Sezione 4.1B dei contenuti locali (specifici per l'Europa): comprendere i mutui in Europa

Obiettivi di apprendimento della lezione:

- Understand the basics of mortgage financing in Europe, including the definition and function of primary and secondary mortgages.

- Explore different types of lenders involved in the European mortgage landscape, from traditional banks to private lenders and secondary market participants.

- Learn about key mortgage concepts, such as interest rates and the differences between fixed-rate and variable-rate mortgages.

- Examine the roles of primary and secondary mortgage markets, including how loans are originated and packaged into mortgage-backed securities.

- Identify challenges and strategies in negotiating mortgages, considering factors like interest rates, loan terms, and associated fees.

Introduzione al finanziamento immobiliare

Real estate financing is a key part of property investment, allowing individuals and businesses to secure the capital needed to purchase property. Most real estate financing involves mortgages, where lenders provide funds to buyers who repay the loan over time. This section explores various aspects of mortgages, including types of lenders, mortgage agreements, and key concepts such as interest rates.

Che cos'è un mutuo?

UN mortgage in Europe is a loan used to purchase property, secured by the real estate itself. In many European countries, mortgage terms can range from 15 to 30 years, with varying interest rates based on local market conditions. The lender holds a legal claim to the property until the loan is fully repaid.

Primary Mortgage

UN primary mortgage is the first lien on the property, which typically finances the bulk of the purchase. In Europe, down payment requirements can vary, with some countries requiring up to 20% or more of the property’s value, particularly in markets like Germania E Francia.

Ipoteca secondaria

In Europe, a secondary mortgage may be used to finance home improvements or to unlock equity in the property. This loan is secured against the same property as the primary mortgage and is considered riskier, leading to higher interest rates. Countries like Spagna E Italia have strict rules governing secondary mortgages.

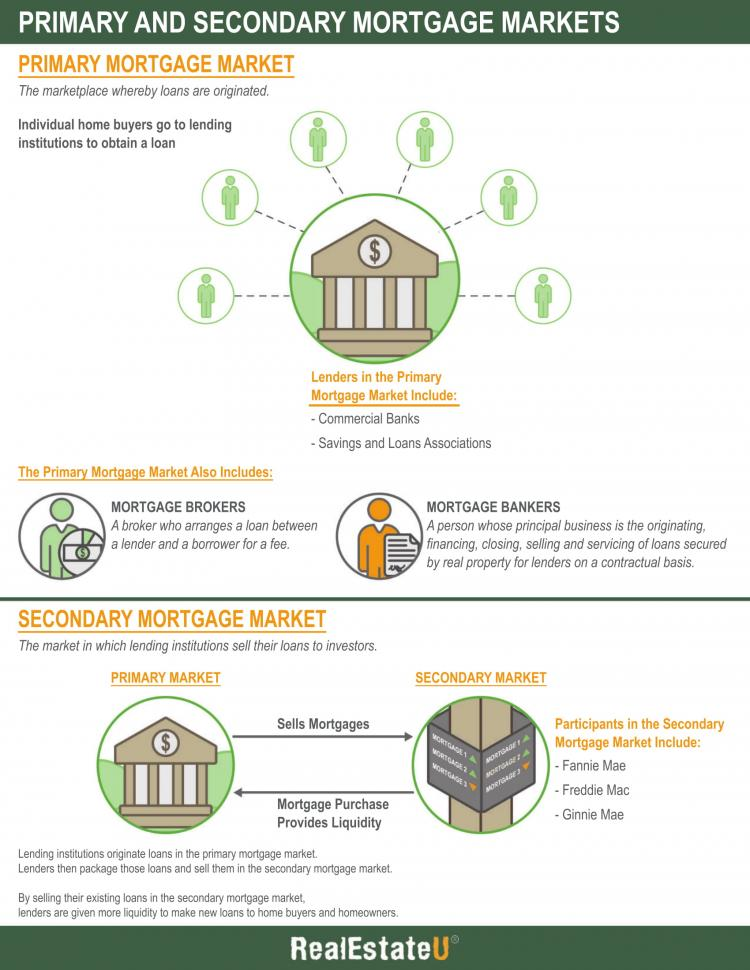

Figura: Infografica sui mercati dei mutui primari e secondari

Descrizione:

L'infografica spiega le differenze e le funzioni del mercato primario e secondario dei mutui ipotecari. Il mercato primario dei mutui ipotecari è il luogo in cui mutuatari e istituti di credito erogano prestiti ipotecari, mentre il mercato secondario dei mutui ipotecari prevede l'acquisto e la vendita di mutui esistenti. L'infografica evidenzia i principali attori di ciascun mercato, come banche e cooperative di credito nel mercato primario, ed enti come Fannie Mae e Freddie Mac nel mercato secondario. Mostra inoltre come i mutui vengono raggruppati e venduti agli investitori come titoli garantiti da ipoteca (MBS).

Punti chiave:

- Mercato dei mutui primari: Dove vengono erogati i mutui; i principali attori sono banche e cooperative di credito.

- Mercato secondario dei mutui: Dove i mutui esistenti vengono acquistati e venduti; coinvolgono entità come Fannie Mae e Freddie Mac.

- Titoli garantiti da ipoteca (MBS): I mutui vengono raggruppati e venduti agli investitori, fornendo liquidità al mercato primario.

- Ruolo degli investitori: Gli investitori in MBS forniscono fondi che vengono utilizzati per erogare nuovi prestiti sul mercato primario.

- Funzioni di mercato: Entrambi i mercati collaborano per garantire la disponibilità e la convenienza dei finanziamenti ipotecari.

Applicazione delle informazioni:

Capire il mercati ipotecari primari e secondari è fondamentale per coloro che sono coinvolti in immobiliare E finanza. Aiuta a spiegare come i prestiti ipotecari vengono originati, finanziati e venduti, influenzando i tassi di interesse e la disponibilità dei prestiti. Per investitori, La conoscenza di questi mercati fornisce spunti sul funzionamento dei titoli garantiti da ipoteca e sul loro impatto sul sistema finanziario più ampio. Questa comprensione aiuta a prendere decisioni informate sugli investimenti immobiliari e a valutare i rischi e i rendimenti associati ai titoli garantiti da ipoteca.

Section 4.2B: Types of Lenders in Europe

Banche tradizionali

Traditional banks in Europe, such as BNP Paribas (France) and Deutsche Bank (Germany), dominate the mortgage lending market. They offer fixed-rate and variable-rate mortgages, often with competitive interest rates and stringent lending requirements.

Prestatori privati

Private lenders in Europe are more flexible than banks, often lending to individuals who may not qualify for traditional bank loans. However, they typically charge higher interest rates. Private lending is particularly prevalent in real estate hotspots like Londra E Parigi, where demand for quick financing is high.

Mercato secondario

IL secondary mortgage market in Europe is less developed than in the United States but is growing. Mortgage-backed securities (MBS) allow banks to sell their mortgages to investors, freeing up capital to issue more loans. Countries like Germania E Svezia have seen an increase in secondary market activity in recent years.

Section 4.3B: Key Mortgage Concepts in Europe

Tassi di interesse

In Europe, interest rates on mortgages are heavily influenced by the Banca centrale europea (BCE), which sets the benchmark rates. Low ECB rates have led to historically low mortgage interest rates in countries like Germania, Mentre Grecia E Portogallo have higher rates due to perceived economic risks.

Mutui a tasso fisso

UN fixed-rate mortgage offers stability with an unchanging interest rate for the term of the loan. This is the most popular type of mortgage in countries like Francia E Belgio, where homeowners value the predictability of payments.

Mutui a tasso variabile (ARM)

In some European countries, mutui a tasso variabile, also called adjustable-rate mortgages (ARMs), are popular. In Spagna, ARMs typically start with lower interest rates but can fluctuate based on Euribor, the European interbank interest rate, making them riskier for borrowers.

