2장: 금융 태도와 행동

수업 학습 목표:

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elittellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

2.1 Introduction

In the landscape of personal finance, understanding how your values, cultural background, cognitive patterns, and emotions influence financial decisions is essential. This chapter explores how these factors shape your financial attitudes and behaviors — from how you spend money to how you plan for the future. You’ll also learn strategies to identify biases, avoid scams, and make rational, informed choices that support your goals throughout life.

2.2 The Role of Personal and Societal Values

Your financial decisions are closely tied to your personal values — the principles that matter most to you. These values may include:

- Security: Building an emergency fund

- Environmental sustainability: Choosing eco-friendly investments

- Freedom: Prioritizing saving for early retirement

- Charity and giving back: Donating regularly to causes

Societal norms and peer expectations also shape your behavior. In cultures where material wealth is highly valued, people may feel pressured to buy luxury items or keep up with social trends, even if those choices conflict with personal goals.

예: Alex values environmental sustainability. Even though an electric vehicle has a higher initial cost, he buys one because it aligns with his personal and long-term financial values — and will save money on fuel over time.

2.3 Defining and Revising Your Concept of Wealth

Wealth is not one-size-fits-all. It’s more than money — it includes your values, goals, and what brings you a sense of security and purpose.

Wealth can include:

- Monetary assets: Cash, savings, property

- Non-monetary assets: Time, health, education, community support

- Personal goals: Freedom to travel, support a family, or pursue education

당신의 definition of wealth may evolve:

- Teenagers may view wealth as financial independence

- Parents may prioritize stability and children’s education

- Retirees may value freedom from financial stress and a secure legacy

2.4 Charitable Giving in Financial Planning

Charity is an important part of a values-based financial plan. Giving can:

- Support communities and causes you care about

- Provide tax benefits in some countries

- Increase personal satisfaction and purpose

Tips for responsible giving:

- Budget a specific amount monthly or yearly

- Research the charity (check ratings and reports)

- Make giving part of your long-term goals

예: Jamal sets aside 5% of his annual income to donate to education-focused nonprofits. It’s part of his values — and it fits into his broader savings plan.

