Figure: Businessman with umbrella protecting his piggy bank, saving money concept.

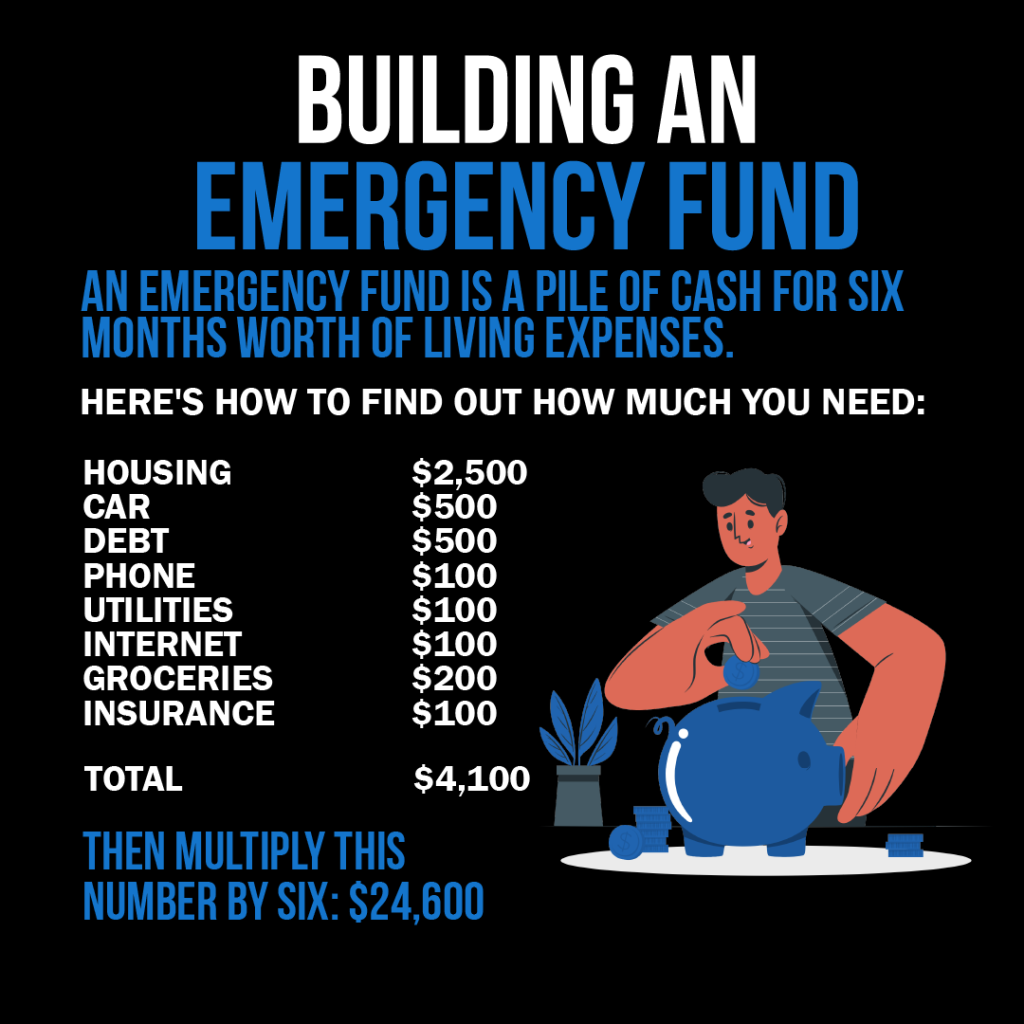

Figure: The infographic is a guide on "Building an Emergency Fund," which it defines as a reserve of cash sufficient to cover six months' worth of living expenses. It breaks down various monthly expenses such as housing, car, debt, phone, utilities, internet, groceries, and insurance, totaling $4,100. To calculate the size of an emergency fund, it advises multiplying this monthly total by six, resulting in $24,600. This visual serves as a practical tool for individuals to estimate the amount they need to save to be financially secure in case of unexpected events. For practical use, users should tally their own monthly expenses, follow the provided formula to determine their emergency fund target, and then create a savings plan to build up to that amount over time. Source: Custom Infographic

