ローカル:EUにおける政府と経済の個人金融への影響を理解する

レッスンの学習目標:

導入:

This chapter explains how government policies and economic factors influence personal finances in the EU. Understanding these impacts can help users make smarter financial decisions and better manage challenges related to economic changes, social benefits, and financial regulations.

- Recognize Government Support Mechanisms: Learn about different welfare benefits そして financial relief programs available across the EU. Knowing how to access these supports can provide financial help during tough times, such as job loss or unexpected emergencies.

- Understand Consumer Protection in Financial Services: Explore how EU consumer protection laws ensure fair treatment by financial service providers. This will help users confidently evaluate financial products and recognize the importance of dealing with licensed, regulated entities.

- Analyze Economic Impacts on Personal Finance: Gain insights into how インフレーション, recession、 そして government policy changes affect personal financial stability. This knowledge will enable users to adapt their financial plans in response to economic shifts, securing long-term financial well-being.

- Assess Risks of Unregulated Financial Products: Learn about the differences between regulated and unregulated financial products. Understanding these distinctions can protect users from potential scams and help them make safer investment choices.

- Adapt Financial Plans for Resilience: Discover strategies like 多様化, sustainable investing、 そして 危機管理 to maintain financial stability in the face of medium- and long-term risks, such as economic downturns or climate-related impacts.

導入

Government policies and broader economic factors have a significant impact on personal finances, from taxation to social benefits and financial regulations. This chapter explores the various ways governments influence personal financial decisions, including welfare programs, consumer protection in financial services, and the role of financial regulators in ensuring transparency and fairness. Additionally, understanding how global and local economic shifts, inflation, and government interventions affect personal wealth is essential for making informed financial decisions. In the EU, individuals must navigate a complex financial environment influenced by both national policies and broader EU directives.

Government Support for Financial Difficulty

Governments across the EU offer various forms of support to individuals and households facing financial difficulties. These supports are designed to provide financial relief during challenging times, such as during unemployment, economic recessions, or unexpected personal emergencies.

- Welfare Benefits: Many EU countries offer unemployment benefits, housing support、 そして social assistance programs to help individuals meet their basic needs when they are unable to earn a stable income. It is essential to know under what circumstances these supports can be accessed and the eligibility criteria.

- Financial Relief During Pandemics: During events like the COVID-19 pandemic, many governments implemented emergency financial relief programs, such as rent and mortgage relief, business support loans, and extended unemployment benefits to support those affected economically.

Example: In ドイツ, individuals who lose their jobs can receive unemployment benefits through the Arbeitslosengeld program, which offers financial support until they find new employment.

形: How Can I Apply for Government Grants Programs

説明:

The figure outlines the 10-step process for applying for government grant programs. It starts with identifying the needed grant type, researching available options, understanding eligibility requirements, and gathering required documents. The process continues with developing a project proposal, completing the application, and submitting it. Finally, the applicant should review, follow up, and be patient throughout the process.

重要なポイント:

- Identifying and researching grants is the first critical step in the application process.

- Understanding eligibility helps in avoiding applications for unsuitable grants.

- Thorough preparation, including gathering documents and developing a proposal, is essential.

- Reviewing and proofreading the application ensures a higher chance of success.

- Persistence and follow-up are key to navigating the application process.

情報の応用:

Knowing how to apply for government grants can help individuals and businesses access funding opportunities. Understanding the step-by-step process ensures applicants are well-prepared, increasing the likelihood of a successful grant application.

Consumer Protection in Financial Services

In the EU, consumer protection measures ensure that individuals are treated fairly when dealing with financial services, whether in-person or digitally. Financial service providers have a legal duty to provide clear, transparent information and to treat consumers fairly.

- Fair Treatment: Financial service providers are required to provide information that is easily understood and not misleading. This includes disclosing all relevant fees, risks, and contract terms when offering financial products like loans, insurance, or investments.

