Local: Debt and Debt Management Standards

Lesson Learning Objectives:

Introduction:

This section focuses on debt management and the importance of building emergency savings to maintain financial stability. By learning about debt, its implications, and strategies to manage it effectively, users can make informed financial decisions and prepare for unexpected expenses.

- Understand the Burden of Debt: Learn how debt can impact both current and future financial well-being. Users will understand how debt affects financial freedom and why managing it responsibly is crucial for long-term financial health.

- Monitor Debt and Credit Use: Discover how tracking debt levels and maintaining a manageable debt-to-income ratio can help protect credit scores. This knowledge helps users maintain financial stability and access better borrowing options.

- Take Early Action to Manage Debt: Understand the importance of taking proactive steps to address debt, such as prioritizing debt payments and reducing discretionary spending. Users will gain the confidence to make early adjustments to avoid escalating financial problems.

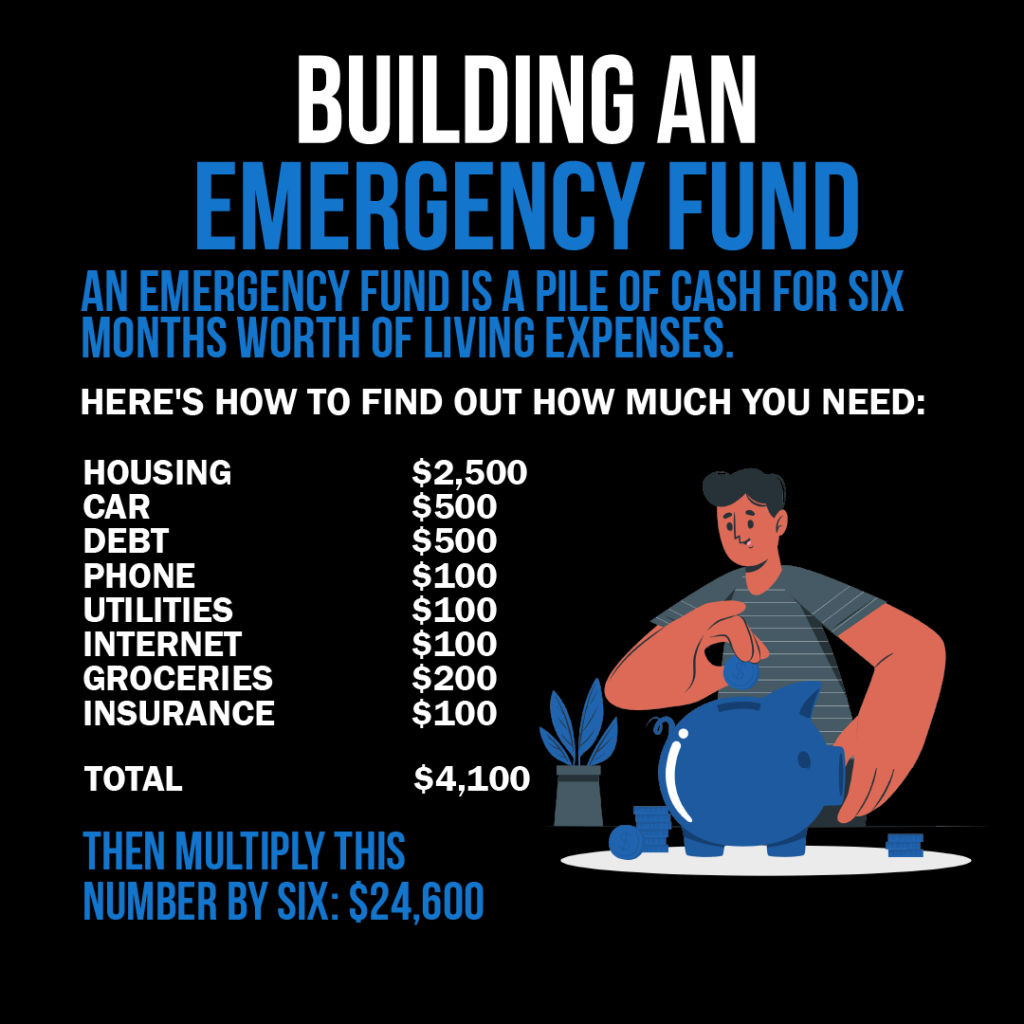

- Establish Emergency Savings: Learn how to build an emergency fund to provide a financial cushion during unexpected situations, reducing reliance on credit. This helps ensure a stable financial foundation.

