वित्तीय योजना और बजट. This knowledge is crucial for advising clients and making strategic decisions about home financing and debt management.

Section 5: Legal Considerations

Mortgage Agreements

A mortgage agreement is a legal document outlining the terms and conditions of the loan. It includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments.

Legal Requirements

- Credit Check: Lenders typically perform a credit check to assess your financial health.

- Proof of Income: You must provide proof of income to demonstrate your ability to repay the loan.

- Property Appraisal: The lender will require an appraisal to determine the property’s value.

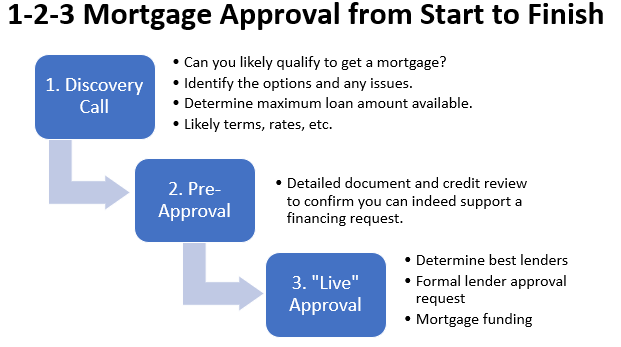

आकृति: Steps to Mortgage Approval

स्रोत: Mortgage insights

विवरण:

The infographic outlines the three main steps to mortgage approval in Canada. The steps include pre-approval, house hunting, and finalizing the mortgage. Each step is broken down into key activities: obtaining a pre-approval letter from a lender, searching for a suitable home and making an offer, and completing the mortgage application process with all necessary documentation and final approval from the lender. This visual guide helps prospective homebuyers understand the sequential process involved in securing a mortgage.

चाबी छीनना:

- Pre-Approval: Obtain a pre-approval letter from a lender to understand your borrowing capacity and budget.

- House Hunting: Search for a suitable home within your budget, make offers, and negotiate the purchase.

- Finalizing the Mortgage: Complete the mortgage application with required documentation and receive final approval from the lender.

- Structured Process: Following these steps helps streamline the mortgage approval process and ensures preparedness.

- Lender Interaction: Continuous communication with the lender is crucial throughout the process for a smooth approval.

सूचना का अनुप्रयोग:

समझना steps to mortgage approval is essential for prospective homebuyers to navigate the home buying process effectively. By following these structured steps, buyers can ensure they are well-prepared, from pre-approval को finalizing the mortgage. This knowledge is beneficial for those learning about real estate finance, as it highlights the importance of बजट, documentation, और lender interaction in securing a mortgage. This structured approach helps in reducing uncertainties and enhances the chances of successful homeownership.

Section 6: Tips for Negotiating a Mortgage

Research and Preparation

- Compare Lenders: Shop around to compare mortgage rates, terms, and fees from different lenders.

- Improve Your Credit Score: A higher credit score can help you secure better interest rates.

- Save for a Larger Down Payment: A larger down payment can reduce your loan amount and monthly payments.

Negotiation Strategies

- ब्याज दर: Negotiate for the lowest possible interest rate. Even a small reduction can save you a significant amount over the life of the loan.

- Fees: Ask the lender to waive or reduce certain fees, such as application fees, origination fees, or appraisal fees.

- ऋण की अवधि: Consider negotiating for a shorter loan term if you can afford higher monthly payments. This can reduce the total interest paid over the life of the loan.

Things to Look Out For

- Prepayment Penalties: Ensure there are no penalties for paying off your mortgage early.

- Adjustable Rates: If considering an ARM, understand how often the rate can change and by how much.

- Hidden Fees: Review the loan agreement carefully for any hidden fees or charges.

