Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elittellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

16.1 Staying Informed about Personal Finance

개인 금융에 대해 지속적으로 스스로를 교육하는 것은 정보에 입각한 금융 결정을 내리고 금융 목표를 달성하는 데 매우 중요합니다. 다음 리소스를 사용하여 지식을 넓히는 것을 고려하세요.

그림: 냅킨에 그린 개인 재정 계획을 설명하는 개념적 낙서. 소박한 나무 테이블 위에는 에스프레소 컵과 동전이 놓여 있다.

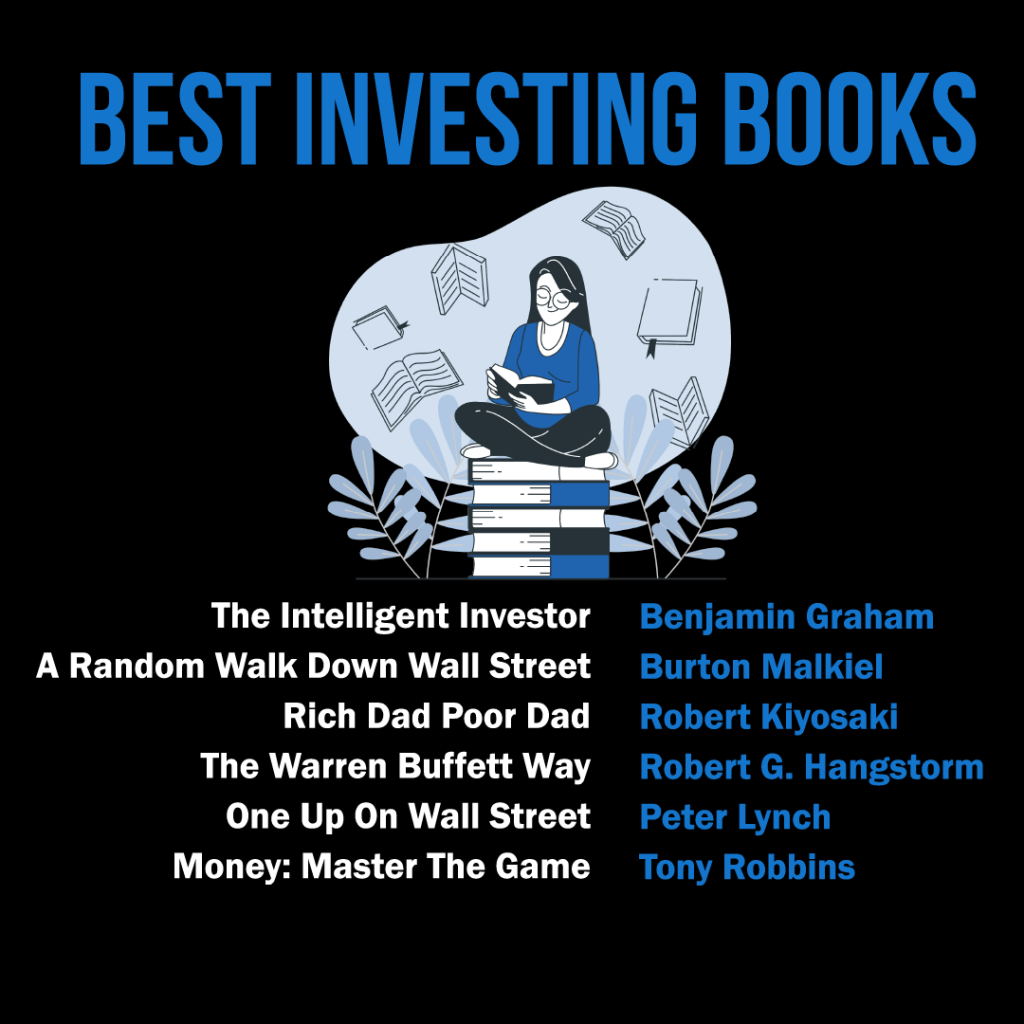

Figure: The infographic lists "Best Investing Books" that are considered must-reads for anyone interested in learning about investing. The books mentioned are: "The Intelligent Investor" by Benjamin Graham "A Random Walk Down Wall Street" by Burton Malkiel "Rich Dad Poor Dad" by Robert Kiyosaki "The Warren Buffett Way" by Robert G. Hagstrom "One Up On Wall Street" by Peter Lynch "Money: Master The Game" by Tony Robbins These books cover a range of investment philosophies, from value investing to personal finance, and offer insights into the strategies of some of the world's most successful investors. For practical use, readers should consider starting with one book that aligns most closely with their investment style or goals and apply the principles learned to their own investment strategies. Source: Custom Infographic

