Rozdział 5: Budżetowanie i zarządzanie wydatkami

Cele lekcji:

Lorem ipsum dolor sit amet, consectetur adipiscing elita. Ut elit tellus, luctus nec ullamcorper Mattis, pulvinar dapibus leo.

Introduction to Budgeting and Expense Management

Budgeting and expense management are fundamental aspects of personal finance. This chapter explores how to create a budget that aligns with both short-term and long-term financial goals, including the allocation for an emergency fund, and addresses the dynamics of consumer decisions and their broader impacts. Additionally, we’ll delve into the essence of saving versus investing, revising budgets to accommodate life changes, and the significance of understanding cash flow and financial charges.

5.1 Developing a Budget

There are various budgeting methods to choose from, each with its own advantages and drawbacks. It’s essential to find the method that best suits your needs and preferences. Here are three popular budgeting methods:

Budgeting involves tracking income, allocating funds to various expenses, and setting aside savings to achieve financial goals. A well-crafted budget includes:

- Stałe wydatki: Recurring costs such as rent or mortgage, loan payments, and insurance.

- Variable Expenses: Costs that fluctuate, like groceries, utilities, and entertainment.

- Savings: Funds earmarked for future use, including emergency funds and long-term savings goals.

- Emergency Fund: A crucial part of financial planning designed to cover unexpected expenses, such as medical emergencies or car repairs.

Example Scenario: Jamie earns $3,000 monthly and wants to save for a vacation while covering living expenses. A budget might allocate $1,000 to rent, $300 to groceries, $200 to utilities, $400 to loan payments, $100 to entertainment, and $600 to an emergency fund, illustrating a balanced approach to managing fixed and variable costs and prioritizing savings.

Postać: Types of Budgeting Methods

Opis:

The image illustrates various budgeting methods that cater to different preferences and financial situations. It simplifies the concept of budgeting, making it more approachable, and explains methods such as the 50/30/20 budget, envelope budgeting, zero-based budgeting, and the no-budget budget, each designed to help individuals manage their finances effectively.

Najważniejsze wnioski:

- 50/30/20 Budget: A simple approach where 50% of income is allocated for needs, 30% for wants, and 20% towards savings or debt paydown.

- Envelope Budgeting: A method where cash is allocated into physical envelopes for specific categories. Spending is limited to the cash available in each envelope.

- Zero-Based Budget: Every dollar earned is assigned a specific purpose, ensuring that the budget balances to zero at the end of the month.

- The No-Budget Budget: Suitable for high-income earners with good financial habits. The focus is on earning more than spending and investing the difference.

Zastosowanie informacji:

Different budgeting methods cater to various personality types and financial situations. Understanding and choosing the right approach can empower individuals to manage their finances effectively, ensuring they live within their means and achieve their financial goals. Whether one is looking to curb overspending, allocate funds efficiently, or simply gain better control over their finances, these methods offer structured ways to achieve those objectives.

5.2 Making Informed Consumer Decisions

Consumer decisions are shaped by factors like price, product alternatives, budget constraints, and the potential societal and environmental impacts.

Process for Making Informed Decisions:

- Research: Gather information about the product and alternatives.

- Budget: Consider how the purchase fits into your budget.

- Impact: Evaluate the potential effects on the environment and society.

Example: Opting for an electric vehicle over a gasoline car can be influenced by long-term savings on fuel, environmental benefits, and available tax incentives, despite a higher initial cost.

5.3 Consumer Decision Factors

Product Selected: Electric Vehicle (EV)

Factors Influencing Purchase Decision:

- Price of Product: The upfront cost of an EV can be higher than that of a gasoline-powered vehicle. However, tax incentives and lower operational costs may offset the initial expense.

- Price of Alternatives: Traditional gasoline vehicles are generally cheaper upfront but have higher fuel and maintenance costs over time.

- Consumer’s Budget and Preferences: A consumer’s ability to afford an EV and their preference for environmentally friendly options play significant roles. Some may prioritize eco-friendliness over cost, while others might focus on long-term savings.