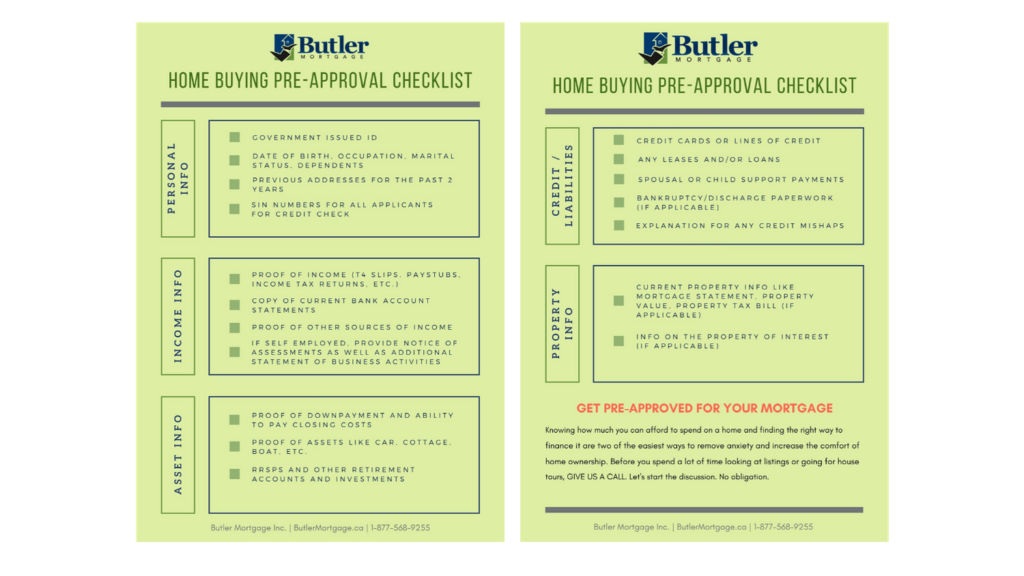

Figure: Mortgage Pre-Approval Checklist

स्रोत: Butler Mortgage

विवरण:

The infographic provides a detailed checklist for obtaining mortgage pre-approval. It includes necessary documents and information that borrowers need to prepare, such as proof of income, credit history, identification, employment verification, and details of existing debts and assets. This checklist ensures that prospective borrowers are well-prepared to meet the lender’s requirements for pre-approval, facilitating a smoother and more efficient mortgage approval process.

चाबी छीनना:

- Proof of Income: Gather recent pay stubs, tax returns, and employment letters.

- Credit History: Obtain a credit report to review and ensure accuracy.

- Identification: Prepare valid government-issued identification.

- Employment Verification: Provide details of current and past employment.

- Debts and Assets: List all existing debts and assets for a comprehensive financial overview.

- Organized Preparation: Following the checklist ensures all necessary documents are ready, speeding up the pre-approval process.

सूचना का अनुप्रयोग:

Having a clear mortgage pre-approval checklist helps borrowers organize their documents and information, making the pre-approval process efficient and less stressful. For those learning about home financing, this checklist highlights the importance of being thoroughly prepared with accurate and complete documentation. Understanding the checklist items helps in advising clients and ensuring that they meet all lender requirements, enhancing their chances of securing a mortgage pre-approval. This organized approach can significantly improve the overall home buying experience.

Section 7: Affordability Considerations

Budgeting for a Mortgage

When planning to buy or rent a property, it’s crucial to consider your overall budget. A common recommendation is that housing costs should not exceed 30% of your gross income. This includes the mortgage payment, property taxes, insurance, and maintenance.

Affordability for Buying

When buying a property, consider the following:

- अग्रिम भुगतान: The initial payment made when purchasing a property. A higher down payment can reduce the mortgage amount and monthly payments.

- Closing Costs: Additional expenses incurred when finalizing a real estate transaction, such as legal fees and taxes.

- Ongoing Expenses: Property maintenance, utilities, and potential homeowners association fees.

