Pasaulinis: asmeninių finansų supratimas

Lesson Learning Objectives:

Įvadas:

This section aims to help users understand the fundamentals of personal finance, including how to manage money, budget, save, and invest effectively. It emphasizes making informed decisions to achieve financial security and improve quality of life.

- Understand the Basics of Personal Finance: Learn how to manage income, expenses, savings, and investments to achieve both short- and long-term financial goals. This knowledge helps you navigate everyday financial decisions and build a foundation for financial security.

- Learn Financial Planning and Budgeting: Gain skills to create a financial plan that includes setting financial goals, creating a budget, and preparing for unexpected expenses. Understanding budgeting helps you allocate funds effectively, avoid overspending, and save for future needs.

- Distinguish Between Needs and Wants: Identify the difference between essential needs (housing, food, healthcare) and non-essential wants (luxuries, entertainment). This skill helps prioritize spending, allocate resources wisely, and improve budgeting.

- Develop Saving and Investing Strategies: Explore how saving provides financial security for short-term goals, while investing helps achieve long-term growth. This understanding will guide decisions about where to allocate funds, depending on financial goals and timeframes.

A. Understanding Personal Finance

Personal finance involves managing your money, savings, investments, and debt in a way that helps you meet both short- and long-term financial goals. It covers a wide range of activities, from everyday budgeting to saving for future needs, like education or retirement. The key to personal finance is making informed decisions that balance income, expensesir financial responsibilities to ensure financial security and stability.

Globally, personal finance plays a vital role in determining an individual’s quality of life. Whether you’re managing a family budget, planning a significant purchase, or preparing for retirement, understanding personal finance helps you navigate life’s financial challenges.

B. The Essentials of Financial Planning and Budgeting

Financial planning involves setting financial goals and creating a roadmap to achieve them. The first step in financial planning is creating a budget. A budget helps you manage your income and expenses by allocating funds toward essential items like housing, food, and bills while ensuring you have money for savings and investment.

A solid financial plan also includes preparing for unexpected events, like medical emergencies, job loss, or market downturns. Having an emergency fund—typically 3-6 months’ worth of living expenses—can provide a financial cushion.

When creating a budget, it’s important to follow these steps:

- Track your income: Understand how much money you have coming in from your job, investments, or other sources.

- List your expenses: Break down your essential expenses (rent, utilities, groceries) and non-essential spending (entertainment, dining out).

- Set financial goals: Establish both short-term (vacation, small savings) and long-term goals (retirement, buying a home).

- Adjust your budget: Make sure your expenses don’t exceed your income, and allocate money for savings.

Following a budget helps you avoid overspending, manage debt, and prioritize saving for future goals.

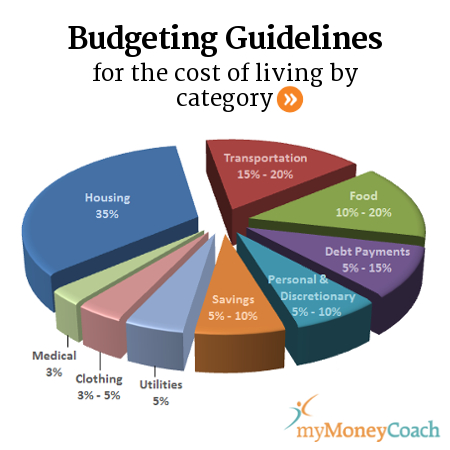

Paveikslėlis: Budgeting Guidelines for the Cost of Living by Category

Aprašymas:

This figure presents suggested budgeting guidelines that categorize living expenses into different percentages of an individual’s total income. The largest portion is allocated to housing (35%), followed by transportation (15-20%) and food (10-20%). Other important categories include debt payments (5-15%), personal and discretionary spending (5-10%), and savings (5-10%). Smaller portions are assigned to utilities (5%), clothing (3-5%), and medical expenses (3%). These percentages provide a clear framework for how to effectively allocate income to different living costs.

Svarbiausios išvados:

- Housing is the largest expense, typically requiring 35% of the budget.

- Transportation ir food take up the next largest portions, together consuming up to 40% of income.

- Savings ir debt payments are essential financial considerations, with recommendations of 5-15% for each.

- Smaller but important categories like medical, clothingir utilities should be capped at 3-5%.

Application of Information:

These budgeting guidelines help individuals plan their finances by suggesting reasonable percentages for different expenses. By following these recommendations, users can ensure that they allocate adequate amounts to essential areas like housing, savingsir food while controlling discretionary spending. This data is particularly useful for those learning how to manage personal finances effectively.

C. Defining Needs and Wants

One of the core principles of personal finance is understanding the difference between needs and wants. Needs are the basic items necessary for living, such as housing, food, and healthcare. Wants are additional luxuries or conveniences, such as dining out, vacations, or the latest gadgets.

Being able to distinguish between needs and wants is critical to managing your budget effectively. For example, when making a spending decision, ask yourself if the purchase is essential or if it can be postponed or avoided altogether. This mindset helps prioritize saving for future financial goals while avoiding unnecessary debt.

Paveikslėlis: Needs vs. Wants

Aprašymas:

This figure contrasts needs ir wants by providing clear examples of each. Needs are described as essential items for living a healthy and safe life, such as housing, transportation, foodir medical care. In contrast, wants represent comforts and luxuries that enhance life but are not necessary, including travel, entertainment, subscriptionsir luxury goods. This distinction helps individuals understand the difference between essential and discretionary spending.