서적 및 출판물: 개인 금융 서적과 출판물을 읽으면 예산 책정, 투자, 은퇴 계획 등 다양한 주제에 대한 심층적인 지식을 얻을 수 있습니다. 인기 있는 제목으로는 Robert Kiyosaki의 "Rich Dad Poor Dad", Dave Ramsey의 "The Total Money Makeover", Vicki Robin과 Joe Dominguez의 "Your Money or Your Life" 등이 있습니다.

온라인 리소스: NerdWallet, Investopedia, The Simple Dollar 등 많은 웹사이트와 블로그에서 개인 금융 조언과 통찰력을 제공합니다. 이러한 리소스는 금융 뉴스에 대한 최신 정보를 얻고, 새로운 전략을 배우고, 유용한 도구를 찾는 데 도움이 될 수 있습니다.

팟캐스트 및 비디오: 개인 금융 팟캐스트를 듣거나 비디오를 시청하는 것은 자금 관리에 대해 배울 수 있는 흥미로운 방법이 될 수 있습니다. 인기 있는 팟캐스트로는 "The Dave Ramsey Show", Farnoosh Torabi의 "So Money", "The Indicator from Planet Money" 등이 있습니다. 또한 Graham Stephan 및 The Financial Diet와 같은 YouTube 채널은 유익하고 재미있는 개인 금융 콘텐츠를 제공합니다.

16.2 Utilizing Financial Tools and Software

금융 도구와 소프트웨어를 사용하면 재무를 효과적으로 관리하고 목표를 계속 달성하는 데 도움이 됩니다. Simple Financial Community의 개인 금융 애플리케이션은 귀하의 재정과 예산을 더 잘 이해할 수 있도록 귀중한 통찰력과 리소스를 제공하도록 설계되었습니다.

예산 및 비용 추적: 당사 애플리케이션은 필요에 따라 예산을 생성, 유지 및 조정하는 데 도움이 되는 사용자 친화적인 예산 도구를 제공합니다. 사용자 정의 가능한 카테고리를 통해 소득과 지출을 쉽게 추적하여 지출 습관을 파악하고 필요한 조정을 할 수 있습니다.

목표 설정 및 진행 상황 모니터링: 애플리케이션 내에서 단기 및 장기 재무 목표를 설정하고 목표 달성을 위한 진행 상황을 추적하세요. 재무 목표에 계속 집중할 수 있도록 시기적절한 업데이트와 알림을 받으세요.

투자 추적 및 분석: 애플리케이션 내에서 투자를 모니터링하고 포트폴리오 성과를 분석하세요. 자산 배분에 대한 통찰력을 얻고 투자 전략에 관해 정보에 입각한 결정을 내리세요.

금융교육 및 지원: 기사, 튜토리얼, 웹 세미나 등 애플리케이션 내에서 풍부한 교육 리소스에 액세스하여 금융 지식을 확장하세요. 금융 여정을 탐색하는 동안 지침을 제공하고 질문에 답할 수 있는 사용자 및 전문가로 구성된 지원 커뮤니티에 참여하세요.

그림: 금융 도구를 중심으로 한 생생한 단어 구름 그림.

교육 자료와 Simple Financial Community의 개인 금융 애플리케이션을 함께 활용하면 정보에 입각한 재무 결정을 내리고 재무 목표를 달성하는 데 필요한 지식과 도구를 얻을 수 있습니다.

16.3 Mobile and Online Banking: Risks and Protections

While mobile and online banking make it easier to manage money, they come with risks like identity theft and scams.

Key tips to protect yourself:

Always use strong passwords and two-factor authentication.

Avoid logging into bank accounts on public Wi-Fi.

Monitor your accounts weekly for suspicious activity.

Set up alerts for large transactions or logins from new devices.

16.4 Comparing Financial Institutions and Services

Not all financial services are the same! Here’s what to compare:

Third-Party Check Cashing: Banks charge less than payday lenders or grocery stores.

Online and Mobile Banks: Often lower fees but fewer physical branches.