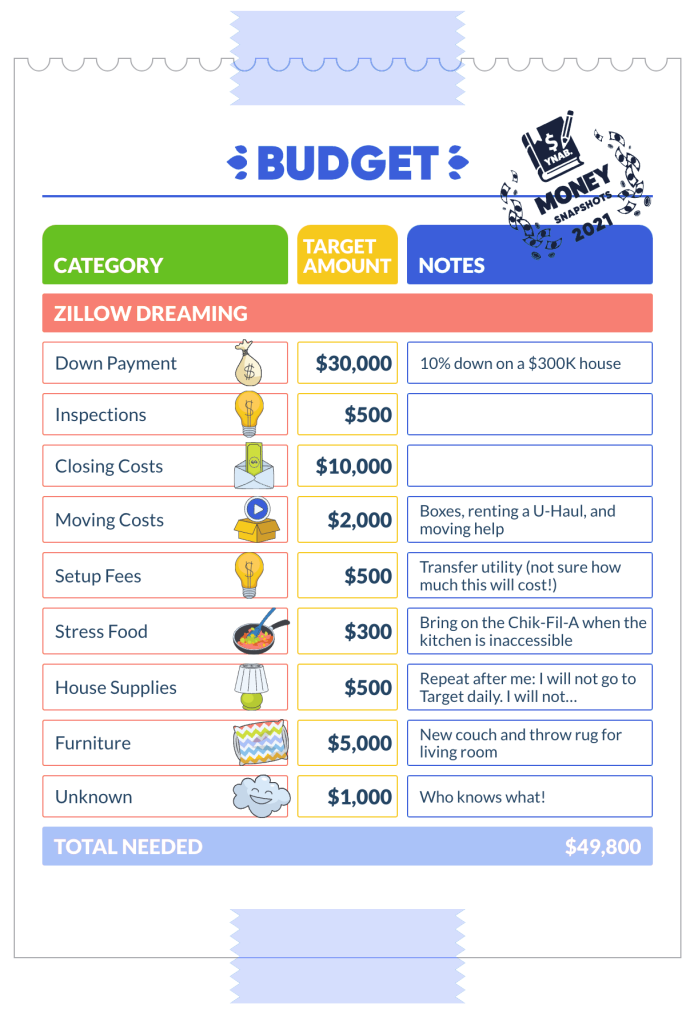

आकृति: How to Budget for a House

स्रोत: YNAB

विवरण:

The infographic provides a comprehensive guide on how to budget for purchasing a house. It includes steps such as determining how much house you can afford, saving for a down payment, accounting for closing costs, and planning for ongoing expenses like property taxes, insurance, and maintenance. Each step is explained with tips and considerations to help potential homeowners manage their finances effectively and ensure they are financially prepared for homeownership.

चाबी छीनना:

- Affordability: Determine how much you can afford based on your income, expenses, and existing debt.

- अग्रिम भुगतान: Save for a substantial down payment to reduce mortgage costs and improve loan terms.

- Closing Costs: Budget for closing costs, which can include fees for inspections, appraisals, and legal services.

- Ongoing Expenses: Plan for ongoing expenses such as property taxes, insurance, and maintenance to avoid financial strain.

- Financial Preparedness: Being financially prepared helps in making informed decisions and avoiding unexpected financial challenges.

सूचना का अनुप्रयोग:

Understanding how to budget for a house is essential for potential homeowners to ensure they are financially ready for the responsibilities of homeownership. By following these steps, individuals can manage their finances, save appropriately, and plan for all associated costs, minimizing the risk of financial hardship. For those learning about व्यक्तिगत वित्त, this guide provides valuable insights into the वित्तीय योजना required for purchasing a home, emphasizing the importance of thorough budgeting and preparation.

Affordability for Renting

When renting, consider these factors:

- Monthly Rent: Should be within your budget to avoid financial strain.

- Security Deposit: Typically required upfront and refundable at the end of the lease, provided no damage occurs.

- Utilities and Maintenance: Some rental agreements include utilities and maintenance, while others do not.