- Impact on Environment, Society, and Economy: Purchasing an EV has a lower environmental impact due to reduced emissions. This choice can also support the growth of the renewable energy sector, influencing societal and economic shifts towards sustainability.

Process for Making an Informed Consumer Decision:

- Research: Gather information on various models, including their features, costs, and reviews.

- Comparison: Compare EVs to traditional vehicles in terms of cost, performance, and suitability for needs.

- Budget Assessment: Evaluate personal finances to determine affordability and consider long-term savings.

- Environmental Impact: Consider the ecological benefits of an EV.

- Final Decision: Choose based on a balanced consideration of above factors.

Effects of Purchasing an EV:

- Positive: Reduces carbon footprint, lowers operational costs, promotes renewable energy industries.

- Negative: Higher initial cost might strain the budget; production and disposal of EV batteries have environmental impacts.

5.4 Managing Expenses and Budgeting

Expenses:

- Fixed Expenses: Rent, mortgage, car payments – costs that remain constant each month.

- Variable Expenses: Groceries, utilities, entertainment – costs that can fluctuate.

- Irregular Expenses: Annual insurance premiums, holiday gifts – costs that occur occasionally and can disrupt a regular budget.

My Monthly Budget Example:

- Fixed Expenses: $1,200 rent, $300 car payment, $100 insurance.

- Variable Expenses: $400 groceries, $150 utilities, $100 entertainment.

- Irregular Expenses: Set aside $50 monthly for annual costs like subscriptions or memberships.

- Savings: Aim to save $500 monthly for an emergency fund and future investments.

- Surplus or Deficit: Calculate income minus total expenses (including savings) to determine if you’re living within your means or overspending.

Budgeting Strategies:

- The Envelope System: Allocate cash for variable expenses into categorized envelopes each month. Once the cash in an envelope is gone, no more spending is allowed in that category until the next month.

- Keeping Budget Alive: Regularly review and adjust your budget. Track spending, recognize patterns, and make changes to ensure goals are met. Utilize budgeting apps or spreadsheets for real-time tracking and adjustments.

Managing Expenses

To control spending, it’s essential to differentiate between necessary and discretionary expenses. Strategies to reduce unnecessary spending include identifying impulse purchases, utilizing the envelope system for managing cash expenditures, and regularly reviewing spending habits.

Necessary (Essential) Expenses are costs required for basic living and functioning in daily life. These expenses cover the minimum needs for an individual or family to maintain a healthy and safe lifestyle. Necessary expenses typically include:

- Housing: Rent or mortgage payments.

- Utilities: Water, electricity, gas, and sometimes internet service, depending on the need for remote work or education.

- Food: Groceries needed for home-prepared meals.

- Healthcare: Insurance premiums, medical bills, prescriptions, and any ongoing medical treatments.

- Transportation: Costs associated with commuting to work or school, including car payments, public transportation fares, gas, and essential vehicle maintenance.

- Insurance: Necessary insurance policies, including health, auto, and homeowners or renters insurance.

Example of Necessary Expenses: Sarah budgets $1,000 monthly for rent, $200 for utilities, $300 for groceries, $250 for her car payment and gas, and $150 for health insurance. These costs are non-negotiable for her to live safely and comfortably.

Discretionary (Non-Essential) Expenses are costs associated with things people want but do not need to live a basic lifestyle. These expenses often enhance quality of life but can be reduced or eliminated if needed. Discretionary expenses include:

- Entertainment: Money spent on movies, concerts, streaming services, or other recreational activities.

- Dining Out: Expenses for eating at restaurants beyond what is necessary for nutrition.

- Hobbies: Costs related to hobbies or leisure activities, such as crafting materials, sports equipment, or book purchases.

- Travel: Costs for vacations and non-essential travel.

- Luxuries: High-end electronics, designer clothing, and other luxury items that go beyond basic needs.