Avoiding Fees: Set up low-balance alerts and opt out of overdraft protection to avoid costly charges.

Being Unbanked: Pros (cash control) vs Cons (lack of FDIC insurance, expensive check cashing).

16.5 Working with Financial Professionals

금융 전문가와 협력하면 귀하의 재무 목표 달성에 도움이 되는 귀중한 지침과 전문 지식을 얻을 수 있습니다. 다음은 몇 가지 일반적인 금융 전문가 유형, 장단점, 이들과 협력하기 위한 모범 사례입니다.

재무설계사

재무 설계사는 고객이 예산 책정, 저축, 투자, 은퇴 계획 및 보험 전략을 포함할 수 있는 종합적인 재무 계획을 세울 수 있도록 지원합니다.

그림: 연금, 청구서, 보험 서류 작업에 중점을 두고 컨설턴트로부터 재정 조언을 받는 노인 부부.

장점:

전체적인 접근 방식: 재무 설계사는 귀하의 전체 재정 상황을 살펴보고 귀하의 고유한 요구 사항과 목표에 맞는 맞춤형 계획을 세웁니다.

전문성: 재무설계사는 개인 금융의 다양한 측면에 대한 전문 지식을 보유하고 있으며 전문적인 조언을 제공할 수 있습니다.

단점:

비용: 재무 설계사를 고용하는 데는 비용이 많이 들 수 있으며 수수료는 수수료 구조(예: 시간당 요금, 고정 수수료 또는 관리 중인 자산 비율)에 따라 다릅니다.

잠재적인 이해 상충: 일부 재무 설계사는 특정 금융 상품 판매로부터 수수료를 받을 수 있으며, 이는 잠재적으로 추천에 영향을 줄 수 있습니다.

모범 사례 및 팁:

엄격한 교육, 시험, 경험 요건을 충족한 공인 재무설계사(CFP)를 찾아보세요.

FINRA나 SEC 등의 기관을 통해 기획자의 자격과 징계 이력을 확인하세요.

기획자의 수수료 구조와 잠재적인 이해 상충에 대해 미리 논의하세요.

투자 자문

투자 자문가는 고객의 투자 포트폴리오 관리를 전문으로 하며 자산 배분, 위험 관리 및 특정 투자 상품에 대한 추천을 제공합니다.

투자 자문

장점:

전문적 지식: 투자상담사는 금융시장 및 투자상품에 대한 전문적인 지식을 보유하고 있습니다.

시간 절약: 투자 자문가가 귀하의 투자를 관리하여 귀하가 금융 생활의 다른 측면에 집중할 수 있도록 해드립니다.

단점:

비용: 투자 자문사는 일반적으로 관리 중인 자산의 비율에 따라 수수료를 청구하는데, 이는 일부 투자자에게는 비용이 많이 들 수 있습니다.

제한된 범위: 투자 자문가는 주로 투자에 중점을 두고 귀하의 재정 상황의 다른 측면을 다루지 않을 수 있습니다.

모범 사례 및 팁:

SEC 또는 주 증권 규제 기관에 등록된 등록 투자 자문가(RIA)를 선택하세요.

고문의 투자 철학과 전략이 귀하의 목표와 위험 허용 범위에 부합하는지 논의하십시오.

고문의 성과 내역을 검토하고 다른 고문과 수수료를 비교하십시오.

세무 전문가

공인회계사(CPA) 또는 등록 대리인(EA)과 같은 세무 전문가는 세금 계획, 준비 및 규정 준수를 전문으로 합니다.

장점:

전문 지식: 세무 전문가는 세법 및 규정에 대한 심층적인 지식을 갖추고 있어 정확하고 규정을 준수하는 세금 신고를 보장합니다.

세금 절약 전략: 세무 전문가는 세금 책임을 최소화하여 잠재적으로 돈을 절약할 수 있는 전략을 추천할 수 있습니다.

단점:

비용: 세금 전문가를 고용하는 것은 특히 복잡한 세금 상황의 경우 비용이 많이 들 수 있습니다.

계절적 가용성: 일부 세무 전문가는 수요가 많아 세금 시즌 외에 연락하기 어려울 수 있습니다.

모범 사례 및 팁:

CPA나 EA 등 관련 경험과 자격을 갖춘 세무 전문가를 선택하세요.