आकृति: How to Budget for Your First Apartment

स्रोत: संतुलन

विवरण:

The infographic provides a step-by-step guide on budgeting for your first apartment. It outlines key financial considerations, including determining your budget, accounting for upfront costs like security deposits and moving expenses, and planning for monthly expenses such as rent, utilities, and groceries. The infographic emphasizes the importance of creating a comprehensive budget to ensure financial stability and preparedness for living independently.

चाबी छीनना:

- Budget Determination: Establish a realistic budget based on your income and essential expenses.

- Upfront Costs: Prepare for initial costs, including security deposits, first month’s rent, and moving expenses.

- Monthly Expenses: Plan for ongoing monthly expenses such as rent, utilities, groceries, and transportation.

- आपातकालीन निधि: Set aside money for unexpected expenses to avoid financial strain.

- Financial Independence: Proper budgeting is crucial for maintaining financial stability while living independently.

सूचना का अनुप्रयोग:

Learning how to budget for your first apartment is vital for young adults and first-time renters to manage their finances effectively. By following these steps, individuals can ensure they have the necessary funds for both initial and ongoing expenses, helping them avoid financial difficulties. For those new to व्यक्तिगत वित्त, this guide provides practical insights into बजट, emphasizing the importance of planning and saving. This knowledge is essential for achieving financial independence and successfully transitioning to independent living.

अनुभाग 8: वास्तविक दुनिया के उदाहरण

उदाहरण 1: मासिक भुगतान की गणना

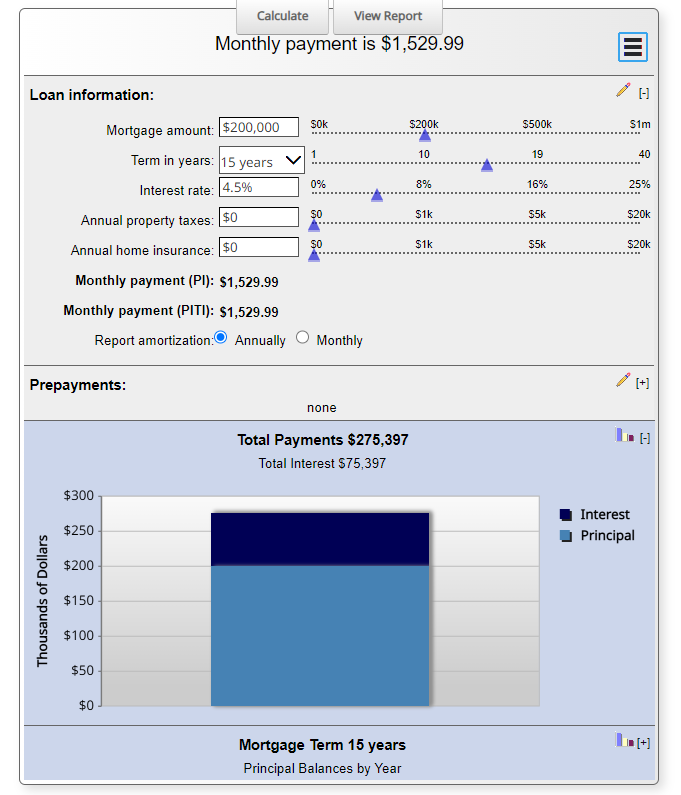

Suppose you are buying a home with a mortgage of $200,000 at an interest rate of 4% for a term of 30 years. Using a mortgage calculator, you can determine that your monthly payment would be approximately $955.

आकृति: Mortgage Payment Calculator

स्रोत: MLS Mortgage

विवरण:

The image showcases a mortgage payment calculator, a tool designed to help users estimate their monthly mortgage payments. The calculator typically requires input details such as the loan amount, interest rate, loan term, and down payment. It provides a breakdown of the monthly payment, including principal and interest, property taxes, homeowners insurance, and possibly private mortgage insurance (PMI). This tool helps prospective homeowners understand their financial commitment and plan accordingly.