- Regulation and Licensing: Consumers should always verify that a financial service provider is regulated and licensed by the relevant national authority. This ensures that the provider follows EU regulations and operates legally.

- 例: In フランス, consumers can check if a financial service provider is registered with the Autorité des marchés financiers (AMF) または Banque de France to ensure legitimacy.

Understanding Financial Regulators and Authorities

Financial regulators and authorities in the EU oversee the financial services sector to protect consumers, maintain market integrity, and ensure compliance with laws.

- National Financial Authorities: Each country has a national regulatory body responsible for overseeing financial markets and institutions. These regulators ensure that financial service providers comply with laws and protect consumers’ rights. For example, the Financial Conduct Authority (FCA) in the UK or the BaFin in Germany.

- Checking Authorizations: Consumers should always check whether a financial service provider is authorized by national regulators to offer their services. If a provider is unauthorized, there may be limited recourse in case of disputes or fraud.

- Out-of-Court Dispute Resolution: Many EU countries provide out-of-court dispute resolution mechanisms to resolve conflicts between consumers and financial service providers. This includes online dispute resolution platforms that are cost-effective and convenient.

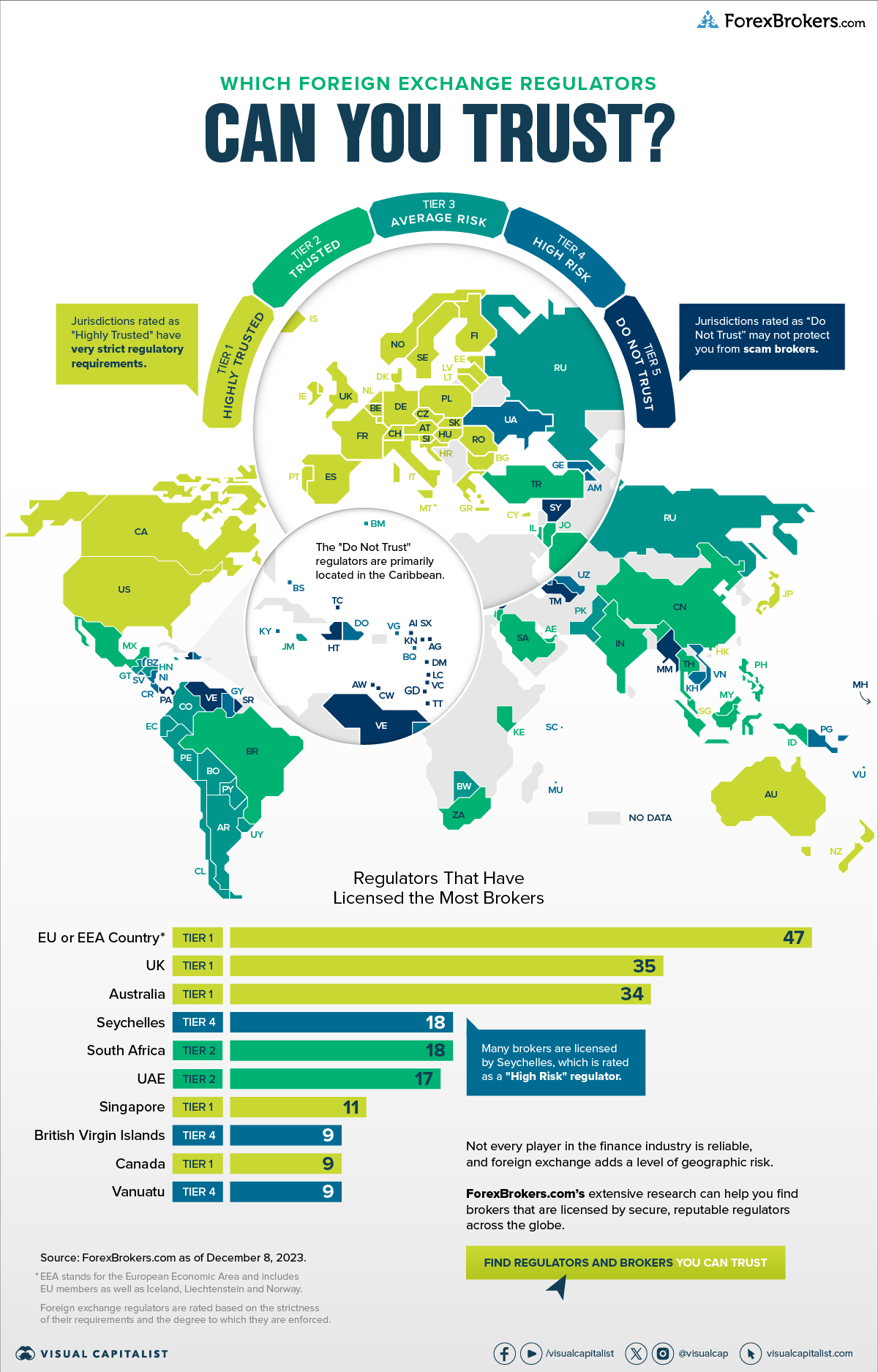

形: : Which Foreign Exchange Regulators Can You Trust?

説明:

The figure illustrates various global foreign exchange regulators, highlighting the perceived risk levels associated with different jurisdictions. Countries are classified into tiers based on the regulatory oversight they provide, ranging from high trust (Tier 1) to average risk (Tier 3). The map visually represents where brokers are licensed, with a focus on regions with the most active licensing. It also identifies key regulators that have issued the most licenses, including the EU, UK, and Australia.

重要なポイント:

- Tier 1 regulators are considered the most trustworthy, setting stringent standards and providing robust oversight.

- の EU, UK, and Australia are among the top jurisdictions for licensing brokers, indicating strong regulatory frameworks.

- Tier 3 regions may present higher risks due to less stringent regulations or oversight.

- Regulatory tiers help traders and investors determine the reliability of brokers based on where they are licensed.

