第五章:预算和费用管理

课程学习目标:

Lorem ipsum dolor sit amet,consectetur adipiscing elit。 Ut elit tellus,luctus nec ullamcorper mattis,pulvinar dapibus leo。

预算和费用管理简介

预算和费用管理是个人理财的基本方面。本章探讨如何制定符合短期和长期财务目标的预算,包括应急基金的分配,并解决消费者决策的动态及其更广泛的影响。此外,我们将深入探讨储蓄与投资的本质、修改预算以适应生活变化,以及了解现金流和财务费用的重要性。

5.1 Developing a Budget

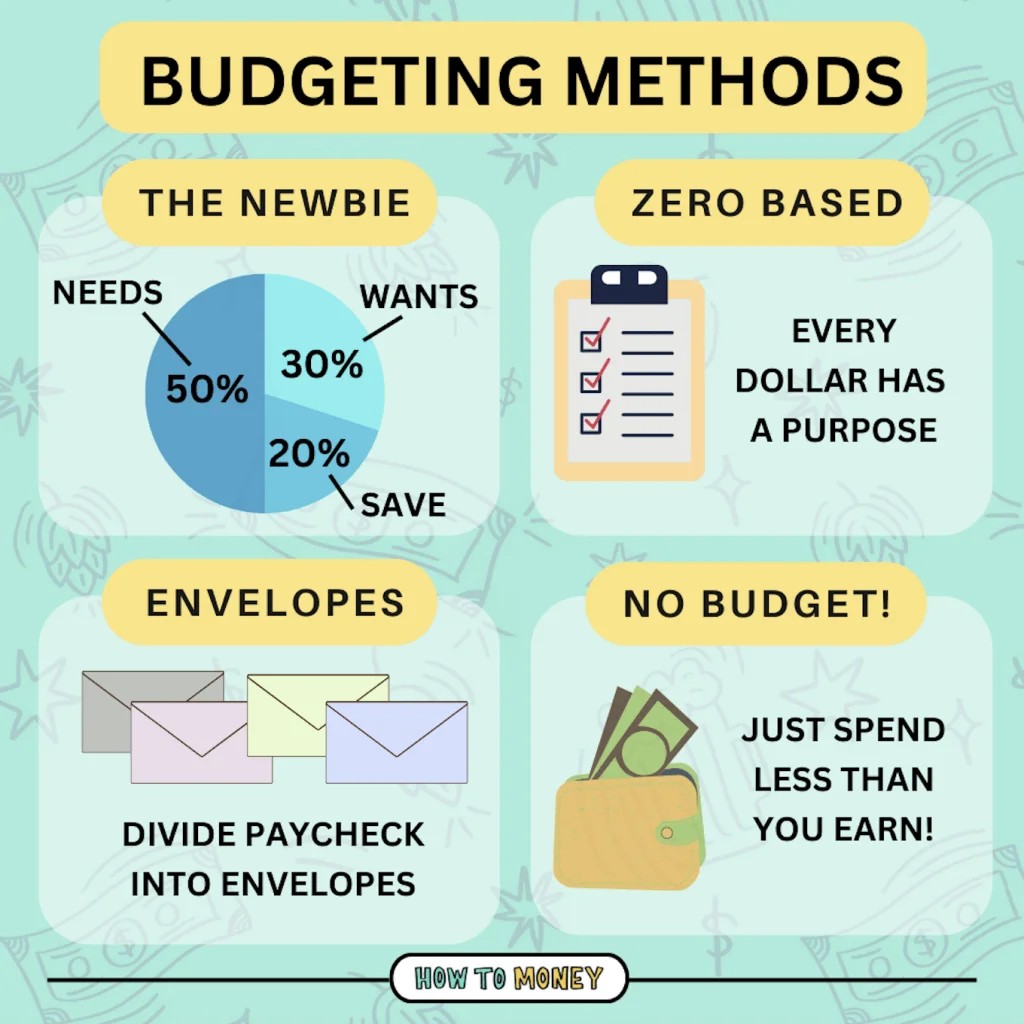

有多种预算方法可供选择,每种方法都有自己的优点和缺点。找到最适合您需求和偏好的方法至关重要。以下是三种流行的预算方法:

预算包括跟踪收入、分配资金用于各种支出以及留出储蓄以实现财务目标。精心制定的预算包括:

- 固定费用:经常性费用,例如租金或抵押贷款、贷款支付和保险。

- 变动费用: 波动的成本,例如食品杂货、水电费和娱乐费。

- 节省: 指定用于未来用途的资金,包括应急资金和长期储蓄目标。

- 应急基金: 财务规划的一个重要部分,旨在支付意外开支,例如医疗紧急情况或汽车维修。

Example Scenario: Jamie earns $3,000 monthly and wants to save for a vacation while covering living expenses. A budget might allocate $1,000 to rent, $300 to groceries, $200 to utilities, $400 to loan payments, $100 to entertainment, and $600 to an emergency fund, illustrating a balanced approach to managing fixed and variable costs and prioritizing savings.

