Глобальний вміст Розділ A: Глобальне розуміння іпотеки

Цілі навчання:

- Understand the fundamental aspects of a mortgage, including primary and secondary mortgages, and their role in financing property purchases.

- Explore the diversity of lenders in the global market, from traditional banks to private lenders and the secondary mortgage market.

- Learn about the impact of interest rates on mortgage affordability and the popularity of different mortgage types across various countries.

- Identify the advantages and risks associated with mortgage financing, including the benefits of leverage and the potential for foreclosure.

- Examine legal and negotiation aspects of mortgages, focusing on global variations in mortgage agreements and strategies for securing favorable terms.

Section A: Understanding Mortgages Globally

What is a Mortgage?

А mortgage is a long-term loan used to finance the purchase of real estate. Mortgages are secured loans, meaning the property serves as collateral. If the borrower fails to repay, the lender can foreclose on the property to recover the debt.

Primary Mortgage

Globally, a primary mortgage is the first loan taken out to purchase a property. The terms of the loan, including the interest rate and down payment requirements, vary widely between countries. In the United States, for example, down payments can range from 3% to 20% depending on the loan type.

Secondary Mortgage

А secondary mortgage, or second lien, is a loan taken out on a property that already has a mortgage. This is more common in markets like the United States, where homeowners use second mortgages to access home equity for renovations or debt consolidation.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Section B: Types of Lenders Globally

Traditional Banks

Traditional banks around the world, such as Chase in the U.S. and HSBC in the U.K., dominate mortgage lending. These banks typically offer competitive rates, but their lending criteria may be strict, including minimum credit score requirements and down payments.

Private Lenders

Globally, private lenders provide alternative financing options for borrowers who may not qualify for traditional loans. In Австралія, for example, private lenders often charge higher rates but offer more flexible terms than banks.

Secondary Market

The secondary mortgage market is well-developed in countries like the United States, where mortgages are bundled into mortgage-backed securities and sold to investors. This allows banks to issue more loans while spreading risk across the financial system.

Section C: Key Mortgage Concepts Globally

Процентні ставки

Globally, interest rates on mortgages are influenced by central bank policies. In the United States, for example, the Federal Reserve’s actions have a direct impact on mortgage rates. Countries like Japan have kept interest rates low for decades, making mortgages more affordable.

Fixed-Rate Mortgages

А fixed-rate mortgage provides stability as the interest rate remains the same throughout the term of the loan. Fixed-rate mortgages are particularly popular in countries like the United States, where homebuyers often seek long-term payment predictability.

Variable-Rate Mortgages (ARM)

А variable-rate mortgage (ARM) has interest rates that fluctuate based on economic conditions. In countries like Канада і Австралія, ARMs are common, with rates tied to market benchmarks.

Section D: Pros and Cons of Mortgages Globally

Плюси

- Leverage: Mortgages allow investors to buy property without paying the full amount upfront, offering leverage to grow wealth through appreciation.

- Income Tax Deductions: In countries like the U.S., mortgage interest is tax-deductible, providing financial benefits to homeowners.

Мінуси

- Risk of Foreclosure: Failure to repay a mortgage results in foreclosure, where the lender takes ownership of the property.

- Interest Costs: Over time, the total amount paid on a mortgage can far exceed the property’s purchase price due to interest.

Section E: Legal Considerations Globally

Mortgage Agreements

Mortgage agreements vary globally but generally outline loan terms, repayment schedules, and conditions for default. In the U.S., mortgage agreements often include clauses allowing for foreclosure if the borrower misses payments.

Legal Requirements

Legal requirements for mortgages differ by country. In Канада, borrowers must pass a mortgage stress test to ensure they can afford the loan. In the U.S., closing costs and title insurance are mandatory.

Section F: Tips for Negotiating a Mortgage Globally

Research and Preparation

Globally, researching and comparing mortgage options is key to successful negotiation. In countries like the United States, mortgage rates and terms can vary widely between banks, credit unions, and online lenders. Use comparison tools and mortgage calculators to understand the best offers available.

Negotiation Strategies

- Down Payment: Offering a larger down payment can reduce your interest rate or shorten the loan term. In countries like Канада і Австралія, lenders may provide better terms for borrowers who offer at least 20% down.

- Interest Rate: You can often negotiate the interest rate, especially if you have a strong credit score. Ask lenders to match or beat competing offers.

- Fee Reduction: Some global lenders charge closing fees, processing fees, or penalties for early repayment. Negotiate to reduce or eliminate these fees where possible.

Things to Look Out For

- Prepayment Penalties: In some countries, such as the United States, paying off your mortgage early may incur penalties. Make sure to review your loan documents carefully.

- Variable Rate Risks: If you opt for an ARM, be aware that interest rates could rise significantly over time, increasing your payments.