- Explore Debt Management Solutions: Gain insights into debt relief agencies, credit counseling, and legal mechanisms like over-indebtedness procedures, which help reduce or manage debt more effectively.

Introduction

Debt management and saving for emergencies are essential aspects of financial well-being. While debt can be a useful tool for achieving significant financial goals, it also requires careful management to avoid becoming a burden. This chapter explores the importance of understanding debt, monitoring debt levels, and taking early action to address potential problems. It also emphasizes the role of emergency funds in providing financial security and preventing reliance on credit during unexpected financial challenges. By adopting responsible borrowing practices and building savings, individuals can maintain financial stability and meet both short-term and long-term goals.

Understanding the Burden of Debt

Debt can be a significant financial burden if not managed properly, impacting both current and future financial well-being. Financial well-being refers to having enough money to meet your current needs and future goals, without being overwhelmed by financial stress. If debt is not carefully monitored and managed, it can disrupt daily life by limiting financial freedom and flexibility.

For example, taking on too much credit card debt or a high-interest loan can mean using most of your income for repayments, leaving little room for savings, investing, or even basic expenses such as rent or groceries.

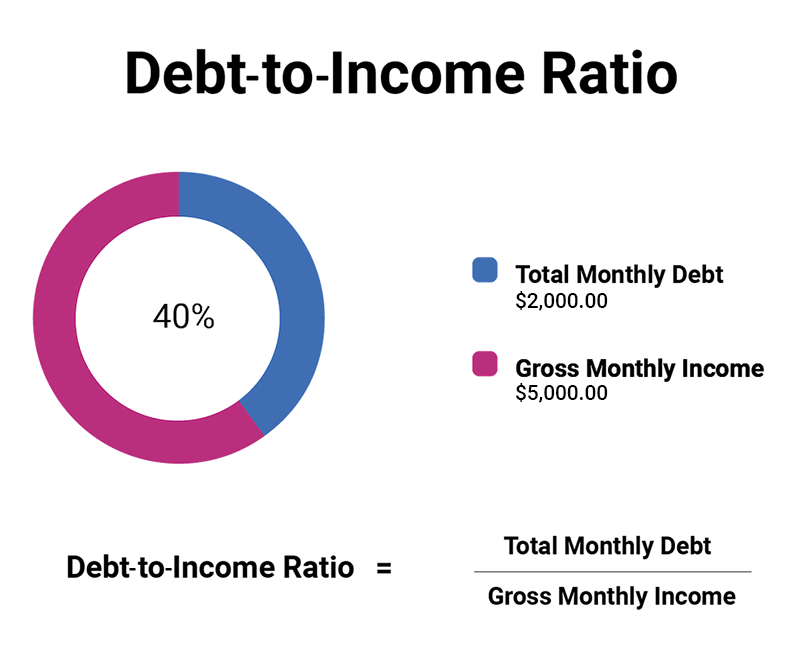

Figure: Debt-to-Income Ratio

Description:

The figure illustrates the concept of the debt-to-income (DTI) ratio, which compares an individual’s total monthly debt to their gross monthly income. In this example, the total monthly debt is $2,000, while the gross monthly income is $5,000, resulting in a DTI ratio of 40%. This ratio helps in assessing a person’s ability to manage monthly debt payments in relation to their income.

Key Takeaways:

- Debt-to-Income Ratio shows how much of your income goes towards paying debt.

- A 40% DTI ratio suggests that 40% of the income is used to cover debt payments.

- Lower DTI ratios are generally preferred by lenders, as they indicate better financial health.