Example of Discretionary Expenses: Alex enjoys dining out, spending an average of $300 a month at restaurants, subscribes to several streaming services costing $50 monthly, and allocates $200 for hobbies and entertainment. While these enhance his life, they can be adjusted based on his financial goals or situation.

Managing Necessary and Discretionary Expenses: Effective financial planning involves first ensuring that necessary expenses are covered within one’s budget. Any remaining income can then be allocated towards discretionary expenses, savings, and investments. Prioritizing savings and debt repayment over discretionary spending is crucial for long-term financial health. Individuals may need to periodically review their spending habits, especially discretionary expenses, to adjust their budget in response to changes in income or financial goals.

By distinguishing between necessary and discretionary expenses and understanding their impact on overall financial planning, individuals can make informed decisions that align with their priorities and financial objectives, ensuring stability and progress towards their goals.

5.5 Creating and Revising Budgets

Budgets need to be flexible to reflect changes in income, life circumstances, and financial goals.

- Short-term Savings: Should cover emergencies and unexpected expenses.

- Long-term Savings: Aimed at future aspirations, such as home ownership or retirement.

Adapting Budgets: Life events, such as a job change or unexpected bills, necessitate budget adjustments to stay on track financially.

Example: If Alex experiences a job loss, the budget must be revised to reduce variable expenses and prioritize essential costs and minimal savings until income stabilizes.

- Saving is setting aside money for future use, typically in low-risk, easily accessible Saving vs. Investing accounts.

- Investing involves purchasing assets with the potential for higher returns over time but comes with greater risk.

Understanding the distinction helps in aligning financial strategies with goals, balancing the security of savings with the growth potential of investments.

5.6 Designing a Personal Budget

A personal budget should reflect an individual’s unique financial situation, goals, and priorities. It involves:

- Setting Goals: Define clear, achievable objectives.

- Allocating Income: Distribute income across expenses, savings, and investments.

- Monitoring and Revising: Regularly review and adjust the budget as circumstances evolve.

5.7 Impact of External Factors:

Taxes, inflation, and personal changes (e.g., marriage, children) significantly influence budgetary needs and financial planning.

Preparing a Realistic Personal or Family Budget:

- Identify Income Sources: Calculate total monthly income from all sources.

- List and Categorize Expenses: Separate expenses into fixed, variable, and irregular categories.

- Allocate Funds for Savings: Prioritize setting aside a portion of income for savings and emergency funds.

- Adjust for Surplus or Deficit: If expenses exceed income, look for areas to cut back. If there’s a surplus, allocate extra funds to savings or debt repayment.

- Monitor and Review: Regularly check your budget against actual spending and adjust as needed to stay on track.

5.8 Interest and Fees in Money Management

Understanding interest rates and fees associated with spending, borrowing, and saving is crucial. Interest can accumulate on savings, enhancing wealth, or on debts, increasing the cost of borrowed funds.

Calculating Interest:

For instance, a savings account with a 1.5% annual interest rate would yield $150 on a $10,000 balance over one year, whereas a credit card with a 20% interest rate could cost $200 in interest on a $1,000 balance unpaid over the same period.

By mastering the principles of budgeting and expense management, individuals can navigate their financial journey with confidence, making informed decisions that foster stability, growth, and fulfillment.

Changes in Taxes

Impact: An increase in taxes, whether it’s income tax, property tax, or sales tax, directly reduces the amount of disposable income an individual or household has. For example, if income taxes rise, the net income after taxes decreases, leaving less money for spending and saving. Conversely, tax decreases can increase disposable income, providing more room in the budget for other expenses or savings.

Example: Suppose Alex’s effective income tax rate increases due to changes in tax legislation. As a result, his monthly take-home pay decreases. To adjust, Alex might need to reduce his discretionary spending or reevaluate his savings contributions to maintain his financial stability.

Inflation

Impact: Inflation erodes purchasing power over time, meaning the same amount of money buys fewer goods and services. As prices for essentials like food, housing, and healthcare rise, individuals may find their existing budget no longer covers their needs. This necessitates either finding ways to increase income or adjusting spending habits to accommodate the higher cost of living.