数字: 预算方法的类型

描述:

该图展示了适合不同偏好和财务状况的各种预算方法。它简化了预算的概念,使其更加平易近人,并解释了 50/30/20 预算、信封预算、零基预算和无预算等方法,每种方法都旨在帮助个人有效地管理财务。

要点:

- 50/30/20 预算: 一种简单的方法,其中 50% 的收入用于满足需求,30% 用于满足想要的东西,20% 用于储蓄或偿还债务。

- 信封预算: 将现金分配到特定类别的实体信封中的一种方法。支出仅限于每个信封中的现金。

- 零基预算: 每赚一美元都有特定的用途,确保月底预算平衡为零。

- 无预算的预算: 适合高收入且有良好理财习惯的人士。重点是赚得比花得多,并将差额投资。

信息应用:

不同的预算方法适合不同的性格类型和财务状况。了解并选择正确的方法可以让人们有效地管理财务,确保他们量入为出并实现财务目标。无论人们是想控制过度支出、有效分配资金,还是只是想更好地控制自己的财务,这些方法都提供了实现这些目标的结构化方法。

5.2 Making Informed Consumer Decisions

消费者的决策受价格、产品选择、预算限制以及潜在的社会和环境影响等因素影响。

做出明智决策的过程:

- 研究: 收集有关产品和替代品的信息。

- 预算: 考虑一下购买是否适合您的预算。

- 影响: 评估对环境和社会的潜在影响。

示例:尽管初始成本较高,但选择电动汽车而不是汽油车是因为可以考虑长期节省燃料、享受环境效益以及享受税收优惠。

5.3 Consumer Decision Factors

所选产品:电动汽车 (EV)

影响购买决策的因素:

- 产品价格: 电动汽车的前期成本可能高于汽油动力汽车。不过,税收优惠和较低的运营成本可能会抵消初期费用。

- 替代品的价格: 传统汽油汽车通常前期成本较低,但随着时间的推移燃料和维护成本会更高。

- 消费者的预算和偏好: 消费者购买电动汽车的能力以及他们对环保选项的偏好起着重要作用。有些人可能优先考虑环保而不是成本,而其他人可能注重长期节省。

- 对环境、社会和经济的影响: 购买电动汽车可以减少排放,对环境的影响较小。这一选择还可以支持可再生能源行业的发展,推动社会和经济向可持续发展转变。

做出明智消费者决策的过程:

- 研究: 收集有关各种模型的信息,包括其特点、成本和评论。

- 比较: 从成本、性能和需求适用性方面比较电动汽车与传统汽车。

- 预算评估: 评估个人财务状况以确定承受能力并考虑长期储蓄。

- 环境影响: 考虑电动汽车的生态效益。

- 最终决定: 请根据以上因素的平衡考虑进行选择。

购买电动汽车的影响:

- 积极:减少碳足迹,降低运营成本,促进可再生能源产业的发展。

- 缺点:较高的初始成本可能会给预算带来压力;电动汽车电池的生产和处理会对环境产生影响。

5.4 Managing Expenses and Budgeting

开支:

- Fixed Expenses: Rent, mortgage, car payments – costs that remain constant each month.

- 变动费用: Groceries, utilities, entertainment – costs that can fluctuate.

- Irregular Expenses: Annual insurance premiums, holiday gifts – costs that occur occasionally and can disrupt a regular budget.