Малюнок: Negotiating Tactics Used in Different Countries

опис:

This table provides an overview of negotiating tactics used in various countries, highlighting the cultural differences in communication and negotiation styles. Countries such as Japan exhibit a polite and non-aggressive style with frequent silent periods, while Korea relies on more commanding tactics, including frequent use of the word “no.” In the United States, negotiating behavior is characterized as balanced, falling between extremes seen in other countries. Other examples include Northern China, where questioning is common, and Russia, where frequent silent periods are combined with questioning. The table underscores the significance of understanding cultural nuances in global negotiations.

Ключові висновки:

- Japan’s negotiation style is polite and indirect, with an emphasis on positive communication and silent periods.

- Korea employs punishment and command, making its style more direct and assertive.

- The United States balances negotiation strategies, aligning closely with German and British styles.

- Northern China’s approach involves detailed questioning and information exchange, with some silent pauses.

- Russia incorporates silence and frequent questioning, while Germany emphasizes self-disclosure over direct questioning.

Застосування інформації:

This data is critical for business professionals, diplomats, and negotiators to tailor their approach when working with people from different cultural backgrounds. Understanding these tactics can foster effective communication, reduce misunderstandings, and build stronger business relationships. Learners can use this knowledge to enhance their cross-cultural negotiation skills and adapt strategies to suit specific cultural preferences.

Section G: Affordability Considerations Globally

Budgeting for a Mortgage

When budgeting for a mortgage globally, consider not only the monthly payments but also property taxes, insurance, та maintenance costs. In the United States, for example, property taxes vary by state and can be a significant expense.

Budgeting Rule: Mortgage payments should not exceed 28-30% of your gross monthly income, a common guideline used globally.

Affordability for Buying

When buying a home in global markets like New York, Tokyo, or Sydney, affordability depends on local property values and interest rates. Use mortgage calculators to estimate monthly payments based on current interest rates and your desired loan term.

Affordability for Renting

In cities with skyrocketing real estate prices, such as Hong Kong або San Francisco, renting may be more cost-effective than buying. Compare rental costs with mortgage payments and other homeownership expenses to determine the best option for your financial situation.

Section H: Real-World Examples Globally

Example 1: Calculating Monthly Payments

Assume you are purchasing a home in the United States with a mortgage of $300,000 at an interest rate of 4% for a 30-year term. The monthly payment calculation is:

M=P×r(1+r)n(1+r)n−1M = \frac{P \times r(1 + r)^n}{(1 + r)^n – 1}M=(1+r)n−1P×r(1+r)n

Where:

- M is the monthly payment.

- P is the loan amount ($300,000).

- r is the monthly interest rate (4% annually = 0.00333 per month).

- n is the number of payments (30 years = 360 months).

This formula gives you the amount you would need to pay monthly, including both principal and interest.

Example 2: Evaluating Affordability

If you earn $5,000 per month, the maximum mortgage payment using the 28% rule would be $1,400. This gives you a benchmark for evaluating different loan offers, helping you choose the most affordable mortgage.