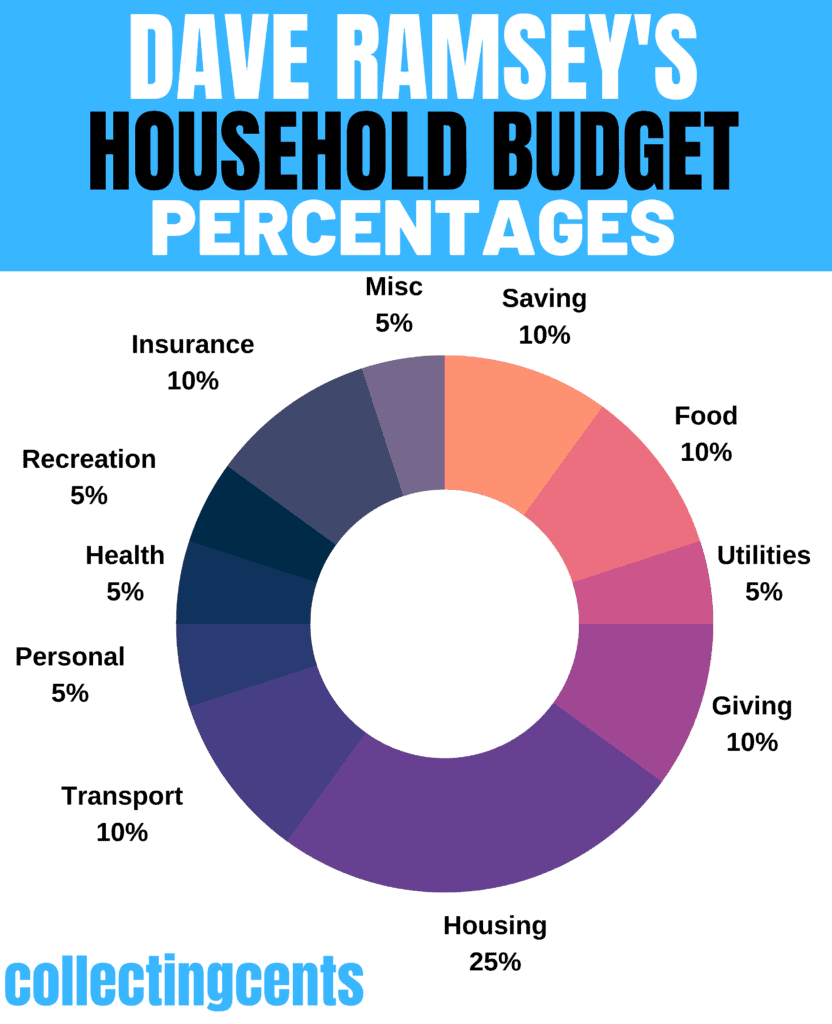

수치: Dave Ramsey’s Recommended Household Budget Percentages

설명:

This image provides a visual guide to financial expert Dave Ramsey’s recommended household budget based on monthly after-tax income. It breaks down spending into specific categories—such as housing, food, and savings—and assigns a percentage of income that should be allocated to each. The purpose of this guide is to provide a balanced framework for managing money effectively.

주요 시사점:

- This model suggests capping major expenses, with 주택 at 25%, 운송 at 10%, and 음식 between 10-15% of your take-home pay.

- A core principle of this budget is to prioritize financial well-being and generosity by dedicating 15% to 절약 and 10% to Giving.

- The budget provides a comprehensive plan by including all key spending areas like 유용, 건강, 보험, and personal spending.

- Following these recommended percentages helps create a balanced budget, preventing overspending in one area and ensuring funds are available for all financial priorities.

정보의 응용:

- You can use these budget percentages as a template to create your first household budget or to analyze your current spending habits.

- By comparing your own spending against these guidelines, you can quickly identify areas where you may need to cut back or adjust your allocations.

- This framework is a practical tool that helps you create a clear financial plan to achieve your goals, whether it’s saving for retirement, a down payment, or getting out of debt.

2.5 Understanding and Combating Behavioral Biases

Even financially smart individuals are affected by behavioral biases — mental shortcuts that lead to poor decisions.

Common Biases:

- 손실 회피: Fear of losing money is stronger than the joy of gaining it.

- 예: Emily is offered an investment opportunity where she could either lose $100 or gain $150. Even though the potential gain outweighs the loss, she declines because the fear of losing $100 feels more painful than the joy she would feel from gaining $150.

Strategies to reduce it:

- Focus on long-term investment goals rather than short-term market fluctuations.

- Reframe losses as opportunities to learn and rebalance your strategy.

- Use dollar-cost averaging (investing small amounts regularly) to reduce fear of investing at the “wrong time.”

- Set pre-defined rules for when to buy or sell to remove emotional reactions.

- 확인 편향: Only looking for information that supports what you already believe.

- 예: John believes that real estate is the only safe investment. When researching online, he only reads articles that support his view and ignores information about the risks of real estate or the benefits of diversifying with stocks or bonds.

Strategies to reduce it:

- Seek out opposing viewpoints and intentionally challenge your assumptions.

- Work with a financial advisor or peer review group that questions your investment decisions.

- Rely on data-driven research instead of opinions.

- Use objective tools like checklists or scoring systems when evaluating investments.

- 무리 심리: Doing what others are doing without analysis.

- 예: When Sarah sees that all her friends are investing in a trendy new cryptocurrency, she quickly buys some too, even though she doesn’t understand how it works — just because “everyone else is doing it.”

Strategies to reduce it:

- Make decisions based on personal financial goals, not market trends or peer pressure.

- Do independent research before making any investment or spending decision.

- Set a clear investment policy statement to stick to your long-term plan.

- Avoid following social media “hype” or investment fads without critical evaluation.

- Mental Accounting: Treating money differently depending on its source.

- 예: Mark receives a $500 tax refund and decides to splurge it on a vacation, even though he’s carrying $3,000 in credit card debt. He mentally treats the refund as “extra money” instead of using it responsibly to pay down his debt.

Strategies to reduce it:

- View all income and expenses through a unified budgeting and planning system.

- Treat all money the same, whether it’s a tax refund, a bonus, or regular income.

- Prioritize paying down high-interest debt or investing regardless of where the money came from.

- Establish automatic transfers to savings or investment accounts for all incoming money.

- 현재 편향: Prioritizing immediate gratification over long-term gains.

- 예: Lisa chooses to buy an expensive new phone today instead of putting that money into her retirement fund, even though saving would have helped her much more in the long run.