चाबी छीनना:

- ऋण राशि: The total amount borrowed to purchase a home.

- ब्याज दर: The percentage charged on the loan amount annually.

- ऋण की अवधि: The length of time over which the loan will be repaid, usually in years.

- अग्रिम भुगतान: The initial payment made when purchasing a home, which reduces the loan amount.

- Monthly Payment Breakdown: Includes principal and interest, property taxes, homeowners insurance, and PMI.

सूचना का अनुप्रयोग:

एक का उपयोग करना mortgage payment calculator helps prospective homeowners and real estate investors estimate their monthly payments and understand the financial commitment of a mortgage. It allows for better financial planning by providing a clear picture of the cost of borrowing and ongoing housing expenses. For those learning about personal finance and real estate, this tool demonstrates the importance of considering all aspects of mortgage costs, helping users make informed decisions about home financing.

उदाहरण 2: सामर्थ्य का मूल्यांकन

If your gross monthly income is $4,000, applying the 30% rule means your housing costs should not exceed $1,200 per month. This helps ensure you have sufficient funds for other expenses and savings.

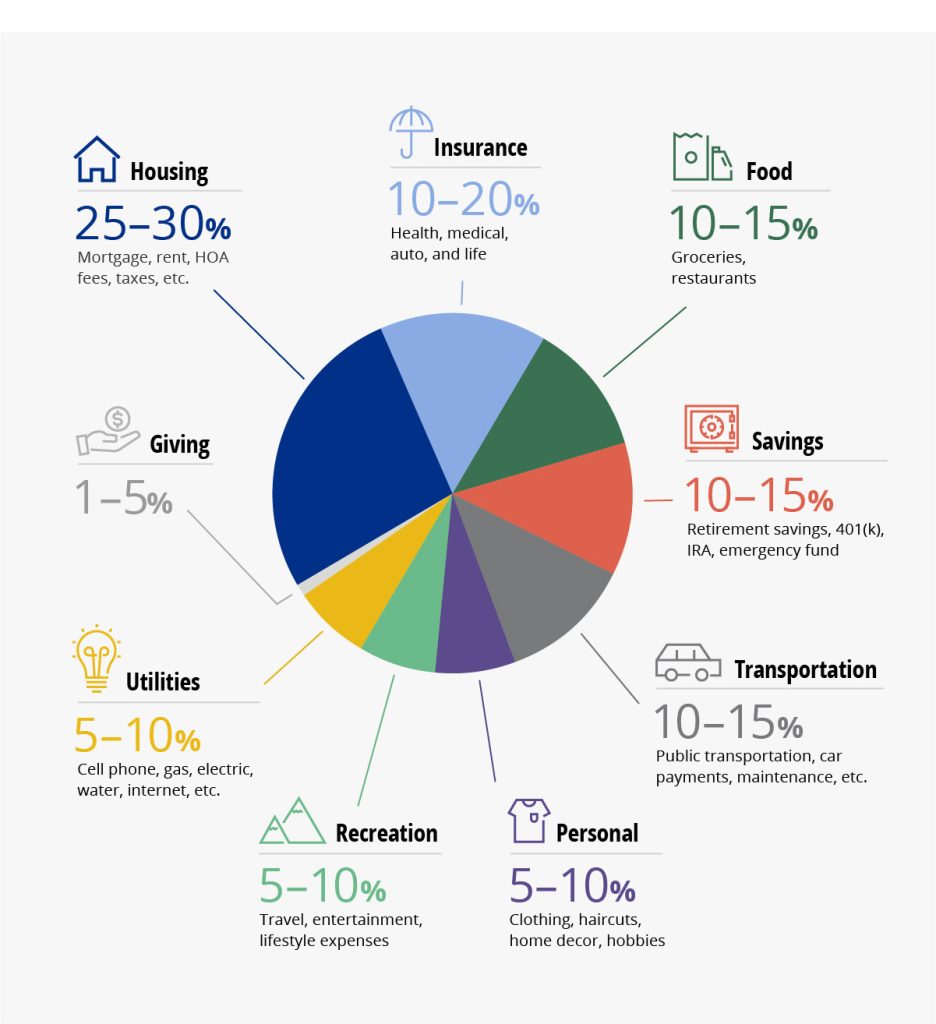

Figure: Creating a Budget with Percentages

स्रोत: Fulton Bank

विवरण:

