Local: analyzing European companies

レッスンの学習目標:

- Learn about the income statement under IFRS. You will understand how revenues, 経費、 そして net income are reported, along with the inclusion of other comprehensive income (OCI). This helps investors assess a company’s profitability and financial performance.

- Understand the balance sheet under IFRS. The balance sheet provides a snapshot of a company’s assets, liabilities、 そして 公平性, offering insights into the company’s financial position. Learn about the distinctions between current and non-current items and how they reflect a company’s liquidity and solvency.

- Explore the cash flow statement under IFRS. The cash flow statement outlines how cash is generated and used across operating, investing、 そして financing activities. You will learn how this statement helps assess a company’s liquidity and its ability to generate cash to fund operations and investments.

- Gain insights into the overall structure and application of IFRS in European financial reporting. Understanding IFRS helps ensure transparency and comparability, making it easier to analyze financial statements and make informed investment decisions across borders.

導入

Understanding the core financial concepts is essential for any investor. Financial statements provide critical insights into a company’s financial health and performance, helping investors evaluate profitability, liquidity, and growth potential. This section will introduce the fundamental financial statements—損益計算書, 貸借対照表、 そして cash flow statement—and explain how to analyze these documents. We will also discuss key financial data points that investors use to assess a company’s performance.

22.1 Financial Statements

When analyzing European companies, it’s essential to understand that their financial statements are typically prepared according to the International Financial Reporting Standards (IFRS), a global accounting framework that ensures transparency and comparability across borders. In Europe, IFRS is mandatory for all publicly listed companies, providing investors with consistent and clear financial information. This section introduces how financial statements in Europe adhere to IFRS, ensuring high-quality reporting.

IFRS and Income Statement

Under IFRS, the 損益計算書 (also called the statement of comprehensive income) follows a structured approach, similar to financial statements globally, but with some unique European nuances. The income statement provides detailed insight into a company’s revenues, costs, and overall profitability.

- Revenue Recognition: Under IFRS, revenue is recognized when control of a product or service is transferred to the customer. European companies must adhere to these rules, ensuring that revenues are reported accurately based on performance obligations, not just when payments are received.

- 運営費: Expenses are classified by either their nature (e.g., wages, materials) or their function (e.g., cost of sales, administrative expenses). This flexibility allows European companies to present their income statements in a way that best reflects their operational structure.

- Other Comprehensive Income: IFRS emphasizes the importance of other comprehensive income (OCI), which includes gains or losses not reflected in the net income, such as foreign exchange differences or revaluation of financial instruments. This is particularly relevant for European companies operating in multiple currencies.

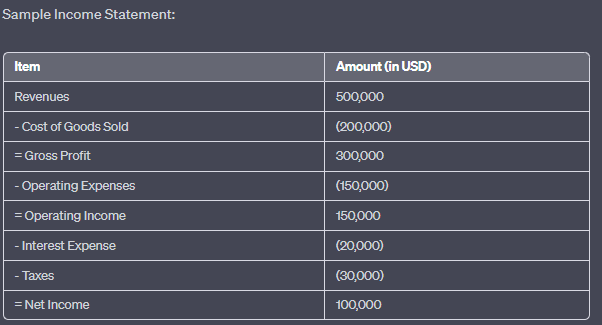

形: 損益計算書のサンプル

説明:

The image presents a sample income statement, breaking down the financial performance of a company over a specific period. It starts with the total revenues and subtracts various expenses to arrive at the net income. The statement showcases the following items:

収益: $500,000

売上原価: $(200,000)

粗利益:$300,000

運営費:$(450,000)

営業利益:$150,000

利息費用:$(20,000)

税金:$(30,000)

純利益:$100,000

重要なポイント:

- 収益: 経費を差し引く前の会社が得た収入の総額。

- 売上原価(COGS): 販売された商品の生産に起因する直接費用。

- 粗利益: 企業が総収益から売上原価を差し引いた後に得る利益。

- 運営費: 企業の日常業務に関連するコスト。

- 営業利益: 事業活動から得られる利益(利子および税金控除前)。

- 利息費用: 資金を借り入れるコスト。

- 税金: 企業の課税所得に基づいて政府に支払われる金額。

- 純利益収益からすべての費用を差し引いた後の会社の総利益。

情報の応用:

損益計算書は、投資家やステークホルダーに特定の期間における企業の収益性に関する洞察を提供する基本的な財務書類です。損益計算書を分析することで、企業の収益源、コスト構造、そして全体的な財務状況を理解することができます。このデータは、情報に基づいた投資判断や企業の経営効率の評価に不可欠です。

22.2 IFRS and Balance Sheet (Statement of Financial Position)

の 貸借対照表, known under IFRS as the statement of financial position, provides a snapshot of a company’s assets, liabilities, and equity. IFRS requires companies to clearly differentiate between current and non-current items to offer a transparent view of a company’s financial health.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

- 負債: Under IFRS, liabilities are also divided into 現在 (due within a year) and non-current. European companies must report their obligations, including debt, leases, and pensions, in this format, providing clear insights into their short-term and long-term obligations.