Strategies to reduce it:

- Automate savings and investment contributions to happen before discretionary spending.

- Create strong visual reminders of long-term goals (vision boards, goal trackers).

- Implement a “cooling-off” period before major purchases (e.g., 24–48 hours).

Break long-term goals into smaller, immediate milestones to stay motivated.

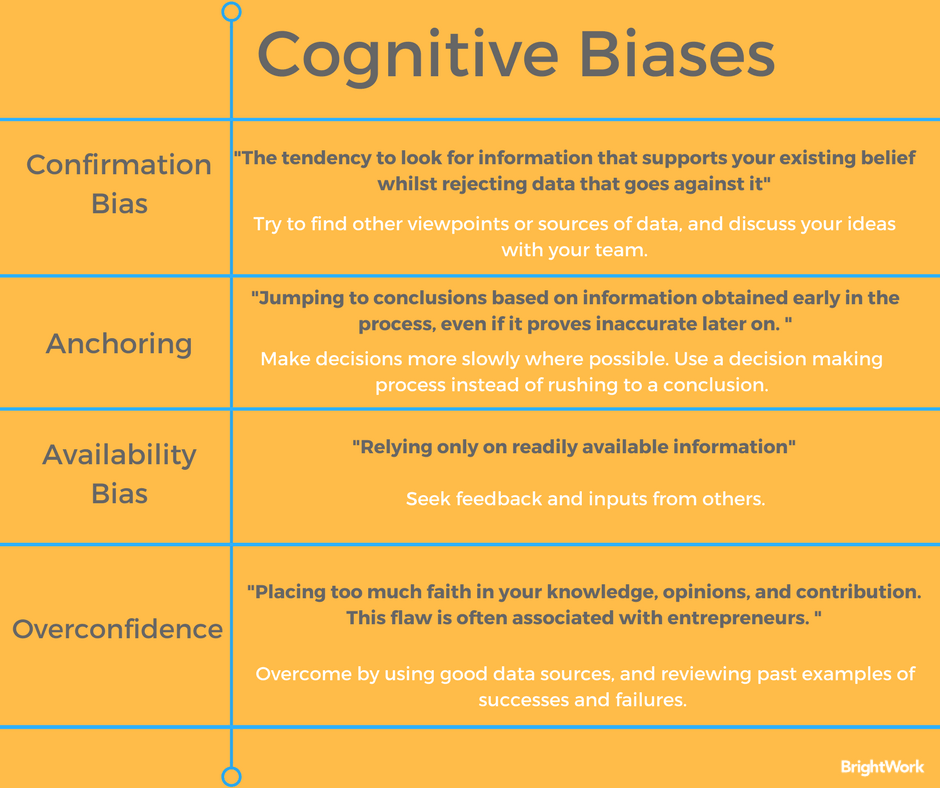

수치: Understanding Confirmation Bias

설명:

This image illustrates the concept of 확인 편향, which is our natural tendency to favor information that supports our existing beliefs or opinions. It shows that a person might actively search for data that confirms what they already think is true, while ignoring or dismissing information that challenges their view. This mental shortcut can lead to poor and unbalanced decision-making.

주요 시사점:

- Confirmation bias is a psychological tendency where you unintentionally look for evidence that proves you are right.

- This bias can create a “filter bubble,” where you only see information that reinforces your pre-existing beliefs.

- It causes you to give more weight to evidence that supports your view and less weight to evidence that contradicts it.

- To overcome this bias, you must make a conscious effort to challenge your own assumptions and actively seek out different perspectives.

정보의 응용:

- For 투자자들, confirmation bias is very risky because it can lead you to only pay attention to good news about a stock you like, while ignoring red flags or warning signs.

- To make better 투자 결정, you must actively fight this bias by looking for information that disagrees with your conclusion.

- This practice of seeking opposing viewpoints helps ensure your financial choices are based on a complete and objective 분석, not just on information that confirms what you hope is true.

Anchoring Bias

Anchoring bias happens when people rely too heavily on the first piece of information they receive — even if it’s outdated or irrelevant — when making a financial decision.

예: If you hear from a friend that a certain stock was $100 a year ago, you might judge its current $75 price as “cheap,” even if the company has had poor performance since. That first number acts as an “anchor,” affecting your judgment.