The infographic provides a guide on how to allocate income into various budget categories using percentages. It suggests breaking down your income into essential categories such as housing, savings, transportation, food, utilities, insurance, and entertainment. Each category is assigned a recommended percentage of your total income, helping individuals create a balanced and manageable budget. This method ensures that all necessary expenses are covered while promoting financial stability and savings.

चाबी छीनना:

- आवास: Allocate a significant portion of your income, typically around 30%, for rent or mortgage payments.

- जमा पूंजी: Aim to save at least 10-20% of your income for future needs and emergencies.

- परिवहन: Budget about 10-15% for transportation costs, including car payments, fuel, and maintenance.

- खाना: Set aside approximately 10-15% for groceries and dining out.

- उपयोगिताओं: Allocate 5-10% for utilities such as electricity, water, and internet.

- बीमा: Budget around 10% for health, auto, and other insurance premiums.

- मनोरंजन: Reserve 5-10% for discretionary spending on entertainment and leisure activities.

सूचना का अनुप्रयोग:

Understanding how to create a budget using percentages helps individuals manage their finances effectively by ensuring that all essential expenses are accounted for. This method promotes financial discipline and aids in achieving financial goals by allocating a portion of income towards savings और emergencies. For those learning about व्यक्तिगत वित्त, this approach provides a practical framework for budgeting, enabling users to balance their spending and improve their overall financial health.

निष्कर्ष

Understanding real estate financing options is crucial for making informed decisions about buying or renting property. By exploring different lenders, understanding key mortgage concepts, and considering affordability, you can better navigate the real estate market and achieve your financial goals.

This chapter provided a comprehensive overview of mortgages, from basic concepts to detailed considerations, legal aspects, and practical tips for negotiation and affordability. Remember, thorough research and preparation can significantly impact your real estate financing experience.

मुख्य पाठ जानकारी:

बंद बयान: Mastering the concepts of real estate financing and mortgages is key to making sound financial decisions when buying or renting property. By understanding mortgages, exploring different financing options, and considering legal and affordability factors, you can confidently navigate the real estate market and achieve your financial goals. This knowledge not only helps you secure favorable terms but also ensures long-term financial stability and growth through informed decision-making.

- Understanding Amortization: A mortgage amortization schedule shows how each payment is divided between interest and principal. Early payments are mostly interest, while later payments reduce the principal. This schedule is crucial for planning your finances and understanding how your loan balance decreases over time.

- Primary vs. Secondary Mortgages: A primary mortgage is your main loan for purchasing property, while a secondary mortgage, such as a home equity loan, is additional financing based on your property’s equity. Understanding the differences helps you make informed decisions about leveraging your home’s value.

- Fixed-Rate vs. Variable-Rate Mortgages: Fixed-rate mortgages provide stable payments, making them easier to budget, while variable-rate mortgages start with lower payments that can increase over time. Choosing between them depends on your financial stability and market conditions.

- Legal and Financial Considerations: Thoroughly reviewing your mortgage agreement, understanding legal requirements like credit checks and property appraisals, and preparing for upfront and ongoing costs are essential steps in securing and maintaining a mortgage.

- Budgeting for Real Estate: Whether buying or renting, it’s important to budget realistically. For homebuyers, this includes down payments, closing costs, and ongoing expenses. Renters should consider monthly rent, security deposits, and utilities. Adhering to the 30% rule ensures your housing costs are manageable within your overall budget.