情報の応用:

Understanding regulatory tiers helps investors choose brokers that operate in jurisdictions with strong oversight, reducing potential risks. This knowledge is critical for assessing the safety and reliability of foreign exchange platforms, ensuring that funds are managed securely and transparently.

Understanding Economic and Environmental Factors

The economic environment—such as インフレーション, recessions、 そして pandemics—can significantly impact personal financial well-being. Being aware of these external factors and their influence on personal finances is key to making informed decisions.

- Impact of Recession and Inflation: Economic downturns like recessions often lead to job losses, reduced income, and lower investment returns. インフレーション reduces the purchasing power of money, making goods and services more expensive. Understanding how these factors influence personal finances helps individuals adjust their spending, saving, and investment strategies.

- 例: During periods of high inflation in the EU, individuals may need to adjust their budgets and reduce discretionary spending to account for rising prices on essentials such as food, fuel, and housing.

- 例: During periods of high inflation in the EU, individuals may need to adjust their budgets and reduce discretionary spending to account for rising prices on essentials such as food, fuel, and housing.

- Climate-Related Financial Risks: Climate change is increasingly recognized as a financial risk. Individuals and businesses alike must plan for the potential impacts of climate-related events, such as natural disasters or new environmental regulations, on their financial security.

- Policy Changes: Changes in government policies—such as interest rate adjustments, state benefit reforms, or tax changes—can affect personal financial decisions. Staying informed about such changes enables individuals to adjust their financial plans accordingly.

Figure: The Relationship between Inflation and Purchasing Power

説明:

The figure explains how inflation impacts purchasing power. It emphasizes that as inflation rises, the value of money decreases, leading to reduced purchasing power. It is also important to consider the type and source of inflation, as these can influence the extent of its effects on currency value and interest rates.

重要なポイント:

- Inflation reduces purchasing power by eroding the value of money over time.

- の type of inflation (e.g., demand-pull or cost-push) can have varying impacts on the economy.

