Leverage in Real Estate Investments

Główne cele edukacyjne:

Wstęp: This section sheds light on the power of leveraging in real estate investments. By understanding the nuances of borrowed capital and its potential rewards and risks, investors can craft a strategy that amplifies their returns and minimizes potential pitfalls.

- Understand Leverage: Grasp the concept of using borrowed capital, typically in the form of mortgages, to finance real estate investments, and its implications.

- Recognize Benefits of Leverage: Dive deep into the benefits such as increased buying power, portfolio diversification, tax incentives, amplified returns, and enhanced cash flow.

- Acknowledge Risks: Understand that while leverage can be beneficial, it also comes with inherent risks such as cash flow challenges, interest rate fluctuations, market volatility, decreased flexibility, and potential default.

- Master Risk Management Strategies: Equip oneself with tools and strategies to mitigate potential risks associated with leveraging, including maintaining cash reserves, diversifying, conservative leveraging, and ensuring adequate insurance among others.

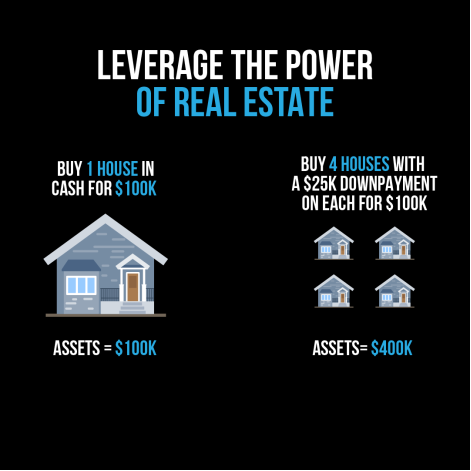

Postać: The infographic emphasizes the power of leveraging in real estate investments. It showcases a comparison: on one side, buying a single house with cash for $100k results in assets worth $100k. On the other side, using the same $100k as a 25% down payment on four houses, each valued at $100k, results in assets totaling $400k. This demonstrates how leveraging can significantly amplify the potential returns and asset base in real estate.

Źródło: Infografika niestandardowa

Leverage refers to the use of borrowed capital to finance an investment, with the expectation that the profits generated will be greater than the cost of borrowing. In real estate, investors use leverage to purchase properties by taking out a mortgage or another form of financing, rather than using their own cash to cover the entire purchase price.

A. Benefits of Using Leverage to Finance Investments:

Postać: The infographic delves into the concept of leverage in real estate. It breaks down a scenario where a property costing $100,000 is purchased with a 20% down payment, resulting in a leverage of 80%. The total revenue generated is $6,000, and after accounting for expenses of $4,000, the cash flow stands at $2,000. The infographic also differentiates between good and bad debt, emphasizing that while bad debt can lead to financial strain, good debt can be a wealth-building tool, especially when someone else is responsible for the payment.

Źródło: Infografika niestandardowa

Increased Buying Power: Leverage enables investors to acquire larger and more valuable properties than they could afford with cash alone. This increased buying power can lead to higher potential rental income and appreciation, ultimately resulting in higher returns on investment.

Dywersyfikacja: By utilizing leverage to finance real estate investments, investors can spread their funds across multiple properties, reducing their overall risk and diversifying their portfolio.

Tax Benefits: Mortgage interest payments are tax-deductible, which lowers an investor’s taxable income. This tax advantage can result in substantial savings, particularly for high-income investors.

Higher Returns: Leverage can amplify returns on investment if a property appreciates in value. For instance, if an investor uses a mortgage to finance 80% of a property’s purchase price, and the property appreciates by 10%, the investor’s return on investment would be 50% higher than if they had purchased the property outright with cash.

Improved Cash Flow: Leveraging a property can enhance cash flow by decreasing the amount of cash required upfront. Instead of allocating all their cash to a single investment, investors can use leverage to distribute payments over time, enabling them to reinvest the cash into other properties or use it for alternative investments.