我的每月预算示例:

- 固定支出:$1,200 租金、$300 车款、$100 保险。

- 变动支出:$400 食品杂货,$150 水电费,$100 娱乐费。

- 不定期开支:每月留出 $50 用于订阅或会员等年度费用。

- 储蓄:目标是每月储蓄 $500 作为应急基金和未来投资。

- 盈余或赤字:计算收入减去总支出(包括储蓄)以确定您是否量入为出或超支。

预算策略:

- 信封系统: 每月将用于变动开支的现金分装到不同的信封中。信封中的现金用完后,直到下个月才允许在该类别中再进行消费。

- 保持预算活力: 定期审查和调整预算。跟踪支出、识别模式并做出更改以确保实现目标。利用预算应用程序或电子表格进行实时跟踪和调整。

管理费用

为了控制支出,区分必要支出和可自由支配支出至关重要。减少不必要支出的策略包括识别冲动性购买、利用信封系统管理现金支出以及定期检查消费习惯。

必要(基本)开支 是日常生活中基本生活和运作所需的费用。这些费用涵盖个人或家庭维持健康和安全生活方式的最低需求。必要费用通常包括:

- 住房:租金或抵押贷款。

- 公用设施:水、电、煤气,有时还有互联网服务,具体取决于远程工作或教育的需要。

- 食物:家庭烹饪所需的食品杂货。

- 医疗保健:保险费、医疗账单、处方和任何正在进行的医疗治疗。

- 交通:上下班或上学的相关费用,包括汽车费用、公共交通费、汽油费和基本车辆维护费。

- 保险:必要的保险单,包括健康、汽车、房主或租房者保险。

必要开支示例:莎拉每月预算 $1,000 用于房租,$200 用于水电费,$300 用于食品杂货,$250 用于汽车贷款和汽油费,$150 用于健康保险。这些费用对于她安全舒适的生活来说是不可商议的。

可自由支配的(非必要)费用 是与人们想要但不需要的基本生活方式相关的费用。这些费用通常会提高生活质量,但如果需要,可以减少或消除。可自由支配的开支包括:

- 娱乐:花在电影、音乐会、流媒体服务或其他娱乐活动上的钱。

- 外出就餐:在餐厅就餐而产生的超出营养所需的费用。

- 爱好:与爱好或休闲活动相关的费用,例如手工材料、运动器材或购买书籍。

- 旅行:度假和非必要旅行的费用。

- 奢侈品:高端电子产品、名牌服装以及其他超出基本需求的奢侈品。

可自由支配支出示例:Alex 喜欢外出就餐,平均每月在餐厅花费 $300,订阅多项流媒体服务,每月花费 $50,并分配 $200 用于爱好和娱乐。虽然这些可以改善他的生活,但可以根据他的财务目标或情况进行调整。

管理必要和可自由支配的开支:有效的财务规划首先要确保必要的开支在预算之内。剩余的收入可以用于自由支配的开支、储蓄和投资。优先考虑储蓄和偿还债务而不是自由支配的开支对于长期的财务健康至关重要。个人可能需要定期审查自己的消费习惯,尤其是自由支配的开支,以根据收入或财务目标的变化调整预算。

通过区分必要开支和可自由支配开支并了解其对整体财务规划的影响,个人可以做出符合其优先事项和财务目标的明智决定,确保稳定并朝着目标前进。

5.5 Creating and Revising Budgets

预算需要灵活,以反映收入、生活环境和财务目标的变化。

- 短期储蓄:应涵盖紧急情况和意外开支。

- 长期储蓄: 旨在实现未来的愿望,例如拥有住房或退休。

调整预算: 生活中的事件,例如工作变动或意外账单,需要调整预算以保持财务状况正常。

Example: If Alex experiences a job loss, the budget must be revised to reduce variable expenses and prioritize essential costs and minimal savings until income stabilizes.

- 储蓄是将钱留作未来使用,通常是低风险、容易获得的 储蓄与投资 帳戶。

- 投资涉及购买可能随着时间的推移获得更高回报的资产,但伴随而来的风险也更大。

理解区别有助于使财务策略与目标保持一致,平衡储蓄的安全性和投资的增长潜力。

5.6 Designing a Personal Budget

个人预算应反映个人独特的财务状况、目标和优先事项。它涉及:

- 设定目标: 定义明确、可实现的目标。

- 分配收入: 将收入分配到支出、储蓄和投资中。

- 监控和修订: 随着情况的变化定期审查并调整预算。

5.7 Impact of External Factors:

税收、通货膨胀和个人变化(例如婚姻、子女)会显著影响预算需求和财务规划。

制定切合实际的个人或家庭预算:

- 确定收入来源: 计算所有来源的每月总收入。

- 列出并分类费用:将费用分为固定、变动和不定期类别。

- 分配资金用于储蓄:优先留出一部分收入作为储蓄和应急资金。

- 调整盈余或赤字: 如果支出超过收入,就寻找可以削减的领域。如果有盈余,就将额外的资金用于储蓄或偿还债务。

- 监督和审查: 定期根据实际支出检查您的预算,并根据需要进行调整以保持预算正常。

5.8 Interest and Fees in Money Management

了解与消费、借贷和储蓄相关的利率和费用至关重要。利息可以累积在储蓄上,增加财富,也可以累积在债务上,增加借款成本。

计算利息:

例如,年利率为 1.5% 的储蓄账户在一年内将产生 $150 的利息,而同一时期内,信用卡的未付余额为 $1,000,则将产生 $200 的利息。

通过掌握预算和费用管理的原则,个人可以自信地驾驭自己的财务旅程,做出促进稳定、增长和成就的明智决策。

税收变化

影响:税收增加(无论是所得税、财产税还是销售税)会直接减少个人或家庭的可支配收入。例如,如果所得税增加,税后净收入就会减少,用于支出和储蓄的资金就会减少。相反,减税可以增加可支配收入,为预算中的其他支出或储蓄提供更多空间。

示例:假设 Alex 的实际所得税率因税法变化而上升。结果,他的每月净收入减少。为了进行调整,Alex 可能需要减少可自由支配的支出或重新评估他的储蓄贡献以保持财务稳定。

通货膨胀

影响:通货膨胀会逐渐侵蚀购买力,这意味着用同样的钱可以买到更少的商品和服务。随着食品、住房和医疗保健等必需品价格上涨,人们可能会发现现有预算已无法满足需求。这就需要找到增加收入的方法或调整消费习惯以适应更高的生活成本。

示例:如果年通货膨胀率为 3%,而 Emily 的工资没有增加,她的生活费用将会增加,从而有效减少她的可支配收入。Emily 可能需要削减非必要支出、寻找其他收入来源或以不同的方式安排支出优先顺序,以管理增加的生活成本。

个人情况影响:结婚、离婚、生孩子、失业或继承遗产等生活事件会显著影响一个人的财务状况和预算。积极的变化可能会增加财务稳定性,而具有挑战性的事件可能需要收紧预算或重新分配资金以满足新的需求。

示例 1:孩子出生后,乔丹和泰勒发现他们现在的公寓太小了。搬到更大的地方会增加房租,因此他们必须调整预算以支付这笔必要的开支。

示例 2:莎拉升职,工资大幅增加。她决定增加退休储蓄供款,并为孩子设立大学基金,以反映其财务状况的改善。

适应变化为了适应税收、通货膨胀和个人情况的变化,个人可能需要:

- 定期审查和调整预算:保持预算灵活性以适应收入和支出的变化。

- 优先考虑支出:关注需求而不是欲望,尤其是在财务紧张的时候。

- 寻找增加收入的机会:探索副业、要求加薪或获取新技能以获得薪水更高的工作。

- 建立应急基金:提供财务缓冲来帮助应对意外的变化或挑战。

有效的预算和费用管理是实现财务稳定和实现长期目标的关键。理解和运用这些原则可让个人做出明智的消费决策并保持健康的财务生活方式。

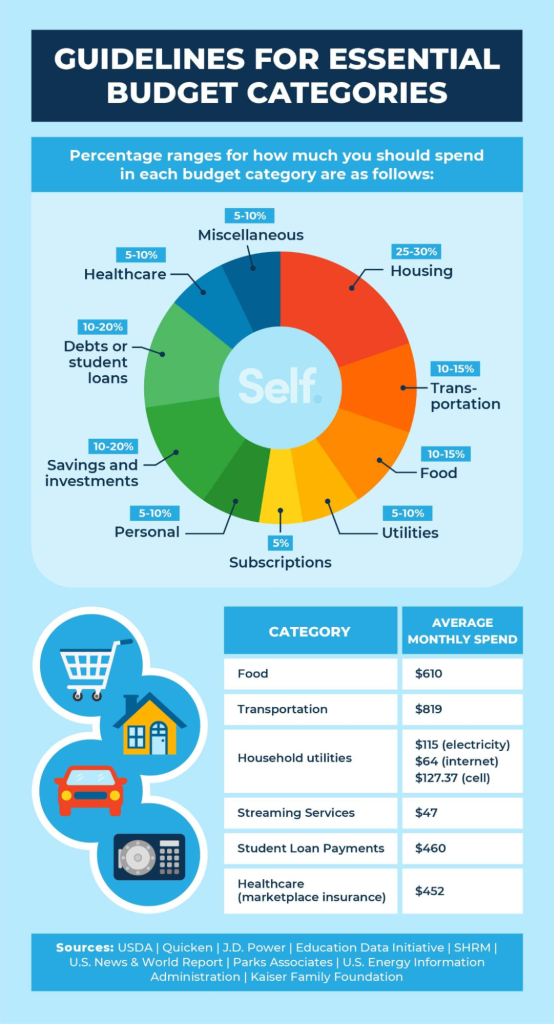

数字: 10 个基本预算类别

描述:

图中列出了个人在规划财务时应考虑的十个基本预算类别。这些类别涵盖了一系列支出和储蓄领域,可帮助个人有效分配资金。

要点:

- 抵押或租赁: 分配资金用于住房开支。

- 储蓄和投资: 留出一些钱用于未来的财务目标和财富积累。

- 债务或学生贷款: 偿还债务和教育贷款的计划。

- 运输: 通勤、车辆维护和其他交通相关费用的预算。

- 杂项开支: 分配资金用于不可预见或变化的开支。

- 订阅: 每月或每年订阅服务的预算。

信息应用:

对预算领域进行清晰的分类对于有效的财务规划至关重要。通过将支出和储蓄细分为特定类别,个人可以更好地了解自己的财务习惯,确定需要改进的领域并做出明智的决定。此分类是任何希望制定全面预算的人的基础指南,确保涵盖所有重要领域并实现财务目标。

Figure: Essential Budget Categories for Financial Planning

描述:

The image from Self.inc outlines ten essential budget categories that are critical for effective financial planning. These categories help individuals understand their spending patterns and manage their finances by allocating funds appropriately to areas such as housing, food, transportation, and healthcare.

要点:

- 住房通常会消耗约30%的收入,包括保险和税收等相关费用。

- 食品支出范围从收入的 10% 到 16%,根据家庭规模和饮食选择而有所不同。

- 交通费用(包括车辆费用和公共交通)理想情况下不应超过月收入的 15%。

- 通过节能措施和服务计划比较,水电费可以控制在收入的 5% 到 10% 之间。

- 建议医疗保健费用预算在 5% 至 10% 之间,同时考虑常规和潜在的意外医疗费用。

信息应用:

By categorizing expenses, individuals can create a structured budget that aligns with their income and financial goals. This approach allows for a clear understanding of where money is being spent and where adjustments can be made to save more or pay off debt. It’s particularly useful for those looking to gain control over their finances and work towards financial stability and independence.

5.9 Factors Influencing Consumer Decisions

Price and Product Comparison

When making a purchase, price is often one of the primary deciding factors. Consumers frequently compare prices for similar products before settling on a purchase. For example, when buying a new smartphone, a consumer may compare prices across various retailers or online platforms to ensure they’re getting the best deal.

- 优点:

- Helps the consumer save money by identifying the most affordable option.

- Encourages consumers to seek the best value for their purchase.

- Helps the consumer save money by identifying the most affordable option.

- 缺点:

- Price comparisons can be time-consuming, especially when there are many options available.

- Focusing too heavily on price may result in overlooking product quality and features.

- Price comparisons can be time-consuming, especially when there are many options available.

Brand and Reputation

Some consumers may have a preference for certain brands due to reputation, previous experiences, or trust in the brand’s quality. For example, someone may opt for an Apple iPhone over other phones due to its known brand reliability, even if it costs more than other smartphones.

- 优点:

- Offers peace of mind knowing that the product is from a trusted brand.

- Ensures a certain level of quality and performance based on brand reputation.

- Offers peace of mind knowing that the product is from a trusted brand.

- 缺点:

- Higher brand premiums may result in paying more than necessary for a product that may not offer significant added value.

- Brand loyalty may limit exploration of more affordable alternatives.

- Higher brand premiums may result in paying more than necessary for a product that may not offer significant added value.

Functionality and Features

The functionality and features of a product greatly influence consumer decisions. For example, when purchasing a laptop, a consumer may prioritize factors like screen size, battery life, or processing speed, depending on their needs (e.g., work or entertainment).

