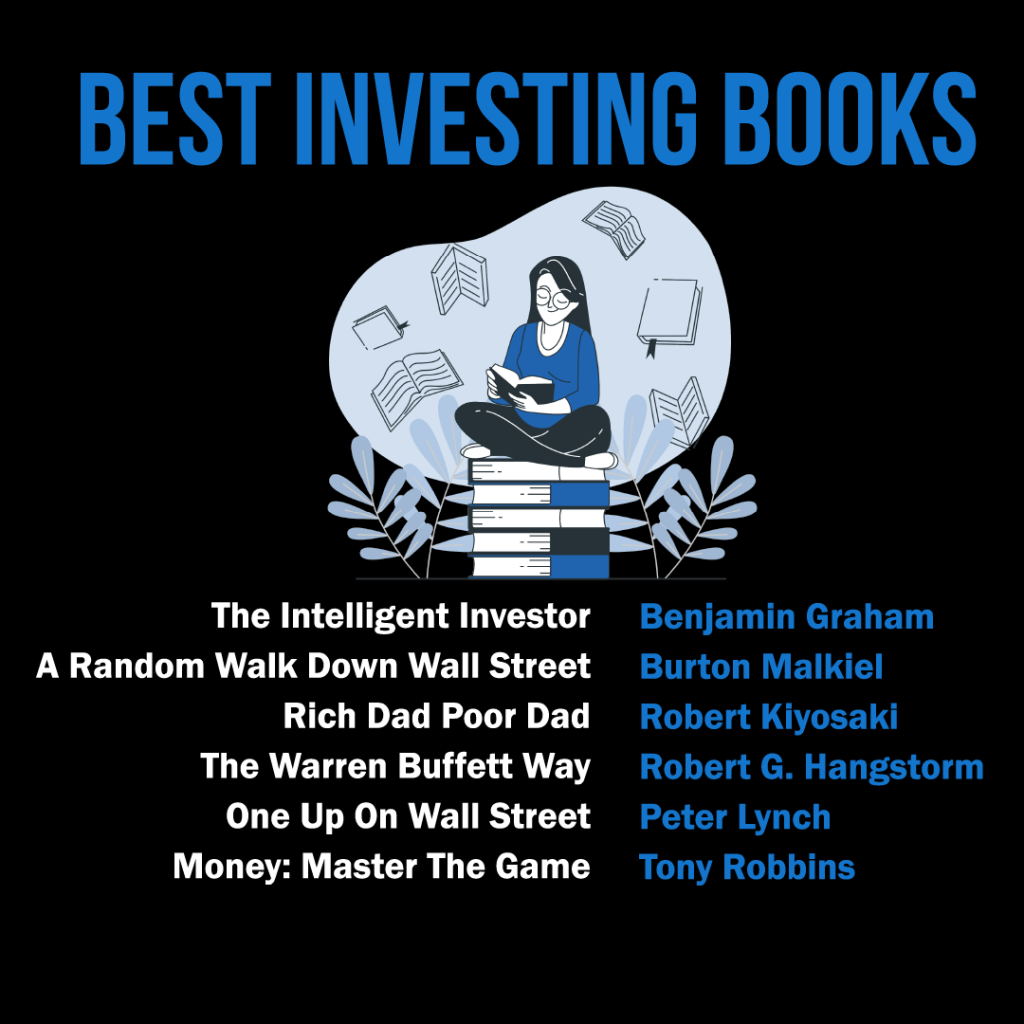

Figure: The infographic lists "Best Investing Books" that are considered must-reads for anyone interested in learning about investing. The books mentioned are: "The Intelligent Investor" by Benjamin Graham "A Random Walk Down Wall Street" by Burton Malkiel "Rich Dad Poor Dad" by Robert Kiyosaki "The Warren Buffett Way" by Robert G. Hagstrom "One Up On Wall Street" by Peter Lynch "Money: Master The Game" by Tony Robbins These books cover a range of investment philosophies, from value investing to personal finance, and offer insights into the strategies of some of the world's most successful investors. For practical use, readers should consider starting with one book that aligns most closely with their investment style or goals and apply the principles learned to their own investment strategies. Source: Custom Infographic

書籍と出版物: 個人金融に関する本や出版物を読むことで、予算編成、投資、退職計画など、さまざまなトピックに関する詳細な知識を得ることができます。人気のあるタイトルには、ロバート・キヨサキ著の『金持ち父さん貧乏父さん』、デイブ・ラムジー著の『The Total Money Makeover』、ヴィッキー・ロビンとジョー・ドミンゲス著の『Your Money or Your Life』などがあります。

オンライン リソース: NerdWallet、Investopedia、The Simple Dollar など、多くの Web サイトやブログが個人金融に関するアドバイスや洞察を提供しています。これらのリソースは、金融ニュースの最新情報を入手したり、新しい戦略を学んだり、役立つツールを見つけたりするのに役立ちます。