- 関心度 are influenced by inflation, affecting borrowing costs and currency value.

- 理解する source of inflation helps in analyzing its potential effects on the economy.

情報の応用:

Knowing how inflation affects purchasing power enables investors to make informed decisions about savings, investments, and borrowing. By understanding the relationship between inflation and interest rates, individuals can better plan their financial strategies and hedge against potential losses due to inflation.

Identifying Biases in Marketing and Information Presentation

Consumers are often influenced by marketing practices, biased presentations of information、 そして peer pressure when making financial decisions. In the digital age, personalized online advertising can target specific users based on their digital footprint, influencing their spending and investment choices.

- Tailored Online Ads: Online advertising platforms use algorithms to target users based on their browsing history, preferences, and behaviors. While these ads may promote relevant products, they can also encourage impulsive financial decisions.

- Marketing Influence on Financial Products: Financial products are often marketed in ways that highlight benefits while downplaying risks. Consumers must develop strategies to objectively assess financial products and avoid falling for misleading advertising or promotional offers.

- Social Media Influence: Peer pressure from social media can lead to impulsive financial decisions, such as making purchases or investments based on trends or influencers. Consumers should be conscious of the influence of social media and avoid making financial choices based on social validation alone.

Example: A consumer in Italy may be influenced by targeted social media ads to purchase a high-risk financial product, such as a cryptocurrency, without fully understanding the risks involved.

形: The Impact of Social Media on Consumer Behavior and Decision-Making

説明:

The figure highlights five key ways in which social media influences consumer behavior. It includes factors such as influencer marketing, user-generated content, and personalized advertising, all of which play a role in shaping purchasing decisions. Additionally, social media fosters trend awareness and social comparison, further affecting how people perceive products and services.

重要なポイント:

- Influencer marketing can sway consumer choices by leveraging the trust and reach of social media personalities.

- User-generated content increases engagement and creates a sense of authenticity around brands.

- Personalized advertising targets users based on their preferences and browsing behavior.

- Trend awareness on social platforms helps users stay informed about new products and market movements.

- Social comparison can influence buying behavior as people assess their own needs relative to others.

情報の応用:

理解する impact of social media on consumer behavior helps businesses develop effective marketing strategies. By using influencer marketing, targeted ads, and user engagement, companies can enhance their reach and create more personalized campaigns that resonate with their audience.

Understanding the Economic and Financial System

Knows the Main Bodies with an Influence on the Economic and Financial System

Various institutions and bodies play significant roles in shaping the economic and financial system in the EU and globally. Knowing these entities allows individuals to understand how policies and regulations impact personal finance, investments, and broader market trends.

- Central Banks: Central banks, such as the European Central Bank (ECB) そして national central banks like the Bank of England, are responsible for 金融政策, including setting interest rates and controlling inflation. Their decisions can directly affect mortgage rates, loan costs, and savings returns.

- 例: When the ECB raises interest rates to combat inflation, borrowing costs increase, affecting both personal and corporate loans.

- 例: When the ECB raises interest rates to combat inflation, borrowing costs increase, affecting both personal and corporate loans.

- Financial Regulators: Regulatory bodies such as the European Securities and Markets Authority (ESMA) and national authorities like BaFin in Germany ensure that financial markets operate transparently and fairly. These regulators enforce rules on financial products and services, including banking, investments, insurance, and securities.

- Government Ministries: National governments and their respective finance ministries (e.g., the Ministry of Finance in France) influence fiscal policies, including taxation and public spending. Changes in tax laws, subsidies, or public investment programs can impact household budgets and financial plans.

Figure: Regulatory Bodies and their Functions

説明:

The figure outlines four key financial regulatory bodies in the United States, each with distinct roles. The Securities and Exchange Commission (SEC) oversees securities markets to protect investors, while the Federal Reserve System (The Fed) manages monetary policy and regulates banks. The Commodity Futures Trading Commission (CFTC) supervises commodity and futures markets, and the Consumer Financial Protection Bureau (CFPB) ensures consumer rights in financial products and services.