- 优点:

- Allows consumers to select products tailored to their needs.

- Increases satisfaction with the purchase when the product meets specific requirements.

- Allows consumers to select products tailored to their needs.

- 缺点:

- A focus on functionality may result in higher costs if consumers opt for more feature-packed versions.

- Sometimes, additional features may be unnecessary for the consumer’s intended use, leading to overpaying.

- A focus on functionality may result in higher costs if consumers opt for more feature-packed versions.

Process for Making Informed Consumer Decisions

Step 1: Identifying Needs vs. Wants

The first step in making an informed purchase is distinguishing between needs and wants. A need could be a basic necessity, such as a phone that can make calls and send messages, while a want could be a high-end model with additional features that aren’t necessary.

- 优点:

- Helps prevent unnecessary purchases and ensures that essential needs are met.

- Promotes smarter financial decisions by focusing on what’s truly needed.

- Helps prevent unnecessary purchases and ensures that essential needs are met.

- 缺点:

- The line between needs and wants can sometimes be subjective, leading to confusion or indecision.

- Restricting spending on wants may reduce immediate satisfaction.

- The line between needs and wants can sometimes be subjective, leading to confusion or indecision.

Step 2: Researching Options

Once needs are determined, consumers should research their options. This involves reading customer reviews, checking product comparisons, and looking into expert opinions.

- 优点:

- Ensures that consumers make an informed and educated decision.

- Provides insight into potential product flaws or advantages that may not be obvious at first glance.

- Ensures that consumers make an informed and educated decision.

- 缺点:

- Researching multiple products can be time-consuming and may cause decision fatigue.

- The abundance of information available can sometimes overwhelm the consumer, making it harder to make a decision.

- Researching multiple products can be time-consuming and may cause decision fatigue.

Step 3: Evaluating Price vs. Value

Before making a final decision, consumers should assess whether the price aligns with the value they are getting. This means considering factors like product quality, longevity, and after-sales service in addition to the initial price tag.

- 优点:

- Helps consumers balance cost with the quality and benefits of the product, ensuring better value for money.

- Encourages more thoughtful and deliberate purchasing, reducing impulse buying.

- Helps consumers balance cost with the quality and benefits of the product, ensuring better value for money.

- 缺点:

- Some products might appear overpriced based on initial cost but offer long-term value through durability or lower maintenance.

- Finding the right balance between price and value can be subjective and vary from person to person.

- Some products might appear overpriced based on initial cost but offer long-term value through durability or lower maintenance.

Positive and Negative Effects of Consumer Decisions

Example: Purchasing an Electric Vehicle (EV)

- Positive Environmental Impact:

- EVs contribute to lower carbon emissions compared to traditional gasoline-powered cars, helping reduce pollution and combating climate change.

- EVs contribute to lower carbon emissions compared to traditional gasoline-powered cars, helping reduce pollution and combating climate change.

- Positive Societal Impact:

- Purchasing an EV supports the growth of the green energy sector, promoting sustainable transportation options and supporting eco-friendly innovations.

- Purchasing an EV supports the growth of the green energy sector, promoting sustainable transportation options and supporting eco-friendly innovations.

- Negative Environmental Impact:

- The production of EV batteries requires mining materials like lithium, which can lead to environmental degradation and significant resource extraction.

- The production of EV batteries requires mining materials like lithium, which can lead to environmental degradation and significant resource extraction.

- Negative Economic Impact:

- EVs often come with a higher upfront cost compared to traditional vehicles, which may be a financial burden for some consumers, especially those on tighter budgets.

- EVs often come with a higher upfront cost compared to traditional vehicles, which may be a financial burden for some consumers, especially those on tighter budgets.

- 优点:

- Encourages sustainable choices and supports global initiatives for environmental protection.

- Helps consumers align their financial decisions with their personal values, like environmental consciousness.

- Encourages sustainable choices and supports global initiatives for environmental protection.

- 缺点:

- The upfront cost may not be accessible for all consumers, which can limit adoption.

- The environmental impact of battery production is a downside that many consumers may overlook.

- The upfront cost may not be accessible for all consumers, which can limit adoption.

Financial Responsibility and Budget Planning

Preparing for Life Events and Changing Budgets

Unexpected life changes, such as job loss, having a child, or a medical emergency, can significantly impact an individual’s budget. For example, after a job loss, a consumer may need to adjust their budget by cutting back on discretionary spending and prioritizing essential expenses.

