Local: Taxas e despesas de investimento

Objetivos de aprendizagem da lição:

- Understand Investment Fees and Expenses: Learn about the transaction fees, active vs. passive ETF management fees, and the impact of these costs on overall investment returns, particularly in the context of the European market.

- Explore Wealth Tax in European Countries: Understand the concept of wealth tax and how it applies to financial assets in countries like França, Espanha, e Switzerland, and how it can impact your investment strategy.

- Learn About Stamp Duties and Financial Transaction Taxes: Understand the taxes levied on buying and selling financial instruments, such as the stamp duty in the UK, financial transaction taxes em França e Itália, and how they affect your investment decisions.

- Understand Capital Gains Tax Across Europe: Learn about capital gains tax in different European countries, how it can affect your investment returns, and the importance of considering these taxes when planning your investments.

Introdução

When building an investment portfolio, understanding the differences between ações, ETF ativos, e ETFs passivos is essential. Each investment type has its own benefits and risks, and choosing the right one depends on your investment strategy, risk tolerance, and financial goals. This chapter explores key aspects of stocks, active ETFs, and passive ETFs, comparing them in terms of fees, strategies, and analysis methods.

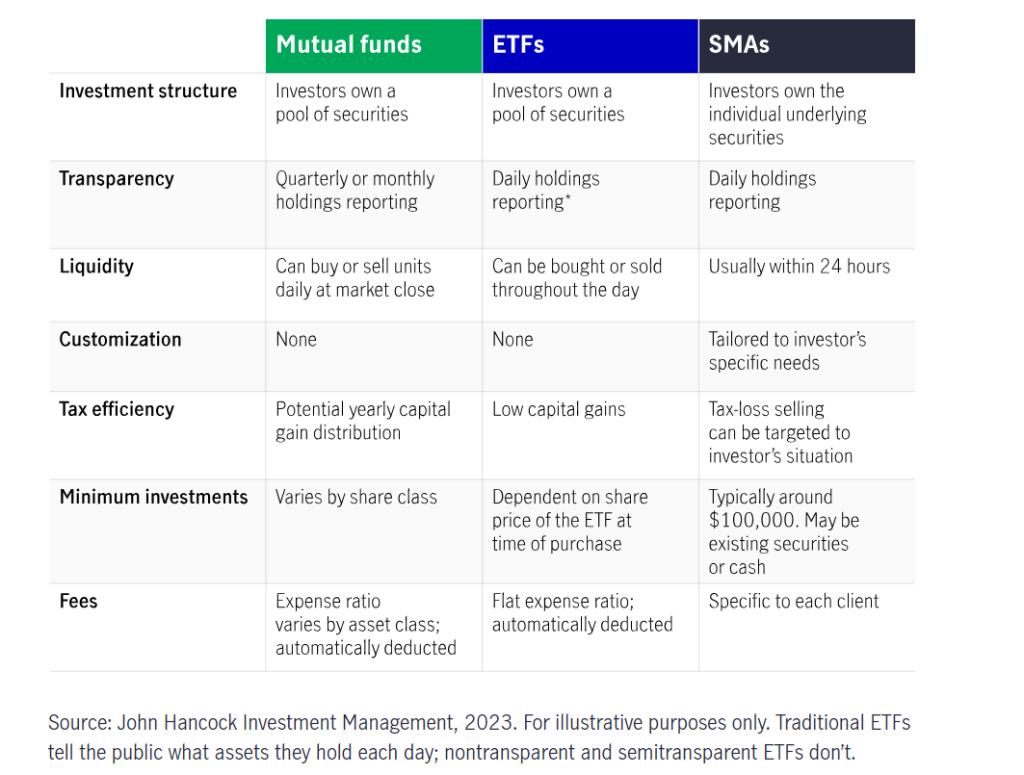

Figura: Mutual Funds vs. ETFs vs. SMAs

Descrição:

The table compares three types of investment options: Fundos mútuos, ETFs (Exchange-Traded Funds), e SMAs (Separately Managed Accounts). It highlights differences in areas like investment structure, transparency, liquidity, customization, tax efficiency, minimum investments, e tarifas. Mutual funds and ETFs allow investors to own a pool of securities, while SMAs provide ownership of individual underlying securities. ETFs offer more frequent holdings reporting and liquidity than mutual funds, whereas SMAs offer personalized customization and tax strategies.

Principais vantagens:

- Investment structure: Mutual funds and ETFs represent pooled securities, while SMAs allow ownership of individual securities.

- Liquidez: ETFs can be traded throughout the day, providing higher liquidity than mutual funds, which are bought or sold at market close.

