Sura ya 7: Akiba na Fedha za Dharura

Malengo ya Somo:

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Utangulizi wa Kuokoa na Bidhaa za Kifedha

Kuelewa bidhaa mbalimbali za kifedha na umuhimu wa kuweka akiba ni muhimu katika usimamizi wa fedha za kibinafsi. Sura hii inaangazia aina tofauti za akaunti za benki, umuhimu wa fedha za dharura, na jinsi mfumuko wa bei na viwango vya riba vinavyoathiri uokoaji. Zaidi ya hayo, inashughulikia misingi ya taasisi za fedha na jinsi ya kusimamia na kukuza fedha za kibinafsi kwa ufanisi.

7.1 Types of Accounts and Financial Services

Taasisi za Fedha hutoa anuwai ya akaunti na huduma, kila moja iliyoundwa kwa mahitaji maalum ya kifedha:

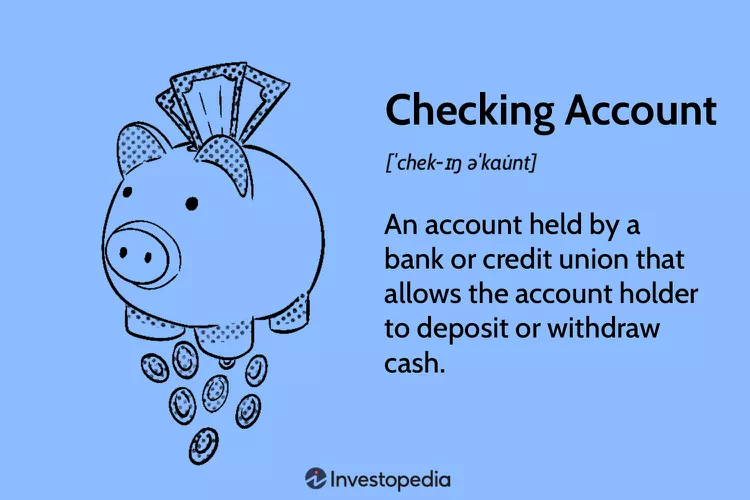

Kuangalia Akaunti:

Inatumika kwa shughuli za kila siku. Kawaida huja na kadi ya debit na kutoa amana na uondoaji usio na kikomo.

- Manufaa: Ufikiaji rahisi wa fedha, ufikiaji wa kadi ya benki, malipo ya bili mtandaoni.

- Hasara: Kawaida ni ya chini au hakuna riba inayopatikana.

Akaunti za Akiba:

Aimed at short-term savings over time. Offer interest on the stored funds.

- Manufaa: Pata riba, hatari ndogo.

- Hasara: Uondoaji mdogo, viwango vya riba vinavyoweza kuwa vya chini ikilinganishwa na bidhaa zingine za akiba.

Akaunti za Soko la Pesa (MMAs):

Mchanganyiko wa akaunti za hundi na akiba, kwa kawaida viwango vya juu vya riba na mahitaji ya juu zaidi ya salio.

- Manufaa: Viwango vya juu vya riba, haki za uandishi wa hundi.

- Hasara: Mahitaji ya juu ya usawa wa chini, miamala ndogo.

Vyeti vya Amana (CD):

Fixed-term savings account with a guaranteed interest rate.

- Manufaa: Viwango vya juu vya riba ikilinganishwa na akaunti za akiba, mapato yasiyobadilika.

- Hasara: Adhabu za kujiondoa mapema, pesa hazipatikani hadi muda utakapomalizika.

Figure: What is a Checking Account?

Maelezo:

This image visually defines a checking account, which is a primary tool for managing day-to-day finances. It highlights the main features of the account, such as a debit card and paper checks, which are used to make purchases and pay bills. The graphic serves as a simple introduction to one of the most basic and essential products in personal finance.

Mambo muhimu ya kuchukua:

- A checking account is a type of bank account that provides easy access to your money for daily transactions.

- It is designed for high ukwasi, meaning you can withdraw or spend your money quickly using tools like a debit card, ATM, or online transfers.

- The main purpose of this account is for spending and bill payments, not for earning interest; most checking accounts offer little to no interest on your balance.

- Keeping track of your transactions through a bank statement or online portal is crucial for kupanga bajeti and avoiding overdrafts.

Utumiaji wa Taarifa:

- A checking account is the foundation of personal financial management, acting as the operational center for your income and expenses.

