This section focuses on long-term financial planning and the importance of balancing immediate needs with future goals. By understanding how to build assets, manage liabilities, and prepare for major life events, you can secure financial stability over time.

Understand the importance of long-term planning by learning how to balance short-term needs with bigger financial goals. This knowledge will help you set priorities and make better decisions about saving, investing, and budgeting.

Learn strategies for planning major life events, like buying a house or retirement. You’ll see how to manage financial changes and prepare for both expected and unexpected costs, improving your ability to adapt to changing circumstances.

Explore end-of-life financial planning to ensure your assets are distributed according to your wishes. Understanding wills, trusts, and life insurance will give you confidence in making decisions that protect your family’s future.

Build confidence in monitoring assets and investments by tracking their growth and understanding how liabilities affect financial decisions. You’ll learn to adjust plans based on performance and financial changes, helping you stay on course toward your long-term goals.

Introduksjon

Planning for the long term is an essential aspect of building financial security and stability. While short-term needs must be managed effectively, long-term financial planning ensures that individuals can achieve larger financial goals, such as buying a home, saving for retirement, or providing for dependents. This chapter explores how to balance immediate needs with future financial goals, plan for life events, and manage assets and liabilities over time. Understanding the importance of long-term financial strategies allows individuals to create a secure foundation for the future while maintaining flexibility to adjust plans as circumstances change.

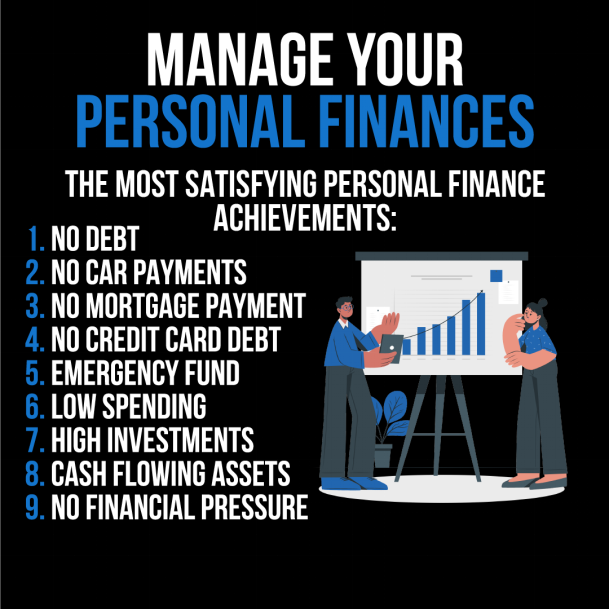

Figure: The infographic is a motivational guide titled "Manage Your Personal Finances," highlighting the most satisfying achievements in personal finance management. It lists nine key milestones, including having no debt, no car or mortgage payments, no credit card debt, establishing an emergency fund, maintaining low spending, making high investments, owning cash-flowing assets, and experiencing no financial pressure. This visual serves as a checklist for individuals aiming to achieve financial freedom and stability. To make this information practical, users should assess their current financial situation against these milestones and create a plan to address each area systematically. Starting with a budget to track spending and making a plan to pay down debts could be initial steps towards these goals.

Understanding the Importance of Long-Term Planning

While managing short-term needs is important, keeping an eye on long-term financial goals is essential for building and maintaining financial stability. Long-term financial planning includes preparing for significant life events such as buying a home, retirement, eller supporting dependents. It also involves saving for future emergencies and considering strategies to grow wealth over time.

Long-term planning often requires different types of financial products compared to emergency savings. While emergency savings should be easily accessible in case of immediate needs, long-term financial products, such as investment accounts, pension plans, eller fast eiendom, are designed to grow over time and provide financial security for future needs.

Balancing Short-Term and Long-Term Needs

Balancing immediate needs with long-term financial goals is a critical skill. Short-term financial pressures, such as daily living expenses, can sometimes overshadow long-term planning. However, developing strategies to overcome procrastination and ensuring that long-term goals remain a priority is crucial for achieving financial security.