Example: If the annual inflation rate is 3%, and Emily’s salary doesn’t increase, her living expenses will rise, effectively reducing her disposable income. Emily might need to cut back on non-essential spending, seek additional sources of income, or prioritize her spending differently to manage the increased cost of living.

Personal CircumstancesImpact: Life events such as marriage, divorce, the birth of a child, job loss, or receiving an inheritance can significantly affect one’s financial situation and budget. Positive changes may result in increased financial stability, while challenging events might require tightening the budget or reallocating funds to meet new demands.

Example 1: After the birth of their child, Jordan and Taylor realize their current apartment is too small. Moving to a larger place increases their rent, necessitating adjustments in their budget to accommodate this essential expense.

Example 2: Sarah receives a promotion with a substantial pay increase. She decides to increase her retirement savings contributions and start a college fund for her children, reflecting her improved financial situation.

Adjusting to ChangesTo adapt to changes in taxes, inflation, and personal circumstances, individuals might need to:

- Review and Adjust Budgets Regularly: Keeping budgets flexible to accommodate changes in income and expenses.

- Prioritize Spending: Focusing on needs over wants, especially during times of financial constraint.

- Seek Opportunities to Increase Income: Exploring side gigs, asking for raises, or acquiring new skills for better-paying jobs.

- Build an Emergency Fund: Providing a financial buffer to help manage unexpected changes or challenges.

Effective budgeting and expense management are key to achieving financial stability and meeting long-term goals. Understanding and applying these principles allows individuals to make informed consumer decisions and maintain a healthy financial lifestyle.

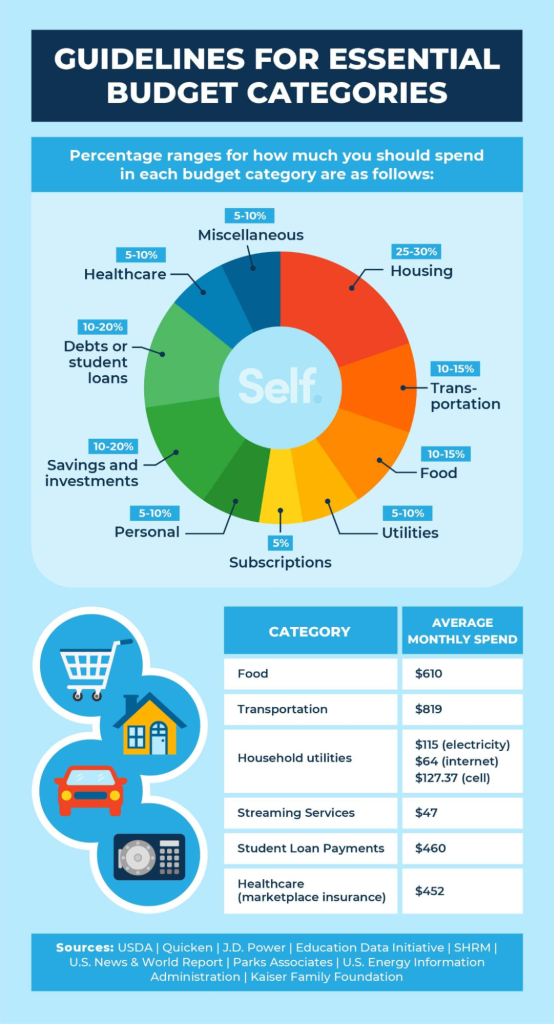

Postać: 10 Essential Budget Categories

Opis:

The image presents a list of ten essential budget categories that individuals should consider when planning their finances. These categories cover a range of expenses and savings areas, helping individuals allocate their funds effectively.

Najważniejsze wnioski:

- Mortgage or Rent: Allocate funds for housing expenses.

- Savings and Investments: Set aside money for future financial goals and wealth accumulation.

- Debt or Student Loans: Plan for repayment of debts and educational loans.

- Transportation: Budget for commuting, vehicle maintenance, and other transportation-related costs.