- 优点:

- Having a flexible budget ensures financial stability during uncertain times.

- Helps individuals stay on track with financial goals even when life events cause disruptions.

- Having a flexible budget ensures financial stability during uncertain times.

- 缺点:

- Regularly revising budgets due to unexpected events can be time-consuming and overwhelming.

- It may require sacrifices in other areas, such as entertainment or personal spending.

- Regularly revising budgets due to unexpected events can be time-consuming and overwhelming.

Factors Affecting Financial Goals

External factors such as location, culture, 和 peer influences can significantly impact one’s financial goals. For example, someone living in a high-cost area may need a larger budget for housing and transportation compared to someone living in a lower-cost area.

- 优点:

- Understanding these external influences helps individuals recognize patterns in their financial behavior and spending.

- Encourages self-awareness, enabling consumers to make more informed financial decisions.

- Understanding these external influences helps individuals recognize patterns in their financial behavior and spending.

- 缺点:

- Overcoming the influence of peer pressure or cultural expectations can be challenging.

- These external factors may lead to unsustainable financial choices if not carefully managed.

- Overcoming the influence of peer pressure or cultural expectations can be challenging.

Techniques to Decrease Expenses

Comparison Shopping

Comparison shopping helps consumers find the best prices for products by comparing different stores and online retailers. For example, when buying a laptop, a consumer might use comparison websites to see if the item is cheaper elsewhere.

- 优点:

- Can lead to substantial savings by identifying the best prices.

- Provides a broader view of available options, ensuring that the consumer gets the best deal.

- Can lead to substantial savings by identifying the best prices.

- 缺点:

- Time-consuming, especially when comparing many different options.

- The lowest price may not always correspond with the best quality or service.

- Time-consuming, especially when comparing many different options.

Negotiating Prices

Negotiating the price of large purchases (e.g., cars, furniture) or even monthly bills (e.g., cable, insurance) can lead to significant savings. For instance, a consumer might negotiate a lower rate on their cable bill by threatening to cancel the service.

- 优点:

- Provides an opportunity to lower the overall cost of big-ticket items or services.

- Can build confidence in consumers when dealing with sales representatives.

- Provides an opportunity to lower the overall cost of big-ticket items or services.

- 缺点:

- Not all merchants are open to negotiation, and it may feel uncomfortable for some consumers.

- It can be difficult to know when negotiation is appropriate, and sometimes it may not be effective.

- Not all merchants are open to negotiation, and it may feel uncomfortable for some consumers.

Using Technology for Financial Management

Financial Management Tools

There are various digital tools and apps that help track and manage spending, such as Mint, YNAB, 和 mobile banking apps. These tools can automatically categorize expenses, track income, and help users stick to their budget.

- 优点:

- Real-time tracking and budgeting make it easier to stay on top of finances.

- Automates savings and bill payments, making it easier for consumers to manage their money.

- Real-time tracking and budgeting make it easier to stay on top of finances.

- 缺点:

- Some apps or tools may require subscriptions or fees, which may eat into savings.

- Technical issues or security concerns with apps could compromise financial data

Conclusion: Mastering Budgeting and Expense Management

Budgeting and managing expenses are the foundations of personal financial success. Throughout this chapter, we explored how creating and maintaining a thoughtful budget empowers individuals to take control of their money, plan for both expected and unexpected life events, and align their spending habits with their long-term goals. Whether choosing a structured method like the 50/30/20 rule, tracking expenses through modern apps, or adapting to life’s inevitable changes, the tools and strategies discussed offer a path toward financial stability and growth.

Effective budgeting is not just about restriction; it’s about making intentional choices that reflect your values and aspirations. Understanding the difference between needs and wants, making informed consumer decisions, adjusting to economic shifts like inflation or tax changes, and regularly revisiting your budget ensures that your financial plan remains a living, flexible guide.

By practicing disciplined budgeting, making mindful purchasing decisions, and proactively managing necessary and discretionary expenses, individuals can not only meet their financial obligations but also build security, achieve personal goals, and enjoy greater peace of mind. Ultimately, mastering budgeting and expense management is not just a financial skill—it’s a key to building a life of opportunity, resilience, and freedom.

主要课程信息:

Lorem ipsum dolor sit amet,consectetur adipiscing elit。 Ut elit tellus,luctus nec ullamcorper mattis,pulvinar dapibus leo。