- Learning to manage a checking account is a critical first step in creating a budget, tracking your spending, and building good financial habits.

- For anyone new to finance, this account is an essential tool for safely storing money, paying bills efficiently, and participating in the modern economy.

Kufungua na Kusimamia Akaunti:

Kufungua akaunti ya benki kwa kawaida huhitaji kutoa kitambulisho cha kibinafsi, Nambari ya Usalama wa Jamii na amana ya awali. Kudhibiti akaunti kunahusisha ufuatiliaji wa salio, kuweka amana na kutoa pesa, na ada za kuelewa kama vile mahitaji ya salio la chini zaidi na ada za overdraft.

Vipengele vya Akaunti:

Nambari ya akaunti hutambulisha akaunti yako kwa njia ya kipekee, huku nambari ya uelekezaji huitambulisha benki yako - muhimu kwa amana za moja kwa moja na kuweka malipo ya kiotomatiki.

Vyama vya Mikopo dhidi ya Benki za Biashara:

Credit unions typically offer lower fees and better interest rates but might have fewer branches and services. Commercial banks offer a broader range of services but may charge higher fees.

Kutathmini Bidhaa za Kifedha kwa Wanafunzi

Wanafunzi wanapaswa kuzingatia hundi na akaunti za akiba na ada za chini, ufikiaji rahisi wa pesa, na rasilimali za elimu kusaidia kusimamia fedha zao. Faida ni pamoja na kujifunza usimamizi wa pesa na kupata riba kwenye akiba. Hasara inaweza kuhusisha kudhibiti mahitaji ya salio la chini zaidi au kuabiri ada zinazowezekana.

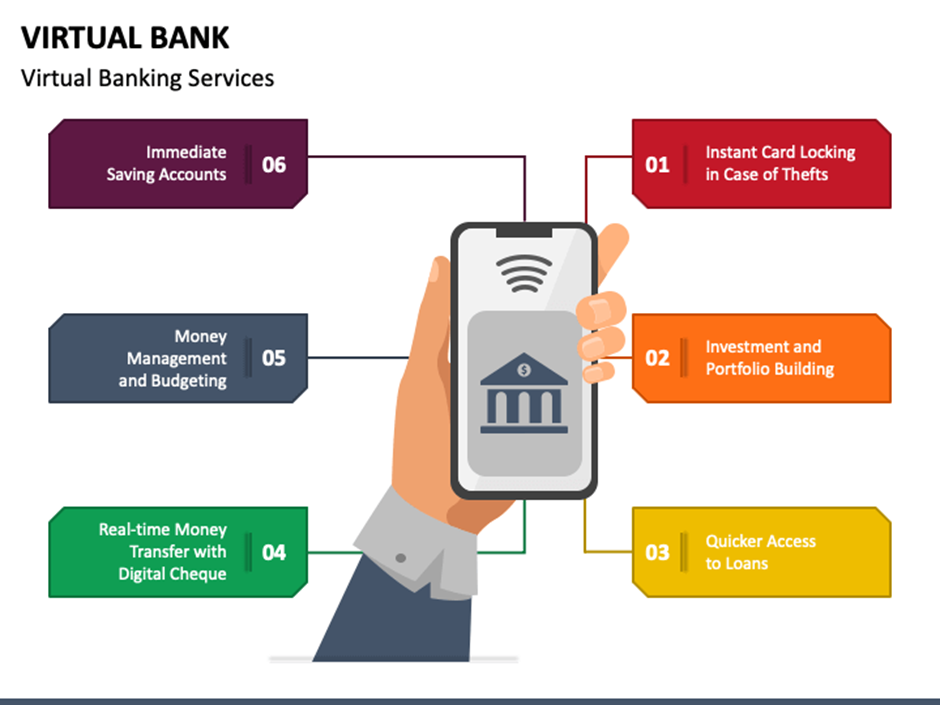

7.2 Online Banking and Account Management

Huduma ya Kibenki Mtandaoni hutoa ufikiaji rahisi wa huduma za kifedha, ikijumuisha kufungua akaunti, kuangalia salio na kuhamisha fedha. Vipengele muhimu ni pamoja na kuelewa mahitaji ya salio la chini zaidi, ada za kila mwezi, adhabu za overdrafti na viwango vya riba. Ni muhimu kufuatilia na kudhibiti fedha mara kwa mara ili kuhakikisha kuwa akaunti hulipa malipo na kuepuka ada.