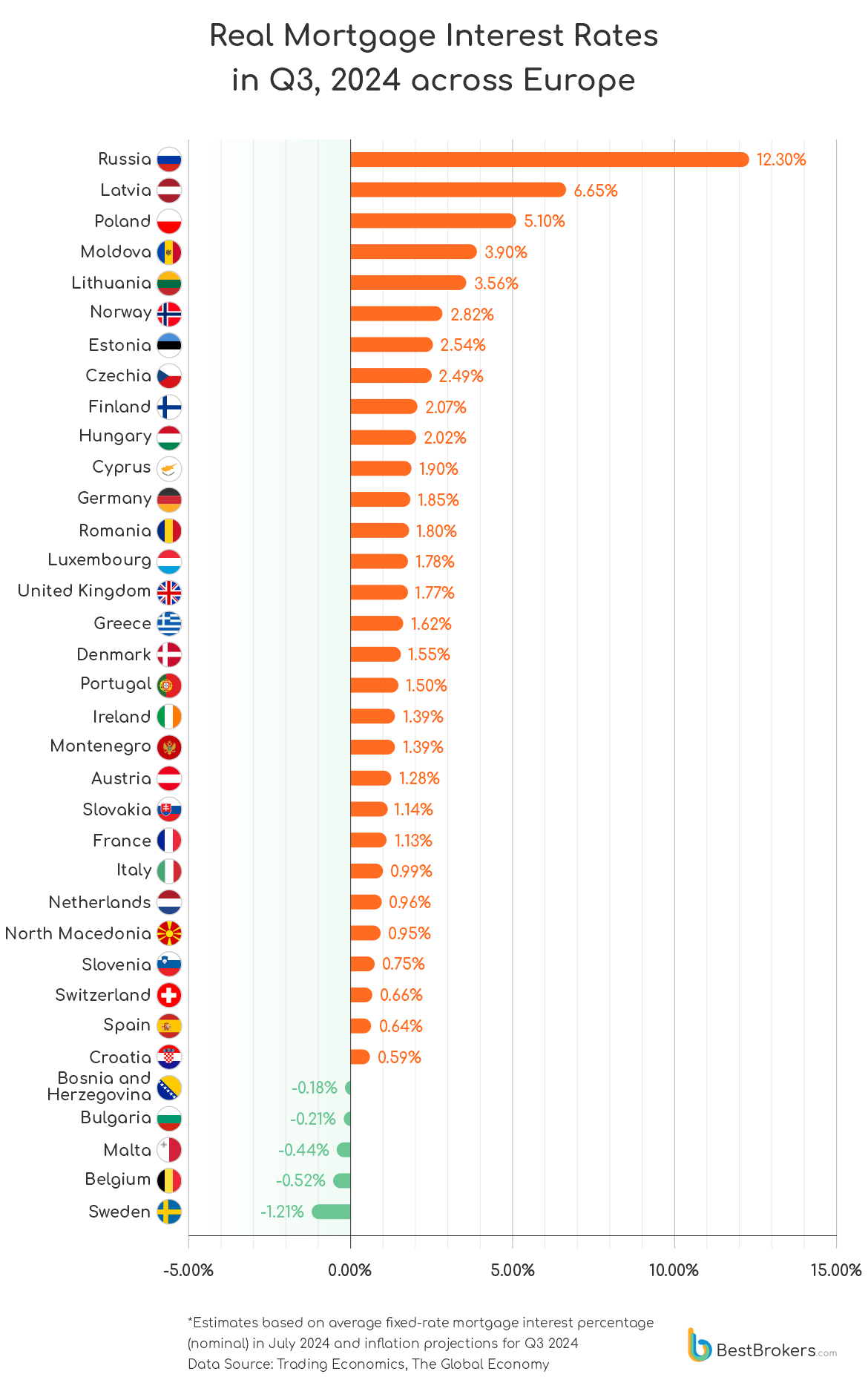

Малюнок: Real Mortgage Interest Rates in Q3, 2024 Across Europe

опис:

This bar chart compares the real mortgage interest rates across European countries in Q3 2024. Countries are ranked from the highest rates, with Russia at 12.30%, to the lowest, where Sweden has a negative rate of -1.21%. High-interest rates in countries like Latvia (6.65%) і Poland (5.10%) suggest a challenging borrowing environment. On the other hand, countries such as Sweden, Belgium (-0.52%), and Malta (-0.44%) offer favorable borrowing conditions. The chart illustrates a stark variation in mortgage rates across Europe, highlighting the diverse economic and financial conditions in the region.

Ключові висновки:

- Russia leads with the highest real mortgage interest rate (12.30%), indicating high borrowing costs.

- Countries such as Sweden (-1.21%) і Belgium (-0.52%) offer the most favorable borrowing conditions, with negative real rates.

- Eastern European countries (e.g., Latvia, Moldova, and Poland) tend to have higher mortgage rates, reflecting inflationary pressures or risk premiums.

- Western European countries як France (1.13%) і Italy (0.99%) have moderate rates, offering balanced borrowing conditions.

- The wide variation in rates underscores the differences in economic stability, monetary policy, and inflation across European countries.

Застосування інформації:

This data is essential for real estate investors, homebuyers, and financial analysts to evaluate borrowing costs across Europe. High-rate countries may deter property purchases or encourage alternative financing methods, while low-rate countries may attract more buyers and boost real estate demand. Understanding these trends helps investors identify market opportunities and assists learners in analyzing how monetary policies and inflation influence mortgage rates.

Висновок

Understanding real estate financing and mortgages is essential for making informed decisions in both local and global real estate markets. By knowing how to negotiate mortgage terms, assess affordability, and account for legal considerations, you can better position yourself to achieve long-term financial success through real estate investments.

Ключова інформація про урок:

- Mortgages are crucial for real estate financing, acting as secured loans where the property serves as collateral.

- Various types of lenders offer different mortgage products, each with its own set of terms and conditions that can impact the borrower’s financial commitments.

- Interest rates greatly influence mortgage affordability, with fixed-rate and variable-rate mortgages providing options to suit different risk tolerances and financial strategies.

- Negotiating a mortgage requires understanding local market conditions and lender practices, which can vary significantly from one country to another.

- Legal considerations and affordability issues are paramount in mortgage agreements, impacting everything from payment terms to foreclosure procedures.

Заключне слово:

Understanding mortgages globally is essential for navigating the complex world of real estate investment. By grasping the different types of mortgages, lender options, and key financial principles, investors can make informed decisions tailored to their financial goals and market conditions.