重要なポイント:

- The SEC protects investors by enforcing securities laws and regulating stock markets.

- The Federal Reserve (The Fed) maintains economic stability by setting interest rates and regulating banks.

- The CFTC oversees futures and commodities markets, ensuring fair trading practices.

- The CFPB safeguards consumer rights by monitoring financial services like loans, credit, and banking products.

情報の応用:

Understanding regulatory bodies helps investors navigate the financial markets by recognizing who ensures fair practices and stability. Awareness of these organizations is vital for analyzing market trends, economic policies, and consumer rights when making informed investment decisions.

Making Changes to Financial Plans Based on External Factors

Individuals must remain flexible and willing to adjust their financial plans in response to external factors such as economic downturns, policy changes, or shifts in market conditions. Regularly reviewing financial plans and making adjustments ensures financial resilience.

- Monitoring Economic Indicators: Keeping track of economic indicators such as inflation rates, unemployment rates, and GDP growth helps individuals anticipate potential impacts on their personal finances. For example, rising inflation may require adjustments to budgeting or investment strategies to protect purchasing power.

- 例: A homeowner in Spain with a variable-rate mortgage might adjust their budget if interest rates rise, leading to higher monthly payments.

- 例: A homeowner in Spain with a variable-rate mortgage might adjust their budget if interest rates rise, leading to higher monthly payments.

- Responding to Policy Changes: Government policies related to taxation, pensions, or social benefits can have significant financial consequences. For instance, changes to retirement age or pension contribution rates may necessitate changes to savings plans to ensure adequate retirement income.

- Adapting to Global Events: Events like pandemics, natural disasters, or geopolitical crises can disrupt financial markets and personal wealth. During the COVID-19 pandemic, for example, many individuals had to adjust their savings strategies or take advantage of government relief programs.

形: How the Inflation Basket Affects Households

説明:

The figure illustrates the concept of the inflation basket, which represents a collection of goods and services used to measure changes in prices over time. It explains how inflation can significantly impact household budgets, particularly for low-income households that spend a larger portion of their income on essentials like food and housing. The image also highlights strategies households can adopt to cope with inflation, such as reducing spending or increasing income.

重要なポイント:

- Inflation impacts household budgets, especially for low-income families who allocate more money to necessities.

- The inflation basket measures price changes over time, showing how costs for goods and services vary.

- Rising prices can lead to reduced consumer spending and slower economic growth.

- Households can adopt strategies to manage inflation by reducing overall spending or seeking ways to boost their income.

情報の応用:

Understanding how inflation affects purchasing power can help individuals make better financial decisions, such as budgeting and spending wisely. For investors, recognizing inflation trends can guide investment choices that hedge against inflation’s impact, such as investing in inflation-resistant assets.

Ensuring Financial Resilience to Medium- and Long-Term Factors

To ensure the long-term resilience of financial assets, individuals should adopt strategies that consider medium- and long-term risks, including those related to climate change, economic volatility、 そして 市場変動.

- 多様化: One key strategy for building financial resilience is diversifying investments. By spreading investments across different asset classes (e.g., stocks, bonds, real estate), individuals can reduce the risk of significant losses from any one area.

- Incorporating Sustainability Factors: Increasingly, investors are considering environmental, social, and governance (ESG) factors when choosing investments. Climate-related risks, for example, can affect industries such as energy or agriculture. Sustainable investment strategies help mitigate long-term risks while promoting responsible practices.

- 例: An investor in Italy may choose to allocate part of their portfolio to green bonds または renewable energy stocks to align with sustainability goals and reduce exposure to industries vulnerable to climate regulations.

3. Risk Management Tools: Financial products like insurance, hedging strategies、 そして emergency savings funds are crucial for managing unforeseen risks, such as job loss, health emergencies, or economic downturns. By preparing for potential scenarios, individuals can minimize financial shocks.