7.1 Types of Accounts and Financial Services

金融機関は、それぞれ特定の金融ニーズに合わせて設計されたさまざまな口座とサービスを提供しています。

当座預金口座:

日常の取引に使用されます。 通常はデビットカードが付属しており、 無制限の入金と出金を提供します。

利点: 資金への簡単なアクセス、デビット カード アクセス、オンラインでの請求書支払い。

デメリット: 通常は利息が低いか、利息がまったく発生しません。

普通預金口座:

Aimed at short-term savings over time. Offer interest on the stored funds.

利点: 利息が付き、リスクが低い。

デメリット: 引き出しが制限されており、他の貯蓄商品に比べて金利が低くなる可能性があります。

マネーマーケット口座(MMA):

当座預金口座と普通預金口座を組み合わせたもので、通常は金利が高く、最低残高要件も高くなります。

利点: より高い金利、小切手発行特権。

デメリット: 最低残高要件が高く、取引が制限されている。

預金証書(CD):

Fixed-term savings account with a guaranteed interest rate.

利点: 普通預金口座に比べて金利が高く、利回りが固定されています。

デメリット: 早期解約にはペナルティがあり、期間が終了するまでお金を引き出すことができません。

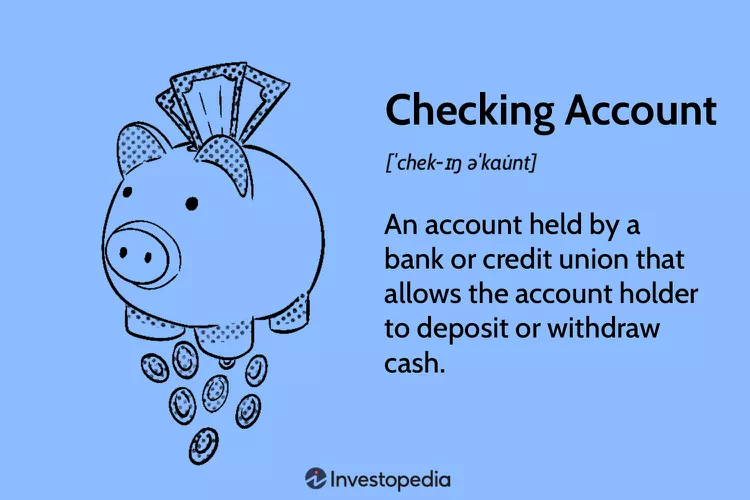

Figure: What is a Checking Account?

説明:

This image visually defines a checking account, which is a primary tool for managing day-to-day finances. It highlights the main features of the account, such as a debit card and paper checks, which are used to make purchases and pay bills. The graphic serves as a simple introduction to one of the most basic and essential products in personal finance.

重要なポイント:

あ checking account is a type of bank account that provides easy access to your money for daily transactions.

It is designed for high liquidity, meaning you can withdraw or spend your money quickly using tools like a debit card, ATM, or online transfers.

The main purpose of this account is for spending and bill payments, not for earning interest; most checking accounts offer little to no interest on your balance.

Keeping track of your transactions through a bank statement or online portal is crucial for 予算編成 and avoiding overdrafts.

情報の応用:

あ checking account is the foundation of personal financial management, acting as the operational center for your income and expenses.

Learning to manage a checking account is a critical first step in creating a 予算, tracking your spending, and building good financial habits.

For anyone new to finance, this account is an essential tool for safely storing money, paying bills efficiently, and participating in the modern economy.

Credit unions typically offer lower fees and better interest rates but might have fewer branches and services. Commercial banks offer a broader range of services but may charge higher fees.

This graphic illustrates the main advantages of using online banking for managing personal or business finances. It visually highlights key features such as 24/7 account access from any device, the ease of making digital payments, and real-time transaction monitoring. The overall message is that online banking offers a more convenient, efficient, and powerful way to handle financial tasks.