To overcome anchoring:

- 사용 current and reliable data

- 비교하다 multiple sources

- Be aware of emotional attachment to old prices or information

2.6 Delayed Gratification and Building Wealth

Delayed gratification is the ability to resist spending now to gain more later. It is essential for:

- Saving for large goals (e.g., home, retirement)

- Growing investments over time

- Avoiding debt

예: Instead of buying a new phone every year, Maria keeps hers for three years and uses the savings to invest monthly. Over five years, that adds up to $3,000 in investments.

This mindset shift is foundational for wealth-building.

2.7 Unconscious Beliefs: The Money Scripts

We all have money scripts — unconscious beliefs developed in childhood that influence how we think about money.

Types of money scripts:

- Money Avoidance: Believing money is bad or undeserved

- Money Worship: Thinking money solves all problems

- Money Status: Tying self-worth to financial success

- Money Vigilance: Being cautious and secretive about money

예: Someone raised to avoid money conversations may neglect budgeting or investing, harming long-term stability.

Awareness is the first step. Understanding your money scripts allows you to challenge them and make better choices.

2.8 The Role of Family, Culture, and Tradition

Your upbringing, culture, and community all shape your financial habits.

Examples of cultural differences:

- 저금: In many Asian cultures, high savings rates reflect deep-rooted values around security and family responsibility.

- 빚: In some cultures, debt is taboo. In others, it’s a common financial tool.

- Work Ethic: One society may value entrepreneurship, another may prioritize job stability in government roles.

- 투자: Some cultures prefer low-risk assets (like real estate), while others embrace stock markets.

예: In Japan, maintaining family honor often means avoiding debt, while in the U.S., it’s common to leverage credit to build wealth.

Being aware of these influences helps you choose which habits support your personal goals — and which ones to change.

2.9 Peer Pressure, Emotions, and Spending

Friends, family, and influencers can shape how we spend.

예: After seeing her friends post luxury vacation photos, Jenna feels pressure to book an expensive trip — even though she’s saving for a car.

Social media, fashion trends, and advertising can trigger emotional decisions that delay financial progress.

Strategies:

- Set clear goals to stay focused

- Use budgeting apps to track behavior

- Surround yourself with supportive people

Reflect before large purchases

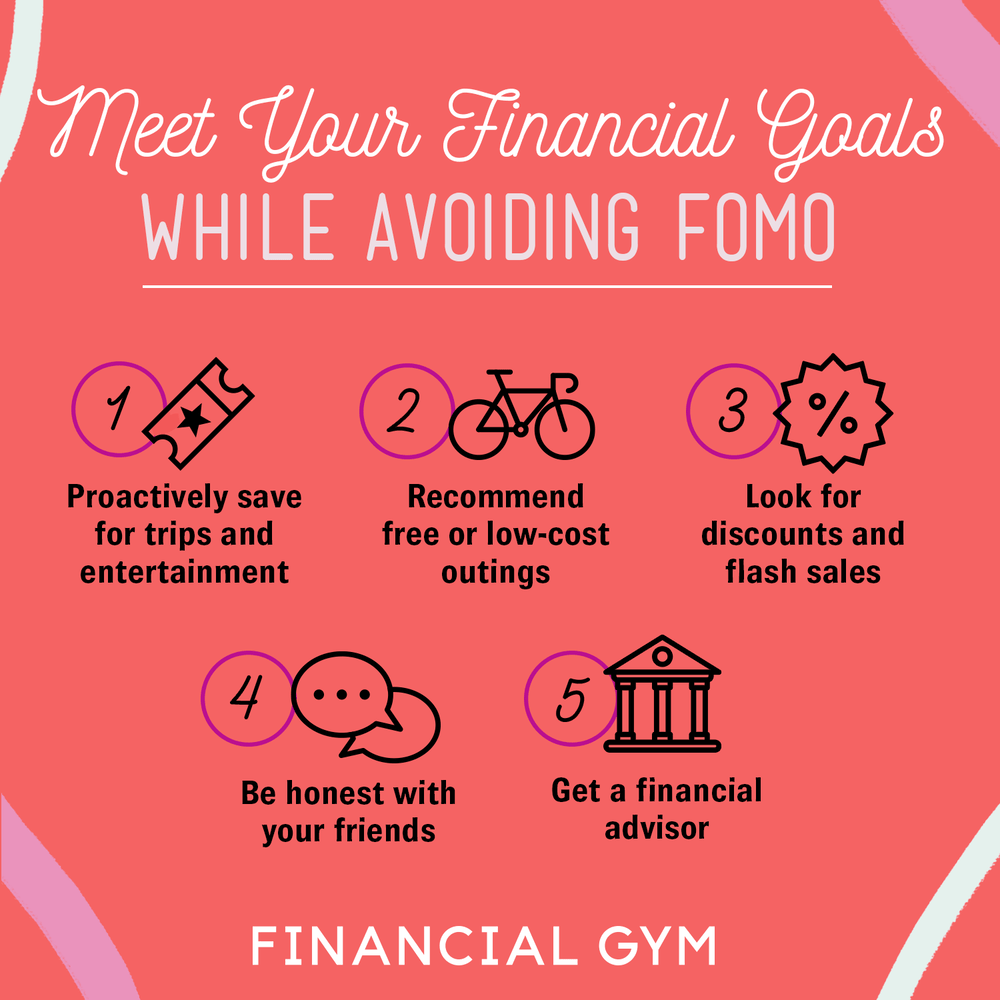

Figure: How to Meet Financial Goals and Avoid FOMO

설명:

This image provides a helpful guide on how to manage the “Fear Of Missing Out,” or FOMO, while working towards your personal financial goals. It outlines several practical strategies that allow you to maintain a healthy social life without overspending and jeopardizing your savings. The core message is that you can find a happy medium between enjoying the present and saving for the future with intentional planning.

주요 시사점:

- FOMO is the feeling of anxiety that you are missing out on exciting events, which can lead to impulsive spending that harms your financial health.

- Having clearly defined financial goals gives you a strong reason to say “no” to expensive outings and stay motivated to save.

- A successful strategy is to create a budget that specifically includes a “fun money” category, so you can spend on social activities without guilt.

- Being open with your friends about your budget and suggesting low-cost or free activities can help you stay social without breaking the bank.

정보의 응용:

- By learning to manage FOMO, you develop the discipline to control your discretionary spending, which directly increases the amount of money you can save and invest.

- For investors, this skill is critical because it frees up more capital to put towards your investment portfolio, allowing your wealth to grow faster.

- Mastering this balance helps you avoid lifestyle inflation (increasing spending as income rises) and builds a strong foundation for achieving long-term financial independence.

2.10 Navigating Financial Partnerships

Fintech tools help reduce emotional decision-making:

- Robo-advisors: Automatically manage your investments

- Budgeting apps: Categorize and track spending

- Savings automations: Move money into savings without thinking

예: Sam uses a robo-advisor that adjusts her investments based on market trends, helping her stay on track even during downturns.

These tools keep you focused on your goals — not your impulses.

2.12 Using Multiple Sources of Financial Information

Making good financial decisions means using objective, accurate, and current sources — not just social media or sales reps.

Reliable sources include:

- Certified financial planners

- Financial news sites (e.g., Bloomberg, Reuters)

- Government websites (e.g., IRS.gov, SEC.gov)

- Product prospectuses and disclosures

예: Before investing, Maya reads independent reviews, a fund’s prospectus, and talks to a certified advisor. She chooses an index fund that aligns with her goals.

Always fact-check, cross-reference, and consider the source’s intentions before making financial moves.

2.13 Identifying Scams and Fraud

Understanding how to spot fraud is key to financial safety.

Common types of scams:

- Phishing emails pretending to be banks

- “Too good to be true” investment offers

- Fake online stores or giveaways

- Romance scams

Red flags:

- Urgency or threats (“Act now or lose everything!”)

- Requests for personal information or money

- Untraceable payment methods (gift cards, crypto)

Tip: Use reputable sites. Report suspicious activity. Keep software and devices secure.