Svarbiausios išvados:

- Needs are vital for survival and include basic expenses like housing, foodir healthcare.

- Wants are non-essential items such as luxuries, entertainmentir subscriptions.

- Understanding the difference between needs ir wants is key to effective budgeting and financial planning.

- Prioritizing needs over wants helps individuals make smarter financial decisions, especially when managing a tight budget.

Application of Information:

By distinguishing between needs ir wants, individuals can allocate their financial resources more effectively. Understanding this difference is crucial for maintaining a healthy financial balance, particularly in budgeting. For investors, identifying and managing spending priorities can lead to better savings and investment strategies, ensuring long-term financial security while allowing for discretionary spending on wants when appropriate.

D. Saving and Investing for the Future

Saving and investing are essential to achieving long-term financial security. Saving involves setting aside money for short-term goals or emergencies, while investing allows your money to grow over time through financial vehicles such as stocks, bonds, or real estate.

- Saving: Build an emergency fund to cover unexpected expenses. Savings accounts provide security but typically offer lower interest rates. Savings should be easily accessible for emergencies or short-term goals.

- Investing: Long-term financial goals like retirement often benefit from investicijos that have the potential to grow over time. Stock market investments, for example, offer higher returns than savings accounts, though they come with more risk. Bonds ir real estate offer more stability but may have lower returns.

For example, if you’re saving for a house down payment within 3 years, putting your money into a high-interest savings account arba low-risk bonds may be the best approach. For longer-term goals like retirement, investing in stocks ir diversified portfolios can help you grow your wealth over time.

Regularly reviewing your savings and investments ensures that they align with your financial goals and risk tolerance.

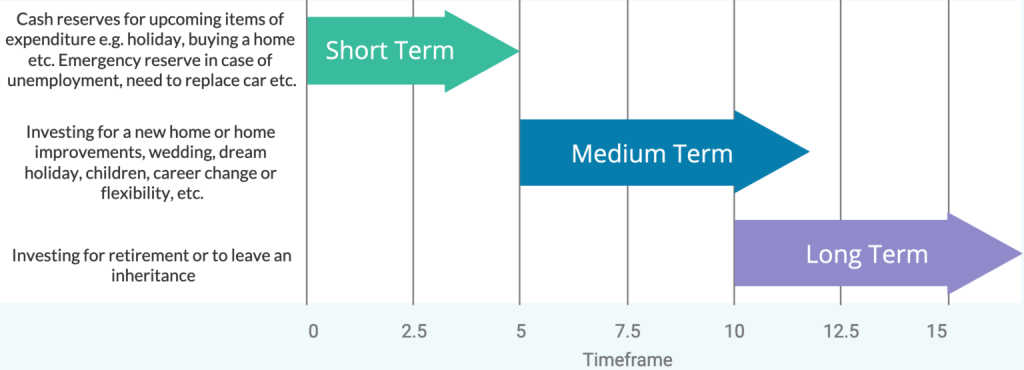

Figure: Investment Timeframes: Short, Medium, and Long Term

Aprašymas:

This figure outlines different investment timeframes and their purposes. Short-term investments (0-5 years) are designed for immediate needs such as building cash reserves for emergencies or upcoming expenditures like holidays or buying a car. Medium-term investments (5-10 years) are typically used for larger financial goals such as purchasing a new home, funding a wedding, or preparing for significant life changes like a career shift. Long-term investments (10+ years) focus on major future events like retirement or leaving an inheritance. Each timeframe requires a different investment strategy to meet financial goals within the specified periods.

Svarbiausios išvados:

- Short-term investments provide liquidity for immediate needs or emergencies.

- Medium-term investments are suited for larger life goals within 5-10 years, such as home purchases or weddings.

- Long-term investments aim to secure financial futures through retirement planning or inheritance.

- Understanding the time horizon helps tailor investment strategies to meet specific financial objectives.

Application of Information:

For investors, recognizing the different investment timeframes helps in selecting appropriate financial vehicles. Short-term investments may require low-risk, easily accessible funds, while long-term investments can tolerate higher risk for potentially greater returns. Knowing how to align personal or financial goals with the right timeframe is essential for effective financial planning.

Pagrindinė pamokos informacija:

- Personal Finance Management: Managing personal finance involves balancing income, expenses, and financial responsibilities. Understanding this concept allows users to make informed decisions that align with their financial goals and improve financial security.

- Budgeting is Essential: A well-planned budget helps control spending, reduce debt, and prioritize saving. By tracking income and expenses, users can ensure that their financial resources are used effectively to meet both short- and long-term needs.

- Needs vs. Wants: Recognizing the difference between needs and wants is crucial in personal finance. By prioritizing needs over wants, users can manage resources better, save more efficiently, and avoid unnecessary debt.

- Saving for Short-Term Goals: Building an emergency fund is a key part of financial planning. Setting aside 3-6 months’ worth of living expenses in a savings account helps protect against unexpected costs and provides financial stability.

- Investing for Long-Term Growth: Investing in assets like stocks, bonds, and real estate can help achieve long-term financial goals, such as retirement. Knowing different investment timeframes (short, medium, long) helps users align their investments with specific financial objectives.

Baigiamasis pareiškimas: A strong grasp of personal finance principles helps users make informed financial decisions that support stability, growth, and well-being. By understanding budgeting, saving, and investing, users can set and achieve financial goals while navigating everyday financial challenges effectively.