Figura: ARMs Dwarf Fixed-Rate Mortgages as Prices Rise

Descrizione:

This line chart compares the average mortgage sizes per adjustable-rate mortgages (ARMs) E mutui a tasso fisso from 2005 to 2019. The vertical axis shows the average mortgage size in thousands of dollars, while the horizontal axis spans time. The blue line (ARMs) demonstrates consistently higher values compared to the red line (fixed-rate mortgages), reflecting ARMs’ popularity for larger loan amounts. A notable decline in ARMs is observed during the 2008–2009 recession period, highlighted on the chart, indicating their vulnerability to market fluctuations. Meanwhile, fixed-rate mortgages exhibit a steady and gradual increase over time, highlighting their stability even during economic downturns.

Punti chiave:

- ARMs have significantly higher average mortgage sizes, appealing to borrowers aiming for larger properties or initial affordability.

- During the 2008–2009 recession, ARMs experienced a steep decline, reflecting reduced borrower confidence and market risks.

- Fixed-rate mortgages offer consistency, showing steady growth in average loan size regardless of economic cycles.

- Rising property prices often make ARMs attractive due to their lower initial interest rates compared to fixed-rate options.

- Borrowers’ preferences for ARMs or fixed-rate mortgages vary depending on economic conditions and interest rate trends.

Applicazione delle informazioni:

This data helps homebuyers, financial analysts, and real estate investors understand the trade-offs between ARMs and fixed-rate mortgages. ARMs are suitable for buyers prioritizing initial affordability or planning to sell before rates adjust, while fixed-rate mortgages are better for those seeking long-term payment stability. This chart also illustrates how external factors, like recessions, shape borrowing trends and preferences.

Section 4.4B: Pros and Cons of Mortgages in Europe

Professionisti

- Long-Term Stability: European real estate markets tend to be stable, making long-term investments via mortgages relatively low-risk.

- Tassi di interesse bassi: Many European countries, particularly in the Eurozone, benefit from historically low interest rates, making mortgages more affordable.

- Tax Advantages: Several countries, such as Portogallo E Spagna, offer tax deductions on mortgage interest, which can help reduce overall costs.

Contro

- High Property Prices: Cities like Londra E Parigi have skyrocketing property prices, making mortgages large and difficult to afford for many.

- Strict Lending Criteria: European banks often have strict lending criteria, particularly in countries like Germania where down payments and credit requirements are high.

- Variable Rates Risk: In countries where variable-rate mortgages are popular, homeowners face potential payment increases if interest rates rise.

Section 4.5B: Legal Considerations in Europe

Contratti di mutuo

Mortgage agreements in Europe vary by country, but most include clauses regarding interest rates, repayment schedules, and penalties for default. In Francia, for example, mortgages must meet strict consumer protection standards.

Requisiti legali

In Europe, legal requirements for mortgages may include property appraisals, credit checks, E income verification. Some countries, like Danimarca, restrict foreign ownership of real estate, impacting mortgage availability for non-residents.

Section 4.6B: Tips for Negotiating a Mortgage in Europe

Ricerca e preparazione

Before negotiating a mortgage in Europe, it’s crucial to research different lenders and mortgage options. Compare interest rates and loan terms from multiple banks and financial institutions in your country. In markets like Germania O Francia, where mortgage products can vary significantly, gathering this information can give you leverage when negotiating.

Strategie di negoziazione

- Acconto: Offering a larger down payment can help reduce the interest rate or lower monthly payments. In countries like Spagna, a higher down payment can also shorten the loan term.

- Loan Terms: Some European banks allow for negotiation on the loan term, which can lower monthly payments or reduce total interest paid. For example, in Italia, negotiating for a 15-year mortgage instead of a 30-year mortgage may reduce overall costs.

- Fee Negotiation: European lenders often charge various fees, such as processing fees or early repayment fees. In countries like the Netherlands, it’s possible to negotiate these fees or have them reduced.

Cose a cui prestare attenzione

- Costi nascosti: Ensure that your mortgage contract in Europe doesn’t include unexpected fees, such as origination or prepayment penalties. Review all documentation carefully.

- Currency Risks: If you’re a foreign buyer using a currency other than the euro, be mindful of exchange rate fluctuations when purchasing real estate in Eurozone countries.