- Miscellaneous Expenses: Allocate funds for unforeseen or varied expenses.

- Subskrypcje: Budget for monthly or annual subscription services.

Zastosowanie informacji:

Having a clear categorization of budget areas is crucial for effective financial planning. By breaking down expenses and savings into specific categories, individuals can gain a better understanding of their financial habits, identify areas for improvement, and make informed decisions. This categorization serves as a foundational guide for anyone looking to establish a comprehensive budget, ensuring that all essential areas are covered and financial goals are met.

Figure: Essential Budget Categories for Financial Planning

Opis:

The image from Self.inc outlines ten essential budget categories that are critical for effective financial planning. These categories help individuals understand their spending patterns and manage their finances by allocating funds appropriately to areas such as housing, food, transportation, and healthcare.

Najważniejsze wnioski:

- Housing should generally consume about 30% of income, including associated costs like insurance and taxes.

- Food expenses can range from 10% to 16% of income, with variations based on household size and dietary choices.

- Transportation costs, which include vehicle payments and public transit, should ideally not exceed 15% of monthly income.

- Utility bills can be kept within 5% to 10% of income through energy-saving measures and service plan comparisons.

- Healthcare costs are recommended to be budgeted between 5% to 10%, considering both regular and potential unexpected medical expenses.

Zastosowanie informacji:

By categorizing expenses, individuals can create a structured budget that aligns with their income and financial goals. This approach allows for a clear understanding of where money is being spent and where adjustments can be made to save more or pay off debt. It’s particularly useful for those looking to gain control over their finances and work towards financial stability and independence.

5.9 Factors Influencing Consumer Decisions

Price and Product Comparison

When making a purchase, price is often one of the primary deciding factors. Consumers frequently compare prices for similar products before settling on a purchase. For example, when buying a new smartphone, a consumer may compare prices across various retailers or online platforms to ensure they’re getting the best deal.

- Pros:

- Helps the consumer save money by identifying the most affordable option.

- Encourages consumers to seek the best value for their purchase.

- Helps the consumer save money by identifying the most affordable option.

- Wady:

- Price comparisons can be time-consuming, especially when there are many options available.

- Focusing too heavily on price may result in overlooking product quality and features.

- Price comparisons can be time-consuming, especially when there are many options available.

Brand and Reputation

Some consumers may have a preference for certain brands due to reputation, previous experiences, or trust in the brand’s quality. For example, someone may opt for an Apple iPhone over other phones due to its known brand reliability, even if it costs more than other smartphones.

- Pros:

- Offers peace of mind knowing that the product is from a trusted brand.

- Ensures a certain level of quality and performance based on brand reputation.

- Offers peace of mind knowing that the product is from a trusted brand.

- Wady:

- Higher brand premiums may result in paying more than necessary for a product that may not offer significant added value.

- Brand loyalty may limit exploration of more affordable alternatives.

- Higher brand premiums may result in paying more than necessary for a product that may not offer significant added value.

Functionality and Features

The functionality and features of a product greatly influence consumer decisions. For example, when purchasing a laptop, a consumer may prioritize factors like screen size, battery life, or processing speed, depending on their needs (e.g., work or entertainment).

- Pros:

- Allows consumers to select products tailored to their needs.

- Increases satisfaction with the purchase when the product meets specific requirements.

- Allows consumers to select products tailored to their needs.

- Wady:

- A focus on functionality may result in higher costs if consumers opt for more feature-packed versions.

- Sometimes, additional features may be unnecessary for the consumer’s intended use, leading to overpaying.

- A focus on functionality may result in higher costs if consumers opt for more feature-packed versions.

Process for Making Informed Consumer Decisions

Step 1: Identifying Needs vs. Wants

The first step in making an informed purchase is distinguishing between needs and wants. A need could be a basic necessity, such as a phone that can make calls and send messages, while a chcieć could be a high-end model with additional features that aren’t necessary.

- Pros:

- Helps prevent unnecessary purchases and ensures that essential needs are met.