In conclusion, leveraging real estate investments can offer numerous benefits, such as increased buying power, diversification, tax advantages, higher returns, and improved cash flow. However, investors should carefully weigh the risks associated with leverage, which can include higher interest rates, potential market fluctuations, and the possibility of default.

B. Risks Associated with High Levels of Debt

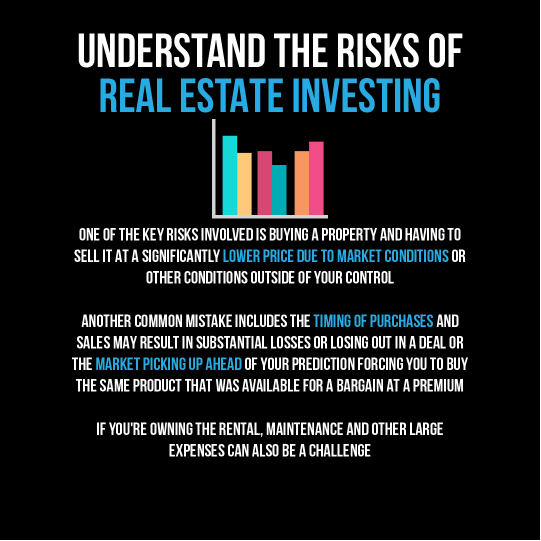

Postać: The infographic sheds light on the potential risks associated with real estate investing. It highlights that one of the primary risks is purchasing a property and later having to sell it at a significantly reduced price due to uncontrollable market conditions. Another risk is the timing of acquisitions and disposals, which can lead to substantial financial losses or missed opportunities. Additionally, for those owning rental properties, unforeseen maintenance and other significant expenses can pose challenges. Aspiring real estate investors should be well-informed about these risks to make strategic decisions.

Źródło: Infografika niestandardowa

While leverage can provide many benefits for real estate investors, it can also come with risks, particularly when high levels of debt are involved. Here are some risks associated with high levels of debt while investing in real estate:

Cash Flow Risk: High levels of debt can increase the risk of negative cash flow, which occurs when the property’s expenses and debt service payments exceed its rental income. Negative cash flow can lead to financial distress and may force the investor to sell the property or default on the loan.

Interest Rate Risk: High levels of debt can also increase the investor’s exposure to interest rate risk. If interest rates rise, the investor’s debt service payments will increase, potentially reducing cash flow and profitability. This risk is particularly significant for investors with adjustable-rate mortgages, which can increase the interest rate over time.

Market Risk: High levels of debt can also increase the investor’s exposure to market risk. Real estate markets can be volatile, with prices and rental rates fluctuating based on local economic conditions. If market conditions deteriorate, the property’s value and rental income could decline, making it more challenging to meet debt service payments.

Decreased Flexibility: High levels of debt can also reduce the investor’s flexibility to respond to changing market conditions or take advantage of investment opportunities. Debt service payments must be made regardless of market conditions, potentially limiting the investor’s ability to reinvest in the property or other investments.

Default Risk: Finally, high levels of debt increase the risk of default, which occurs when the investor cannot make their debt service payments. Default can lead to foreclosure, resulting in the loss of the property and damage to the investor’s credit score.