One way to balance these priorities is to create a budsjett that allocates funds toward both immediate needs og long-term savings. By setting aside a portion of income each month for retirement, investments, or future financial needs, individuals can ensure that they stay on track for their long-term goals without neglecting current obligations.

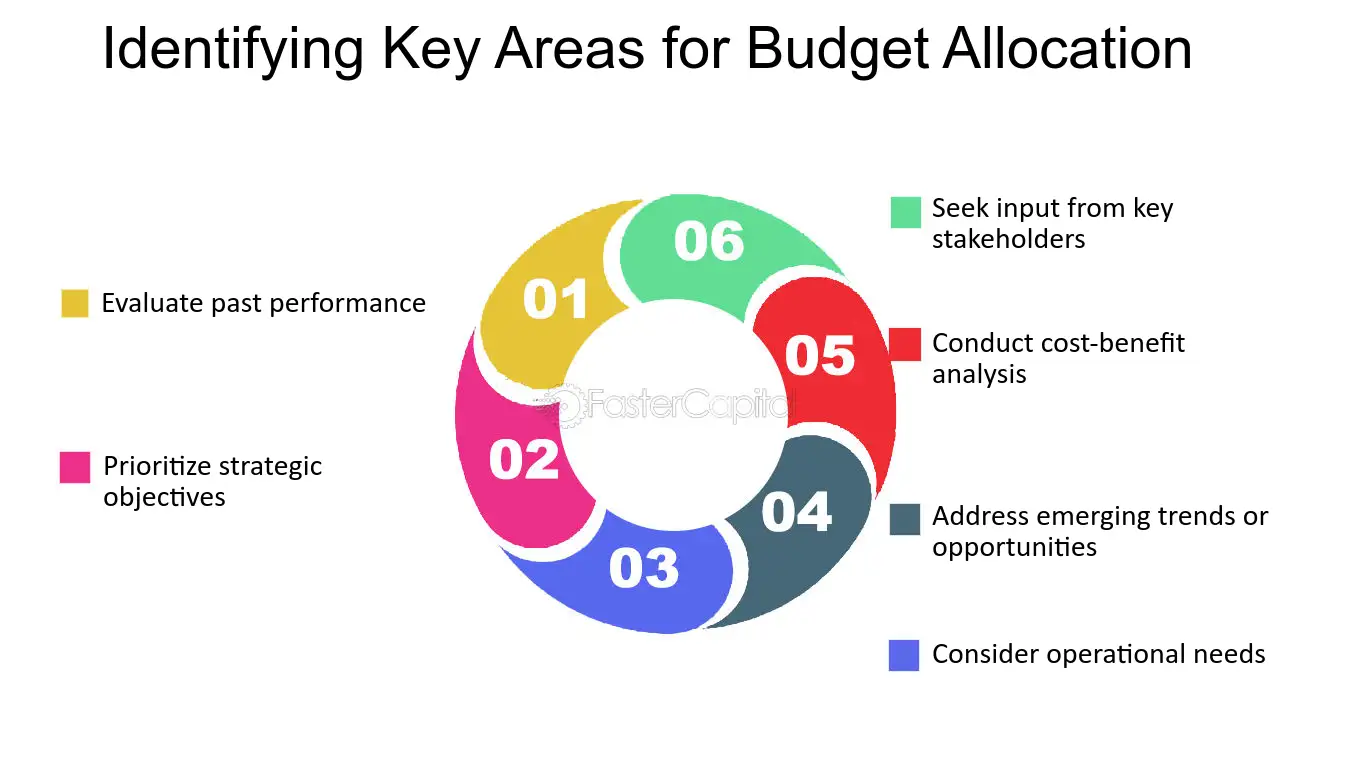

Figure: Identifying Key Areas for Budget Allocation

Beskrivelse:

The figure outlines six key areas to focus on when allocating a budget: evaluating past performance, prioritizing strategic objectives, considering operational needs, addressing emerging trends or opportunities, conducting cost-benefit analysis, og seeking input from key stakeholders. Each element is presented as a section of a circular flow, emphasizing the continuous nature of effective budget allocation.