- Shareholders’ Equity: The shareholders’ equity section under IFRS is structured to show both contributed capital (from shareholders) and retained earnings (profits that have been reinvested into the business). European firms must also disclose other reserves, including revaluation reserves and foreign currency translation adjustments.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

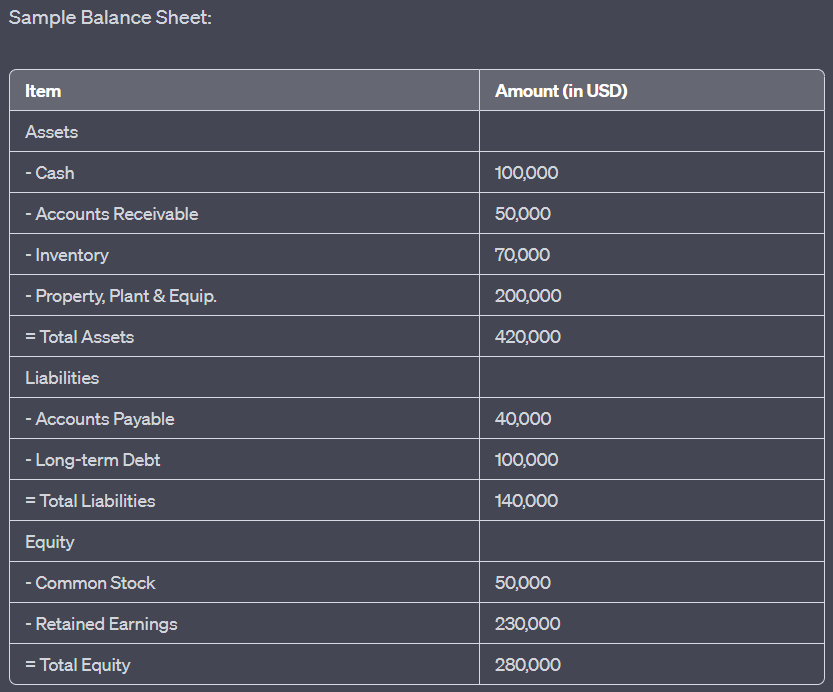

形: Sample Balance Sheet

説明:

The image displays a sample balance sheet, which provides a snapshot of a company’s financial position at a specific point in time. It categorizes the company’s resources (assets) and the claims against those resources (liabilities and equity). The balance sheet showcases the following items:

- 資産: 現金($400,000)、売掛金($50,000)、在庫($70,000)、有形固定資産($200,000)を含む合計$420,000。

- 負債: 合計は$140,000で、買掛金($40,000)と長期債務($400,000)で構成されています。

- 公平性: 普通株($50,000)と利益剰余金($230,000)を合わせて合計$280,000。

重要なポイント:

- 資産: 企業が所有する経済的価値のある資源。

- 負債: 会社が外部団体に対して負う義務。

- 公平性: 株主が投資した資金や累積利益など、会社に対する所有権を表します。

- 基本的な会計方程式: 資産 = 負債 + 資本。

\(\textbf{会計方程式:}\)

\[ \displaystyle \text{資産} = \text{負債} + \text{純資産} \]

\(\textbf{凡例:}\)

\(\text{資産}\) = 総資産

\(\text{負債}\) = 総負債

\(\text{Equity}\) = 総資本

情報の応用:

A balance sheet is a foundational financial statement that offers insights into a company’s financial health. By analyzing the balance sheet, stakeholders can assess the company’s liquidity, solvency, and overall financial stability. This information is vital for investors, creditors, and other stakeholders to make informed decisions related to the company’s financial position

22.3 IFRS and Cash Flow Statement

の cash flow statement under IFRS follows a similar structure to other global standards but places particular emphasis on transparency in how cash is generated and used by the company. European companies use this statement to report cash flows from operating, investing, and financing activities.

- 営業活動: IFRS allows for flexibility in reporting cash flows from operating activities, either through the direct method (showing cash receipts and payments) or the indirect method (starting with net income and adjusting for non-cash items). Most European companies opt for the indirect method.

- Investing and Financing Activities: Cash flows related to investments in assets or securities and activities such as issuing shares or repaying debt are reported here. European companies must clearly distinguish these transactions to show how they are funding their growth and managing their financial obligations.

- Foreign Exchange Impacts: Given that many European companies operate across multiple countries and currencies, IFRS requires the inclusion of cash flow impacts due to changes in foreign exchange rates, providing investors with a clearer understanding of how currency movements affect a company’s cash position.