- This ratio is crucial for loan approvals, especially in determining eligibility for mortgages and other loans.

Application of Information:

Understanding the Debt-to-Income Ratio can help individuals evaluate their financial situation and identify if they are taking on too much debt. It is an essential tool for investors and borrowers to determine loan eligibility and assess their capacity to handle additional loans responsibly.

Monitoring Debt Levels and Credit Use

An important step in debt management is monitoring the ratio of debt to income. The debt-to-income ratio is a financial measure used to compare the total amount of monthly debt payments to your gross monthly income. A lower ratio indicates healthier finances, while a higher ratio suggests potential financial trouble.

For example, if your monthly income is €2,000 and you spend €500 on debt payments, your debt-to-income ratio is 25%. Lenders usually prefer a ratio of 36% or lower.

Maintaining a manageable debt-to-income ratio helps protect credit scores and overall financial health. Credit scores are numerical ratings that reflect an individual’s creditworthiness, based on their credit history and ability to repay debts. A high credit score can help you qualify for loans with lower interest rates, while a low score can make borrowing more expensive or difficult.

It’s essential to regularly monitor overall credit use, which refers to the total amount of credit you are using compared to your credit limit. Using a high percentage of your available credit can negatively affect your credit score, so it’s important to keep credit utilization below 30% of your total credit limit.

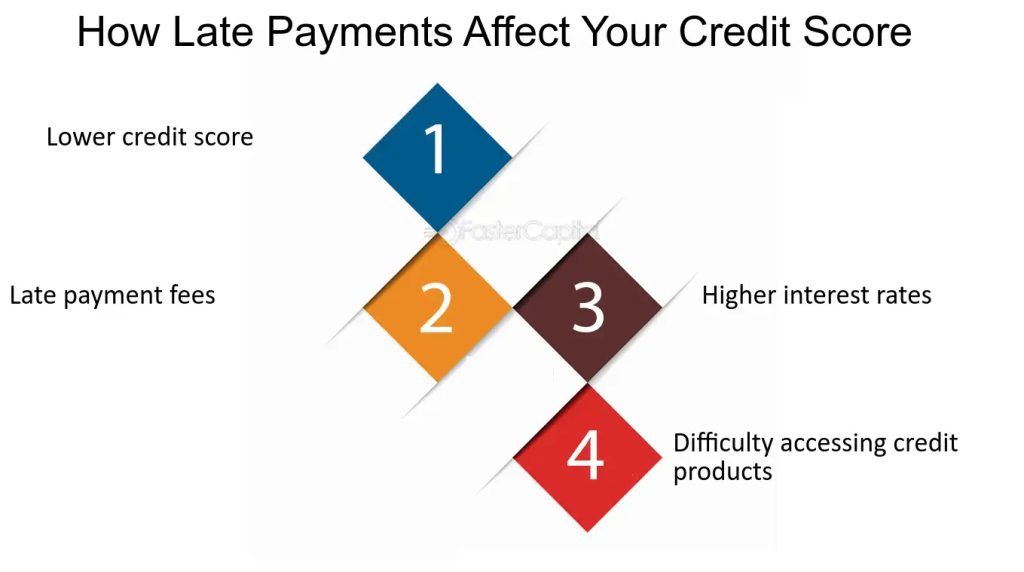

Figure: How Late Payments Affect Your Credit Score

Description:

The image outlines four key consequences of late payments on your credit score. It emphasizes that making late payments can lead to a lower credit score, late payment fees, higher interest rates on future loans, and difficulty in accessing new credit products. Each consequence is presented in a stepwise format, highlighting the significant effects of delayed payments.

Key Takeaways:

- Lower credit score: Missing payments can reduce your credit score, impacting your financial reputation.

- Late payment fees: Credit card companies and lenders may charge fees when payments are not made on time.

- Higher interest rates: A lower credit score may lead to higher interest rates for future loans and credit products.

- Difficulty accessing credit products: Late payments can make it harder to get approved for new loans or credit cards.