重要なポイント:

Constant Accessibility: A major benefit of online banking is 24/7 access to your accounts from anywhere with an internet connection, eliminating the need to visit a physical bank.

Efficiency and Cost Savings: It saves significant time by allowing you to automate bill payments and transfer funds instantly, and it often comes with lower fees than traditional banking services.

Enhanced Financial Control: Online banking provides real-time visibility into your transactions and account balances, which is crucial for accurate budgeting and managing cash flow.

Simplified Record-Keeping: Many platforms can integrate with accounting software, which automates bookkeeping and makes financial reporting much easier for individuals and businesses.

情報の応用:

Adopting online banking is a foundational step for modern and efficient money management.

It provides the tools to actively track your spending, automate your savings contributions, and maintain a clear, up-to-the-minute picture of your financial health.

By leveraging these digital tools, you can reduce time spent on financial administration and focus more energy on achieving your primary goals, like investing for the future or growing a business.

7.3 Comparing Mobile Payment Accounts, Cryptocurrency Accounts, and Traditional Bank Accounts

While mobile payment platforms like Venmo or Cash App and cryptocurrency wallets offer convenience and fast transactions, they typically do not provide interest earnings or federal insurance protections (like FDIC or NCUA insurance). Traditional savings and checking accounts offer lower risk, provide interest (even if modest), and are protected against institutional failures up to certain limits.

Feature

Mobile Payments

暗号通貨アカウント

Traditional Bank Accounts

保険

No federal insurance

No federal insurance

FDIC/NCUA insured

Interest Earnings

None

Very rare

Common (low to moderate)

Accessibility

High (instant transfer)

High (global access)

High (ATM, online banking)

リスクレベル

Medium to high

High (market volatility)

低い

7.4 Why Certificates of Deposit (CDs) Typically Pay Higher Interest Rates

Certificates of Deposit (CDs) generally offer higher interest rates than regular savings accounts or interest-bearing checking accounts because they require depositors to commit their money for a specific period. This commitment gives banks more certainty about the availability of funds for lending and investments. In exchange for giving up liquidity (easy access to their funds), depositors are rewarded with higher rates. Early withdrawal often results in penalties, reinforcing the importance of keeping funds deposited for the full term.

例: A savings account might offer a 1% interest rate, while a 12-month CD could offer 4% during the same period.

長所:

Higher guaranteed returns over the term.

Safe and predictable growth.

短所:

Funds are locked until maturity.

Penalties for early withdrawal.

7.5 Impact of Loan Demand on Deposit Interest Rates

When the demand for loans rises, banks often need additional funds to meet the demand. To attract more deposits (which they use to fund new loans), they may offer higher interest rates on savings accounts, CDs, and other deposit products. Essentially, banks are willing to pay more to bring in money they can lend out profitably.

例:

If mortgage applications rise sharply, banks may raise deposit rates from 1.5% to 2% to attract savers and balance their funding needs.

7.6 Market Conditions Leading to Lower Savings Rates

In times of economic slowdown or when consumers and businesses are not borrowing as much, banks don’t need as many deposits. As a result, they may lower the interest rates paid on savings accounts. This often occurs during recessions or when central banks lower benchmark interest rates to stimulate the economy.

例:

During a recession, banks may drop savings account interest rates from 2% down to 0.5%, reflecting lower loan demand and economic conditions.