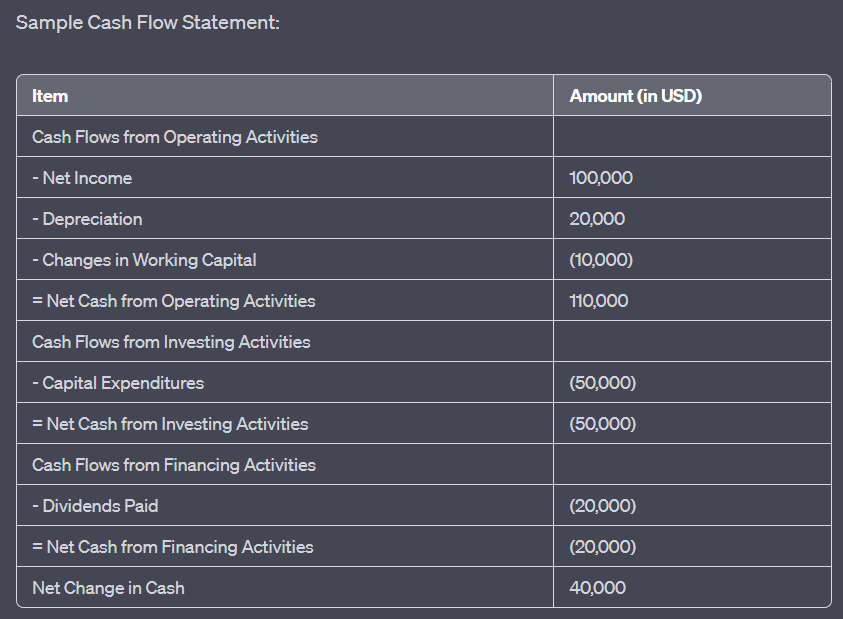

形: Sample Cash Flow Statement

説明:

The image illustrates a sample cash flow statement, which provides a detailed account of the cash inflows and outflows for a company over a specific period. The statement is segmented into three main categories: Operating Activities, Investing Activities, and Financing Activities. The key items include:

営業活動によるキャッシュフロー: 純利益 ($100,000)、減価償却費 ($20,000)、運転資本の変動 (-$10,000) により、営業活動による純現金は $110,000 となります。

投資活動によるキャッシュフロー: 資本的支出(-$50,000)により、投資活動による純現金は-$50,000となります。

財務活動によるキャッシュフロー: 配当金が支払われ(-$20,000)、財務活動による純現金は-$20,000となりました。

現金の全体的な純増減は $40,000 です。

重要なポイント:

- 営業活動: コア事業活動で生み出された、または使用された現金を反映します。

- 投資活動: 資産への投資に使用された現金、または資産の売却から受け取った現金を表します。

- 資金調達活動: 貸し手や株主などの外部の資金調達源からのキャッシュフローや、外部の資金調達源へのキャッシュフローを表示します。

- 現金の純増減は、期間中の会社の現金残高の全体的な増加または減少のスナップショットを提供します。

情報の応用:

The cash flow statement is an essential financial tool that offers insights into a company’s liquidity and its ability to generate and use cash effectively. By analyzing the cash flow statement, stakeholders can understand how a company manages its cash resources, which is crucial for assessing its financial health and making informed investment decisions.

結論

In Europe, financial statements are prepared according to IFRS, ensuring a high level of consistency, transparency, and comparability across countries and industries. The 損益計算書, 貸借対照表、 そして cash flow statement under IFRS provide investors with the detailed information needed to assess the financial health of European companies. IFRS’s global standards ensure that European companies’ financial reports meet international expectations, making it easier for investors to analyze and compare firms operating in different regions.

主なレッスン情報:

- The income statement shows a company’s profitability. The income statement provides a breakdown of a company’s revenues, cost of goods sold (COGS), operating expenses、 そして net income. By analyzing this statement, investors can evaluate how efficiently a company is generating profits and managing costs. Revenue recognition under IFRS ensures accurate reporting based on performance obligations.

- The balance sheet offers a snapshot of a company’s financial position. It categorizes a company’s assets, liabilities、 そして 公平性. By examining these elements, investors can assess a company’s liquidity (ability to meet short-term obligations), solvency (ability to meet long-term obligations), and financial health. The fundamental accounting equation の assets = liabilities + equity is key to understanding this statement.

- The cash flow statement tracks how cash is used. The statement divides cash flows into operating, investing、 そして financing activities. By analyzing this statement, investors can understand how the company generates cash from its operations, how it funds investments, and how it manages external financing. Positive cash flow from operating activities signals a strong cash position.

閉会の辞:

Financial statements under IFRS provide essential insights into a company’s financial health and performance. By analyzing the 損益計算書, 貸借対照表、 そして cash flow statement, investors can make well-informed decisions based on transparency, consistency, and detailed reporting, helping them assess the company’s profitability, liquidity, and long-term sustainability.