- Customization: SMAs are more customizable to individual investor needs, unlike mutual funds and ETFs.

- Tax efficiency: SMAs can provide targeted tax strategies, while ETFs generally have lower capital gains compared to mutual funds.

Aplicação de informações:

This comparison helps investors choose an investment vehicle based on liquidity needs, customization preferences, e tax strategy considerations. ETFs might suit those looking for flexible trading, enquanto SMAs may appeal to those seeking personalized investment strategies e tax management. Understanding these differences can aid in creating a more aligned investment strategy.

45t

19.1: Investment Fees & Expenses

When investing in ações, ETF ativos, ou ETFs passivos in the European Union, understanding the various fees and expenses associated with these investments is crucial. Beyond standard trading costs, European investors must also consider region-specific taxes and regulatory fees that can impact overall returns. Notably, certain European countries impose taxes such as wealth tax, which may apply depending on an investor’s assets and country of residence.

Transaction Fees and Management Expenses

- Transaction Fees: Just like in other regions, European investors pay transaction fees when buying or selling individual stocks or ETFs. These fees can vary depending on the brokerage used, the stock exchange, and the type of investment. For instance, trading on the London Stock Exchange (LSE) ou Euronext may involve different fee structures than other European exchanges.

- Active ETF Management Fees: Active ETFs, being professionally managed, typically charge higher expense ratios compared to passive ETFs. In Europe, these fees can range from 0.5% to 2% annually, depending on the fund’s management and performance.

- Passive ETF Management Fees: In contrast, passive ETFs, which track a market index such as the Euro Stoxx 50 ou FTSE 100, generally have much lower fees, often ranging from 0.05% to 0.5%. These lower costs make passive ETFs a cost-efficient option for long-term investors in Europe seeking broad market exposure.

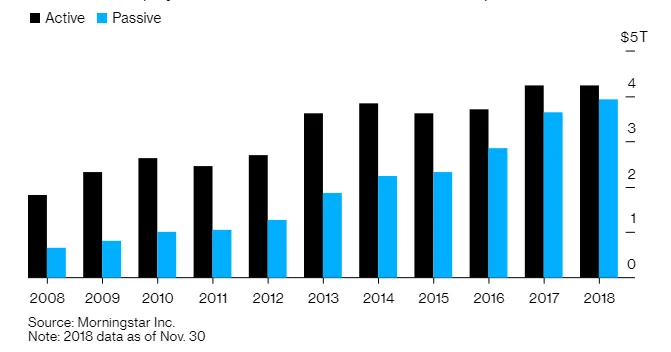

Figura: Active vs. Passive Investment Growth (2008–2018)

Descrição:

The bar chart illustrates the growth of active e passive investments from 2008 to 2018. The chart shows two bars for each year, with the black bar representing active investments and the blue bar indicating passive investments. It highlights how passive investments have steadily increased over the decade, gradually closing the gap with active investments, especially from 2013 onward. In 2018, passive investments nearly matched the total amount of active investments, indicating a strong shift towards passive investment strategies.

Principais vantagens:

- Passive investments have seen consistent growth over the decade, reflecting increased investor interest.

- Active investments still have a higher total value but have experienced slower growth compared to passive investments.

- By 2018, the difference between active and passive investment totals was minimal, suggesting a potential equalization in popularity.

Aplicação de informações:

This chart helps investors understand the growing trend towards passive investing, which could be beneficial for long-term investors seeking low-cost diversification. The data indicates a shift in investor behavior favoring passive strategies, emphasizing the importance of understanding both active and passive approaches to develop a well-rounded portfolio.

19.2 Wealth Tax in European Countries

One unique aspect of investing in Europe is the potential for wealth tax, which applies in several countries. This tax is levied on an individual’s net wealth, including stocks, real estate, and other financial assets. The rates and thresholds vary by country, so it’s important for investors to understand how wealth tax might impact their portfolios.

- França: In France, a wealth tax called Impôt sur la Fortune Immobilière (IFI) applies to real estate assets worth over €1.3 million. Though it doesn’t directly apply to financial assets like stocks or ETFs, it can affect investors with significant real estate holdings.

- Espanha: Spain imposes a wealth tax on individuals whose assets exceed €700,000, with rates ranging from 0.2% to 2.5%, depending on the value of the assets. This tax includes financial assets, such as stocks, bonds, and mutual funds.

- Switzerland: Switzerland applies a wealth tax at the cantonal level, with varying rates depending on the region. Wealth taxes typically range from 0.1% to 1% and include financial assets like stocks and ETFs.

- Norway: In Norway, wealth tax applies to assets over NOK 1.5 million (around €145,000), with a rate of 0.85%. This tax includes both real estate and financial assets like stocks and ETFs.