Kielelezo: Key Benefits of Online Banking

Maelezo:

This graphic illustrates the main advantages of using online banking for managing personal or business finances. It visually highlights key features such as 24/7 account access from any device, the ease of making digital payments, and real-time transaction monitoring. The overall message is that online banking offers a more convenient, efficient, and powerful way to handle financial tasks.

Mambo muhimu ya kuchukua:

- Constant Accessibility: A major benefit of online banking is 24/7 access to your accounts from anywhere with an internet connection, eliminating the need to visit a physical bank.

- Efficiency and Cost Savings: It saves significant time by allowing you to automate bill payments and transfer funds instantly, and it often comes with lower fees than traditional banking services.

- Enhanced Financial Control: Online banking provides real-time visibility into your transactions and account balances, which is crucial for accurate budgeting and managing cash flow.

- Simplified Record-Keeping: Many platforms can integrate with accounting software, which automates bookkeeping and makes financial reporting much easier for individuals and businesses.

Utumiaji wa Taarifa:

- Adopting online banking is a foundational step for modern and efficient money management.

- It provides the tools to actively track your spending, automate your savings contributions, and maintain a clear, up-to-the-minute picture of your financial health.

- By leveraging these digital tools, you can reduce time spent on financial administration and focus more energy on achieving your primary goals, like kuwekeza for the future or growing a business.

Viwango vya Riba na Akiba

Wakati mahitaji ya mikopo yanapoongezeka, benki zinaweza kutoa viwango vya juu vya riba kwa amana ili kuvutia waokoaji zaidi, kuwapa pesa za kukopesha. Kinyume chake, katika soko la mikopo iliyojaa au kuzorota kwa uchumi, mahitaji ya kukopa hupungua, na benki zinaweza kupunguza viwango vya riba kwenye akaunti za akiba.

Akaunti za Malipo ya Simu dhidi ya Benki ya Kawaida

Akaunti za Malipo ya Simu hutoa urahisi na urahisi wa matumizi lakini kwa kawaida hukosa mapato ya riba, hivyo kupunguza uwezekano wa ukuaji wa akiba ikilinganishwa na jadi. Akaunti za Akiba, ambayo hutoa riba. Akaunti za Cryptocurrency hutoa tete na faida zinazowezekana lakini hazina bima ya shirikisho, tofauti na usalama na uwezekano wa ukuaji wa akaunti za akiba zilizo na bima ya shirikisho.

7.3 Comparing Mobile Payment Accounts, Cryptocurrency Accounts, and Traditional Bank Accounts

While mobile payment platforms like Venmo or Cash App and cryptocurrency wallets offer convenience and fast transactions, they typically do not provide interest earnings or federal insurance protections (like FDIC or NCUA insurance). Traditional savings and checking accounts offer lower risk, provide interest (even if modest), and are protected against institutional failures up to certain limits.

Feature | Mobile Payments | Akaunti za Cryptocurrency | Traditional Bank Accounts |

Bima | No federal insurance | No federal insurance | FDIC/NCUA insured |

Interest Earnings | None | Very rare | Common (low to moderate) |

Accessibility | High (instant transfer) | High (global access) | High (ATM, online banking) |

Risk Level | Medium to high | High (market volatility) | Low |

7.4 Why Certificates of Deposit (CDs) Typically Pay Higher Interest Rates

Certificates of Deposit (CDs) generally offer higher interest rates than regular savings accounts or interest-bearing checking accounts because they require depositors to commit their money for a specific period. This commitment gives banks more certainty about the availability of funds for lending and investments. In exchange for giving up liquidity (easy access to their funds), depositors are rewarded with higher rates. Early withdrawal often results in penalties, reinforcing the importance of keeping funds deposited for the full term.

Mfano:

A savings account might offer a 1% interest rate, while a 12-month CD could offer 4% during the same period.

Faida:

- Higher guaranteed returns over the term.

- Safe and predictable growth.

Hasara:

- Funds are locked until maturity.

- Penalties for early withdrawal.

7.5 Impact of Loan Demand on Deposit Interest Rates

When the demand for loans rises, banks often need additional funds to meet the demand. To attract more deposits (which they use to fund new loans), they may offer higher interest rates on savings accounts, CDs, and other deposit products. Essentially, banks are willing to pay more to bring in money they can lend out profitably.

Mfano:

If mortgage applications rise sharply, banks may raise deposit rates from 1.5% to 2% to attract savers and balance their funding needs.