- Promotes smarter financial decisions by focusing on what’s truly needed.

- Helps prevent unnecessary purchases and ensures that essential needs are met.

- Wady:

- The line between needs and wants can sometimes be subjective, leading to confusion or indecision.

- Restricting spending on wants may reduce immediate satisfaction.

- The line between needs and wants can sometimes be subjective, leading to confusion or indecision.

Step 2: Researching Options

Once needs are determined, consumers should research their options. This involves reading customer reviews, checking product comparisons, and looking into expert opinions.

- Pros:

- Ensures that consumers make an informed and educated decision.

- Provides insight into potential product flaws or advantages that may not be obvious at first glance.

- Ensures that consumers make an informed and educated decision.

- Wady:

- Researching multiple products can be time-consuming and may cause decision fatigue.

- The abundance of information available can sometimes overwhelm the consumer, making it harder to make a decision.

- Researching multiple products can be time-consuming and may cause decision fatigue.

Step 3: Evaluating Price vs. Value

Before making a final decision, consumers should assess whether the price aligns with the value they are getting. This means considering factors like product quality, longevity, and after-sales service in addition to the initial price tag.

- Pros:

- Helps consumers balance cost with the quality and benefits of the product, ensuring better value for money.

- Encourages more thoughtful and deliberate purchasing, reducing impulse buying.

- Helps consumers balance cost with the quality and benefits of the product, ensuring better value for money.

- Wady:

- Some products might appear overpriced based on initial cost but offer long-term value through durability or lower maintenance.

- Finding the right balance between price and value can be subjective and vary from person to person.

- Some products might appear overpriced based on initial cost but offer long-term value through durability or lower maintenance.

Positive and Negative Effects of Consumer Decisions

Example: Purchasing an Electric Vehicle (EV)

- Positive Environmental Impact:

- EVs contribute to lower carbon emissions compared to traditional gasoline-powered cars, helping reduce pollution and combating climate change.

- EVs contribute to lower carbon emissions compared to traditional gasoline-powered cars, helping reduce pollution and combating climate change.

- Positive Societal Impact:

- Purchasing an EV supports the growth of the green energy sector, promoting sustainable transportation options and supporting eco-friendly innovations.

- Purchasing an EV supports the growth of the green energy sector, promoting sustainable transportation options and supporting eco-friendly innovations.

- Negative Environmental Impact:

- The production of EV batteries requires mining materials like lithium, which can lead to environmental degradation and significant resource extraction.

- The production of EV batteries requires mining materials like lithium, which can lead to environmental degradation and significant resource extraction.

- Negative Economic Impact:

- EVs often come with a higher upfront cost compared to traditional vehicles, which may be a financial burden for some consumers, especially those on tighter budgets.

- EVs often come with a higher upfront cost compared to traditional vehicles, which may be a financial burden for some consumers, especially those on tighter budgets.

- Pros:

- Encourages sustainable choices and supports global initiatives for environmental protection.

- Helps consumers align their financial decisions with their personal values, like environmental consciousness.

- Encourages sustainable choices and supports global initiatives for environmental protection.

- Wady:

- The upfront cost may not be accessible for all consumers, which can limit adoption.

- The environmental impact of battery production is a downside that many consumers may overlook.

- The upfront cost may not be accessible for all consumers, which can limit adoption.

Financial Responsibility and Budget Planning

Preparing for Life Events and Changing Budgets

Unexpected life changes, such as job loss, having a child, or a medical emergency, can significantly impact an individual’s budget. For example, after a job loss, a consumer may need to adjust their budget by cutting back on discretionary spending and prioritizing essential expenses.

- Pros:

- Having a flexible budget ensures financial stability during uncertain times.

- Helps individuals stay on track with financial goals even when life events cause disruptions.

- Having a flexible budget ensures financial stability during uncertain times.

- Wady:

- Regularly revising budgets due to unexpected events can be time-consuming and overwhelming.

- It may require sacrifices in other areas, such as entertainment or personal spending.