Viktige takeaways:

Evaluating past performance helps in understanding which areas were successful or need improvement.

Strategic objectives should be prioritized to align the budget with company goals.

Operational needs must be considered to ensure smooth daily functions.

Emerging trends and opportunities should be addressed to stay competitive.

Cost-benefit analysis helps in making data-driven financial decisions.

Stakeholder input ensures the budget reflects diverse perspectives and needs.

Anvendelse av informasjon:

This framework is useful for investors og managers to ensure budgets are effectively allocated by considering past performance and future needs. By addressing strategic objectives, operational requirements, and seeking stakeholder input, financial planners can create more efficient and impactful budgets.

Planning for Life Events

Major life events—such as marriage, childbirth, education, og retirement—often have significant financial implications. It is important to make financial plans for both positive og negative events that are likely to have long-term consequences. This could involve saving for future education costs for children, planning for healthcare expenses in retirement, or ensuring that there is sufficient insurance coverage in case of emergencies.

It’s also important to consider the possibility of predictable fluctuations in income or expenses when making long-term plans. For example, income may decrease upon retirement, while healthcare costs may increase. Taking these fluctuations into account allows individuals to adjust their long-term financial plans accordingly.

End-of-Life Planning

End-of-life financial planning is an often-overlooked aspect of long-term planning. It’s important to make decisions about how outstanding debts, kostnader, og assets should be handled. Writing a will ensures that assets are distributed according to one’s wishes and that any remaining debts are properly managed.

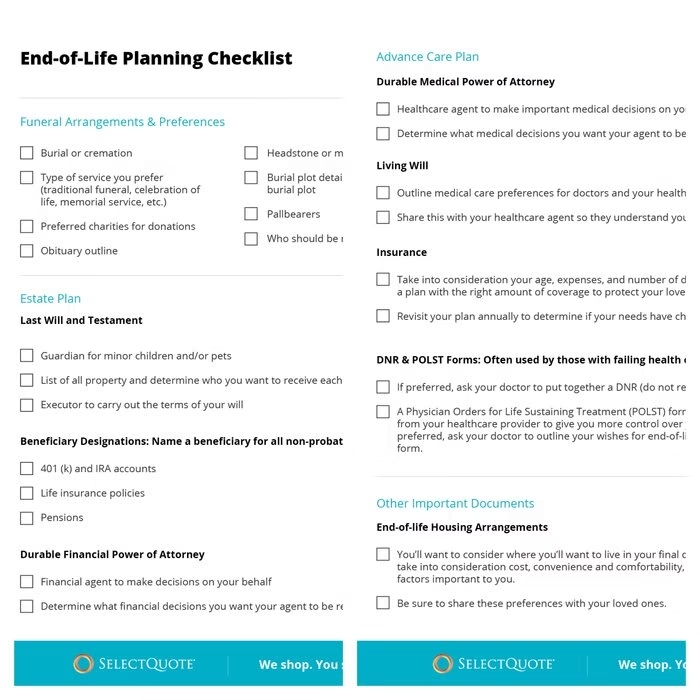

Figur: End-of-Life Planning Checklist

Beskrivelse:

This figure presents a comprehensive checklist that helps individuals organize and plan for end-of-life decisions. It is divided into key sections: Funeral Arrangements & Preferences, Estate Plan, Advance Care Plan, og Other Important Documents. Each section covers critical decisions such as burial or cremation preferences, beneficiary designations, durable powers of attorney, living wills, insurance reviews, and the necessary forms for end-of-life care. The checklist serves as a guide to ensure all important decisions are addressed.