7.6 Market Conditions Leading to Lower Savings Rates

In times of economic slowdown or when consumers and businesses are not borrowing as much, banks don’t need as many deposits. As a result, they may lower the interest rates paid on savings accounts. This often occurs during recessions or when central banks lower benchmark interest rates to stimulate the economy.

Mfano:

During a recession, banks may drop savings account interest rates from 2% down to 0.5%, reflecting lower loan demand and economic conditions.

7.7 Impact of Spending vs. Saving

Kuchagua kati ya kutumia mara moja na kuweka akiba kwa ajili ya siku zijazo ni tatizo la kawaida. Kutosheka mara moja kunaweza kusababisha majuto ikiwa kutazuia kufikia malengo muhimu zaidi ya kifedha, kama vile kununua nyumba au kupata kustaafu kwa starehe.

Hali ya 1:

Emily anaamua kununua kompyuta ya mkononi ya hali ya juu kwa msukumo, inayotolewa na vipengele vyake vya juu. Miezi kadhaa baadaye, anajuta kwa kutohifadhi pesa hizo kwa cheti cha kitaaluma ambacho kingeweza kuendeleza kazi yake, akionyesha umuhimu wa kutanguliza malengo ya kifedha ya muda mrefu badala ya kujiridhisha mara moja.

Hali ya 2:

Baada ya kupokea bonasi, Jake mara moja huweka likizo ya gharama kubwa. Ingawa ni jambo la kufurahisha, baadaye anatamani angehifadhi sehemu ya pesa kwa ajili ya hazina ya dharura wakati gari lake lilipohitaji matengenezo yasiyotazamiwa, akikazia usawaziko kati ya kufurahia sasa na kujitayarisha kwa ajili ya wakati ujao.

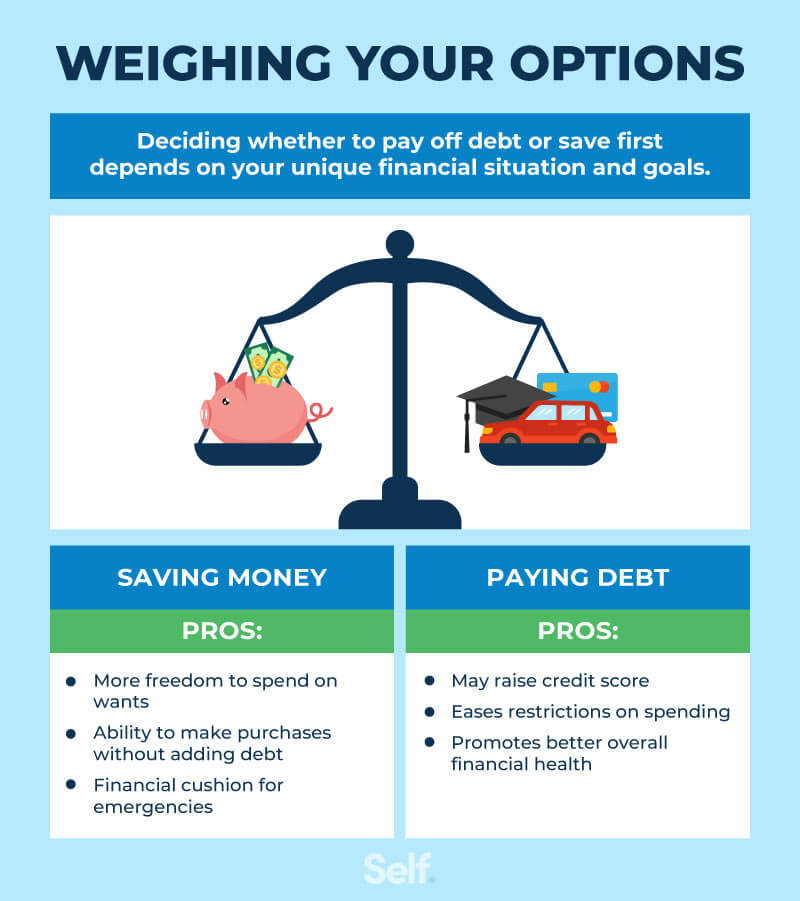

Kielelezo: Pay Off Debt vs. Save Money: Which Comes First?

Maelezo:

This image tackles the common financial dilemma of whether to focus on paying off debt au building savings. It presents a clear, step-by-step guide to help you decide where to direct your money first. The framework helps you create a balanced strategy that allows you to build a financial safety net while efficiently eliminating debt.