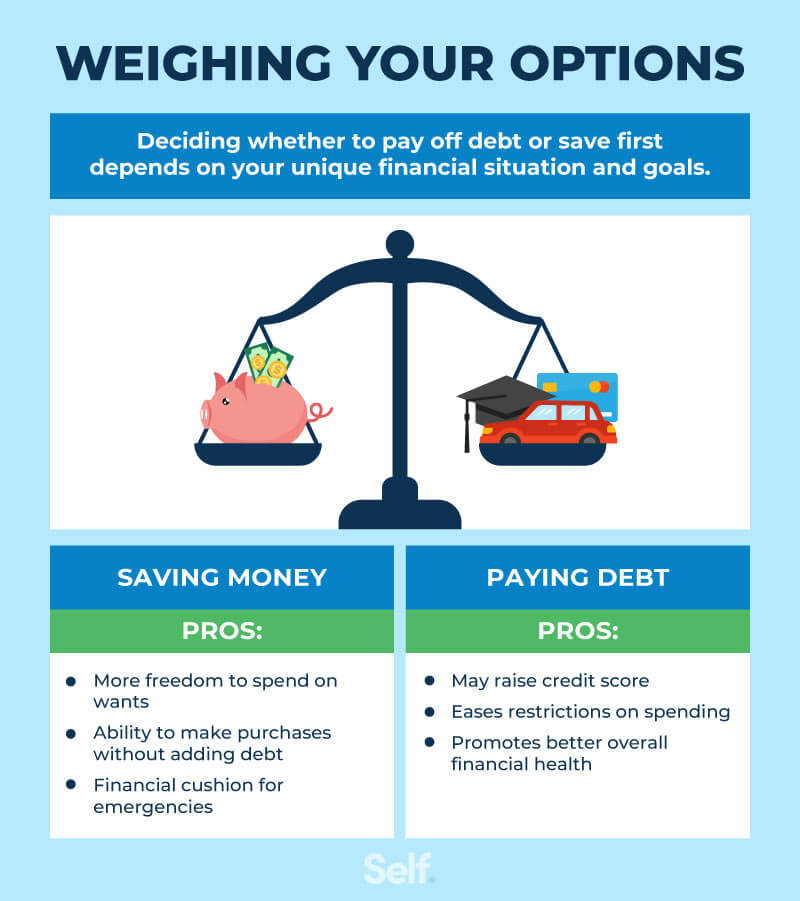

This image tackles the common financial dilemma of whether to focus on paying off debt または building savings. It presents a clear, step-by-step guide to help you decide where to direct your money first. The framework helps you create a balanced strategy that allows you to build a financial safety net while efficiently eliminating debt.

重要なポイント:

The first priority for almost everyone should be to build a starter 緊急資金 of at least $500 to $1,000. This prevents small emergencies from forcing you into more debt.

After establishing a small emergency fund, you should aggressively pay down any 高利子債務, like credit card balances, as the interest charged is often very high.

If your employer offers a retirement plan with a company match, contribute enough to get the full match, as this is essentially a 100% return on your investment and a top priority.

Once high-interest debt is gone, you can adopt a balanced approach by simultaneously building your full 3-6 month emergency fund and saving for other long-term goals.

情報の応用:

This model provides a clear roadmap to help you make smart decisions and reduce financial stress when you have competing financial priorities.

You can use this framework to create an effective cash flow plan, ensuring your money is allocated in the most impactful way.

By following these steps—starter 緊急資金, attacking 高利子債務, and securing an employer match—you can build a strong financial foundation for future wealth creation.

債券はインフレに対抗する目的で設計されており、その金利はインフレに応じて調整されます。インフレが上昇すると、債券の金利も上昇し、高インフレ環境では固定金利により実質リターンがマイナスになる可能性がある従来の CD とは異なり、貯蓄の購買力が長期にわたって維持されます。

将来価値と割引

形: Calculating the Future Value of a Single Cash Flow

説明:

The infographic likely demonstrates the formula for calculating the future value of a single cash flow, which is a fundamental concept in finance. This formula helps in understanding how much an investment made today will grow to at a future date, considering a specific rate of interest. The formula is typically represented as FV = PV(1 + r)^n, where FV is the future value, PV is the present value, r is the interest rate, and n is the number of periods.

This concept is essential for anyone involved in financial planning, investment analysis, or saving for future goals. By applying this formula, individuals can make informed decisions about their investments, understanding how different rates of interest and time periods affect the growth of their money. It encourages strategic investment and helps in setting realistic expectations for investment returns, which is fundamental for long-term financial planning and wealth accumulation.