세무 전문가가 귀하의 특정 세금 상황(예: 자영업, 임대 부동산 또는 해외 소득)에 대한 경험이 있는지 확인하십시오.

예상치 못한 일을 피하기 위해 전문가의 수수료와 가용성에 대해 미리 논의하십시오.

금융 전문가와 협력할 때는 항상 실사를 수행하고, 추천을 요청하고, 그들이 귀하에게 최선의 이익을 위해 행동하는지 확인하십시오. 잘 선택된 금융 전문가는 귀하의 재무 목표 달성에 도움이 되는 귀중한 전문 지식과 지원을 제공할 수 있습니다.

16.6 Regulatory Agencies that Protect Consumers

Several federal and state agencies protect your savings and investments:

FDIC and NCUA: Insure your deposits up to $250,000.

Federal Reserve: Regulates banks and manages the economy through monetary policy.

Securities and Exchange Commission (SEC) 그리고 소비자 금융 보호국 (CFPB): Protect investors and consumers from fraud and abuse.

Indiana Securities Division (or your state’s equivalent): Offers local protections for investors.

16.7 Protecting Your Personal Financial Information

To protect your identity and money:

Keep your Social Security number private.

Check your credit reports regularly.

Shred sensitive documents before throwing them away.

Only share personal financial data with trusted entities like your bank or tax agency.

If identity theft happens:

Contact your bank and freeze your accounts.

Report the fraud to the Federal Trade Commission (FTC) at IdentityTheft.gov.

Notify the major credit bureaus.

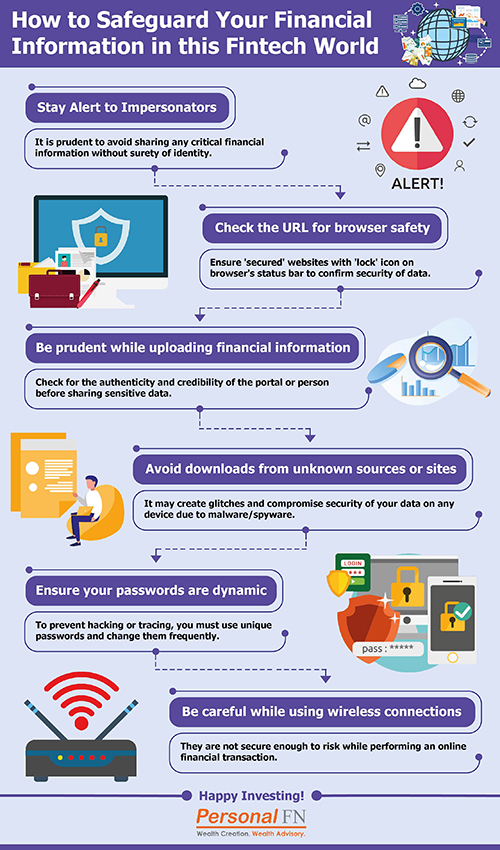

수치: How to Safeguard Your Financial Information in the FinTech World

설명:

This infographic provides a list of essential security practices for protecting your sensitive financial information in the age of digital finance. It visually outlines key actions you can take, such as creating strong passwords and being aware of phishing scams. The overall purpose is to educate users on how to safely navigate the world of online banking and FinTech applications.

주요 시사점:

The foundation of digital security is using strong, unique passwords for each financial account and enabling Two-Factor Authentication (2FA) as an extra layer of protection.

Be constantly vigilant for phishing scams, which are deceptive emails, text messages, or phone calls designed to trick you into revealing your confidential data.

It is crucial to avoid using unsecured public Wi-Fi for any banking or financial transactions, as your information can be easily intercepted.

You should regularly monitor your financial statements and account activity to quickly identify and report any suspicious or unauthorized transactions.

정보의 응용:

By adopting these habits, you can dramatically reduce your risk of suffering from identity theft and financial fraud.

These security practices are fundamental for safely using the convenient tools offered by FinTech and online banking.

Making cybersecurity a part of your routine is a critical component of modern financial management and protecting your assets.

16.8 Financial Contingency Planning

Emergencies like job loss, medical bills, or a car accident can derail finances. Always have a contingency plan:

Maintain 3-6 months’ worth of expenses in an emergency fund.

Know which bills must be paid first (housing, utilities, transportation).

Have a backup source of credit (like a low-interest credit card) only for emergencies.

주요 수업 정보:

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elittellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.