- Regularly revising budgets due to unexpected events can be time-consuming and overwhelming.

Factors Affecting Financial Goals

External factors such as location, culture, I peer influences can significantly impact one’s financial goals. For example, someone living in a high-cost area may need a larger budget for housing and transportation compared to someone living in a lower-cost area.

- Pros:

- Understanding these external influences helps individuals recognize patterns in their financial behavior and spending.

- Encourages self-awareness, enabling consumers to make more informed financial decisions.

- Understanding these external influences helps individuals recognize patterns in their financial behavior and spending.

- Wady:

- Overcoming the influence of peer pressure or cultural expectations can be challenging.

- These external factors may lead to unsustainable financial choices if not carefully managed.

- Overcoming the influence of peer pressure or cultural expectations can be challenging.

Techniques to Decrease Expenses

Comparison Shopping

Comparison shopping helps consumers find the best prices for products by comparing different stores and online retailers. For example, when buying a laptop, a consumer might use comparison websites to see if the item is cheaper elsewhere.

- Pros:

- Can lead to substantial savings by identifying the best prices.

- Provides a broader view of available options, ensuring that the consumer gets the best deal.

- Can lead to substantial savings by identifying the best prices.

- Wady:

- Time-consuming, especially when comparing many different options.

- The lowest price may not always correspond with the best quality or service.

- Time-consuming, especially when comparing many different options.

Negotiating Prices

Negotiating the price of large purchases (e.g., cars, furniture) or even monthly bills (e.g., cable, insurance) can lead to significant savings. For instance, a consumer might negotiate a lower rate on their cable bill by threatening to cancel the service.

- Pros:

- Provides an opportunity to lower the overall cost of big-ticket items or services.

- Can build confidence in consumers when dealing with sales representatives.

- Provides an opportunity to lower the overall cost of big-ticket items or services.

- Wady:

- Not all merchants are open to negotiation, and it may feel uncomfortable for some consumers.

- It can be difficult to know when negotiation is appropriate, and sometimes it may not be effective.

- Not all merchants are open to negotiation, and it may feel uncomfortable for some consumers.

Using Technology for Financial Management

Financial Management Tools

There are various digital tools and apps that help track and manage spending, such as Mint, YNAB, I mobile banking apps. These tools can automatically categorize expenses, track income, and help users stick to their budget.

- Pros:

- Real-time tracking and budgeting make it easier to stay on top of finances.

- Automates savings and bill payments, making it easier for consumers to manage their money.

- Real-time tracking and budgeting make it easier to stay on top of finances.

- Wady:

- Some apps or tools may require subscriptions or fees, which may eat into savings.

- Technical issues or security concerns with apps could compromise financial data

Conclusion: Mastering Budgeting and Expense Management

Budgeting and managing expenses are the foundations of personal financial success. Throughout this chapter, we explored how creating and maintaining a thoughtful budget empowers individuals to take control of their money, plan for both expected and unexpected life events, and align their spending habits with their long-term goals. Whether choosing a structured method like the 50/30/20 rule, tracking expenses through modern apps, or adapting to life’s inevitable changes, the tools and strategies discussed offer a path toward financial stability and growth.

Effective budgeting is not just about restriction; it’s about making intentional choices that reflect your values and aspirations. Understanding the difference between needs and wants, making informed consumer decisions, adjusting to economic shifts like inflation or tax changes, and regularly revisiting your budget ensures that your financial plan remains a living, flexible guide.

By practicing disciplined budgeting, making mindful purchasing decisions, and proactively managing necessary and discretionary expenses, individuals can not only meet their financial obligations but also build security, achieve personal goals, and enjoy greater peace of mind. Ultimately, mastering budgeting and expense management is not just a financial skill—it’s a key to building a life of opportunity, resilience, and freedom.

Najważniejsze informacje dotyczące lekcji:

Lorem ipsum dolor sit amet, consectetur adipiscing elita. Ut elit tellus, luctus nec ullamcorper Mattis, pulvinar dapibus leo.