Section 4.7B: Affordability Considerations in Europe

Budget per un mutuo

In Europe, budgeting for a mortgage involves calculating not just the monthly mortgage payments but also tasse sulla proprietà, maintenance fees, and other local charges. Some countries, like Francia, have additional costs like notary fees that must be considered in the overall budget.

Rule of Thumb: It’s recommended that monthly mortgage payments do not exceed 30-35% of your monthly income.

Convenienza per l'acquisto

Before buying property in Europe, use online mortgage calculators to determine affordability. Lenders in countries like Germania E Svezia may require a debt-to-income ratio that limits how much you can borrow. Ensure that you can comfortably afford monthly payments, property maintenance, and potential interest rate fluctuations.

Convenienza per l'affitto

In some European markets, such as Parigi O Amsterdam, renting may be more affordable than buying, especially when property prices are high. Consider local rent-vs-buy calculators to compare the costs of purchasing a home versus renting.

Figura: Home Purchase Affordability in Europe

Descrizione:

Questa mappa illustra la home purchase affordability across Europe by comparing the price of a median apartment to the median local family income (expressed in years of income). Cities are color-coded, with lighter colors representing more affordable housing markets (4–8 years of income) and darker colors indicating less affordable markets (18–22 years). Limerick (4.3 years) in Ireland is the most affordable city, while Moscow (21.6 years) in Russia is the least affordable. The map highlights significant disparities in affordability, reflecting differences in housing markets and local income levels across Europe.

Punti chiave:

- Limerick, Cork, and The Hague are among the most affordable cities, requiring less than 6 years of median local family income to purchase a home.

- Moscow, Cascais, and Paris are the least affordable, with home prices exceeding 20 years of income.

- Cities in Eastern Europe (e.g., Belgrade and Gdańsk) tend to have higher affordability ratios, reflecting disparities between property prices and local income levels.

- Western and Northern European cities, such as Stockholm and Amsterdam, exhibit moderate affordability ratios, with prices requiring around 10–13 years of income.

- The map showcases significant regional variations in affordability, highlighting economic and housing market differences across Europe.

Applicazione delle informazioni:

Questi dati sono essenziali per real estate investors, policymakers, and homebuyers to understand the affordability landscape in Europe. Investors can target markets with favorable affordability ratios for potential returns, while policymakers can use the data to address housing affordability issues. For learners, the map demonstrates the importance of considering income-to-price ratios quando si valutano i mercati immobiliari.

Section 4.8B: Real-World Examples in Europe

Esempio 1: Calcolo dei pagamenti mensili

Suppose you are purchasing a property in Germania with a mortgage of €250,000 at an interest rate of 3% over a 20-year term. You can calculate the monthly payments as follows:

M=P×r(1+r)n(1+r)n−1M = \frac{P \times r(1 + r)^n}{(1 + r)^n – 1}M=(1+r)n−1P×r(1+r)n

Where:

- M is the monthly payment.

- P is the loan amount (€250,000).

- r is the monthly interest rate (3% annually = 0.0025 per month).

- n is the number of payments (20 years = 240 months).

This formula helps determine the monthly payment amount, which includes both principal and interest.

Esempio 2: Valutazione dell'accessibilità economica

Let’s say you earn €4,000 per month. Following the 30-35% rule, your maximum mortgage payment should not exceed €1,200-€1,400 per month. Use this range to evaluate different loan terms and interest rates from European lenders to ensure affordability.

Informazioni chiave sulla lezione:

- Mortgages are secured loans where property serves as collateral, essential for purchasing real estate in Europe.

- Primary mortgages finance the majority of property costs, while secondary mortgages can fund home improvements or help unlock equity.

- Interest rates on mortgages vary by country and can significantly impact the total cost of borrowing.

- The mortgage market is divided into primary (loan origination) and secondary (loan resale) sectors, each playing a crucial role in the availability and cost of mortgage financing.

- Negotiating a mortgage requires careful consideration of terms, rates, and fees to ensure the financing meets the buyer’s needs and financial situation.

Dichiarazione di chiusura:

Mortgage financing is a critical aspect of real estate investment in Europe, providing the capital necessary for purchasing properties. By understanding the different components of the mortgage process, including the types of loans and market practices, investors can make informed decisions to optimize their real estate investments.