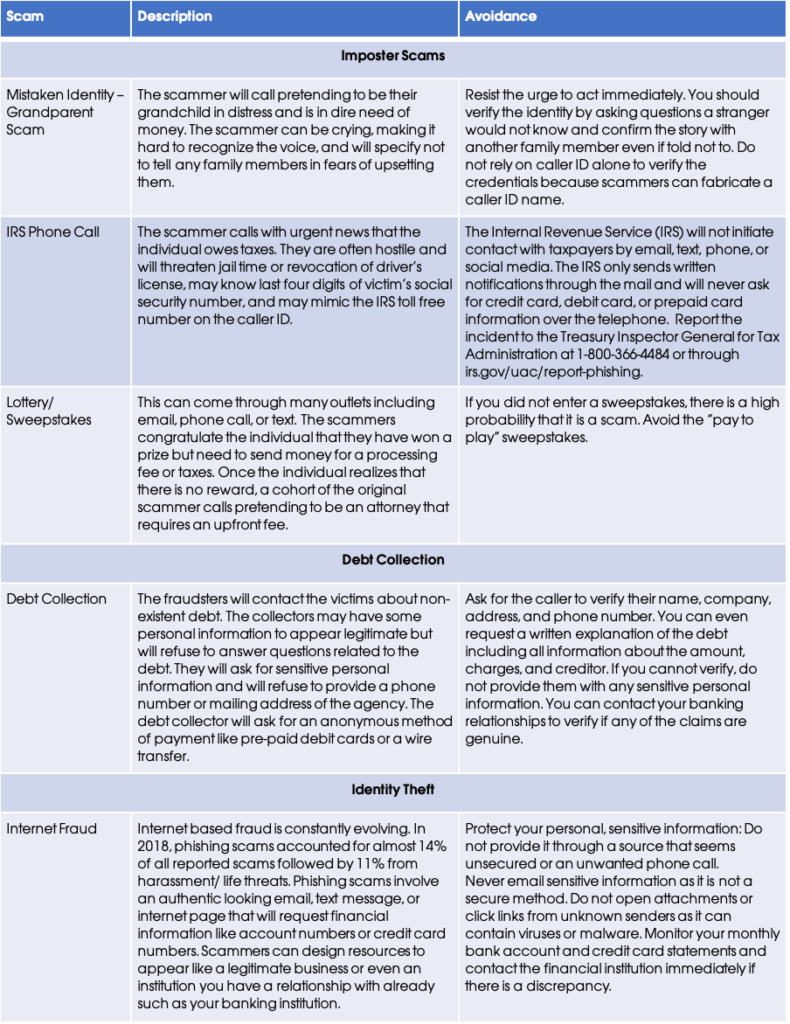

Figure: Common Financial Scams

설명:

This image serves as a public service announcement, highlighting several of the most common financial scams designed to trick people into giving away their money or personal information. It visually represents different fraudulent tactics, such as impostor scams and fake prizes, to help individuals recognize the warning signs. The main goal is to increase awareness and help people protect themselves from becoming victims of fraud.

주요 시사점:

- Scammers often create a sense of urgency or excitement, like claiming you have won a lottery or owe money to the government, to rush you into making a bad decision.

- Be wary of impostor scams, where someone pretends to be from a trusted entity like a bank, tech support, or a government agency to gain your trust.

- A major red flag for any prize or offer is a requirement to pay an upfront fee to receive it, especially if the payment is requested via gift card or wire transfer.

- Phishing is a common digital scam that uses deceptive emails or text messages, which look legitimate, to steal your passwords and personal data.

정보의 응용:

- Being aware of these scams is the first line of defense in protecting your money and identity from criminals.

- For investors, it is crucial to critically evaluate any investment opportunity, especially those that promise guaranteed high returns with little or no risk, as this is a classic sign of an investment scam.

- Always verify information independently by contacting the company or organization through their official channels, not through any links or phone numbers provided in an unsolicited message.

2.14 Rational Decision-Making in Practice

ㅏ rational decision-making process helps avoid emotional or impulsive choices.

Steps:

- Identify the problem or goal

- List possible options

- Determine your decision criteria

- Compare each option against those criteria

- Make the best choice

Example: Should I invest in stock A or B?

Option | Risk Level | Long-term Return | Ethical Fit | Score |

Stock A | Medium | High | Yes | 9 |

Stock B | Low | 보통의 | No | 6 |

Cost-benefit thinking helps you stay focused on facts and goals — not peer pressure or short-term gains.

결론

Financial behaviors are shaped by values, emotions, culture, and unconscious biases — but awareness and planning help you take control. By building strong habits, using objective sources, discussing finances openly, and making rational decisions, you can create a secure financial future that reflects your personal definition of success and wealth.

주요 수업 정보:

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elittellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.