Mambo muhimu ya kuchukua:

- The first priority for almost everyone should be to build a starter mfuko wa dharura of at least $500 to $1,000. This prevents small emergencies from forcing you into more debt.

- After establishing a small emergency fund, you should aggressively pay down any high-interest debt, like credit card balances, as the interest charged is often very high.

- If your employer offers a retirement plan with a company match, contribute enough to get the full match, as this is essentially a 100% return on your investment and a top priority.

- Once high-interest debt is gone, you can adopt a balanced approach by simultaneously building your full 3-6 month emergency fund and saving for other long-term goals.

Utumiaji wa Taarifa:

- This model provides a clear roadmap to help you make smart decisions and reduce financial stress when you have competing financial priorities.

- You can use this framework to create an effective cash flow plan, ensuring your money is allocated in the most impactful way.

- By following these steps—starter mfuko wa dharura, attacking high-interest debt, and securing an employer match—you can build a strong financial foundation for future wealth creation.

7.8 Inflation and Interest Rates

Mfumuko wa bei hupunguza thamani ya pesa kwa wakati, na kupunguza uwezo wa ununuzi wa akiba. Kiwango cha kawaida cha riba hakizingatii mfumuko wa bei, ilhali kiwango cha riba halisi (kiwango cha kawaida chini ya kiwango cha mfumuko wa bei) kinaonyesha ukuaji halisi wa akiba. Waokoaji wanapaswa kutafuta kiwango cha kawaida ambacho kinapita mfumuko wa bei ili kuhifadhi thamani yao ya akiba.

Kiwango cha riba= riba ya jina - kiwango cha mfumuko wa bei

Mfano:

Ikiwa kiwango cha kawaida cha riba kwenye akaunti ya akiba ni 3% na kiwango cha mfumuko wa bei ni 2%, kiwango cha riba halisi ni 1%. Zaidi ya mwaka mmoja, uwezo wa kununua wa pesa katika akaunti hii hukua kwa 1% pekee inaporekebishwa kwa mfumuko wa bei, na hivyo kusisitiza umuhimu wa kutafuta chaguo za kuokoa au uwekezaji ambazo hupita kasi ya mfumuko wa bei ili kukuza utajiri kikweli baada ya muda.

7.9 Inflation Protection and I Bonds

Dhamana zimeundwa ili kulinda dhidi ya mfumuko wa bei, kwani viwango vyao vya riba vinabadilika kulingana na mfumuko wa bei. Mfumuko wa bei unapopanda, kiwango cha riba kwenye Dhamana huongezeka, na hivyo kuhakikisha kwamba akiba hudumisha uwezo wao wa kununua kwa wakati, tofauti na CD za kawaida, ambapo viwango vya riba vilivyoidhinishwa vinaweza kusababisha mapato hasi halisi katika mazingira ya juu ya mfumuko wa bei.

Thamani ya Baadaye na Punguzo

Kielelezo: Calculating the Future Value of a Single Cash Flow

Maelezo:

The infographic likely demonstrates the formula for calculating the future value of a single cash flow, which is a fundamental concept in finance. This formula helps in understanding how much an investment made today will grow to at a future date, considering a specific rate of interest. The formula is typically represented as FV = PV(1 + r)^n, where FV is the future value, PV is the present value, r is the interest rate, and n is the number of periods.

Mambo muhimu ya kuchukua:

- Fomula ya thamani ya siku za usoni (FV) ni muhimu kwa kukokotoa jinsi uwekezaji unavyokua kwa wakati.

- Kuelewa fomula hii huruhusu wawekezaji kukadiria thamani ya uwekezaji katika siku zijazo.

- Vigezo katika fomula ni pamoja na thamani ya sasa (PV), kiwango cha riba (r), na idadi ya vipindi (n), kila kimoja kikiwa na jukumu muhimu katika kukokotoa.

Utumiaji wa Taarifa:

This concept is essential for anyone involved in financial planning, investment analysis, or saving for future goals. By applying this formula, individuals can make informed decisions about their investments, understanding how different rates of interest and time periods affect the growth of their money. It encourages strategic investment and helps in setting realistic expectations for investment returns, which is fundamental for long-term financial planning and wealth accumulation.