Viktige takeaways:

Funeral preferences such as burial or cremation, headstone, and pallbearers should be documented.

Estate planning includes creating a will, naming guardians for children or pets, and designating beneficiaries.

Advance care planning involves durable medical power of attorney, living wills, and insurance considerations.

Important documents like DNR forms and end-of-life housing arrangements should be discussed and outlined.

Planning ensures that family members are aware of your preferences, reducing stress during difficult times.

Anvendelse av informasjon:

Investors and individuals can use this checklist to ensure that they have comprehensive plans in place for both their estate and end-of-life preferences. It provides a structured approach to preparing for future events and ensures that one’s wishes are clearly outlined, protecting both financial assets og personal wishes during critical moments.

Monitoring Investments, Assets, and Liabilities

Financial planning also involves regularly monitoring the value of one’s investments, assets, og liabilities. By keeping track of how investments perform over time and understanding how assets grow eller depreciate, individuals can make informed decisions about when to adjust their plans or rebalance their portfolios.

It is also crucial to consider household assets and liabilities when making long-term plans. For example, paying off a mortgage can increase home equity and contribute to long-term financial security, while ongoing liabilities like credit card debt may limit future financial flexibility. Understanding these factors allows for better decision-making about when to invest, save, eller adjust spending.

Financial Support for Family and Community

Long-term planning should also take into account the possibility that family members or members of the community may require financial support in the future. Whether it’s providing financial assistance to aging parents or helping adult children with housing or education costs, individuals should factor these potential obligations into their financial plans.

Planning for these needs in advance ensures that financial support can be provided without jeopardizing one’s own long-term financial goals.

Taking Action on Long-Term Financial Plans

Putting long-term financial plans into action requires both confidence og flexibility. It is essential to regularly review and update long-term plans to account for changes in financial circumstances, such as income fluctuations or changes in personal goals. Being confident in making adjustments when necessary allows individuals to stay on course toward achieving their long-term financial objectives.

Taking action could involve investing in retirement accounts, setting up automatic contributions to long-term savings, or seeking professional advice to ensure that long-term goals are aligned with personal financial circumstances.

Figure: A visual representation of financial planning, wealth management, and retirement strategies, featuring a large calculator, growth charts, a money bag, and a retirement checklist. This image highlights the key stages of managing personal finances.

Viktig informasjon om leksjoner:

Long-term financial planning is crucial for financial stability. It involves preparing for major life events, managing assets, and considering future emergencies. This approach helps you secure your financial future while still addressing short-term needs.

Balancing short-term and long-term needs is key to financial success. By budgeting for both immediate expenses and long-term savings, you can avoid neglecting future goals while still managing daily living costs effectively. Consistent savings towards long-term goals, such as retirement, ensures progress without financial strain.

Major life events can greatly impact your financial situation. Planning for changes like marriage, childbirth, or retirement helps you manage income fluctuations and unexpected costs. Being prepared ensures that you can adjust your finances without compromising stability.

End-of-life planning is essential for protecting your family’s financial well-being. Writing a will, setting up trusts, and having life insurance in place ensure that your assets are distributed according to your wishes and that dependents are provided for after your passing.

Regular monitoring of assets, investments, and liabilities is necessary for maintaining financial health. By tracking how investments perform and understanding the impact of liabilities, you can make informed decisions and adjust your plans to maintain a secure financial future.

Taking action on long-term plans requires confidence and regular adjustments. Whether investing in retirement accounts, setting up automatic savings, or seeking professional advice, it’s important to stay proactive in managing your financial goals. This approach builds a solid foundation for achieving financial freedom.

Avsluttende uttalelse: Long-term financial planning is about more than just saving money—it’s about creating a secure future by setting clear goals, preparing for life’s changes, and managing assets and liabilities wisely. By taking informed action, you can confidently work towards financial independence and protect your family’s future.