Application of Information:

Understanding how late payments affect your credit score is essential for managing finances effectively. Timely payments help maintain a good credit score, lower interest rates, and access to better loan options. It is crucial to be aware of the consequences of missed payments to avoid financial challenges in the future.

Early Action and Responsible Debt Management

Taking early action to address debt is critical in preventing it from becoming a burden. Early action means recognizing potential debt problems before they escalate, such as reaching out to creditors if you anticipate trouble meeting payments or adjusting your budget when expenses rise unexpectedly.

For example, if you lose your job, taking early action might involve reducing discretionary spending or contacting your lenders to negotiate a lower payment plan. If circumstances change, such as a loss of income or unexpected expenses, individuals should take immediate steps to adjust their repayment plans.

This includes prioritizing bills and credit repayments over discretionary spending. Discretionary spending refers to non-essential expenses, such as entertainment, vacations, or luxury items, which can be postponed or reduced when finances are tight.

By staying proactive and addressing potential debt issues early, individuals can avoid penalties, which are extra fees or charges for late payments, interest charges, and debt recovery processes. Debt recovery processes refer to the steps creditors take to collect unpaid debts, which can include legal action or turning the debt over to a collection agency. These actions can further damage your credit score and financial situation.

Accepting responsibility for debt management is key to resolving issues before they become unmanageable. This means being proactive, keeping track of debt, and making informed decisions to ensure that payments are manageable within your financial plan.

Figure: Prioritizing Debt Payments

Description:

The image outlines six essential steps for prioritizing debt payments effectively. It suggests understanding your debt, assessing interest rates, evaluating minimum payments, choosing between the snowball or avalanche method, considering the debt-to-income ratio, and seeking professional advice. These steps provide a structured approach to managing and paying off debt strategically.

Key Takeaways:

- Understand your debt: Knowing all details about your debts helps in making informed decisions.

- Assess interest rates: Focus on paying off higher interest rate debts first to save money.

- Evaluate minimum payments: Ensure at least the minimum payments are made to avoid penalties.

- Debt payment strategies: Choose between the snowball (paying off small debts first) or avalanche (tackling high-interest debts first) methods.

- Seek professional advice: Consider consulting financial experts for personalized debt management strategies.

Application of Information:

Understanding how to prioritize debt payments can help individuals manage their finances more efficiently. By following these steps, users can reduce overall debt, save on interest, and work toward financial freedom. This process is beneficial for anyone looking to pay off debt in a structured and strategic manner.

Understanding the Cost of Late Payments

Unpaid bills and late credit payments often come with additional costs, such as late fees and increased interest rates. Late fees are penalties charged when payments are made after the due date, and increased interest rates may be applied as a penalty for late payments or higher-risk borrowing. These added costs can accumulate quickly, making it even harder to catch up on missed payments.

For example, if a credit card payment is missed, the lender may charge a late fee of €30, and the interest rate may rise from 18% to 24%, significantly increasing the total amount owed.

In cases where repayment is not possible due to unforeseen circumstances, individuals should inform creditors as soon as possible, potentially securing grace periods or public support measures to help manage the debt. A grace period is a set amount of time after the due date during which payment can be made without penalties, while public support measures may include government programs that help individuals manage or repay their debts during financial hardship.

Communicating with creditors shows responsibility and can sometimes lead to more favorable repayment options, such as lowering the interest rate, extending the repayment period, or waiving certain fees.

Seeking Help and Prioritizing Debt

In situations where debt becomes unmanageable, it’s important to know where to seek help. Debt relief agencies, financial advisors, or credit counselors can provide advice on how to reduce the debt burden and avoid further financial distress. Debt relief agencies specialize in negotiating with creditors to reduce the total debt or restructure payment plans, while credit counselors offer personalized guidance on managing finances and reducing debt.

Certain debts, such as mortgage payments or tax obligations, may need to be prioritized over other debts if payments become difficult to manage. This means ensuring that essential debts, like a mortgage or utility bills, are paid before focusing on lower-priority debts, such as credit card payments or personal loans.