Figure: Implementing Risk Management Strategies

説明:

The figure outlines a step-by-step process for implementing risk management strategies, starting with identifying potential risks and then developing and implementing risk management plans. It emphasizes continuous monitoring and review, along with the use of insurance coverage to mitigate risk. Each step is presented in a clear sequence to guide users through effective risk management practices.

重要なポイント:

- 潜在的なリスクの特定 is the first step in risk management, allowing organizations to anticipate and prepare.

- Developing risk management plans ensures that there are strategies in place to address identified risks.

- Insurance coverage is a crucial tool for transferring and minimizing financial risk.

- Continuous monitoring and review help to keep the risk management plan relevant and effective.

情報の応用:

Understanding and implementing risk management strategies is essential for businesses and individuals to protect their assets and investments. This step-by-step approach helps ensure that risks are identified, planned for, and mitigated, reducing potential financial losses.

Understanding Financial Regulators and Authorities

Financial regulators are essential for ensuring the stability and fairness of financial markets. Individuals need to be aware of the roles of financial regulators and their importance in protecting consumer rights.

- Roles of Financial Regulators: Regulators like the European Banking Authority (EBA) そして national regulators enforce rules on financial products and services, protect consumers, and maintain financial market stability. They oversee banks, investment firms, insurance companies, and other financial institutions to ensure that they comply with the law.

- 例: In France, the Autorité des marchés financiers (AMF) regulates stock market activities, while the Banque de France ensures the stability of the banking sector.

- 例: In France, the Autorité des marchés financiers (AMF) regulates stock market activities, while the Banque de France ensures the stability of the banking sector.

- Checking Authorizations: Consumers must verify that the financial service providers they engage with are licensed そして authorized by the relevant regulatory bodies. Unauthorized providers can be fraudulent or fail to comply with consumer protection regulations, increasing the risk for individuals.

- 例: A consumer in Germany can check whether an investment firm is authorized by BaFin (Federal Financial Supervisory Authority) before investing in its products.

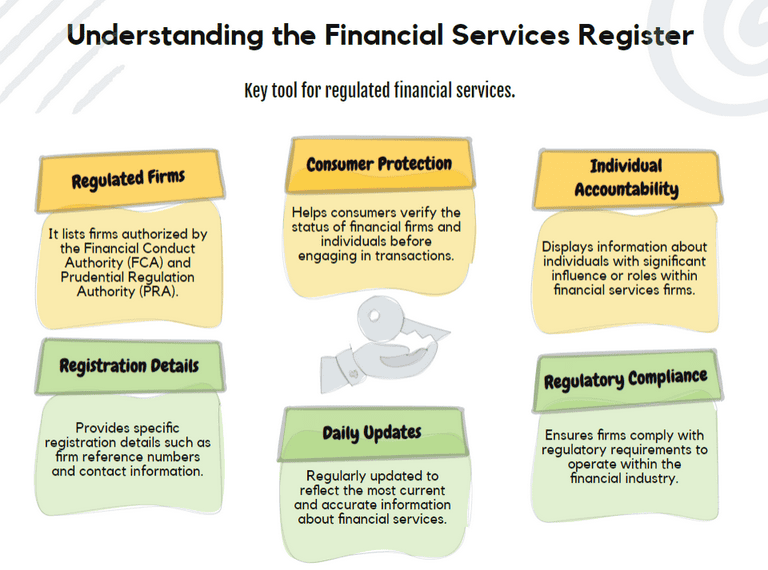

Figure: Understanding the Financial Services Register

説明:

The figure explains the key elements of the Financial Services Register, a tool designed to help consumers and businesses navigate regulated financial services. It outlines aspects such as listing regulated firms, ensuring consumer protection, maintaining individual accountability, and providing detailed registration information. It also emphasizes regular updates and regulatory compliance to ensure accurate and current information is available.

重要なポイント:

- Regulated firms listed on the register are authorized by official regulatory bodies like the FCA and PRA.