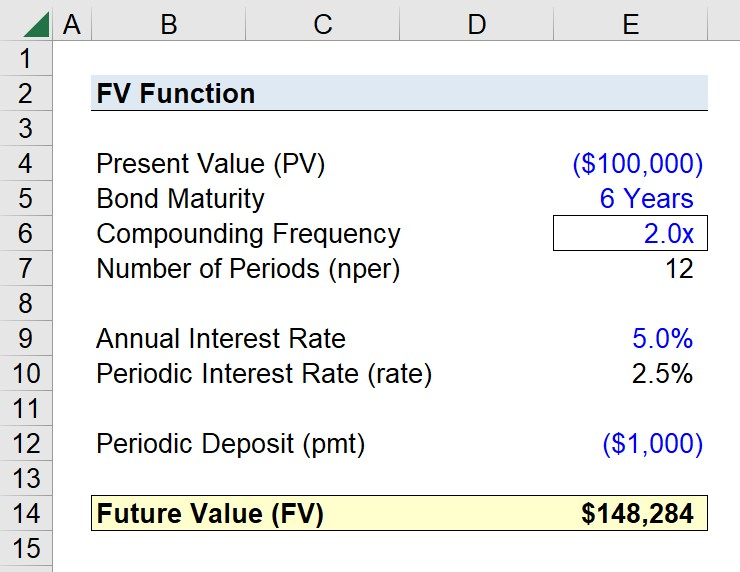

形: Using the FV Function in Excel to Calculate Future Value

説明:

The infographic likely demonstrates how to use the FV function in Excel to calculate the future value of an investment, considering a constant interest rate over a number of periods. The FV function is a powerful tool in Excel for financial analysis, allowing users to input variables such as rate, number of periods, payments, present value, and type (whether payments are made at the beginning or end of periods) to compute the future value of an investment.

重要なポイント:

Excel の FV 関数は、投資の将来価値を計算するために不可欠です。

FV 関数の主な入力には、金利、期間数、定期的な支払い、現在価値、支払い時期などがあります。

FV 関数の使い方を理解すると、財務モデリングと投資分析のスキルが大幅に向上します。

情報の応用:

This knowledge is crucial for finance students, financial analysts, and anyone involved in investment planning or analysis. By mastering the FV function, users can quickly assess the potential future value of investments, aiding in decision-making processes. It’s particularly useful for evaluating the growth of savings accounts, retirement funds, or any investment over time, providing a clear picture of financial futures.

Contingency planning involves preparing for unexpected financial shocks by having backup savings or insurance. A good contingency plan can help cover emergency expenses such as car repairs, medical bills, sudden unemployment, or major household repairs without derailing long-term financial goals.

例:

Backup Fund: Besides an emergency fund, maintain a small “contingency fund” specifically for very short-term needs.

Insurance: Maintain adequate health, auto, and renters/homeowners insurance to mitigate major risks.

Backup Budget: Create a reduced-spending version of your budget to activate if income drops suddenly.

The Federal Deposit Insurance Corporation (FDIC) insures deposits at banks, while the National Credit Union Administration (NCUA) insures deposits at credit unions. Both agencies guarantee deposit accounts (up to $250,000 per depositor, per insured bank or credit union) in case the financial institution fails. This insurance provides consumers with peace of mind that their money is protected against institutional collapse.

例: If your bank closes unexpectedly, the FDIC will reimburse your insured deposits up to the coverage limit.

結論

Saving, managing financial products, preparing for inflation, and understanding the broader banking environment are essential skills for long-term financial success. By supplementing your knowledge with insights about CDs, market influences on interest rates, the differences between mobile/crypto accounts and traditional banks, federal insurance protections, and emergency contingency planning, you’ll be even better equipped to protect and grow your financial future.

主なレッスン情報:

Lorem ipsum dolor sit amet、consectetur adipiscing elit。ウト・エリート・テルス、ルクトゥス・ネク・ウラムコーペル・マティス、プルヴィナー・ダピブス・レオ。