Failing to pay priority debts, such as a mortgage, can lead to severe consequences, including foreclosure, which is the legal process by which a lender takes control of a property when the borrower fails to make payments. This ensures that the most critical financial obligations are addressed first, minimizing the risk of foreclosure or legal consequences.

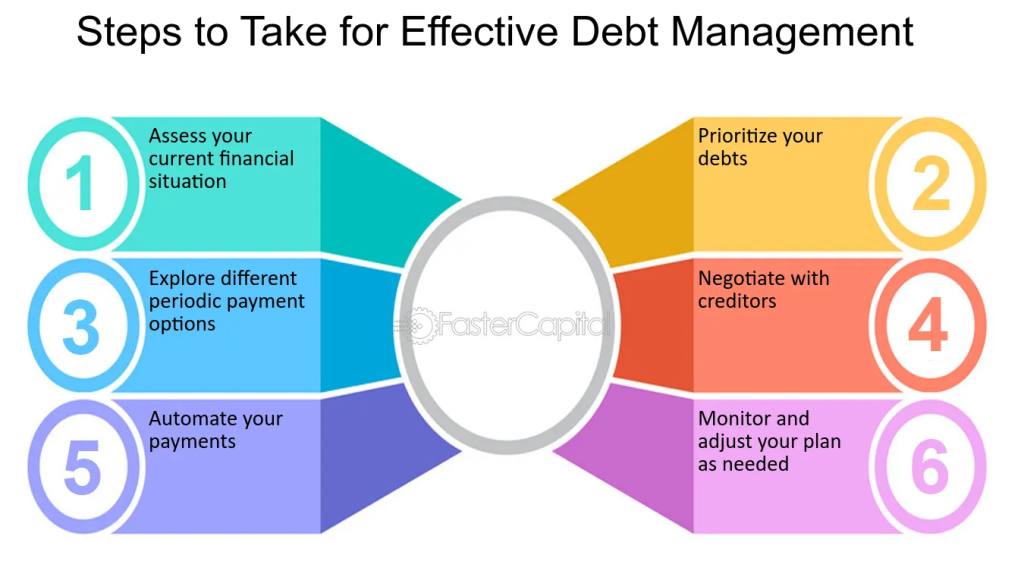

Figure: Steps to Take for Effective Debt Management

Description:

The image illustrates six key steps for managing debt effectively. It begins with assessing your current financial situation, followed by prioritizing your debts. It suggests exploring different periodic payment options and negotiating with creditors. Automating payments helps maintain consistency, and monitoring the plan ensures adjustments can be made when needed.

Key Takeaways:

- Assess your financial situation: Understanding your finances is crucial for effective debt management.

- Prioritize debts: Focus on high-interest or most critical debts first.

- Explore payment options: Consider different payment plans that suit your situation.

- Negotiate with creditors: Communicate with lenders to seek better terms or relief.

- Automate payments: Ensures timely payments and avoids penalties.

- Monitor and adjust: Regularly review your progress and adjust your plan as needed.

Application of Information:

These steps can help individuals create a clear strategy for reducing debt efficiently. By following this process, users can manage their finances better, reduce stress, and work towards financial stability. Understanding these principles is essential for making informed decisions about debt management.

Rights and Responsibilities in Debt Management

Consumers have both rights and responsibilities when managing debt. It’s crucial to understand these rights, as they offer protection and options when dealing with creditors, especially if repayment difficulties arise. Key consumer rights include the right to receive clear and accurate information about the debt, such as interest rates, payment schedules, and any fees associated with borrowing.

Consumers also have the right to negotiate repayment terms, especially in cases where financial hardship occurs.

For example, if a borrower is unable to make payments due to a sudden drop in income, they can request debt restructuring or extended payment terms from the creditor. Debt restructuring can involve lowering the monthly payment, extending the repayment period, or reducing interest rates, all of which can make it easier to manage the debt.

Additionally, consumers are responsible for ensuring they meet their obligations by repaying debts on time, staying informed about their debt situation, and communicating with creditors when necessary. Part of this responsibility includes being proactive about budgeting and managing debt in a way that prevents financial issues from escalating.