- Consumer protection is a primary function, ensuring individuals can verify the legitimacy of firms and individuals before engaging in transactions.

- Daily updates keep the information accurate and up-to-date, reflecting the latest regulatory status of firms.

- Regulatory compliance ensures that firms operate within the financial industry’s legal framework.

情報の応用:

理解する Financial Services Register is crucial for consumers and businesses to verify the legitimacy and compliance of financial firms. It helps investors make informed decisions by confirming that firms are properly regulated and operate within the legal standards.

Awareness of Unregulated Financial Products

Not all financial products are subject to the same level of regulation. In the EU, some financial products and services are not regulated at the EU or national level, leaving consumers vulnerable to higher risks. These products may include cryptocurrencies, peer-to-peer lending, or crowdfunding platforms.

- Cryptocurrency Risks: Cryptocurrencies, for example, are often unregulated and highly volatile. Consumers must be aware of the risks associated with these investments, including the potential for fraud, lack of consumer protections, and extreme price fluctuations.

- Unregulated Services: Financial products offered through online platforms may also lack the same consumer protections as traditional banks or investment firms. Consumers should exercise caution when dealing with unregulated entities.

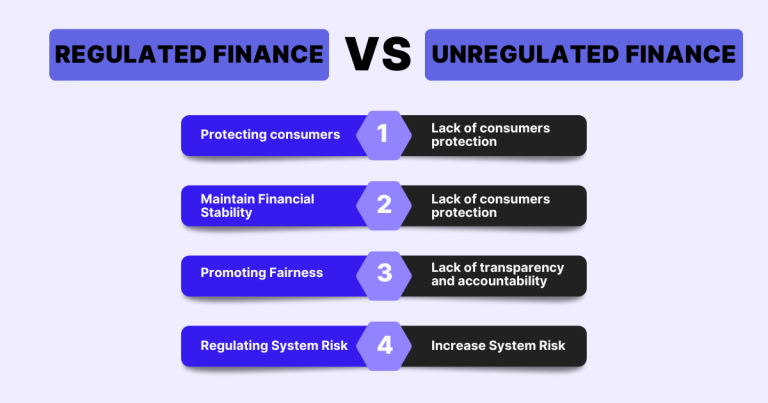

Figure: Regulated Finance vs Unregulated Finance

説明:

The figure contrasts the characteristics of regulated and unregulated financial systems. It highlights how regulated finance focuses on protecting consumers, maintaining financial stability, promoting fairness、 そして regulating system risk. In contrast, unregulated finance often lacks consumer protection, transparency, and accountability, leading to increased system risk.

重要なポイント:

- Regulated finance ensures consumer protection, providing safety measures for individuals.

- Financial stability is maintained in regulated systems, reducing risks of financial crises.

- Transparency and accountability are promoted in regulated environments, ensuring fairness.

- Unregulated finance often leads to increased risks, as it lacks structured oversight and protection.

情報の応用:

Understanding the differences between regulated and unregulated finance helps users make informed decisions when engaging in financial activities. For investors, it’s crucial to consider the level of regulation to assess risk and ensure the safety of their investments.

Reading and Checking Product Information and Disclosures

When purchasing financial products or services, individuals must carefully review product information そして disclosure documents. This includes understanding the 手数料, リスク、 そして terms associated with financial products, whether provided digitally or physically.

- Transparency in Financial Products: Financial service providers are legally required to disclose key information to consumers, such as interest rates, repayment terms, and potential risks. However, it is the consumer’s responsibility to carefully read and verify this information before making decisions.

- Electronic Disclosures: In today’s digital world, financial products are often offered online, and disclosures are provided electronically. Consumers should ensure they thoroughly review these documents, even when they are presented digitally.

- Verifying Provider Information: Before engaging with a financial service provider, consumers should verify their reputation by checking reviews, complaint records、 そして regulatory compliance. Providers that have violated regulations or treated consumers unfairly may have records or warnings available through national regulators.