C. Strategies for Managing Risk in Leveraged Investments

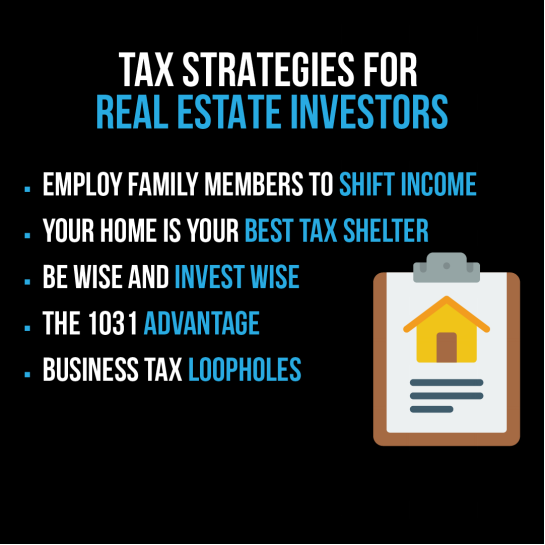

Postać: The infographic offers a concise overview of tax strategies tailored for real estate investors. It suggests various approaches such as employing family members to redistribute income, recognizing one’s home as a prime tax shelter, making informed and wise investment decisions, leveraging the benefits of the 1031 exchange, and exploiting business tax loopholes. These strategies can be instrumental for investors aiming to optimize their tax liabilities and enhance their investment returns.

Źródło: Infografika niestandardowa

Managing risk is critical when investing in leveraged real estate. Here are some strategies that investors can use to manage risk in leveraged investments:

Adequate Cash Reserves: Maintaining adequate cash reserves can help investors manage potential cash flow shortfalls or unexpected expenses. Investors should have cash reserves to cover several months of mortgage payments and other expenses.

Dywersyfikacja: Diversifying investments across multiple properties and markets can reduce risk by spreading it out. Investors should consider investing in different types of properties, such as residential, commercial, or industrial, in different locations to reduce exposure to local market fluctuations.

Conservative Leverage: Investors should avoid over-leveraging and aim for conservative leverage levels to reduce the risk of negative cash flow or default. A conservative leverage level is typically between 50% and 75% of the property’s value.

Long-Term Financing: Investors can reduce interest rate risk by choosing long-term financing options, such as 15- or 30-year mortgages. Long-term financing can provide more stability in the face of interest rate fluctuations.

Professional Property Management: Professional property management can help investors manage their properties more efficiently, reducing the risk of vacancies or missed rental payments.

Regular Property Inspections: Regular property inspections can help investors identify potential issues early and address them before they become more significant problems, reducing the risk of unexpected expenses or property damage.

Adequate Insurance: Adequate insurance coverage can protect investors against unforeseen events, such as natural disasters, accidents, or liability claims. Investors should ensure they have adequate coverage for their properties and review their policies regularly.

In summary, managing risk in leveraged real estate investments requires careful planning and execution. Investors should maintain adequate cash reserves, diversify their investments, aim for conservative leverage levels, choose long-term financing options, consider professional property management, conduct regular property inspections, and ensure adequate insurance coverage. These strategies can help investors manage potential risks and maximize their returns over the long term.

Najważniejsze wnioski:

Oświadczenie końcowe: Leverage, when wielded judiciously, emerges as a potent tool in the real estate investment realm, amplifying buying power and potential returns. This section equips investors with a comprehensive understanding of both the power and perils of leveraging, guiding them to make informed choices and implement risk mitigation strategies effectively.

- Essence of Leverage: Borrowed capital, predominantly in the form of mortgages, allows investors to finance their real estate ventures, hoping the ensuing profits surpass borrowing costs.

- Power of Leverage: It unlocks avenues for increased purchasing capacity, opportunities for diversification, enticing tax breaks, augmented returns, and improved liquidity.

- Risks Inherent: Despite its allure, high leverage levels can introduce risks like constricted cash flow, vulnerability to interest rate hikes, exposure to market downturns, diminished investment agility, and an elevated chance of default.

- Strategies for Mitigating Risks: Prudent risk management is paramount. Ensuring sufficient cash reserves, investment diversification, moderate leveraging, opting for long-term financing, seeking professional property management, routine property checks, and adequate insurance coverage are pivotal strategies to safeguard investments.

- Holistic Approach: While the potential rewards of leverage are tempting, investors must exercise caution, constantly evaluating market conditions, personal financial health, and the specific details of their financing arrangements to ensure sustainable and profitable investment trajectories.