Kwa kutumia lahajedwali, tunakokotoa kuwa mtoto wa miaka 10 anahitaji kuokoa $200 kwa mwezi kwa kiwango cha riba cha mwaka cha 5% ili kumudu mwaka mmoja wa masomo ya chuo kikuu, inayokadiriwa kuwa $20,000 miaka minane kutoka sasa. Mfano huu unaonyesha punguzo la thamani ya baadaye ya pesa, kuhesabu riba ili kubainisha ni kiasi gani kinahitaji kuokolewa leo ili kutimiza malengo ya kifedha ya siku zijazo.

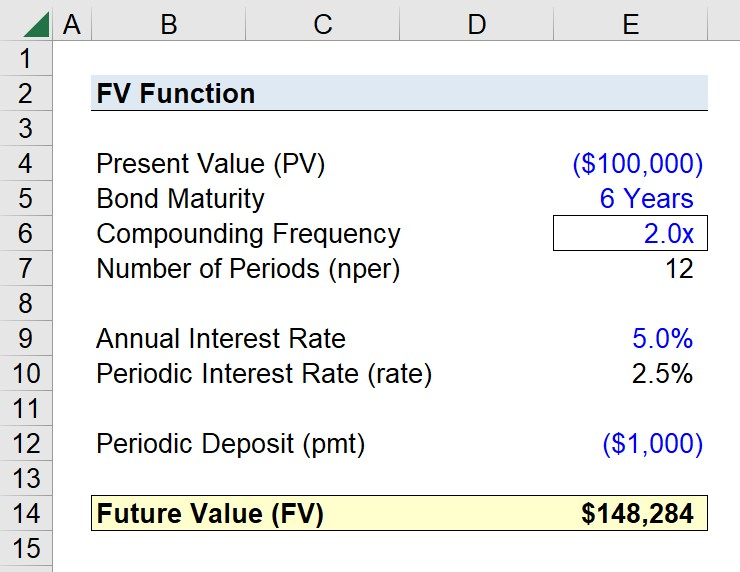

Kielelezo: Using the FV Function in Excel to Calculate Future Value

Maelezo:

The infographic likely demonstrates how to use the FV function in Excel to calculate the future value of an investment, considering a constant interest rate over a number of periods. The FV function is a powerful tool in Excel for financial analysis, allowing users to input variables such as rate, number of periods, payments, present value, and type (whether payments are made at the beginning or end of periods) to compute the future value of an investment.

Mambo muhimu ya kuchukua:

- Chaguo za kukokotoa za FV katika Excel ni muhimu kwa kukokotoa thamani ya baadaye ya uwekezaji.

- Ingizo muhimu za chaguo za kukokotoa za FV ni pamoja na kiwango cha riba, idadi ya vipindi, malipo ya mara kwa mara, thamani ya sasa na muda wa malipo.

- Kuelewa jinsi ya kutumia kipengele cha FV kunaweza kuboresha kwa kiasi kikubwa uundaji wa muundo wa kifedha na ujuzi wa kuchanganua uwekezaji.

Utumiaji wa Taarifa:

This knowledge is crucial for finance students, financial analysts, and anyone involved in investment planning or analysis. By mastering the FV function, users can quickly assess the potential future value of investments, aiding in decision-making processes. It’s particularly useful for evaluating the growth of savings accounts, retirement funds, or any investment over time, providing a clear picture of financial futures.

7.10 Down Payments and Loans

Kufanya malipo ya awali ya mkopo, kama vile malipo ya chini ya 20% kwenye nyumba, hupunguza jumla ya kiasi kilichokopwa, hivyo basi kupunguza malipo ya kila mwezi na viwango bora vya riba. Hii humfanya mkopaji kuvutia zaidi kwa wakopeshaji na inaweza kupunguza kwa kiasi kikubwa gharama ya mkopo kwa muda.