Informs Creditors Before Repayment Issues Arise

One of the most important steps in managing debt responsibly is to inform creditors before the due date if/ it becomes clear that a payment cannot be made. Communication with creditors can prevent the situation from worsening. This step allows borrowers to negotiate new terms or request assistance, such as a payment extension or temporary relief measures.

For instance, if an individual anticipates being unable to make their monthly loan payment due to an unexpected medical expense, they should contact their lender as early as possible. Many creditors are willing to work with borrowers who are upfront about their financial struggles, and may offer grace periods, reduced payments, or even temporary suspension of interest accrual, depending on the situation.

This proactive communication can help borrowers avoid penalties such as late fees or higher interest rates, and it demonstrates a willingness to resolve the issue in good faith. Most importantly, addressing the issue early on can prevent more severe consequences, such as damage to credit scores or the initiation of debt recovery processes.

Applying for Over-Indebtedness Procedures

In situations where debts become unmanageable, many countries offer legal mechanisms known as over-indebtedness procedures to help individuals regain control of their finances. These procedures are designed for borrowers who are unable to meet their debt obligations and need assistance in restructuring or reducing their debt load.

An over-indebtedness procedure typically involves consolidating existing debts, creating a manageable repayment plan, or, in extreme cases, reducing the overall debt amount. This process often requires court approval and may involve a trustee or financial counselor who works with creditors on behalf of the borrower. These programs may also include protections, such as halting collection efforts or preventing creditors from seizing assets while the procedure is in progress.

For example, in some countries, the bankruptcy process is a form of over-indebtedness procedure, where a court helps reorganize a debtor’s obligations, sometimes discharging certain debts entirely. Other countries may offer more specific consumer protections, such as debt settlement plans or debt relief programs.

Consumers who qualify for these procedures must provide evidence that they are genuinely unable to pay their debts, and they may be required to commit to a strict financial plan. It’s essential to understand that while these programs can offer relief, they also come with long-term consequences, such as a negative impact on credit scores and restricted access to new credit in the future.

Confidently Managing Debt Issues

To successfully navigate debt challenges, it’s vital for individuals to feel confident in discussing debt management options with relevant parties, whether it’s a creditor, a financial advisor, or a legal professional. This includes asking for debt repayment plans, seeking out over-indebtedness procedures, and ensuring they are informed of their rights and responsibilities as borrowers.

For example, if a borrower is faced with multiple debts, they might speak to a financial counselor to determine which debts should be prioritized and whether any debt consolidation options are available. Debt consolidation involves combining multiple debts into a single loan with a lower interest rate, making it easier to manage monthly payments.

Borrowers should also take responsibility for seeking reputable assistance when necessary. This includes contacting debt relief agencies or credit counseling services to help negotiate with creditors, create repayment plans, and prevent legal action.

Key Lesson Information:

Closing Statement: Effective debt management and emergency savings are essential for financial well-being. This section provides practical strategies to manage debt, maintain credit, and build savings, promoting long-term financial stability.

- Debt-to-Income Ratio: Monitoring the debt-to-income ratio is crucial for assessing financial health. A lower ratio indicates better control over debt, making it easier to access loans and maintain good credit. Users should aim for a DTI ratio of 36% or lower for financial stability.

- Credit Use and Scores: High credit utilization and missed payments can lead to a lower credit score. Maintaining low credit usage (below 30%) and making timely payments can help users improve their credit scores and access better loan options.

- Early Action on Debt: Addressing potential debt issues early—such as negotiating with lenders or adjusting budgets—prevents penalties and escalated costs. Proactive debt management helps users maintain financial control and avoid severe consequences like legal action.

- Building Emergency Funds: An emergency fund covering six months of living expenses can reduce reliance on credit during unexpected events. Users should prioritize savings to achieve this goal, creating a financial safety net.

- Rights and Responsibilities in Debt Management: Consumers have the right to clear information about their debts and can negotiate repayment terms. It’s essential to understand these rights and fulfill responsibilities like timely repayments to maintain good financial standing.