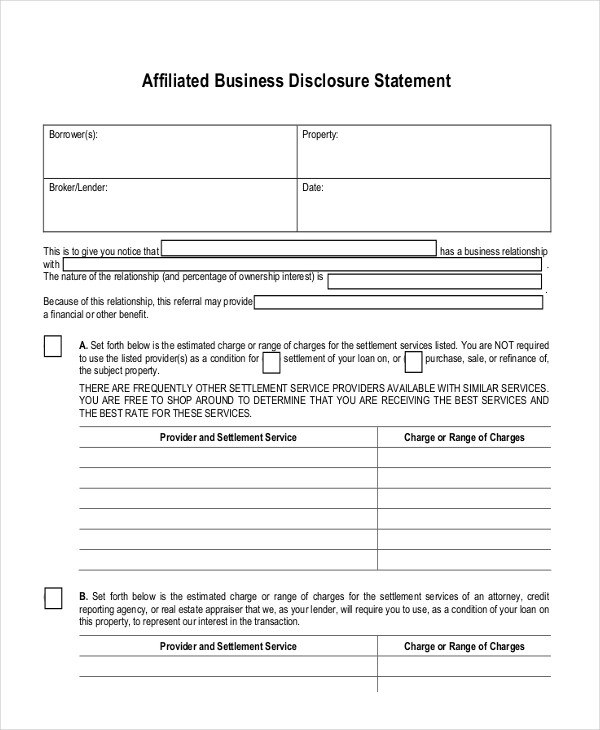

Figure: Affiliated Business Disclosure Statement

説明:

The figure shows a standard Affiliated Business Disclosure Statement used to disclose any business relationships between lenders, brokers, and service providers. It requires details about the borrower, property, and the nature of the business relationship. This document ensures transparency by listing possible charges from affiliated service providers and states that consumers are not obligated to use these services, encouraging them to shop around for the best rates.

重要なポイント:

- Disclosure of business affiliations ensures transparency between lenders and borrowers.

- Consumers are informed of potential conflicts of interest, helping them make better decisions.

- The form emphasizes that consumers are not obliged to use affiliated services.

- Encourages comparison shopping to find the best rates for settlement services.

情報の応用:

This disclosure helps users understand the importance of transparency in financial transactions and encourages them to actively seek the best rates. Investors and borrowers can use this information to avoid potential conflict of interest scenarios and make well-informed decisions when selecting service providers.

主なレッスン情報:

- Government support programs offer financial relief during difficult times, such as unemployment or economic downturns. Accessing these programs requires understanding eligibility criteria and the application process. Being aware of available benefits can help users secure necessary funds during emergencies.

- 消費者保護法 in the EU are designed to ensure fair treatment by financial service providers. Consumers should verify that a provider is regulated, ensuring compliance with laws and reducing the risk of fraud or misleading practices. This protects users when engaging with financial products like loans or investments.

- Economic shifts like inflation or recessions can directly impact personal finances. For example, rising inflation can reduce purchasing power, while recessions might lead to job losses. Staying informed about these changes can help users adjust spending, savings, and investments to protect financial stability.

- Regulated financial products offer more security, while unregulated products, such as cryptocurrencies, carry higher risks due to limited oversight. Users should prioritize regulated investments to ensure better protection and lower potential for fraud.

- Financial resilience requires adapting to changing conditions. Strategies like 多様化, sustainable investing, and using リスク管理ツール (e.g., insurance) can protect against unforeseen challenges. Users can enhance their financial security by implementing these strategies and regularly reviewing their plans.

- Financial regulators play a crucial role in maintaining market stability and protecting consumers. Before engaging with a financial provider, users should check for proper licensing and regulation, ensuring a safer financial environment.

閉会の辞:

By understanding the role of government policies, economic factors, and financial regulations, users can better navigate the complexities of personal finance in the EU. This knowledge helps protect wealth, reduce risks, and promote financial resilience in both stable and uncertain times.