- França: In France, a wealth tax called Impôt sur la Fortune Immobilière (IFI) applies to real estate assets worth over €1.3 million. Though it doesn’t directly apply to financial assets like stocks or ETFs, it can affect investors with significant real estate holdings.

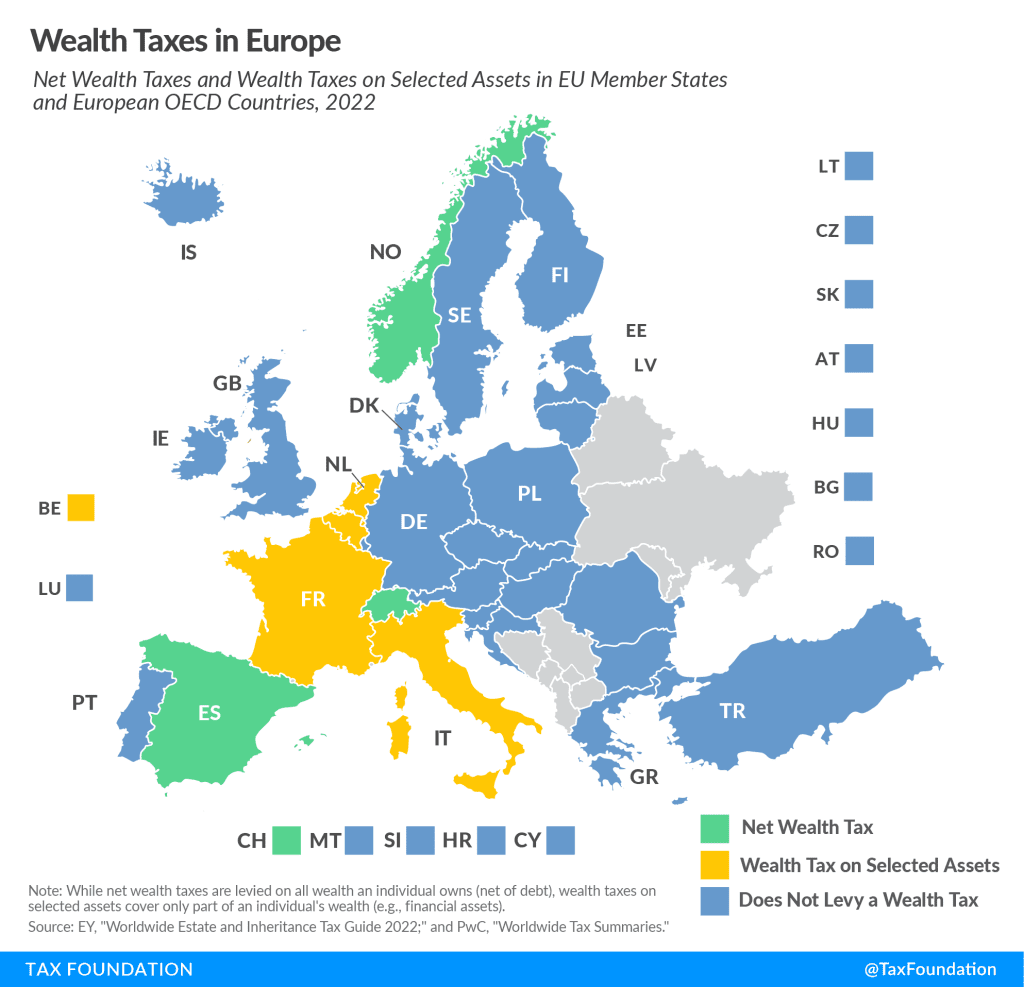

Figura: Wealth Taxes in Europe (2022)

Descrição:

The map illustrates the presence of wealth taxes across European countries in 2022, differentiating between Net Wealth Tax (countries marked in green), Wealth Tax on Selected Assets (countries marked in yellow), and countries without a wealth tax (marked in blue). The net wealth tax applies to an individual’s total net wealth, while the wealth tax on selected assets applies only to certain types of assets, such as financial assets. The map helps provide a geographic perspective on wealth tax policies across EU member states and other European OECD countries.

Principais vantagens:

- Net Wealth Tax is implemented in countries like Espanha, Norway, e Switzerland.

- Wealth Tax on Selected Assets exists in França, Belgium, e Luxembourg, targeting specific asset classes.

- No Wealth Tax is present in most other European countries, reflecting a broader trend towards wealth tax elimination or non-adoption.