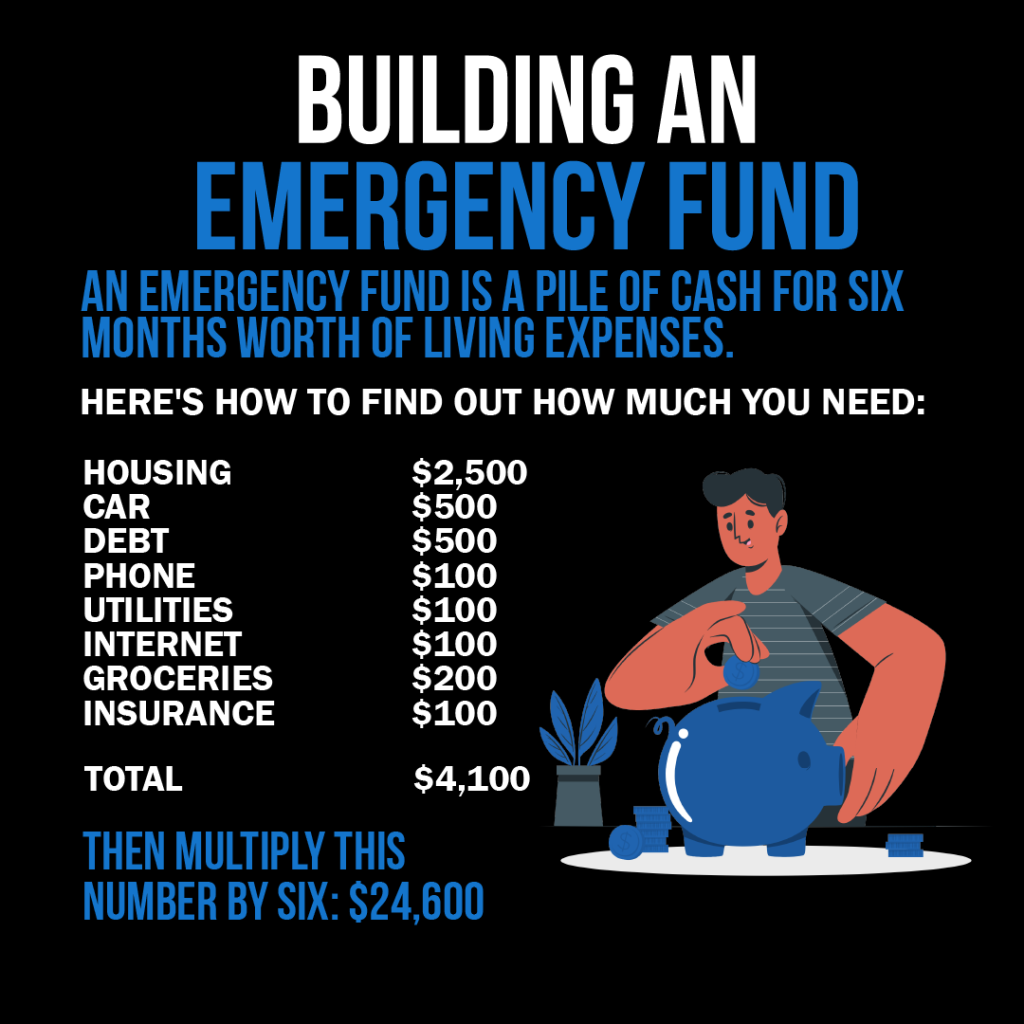

7.11 Emergency Funds and Financial Planning

Hazina ya Dharura ni muhimu kwa utulivu wa kifedha, kutoa wavu wa usalama kwa gharama zisizotarajiwa. Kuunda na kudumisha bajeti inayojumuisha utengaji wa akiba ya muda mfupi na ya muda mrefu huhakikisha kujiandaa kwa kutokuwa na uhakika wa maisha na maendeleo kuelekea malengo ya kifedha.

Mfano:

Gari la Maria linaharibika, na kuhitaji matengenezo ya gharama kubwa. Yeye hurekebisha bajeti yake ili kupunguza matumizi ya hiari na kutenga tena pesa kutoka kwa aina zake za burudani na milo ili kulipia gharama za ukarabati, huku akipunguza michango kwa akaunti yake ya akiba kwa muda.

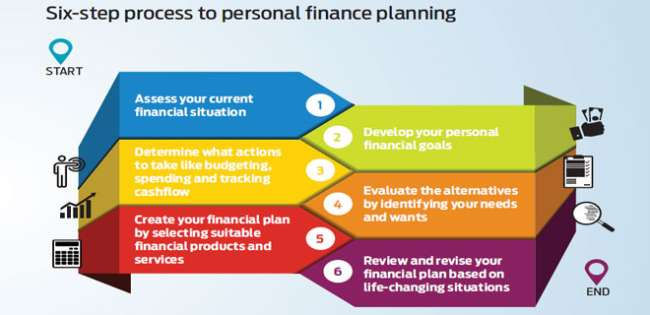

Kielelezo:Mchakato wa Hatua Sita kwa Mipango ya Fedha Binafsi

Maelezo:

Picha inatanguliza mchakato wa hatua sita wa upangaji wa fedha za kibinafsi. Huanza kwa kutathmini hali ya sasa ya kifedha ya mtu, ikijumuisha mali na madeni, na kuendelea kupitia kuweka malengo ya kifedha, kuunda mpango wa utekelezaji, kutathmini chaguzi za uwekezaji, kutekeleza mpango, na kupitia upya na kurekebisha mkakati mara kwa mara.