ポッドキャストとビデオ: 個人金融に関するポッドキャストを聞いたり、ビデオを見たりすることは、お金の管理について学ぶ魅力的な方法です。人気のポッドキャストには、「The Dave Ramsey Show」、Farnoosh Torabi の「So Money」、および「The Indicator from Planet Money」などがあります。さらに、Graham Stephan や The Financial Diet などの YouTube チャンネルでは、有益で楽しい個人金融コンテンツを提供しています。

16.2 Utilizing Financial Tools and Software

財務ツールやソフトウェアを使用すると、財務を効果的に管理し、目標を達成するのに役立ちます。Simple Financial Community の個人財務アプリケーションは、財務と予算をよりよく理解するための貴重な洞察とリソースを提供するように設計されています。

Several federal and state agencies protect your savings and investments:

FDIC and NCUA: Insure your deposits up to $250,000.

Federal Reserve: Regulates banks and manages the economy through monetary policy.

Securities and Exchange Commission (SEC) そして 消費者金融保護局 (CFPB): Protect investors and consumers from fraud and abuse.

Indiana Securities Division (or your state’s equivalent): Offers local protections for investors.

16.7 Protecting Your Personal Financial Information

To protect your identity and money:

Keep your Social Security number private.

Check your credit reports regularly.

Shred sensitive documents before throwing them away.

Only share personal financial data with trusted entities like your bank or tax agency.

If identity theft happens:

Contact your bank and freeze your accounts.

Report the fraud to the Federal Trade Commission (FTC) at IdentityTheft.gov.

Notify the major credit bureaus.

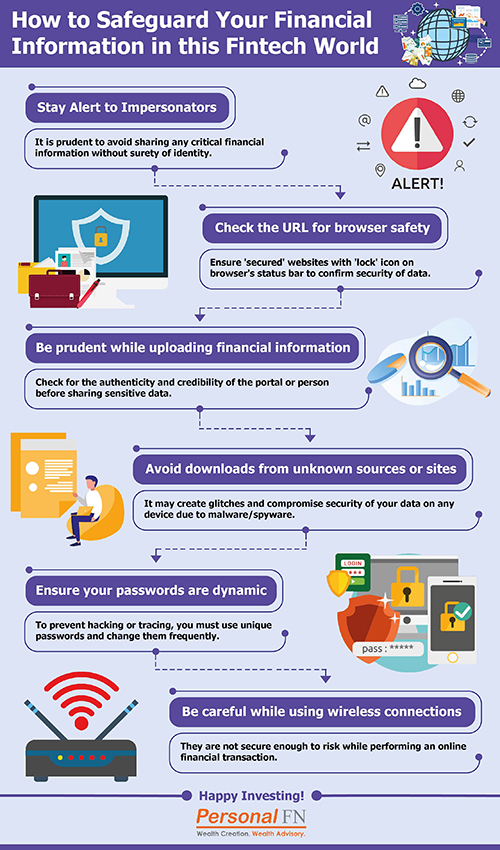

形: How to Safeguard Your Financial Information in the FinTech World

説明:

This infographic provides a list of essential security practices for protecting your sensitive financial information in the age of digital finance. It visually outlines key actions you can take, such as creating strong passwords and being aware of phishing scams. The overall purpose is to educate users on how to safely navigate the world of online banking and FinTech applications.

重要なポイント:

The foundation of digital security is using strong, unique passwords for each financial account and enabling Two-Factor Authentication (2FA) as an extra layer of protection.

Be constantly vigilant for phishing scams, which are deceptive emails, text messages, or phone calls designed to trick you into revealing your confidential data.

It is crucial to avoid using unsecured public Wi-Fi for any banking or financial transactions, as your information can be easily intercepted.

You should regularly monitor your financial statements and account activity to quickly identify and report any suspicious or unauthorized transactions.

情報の応用:

By adopting these habits, you can dramatically reduce your risk of suffering from identity theft and financial fraud.

These security practices are fundamental for safely using the convenient tools offered by FinTech and online banking.

Making cybersecurity a part of your routine is a critical component of modern financial management and protecting your assets.

16.8 Financial Contingency Planning

Emergencies like job loss, medical bills, or a car accident can derail finances. Always have a contingency plan:

Maintain 3-6 months’ worth of expenses in an emergency fund.

Know which bills must be paid first (housing, utilities, transportation).

Have a backup source of credit (like a low-interest credit card) only for emergencies.

主なレッスン情報:

Lorem ipsum dolor sit amet、consectetur adipiscing elit。ウト・エリート・テルス、ルクトゥス・ネク・ウラムコーペル・マティス、プルヴィナー・ダピブス・レオ。