Aplicação de informações:

This information is useful for investors and policymakers to understand tax implications in different European countries. It can help investors decide where to allocate assets or establish residency based on tax efficiency. For financial planning, knowing the presence of a wealth tax can impact strategies related to asset diversification, investment location, and overall wealth management.

19.3 Stamp Duties and Financial Transaction Taxes

Several European countries impose stamp duties ou financial transaction taxes (FTT) on the buying and selling of financial instruments, including stocks and ETFs. These taxes increase the overall cost of investing and should be considered when making investment decisions.

- United Kingdom: The UK stamp duty is 0.5% on the purchase of UK company shares, including stocks and ETFs, when buying directly through a broker.

- Itália: Italy levies a financial transaction tax of 0.1% on the purchase of shares issued by Italian companies and ETFs listed on Italian exchanges.

- França: France imposes a financial transaction tax of 0.3% on purchases of French companies with a market capitalization above €1 billion. This tax applies to both stocks and ETFs.

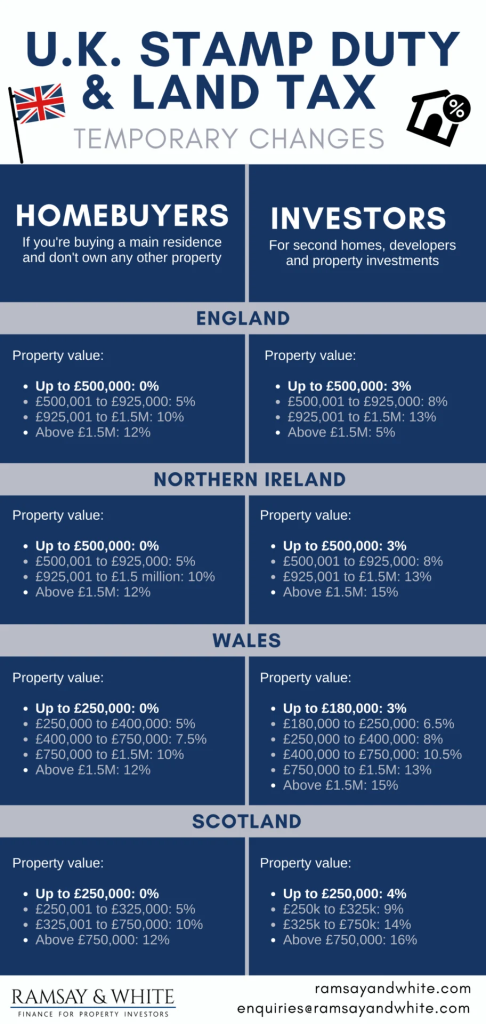

Figura: U.K. Stamp Duty & Land Tax: Temporary Changes

Descrição:

This infographic provides an overview of temporary changes in stamp duty and land tax rates across the United Kingdom for homebuyers and investors. It shows different property value bands and the applicable tax rates for England, Northern Ireland, Wales, e Scotland. For homebuyers, the tax rates start at 0% for lower-value properties and increase progressively with the property value. For investidores, higher rates apply, beginning at 3% for properties up to £500,000. Each region has different thresholds and percentages.

Principais vantagens:

- Stamp duty rates vary by property value and region in the UK.

- Homebuyers pay lower rates compared to investidores, reflecting government policies to support homeownership.

- England and Northern Ireland share similar tax rates, while Wales e Scotland have distinct thresholds and rates.

- The tax rates increase progressively as the property value rises, with higher rates for investors.

Aplicação de informações:

Understanding stamp duty rates is crucial for real estate investors e homebuyers to plan accurately for property purchases. The differences in rates across regions and property types highlight the need to consider location-specific tax implications. Investors can use this information to calculate transaction costs and assess the feasibility of investments. For homebuyers, knowing the progressive tax structure can help in budgeting and financial planning.

19.4 Capital Gains Tax

Capital gains tax applies to profits made from selling stocks or ETFs. While the rates vary across European countries, capital gains taxes can significantly impact investment returns.

- Alemanha: Capital gains on the sale of stocks and ETFs are taxed at a flat rate of 25%, plus a solidarity surcharge and church tax, resulting in an effective tax rate of around 26.4% for most investors.

- Netherlands: The Netherlands does not tax capital gains directly for private investors. However, a wealth tax on assets, including stocks and ETFs, applies, with an effective rate that varies based on total assets.

- Sweden: In Sweden, capital gains on stocks and ETFs are taxed at a rate of 30%, which is higher than in many other European countries, making it essential for investors to factor this into their investment planning.