Mambo muhimu ya kuchukua:

- Tathmini ya fedha za sasa is crucial as a starting point for planning.

- Mpangilio wa malengo involves assigning value and timelines to short, medium, and long-term financial aspirations.

- An mpango kazi must consider one’s risk tolerance and align investment choices accordingly.

- Chaguzi za uwekezaji inapaswa kuunganishwa na malengo mahususi na kuchaguliwa kwa kuzingatia ufanisi na ufaafu wa kodi.

- Uwekezaji wa mara kwa mara inachangia malezi ya tabia na mafanikio laini ya malengo ya kifedha.

- Mapitio ya mara kwa mara kuhakikisha kuwa uwekezaji uko kwenye mstari na kuruhusu marekebisho inavyohitajika.

Utumiaji wa Taarifa:

Kuanzia na tathmini ya hali ya sasa ya kifedha ya mtu ni msingi katika upangaji wa fedha za kibinafsi. Kwa kuelewa mahali unaposimama kifedha, unaweza kuweka malengo ya kweli, kutambua maeneo ya kuboresha, na kuunda ramani ya kufikia utulivu na ukuaji wa kifedha. Hatua hii inahakikisha kwamba upangaji unaofuata una msingi katika uhalisia na kulengwa kulingana na hali ya kipekee ya kifedha ya mtu binafsi.

Contingency Planning for Financial Emergencies

Contingency planning involves preparing for unexpected financial shocks by having backup savings or insurance. A good contingency plan can help cover emergency expenses such as car repairs, medical bills, sudden unemployment, or major household repairs without derailing long-term financial goals.

Mfano:

- Backup Fund: Besides an emergency fund, maintain a small “contingency fund” specifically for very short-term needs.

- Insurance: Maintain adequate health, auto, and renters/homeowners insurance to mitigate major risks.

- Backup Budget: Create a reduced-spending version of your budget to activate if income drops suddenly.

Kuelewa Malipo na Makato

Malipo ya Jumla ni jumla ya mapato ya mfanyakazi kabla ya makato yoyote. Net Pay, au malipo ya kurudi nyumbani, ndiyo yanayosalia baada ya kodi, huduma za afya na makato mengine. Kuelewa tofauti ni muhimu kwa upangaji sahihi wa bajeti.

7.12 Financial Institutions and Services

Taasisi za Kifedha, zikiwemo benki, vyama vya mikopo na mifumo ya mtandaoni, hutoa bidhaa mbalimbali kama vile akaunti za hundi na akiba na huduma za kupanga fedha. Kuchagua taasisi na huduma zinazofaa ni muhimu kwa usimamizi mzuri wa pesa na kufikia malengo ya kifedha.

Mfano wa Usimamizi wa Akaunti:

Ili kudhibiti akaunti ya ukaguzi kwa ufanisi, kagua mara kwa mara miamala na upatanishe na rekodi za kibinafsi ili kuhakikisha usahihi. Kutumia programu za benki ya simu kunaweza kurahisisha ufuatiliaji na kusaidia kuzuia ada za overdraft.

7.13 The Role of FDIC and NCUA Insurance

The Federal Deposit Insurance Corporation (FDIC) insures deposits at banks, while the National Credit Union Administration (NCUA) insures deposits at credit unions. Both agencies guarantee deposit accounts (up to $250,000 per depositor, per insured bank or credit union) in case the financial institution fails. This insurance provides consumers with peace of mind that their money is protected against institutional collapse.

Mfano:

If your bank closes unexpectedly, the FDIC will reimburse your insured deposits up to the coverage limit.

Hitimisho

Saving, managing financial products, preparing for inflation, and understanding the broader banking environment are essential skills for long-term financial success. By supplementing your knowledge with insights about CDs, market influences on interest rates, the differences between mobile/crypto accounts and traditional banks, federal insurance protections, and emergency contingency planning, you’ll be even better equipped to protect and grow your financial future.

Habari Muhimu ya Somo:

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.