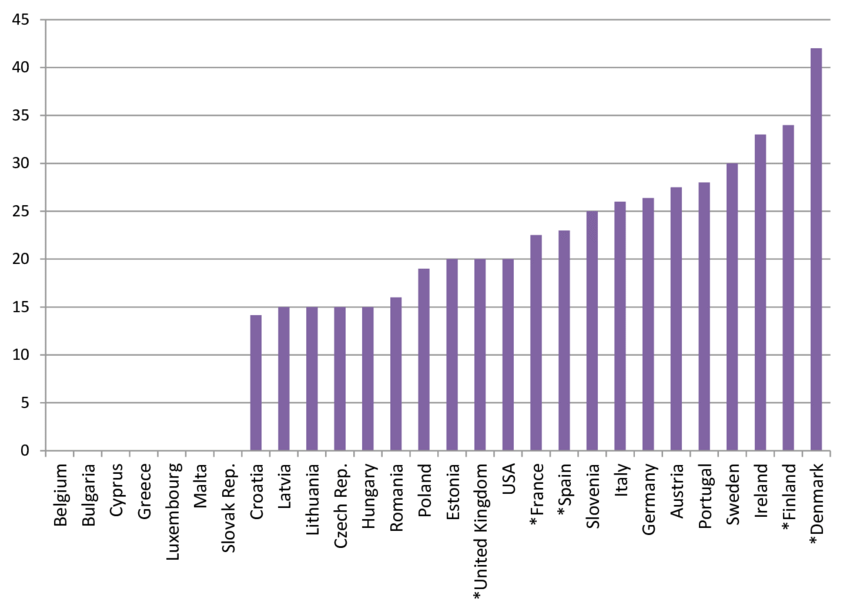

Figura: Statutory Tax Rates on Capital Gains in Europe and the U.S.

Descrição:

This bar graph illustrates the statutory tax rates on capital gains across various countries in Europe e a United States. The x-axis displays the list of countries, while the y-axis indicates the tax rates as a percentage, ranging from 0% to 45%. The chart reveals that Denmark has the highest capital gains tax rate, exceeding 40%, while countries like Belgium e Bulgaria have the lowest rates, hovering around 0%. The graph provides a comparison of capital gains taxation across these regions, with noticeable differences in rates among countries.

Principais vantagens:

- Denmark has the highest capital gains tax rate among the countries listed.

- Belgium, Bulgaria, e Cyprus have some of the lowest capital gains tax rates, close to 0%.

- Countries like Ireland, Sweden, e Finland also have high rates, ranging between 30% and 35%.

- O United States is positioned near the middle of the graph, reflecting moderate capital gains taxation compared to European counterparts.

Aplicação de informações:

This data is useful for investidores analyzing the impact of capital gains taxes on their investment returns in different countries. Understanding tax variations can help in making informed decisions about where to invest and estimating potential tax liabilities. Investors can use this information to optimize their estratégias de investimento by considering tax-efficient jurisdictions, ultimately enhancing their net returns.

Conclusão

When investing in ações, ETF ativos, ou ETFs passivos in the European Union, it is important to account for a range of fees and taxes specific to the region. In addition to transaction fees and management expenses, European investors must consider potential wealth taxes, stamp duties, e capital gains taxes that can impact their returns. Understanding these region-specific costs allows investors to better manage their portfolios and make informed decisions that align with their financial goals.

Principais informações da lição:

- Transaction fees vary across brokerage firms and stock exchanges in Europe. For instance, buying stocks on the London Stock Exchange ou Euronext may involve different fee structures, which can impact your overall cost of investing.

- ETFs ativos tend to have higher management fees (0.5% to 2%) due to professional management, while ETFs passivos generally have lower fees (0.05% to 0.5%) as they track market indices like the Euro Stoxx 50, making passive ETFs a more cost-efficient option for long-term investors.

- Wealth tax is imposed in countries like França, Espanha, Switzerland, e Norway, which tax an individual’s total net wealth, including stocks, real estate, and other financial assets. Wealth tax rates and thresholds vary, so investors should consider how these taxes might impact their portfolios.

- Capital gains tax varies significantly across Europe. For example, Alemanha taxes capital gains at 25%, while Sweden imposes a 30% tax rate. Countries like Belgium e Bulgaria have some of the lowest rates, making them more attractive for capital gains investors.

- Stamp duties e financial transaction taxes also add costs to investments. For example, UK investors pay a 0.5% stamp duty on UK company shares, while França imposes a 0.3% tax on purchases of French companies with market capitalizations above €1 billion. These taxes should be factored into your investment decision.

Declaração de encerramento:

Knowing the tarifas e taxes associated with your investments is essential for effective portfolio management. By understanding the various transaction fees, wealth taxes, e capital gains taxes, you can better assess your potential returns and make more informed decisions about where to invest and how to optimize your portfolio.