Global: Key Considerations for Retirement Planning

Στόχοι Μαθήματος:

Εισαγωγή: This section explores key aspects of retirement planning, including estimating expenses, understanding public and private pension options, and utilizing home equity as a financial resource. By understanding these factors, users can create a comprehensive retirement plan that aligns with their lifestyle goals and financial needs.

- Estimate retirement expenses effectively by considering living costs, healthcare needs, and lifestyle choices. This will help users determine the income needed for a comfortable retirement, helping them set realistic savings goals.

- Understand the roles of public and private pensions in retirement planning. You will learn how these two types of pensions can work together to create a reliable income stream, ensuring long-term financial stability.

- Explore ways to leverage home equity, such as downsizing, reverse mortgages, or renting out part of the property. These strategies can offer additional income during retirement while allowing users to maintain their lifestyle.

- Make informed decisions about pension withdrawal options, considering annuities, lump sums, or phased withdrawals. Understanding the pros and cons of each option will help users plan how to manage their savings throughout retirement.

A. Retirement Needs

Planning for retirement requires a clear understanding of individual retirement needs, which can vary depending on lifestyle, health, family circumstances, and financial goals. Retirement needs encompass everything from covering basic living expenses to funding healthcare, travel, and leisure. It’s crucial to estimate how much income will be required during retirement, keeping in mind πληθωρισμός, changes in health, and potential unforeseen expenses.

- Estimating Retirement Expenses: A common rule of thumb is that retirees will need around 70-80% of their pre-retirement income to maintain their standard of living. However, this can vary based on personal goals. For instance, those planning an active retirement with travel or expensive hobbies may need more, while those with minimal lifestyle changes may need less.

- Healthcare Costs: One of the biggest uncertainties in retirement is healthcare. In some countries, retirees may have access to public healthcare, while others may need to budget for private insurance or out-of-pocket costs. Long-term care, such as nursing homes or home care services, should also be factored in.

Example: In the United States, retirees must consider the costs of Medicare, which provides healthcare for those aged 65 and over but often requires supplemental coverage for additional services like prescriptions.

Figure: 5 Steps to Create a Retirement Budget

Περιγραφή:

The figure illustrates five essential steps to create a retirement budget. It begins with making a list of expected monthly expenses, categorizing them as fixed, variable, or one-time. The second step involves estimating retirement income from various sources like Social Security, pensions, and investments. Next, it advises comparing expected expenses with expected income to identify if adjustments are needed. The fourth step emphasizes contributing regularly to a retirement account to take advantage of compounding. Finally, the last step involves setting a realistic timeline for retirement based on a savings formula.

Βασικά συμπεράσματα:

- Identify and organize expenses to create a clear view of what to expect in retirement.

- Estimate income from various sources to understand how much you will have available each month.

- Compare income to expenses and make adjustments if necessary by reducing costs or increasing savings.

- Contribute regularly to retirement accounts early to benefit from compound interest.

- Plan your retirement timeline based on your financial goals and projected savings.

Εφαρμογή πληροφοριών:

Creating a retirement budget helps individuals plan their finances effectively by knowing their future income and expenses. It allows them to make τεκμηριωμένες αποφάσεις about saving, investing, and adjusting their lifestyle for a more secure retirement. This step-by-step approach can guide users in achieving long-term financial stability.

Β. Δημόσιες και Ιδιωτικές Συντάξεις

Retirement income often comes from a combination of public pensions, private pensions, and personal savings. Understanding the difference between these sources is critical for creating a balanced and sustainable retirement plan.

- Public Pensions: Public pensions (also known as state pensions) are provided by the government and are usually funded through mandatory contributions made during one’s working life. The size of the pension typically depends on how long an individual has contributed to the system and their average earnings. Public pensions are designed to provide a baseline income in retirement, but in many cases, they are not sufficient to cover all expenses.

- Παράδειγμα: In Καναδάς, retirees receive a Canada Pension Plan (CPP) payment, which is based on their contributions during their working life. In the UK, retirees receive a state pension, which is also determined by contributions and years of work.

- Global Example: Many countries in Europe, like Γερμανία και Γαλλία, offer robust public pension systems where workers contribute a percentage of their income, but these systems often require supplemental private savings to meet full retirement needs.

- Παράδειγμα: In Καναδάς, retirees receive a Canada Pension Plan (CPP) payment, which is based on their contributions during their working life. In the UK, retirees receive a state pension, which is also determined by contributions and years of work.

- Private Pensions: Private pensions are typically offered through employers (as occupational pensions) or set up individually. These plans allow individuals to save money throughout their working life, with many employers offering matching contributions as an incentive to save. In contrast to public pensions, private pensions offer more flexibility and higher income potential, depending on how well the investments perform.

- Defined Contribution (DC) Plans: In DC plans, individuals and sometimes their employers make regular contributions to a retirement fund that is invested in financial markets. The retirement income from these plans depends on the value of the investments at retirement.

- Defined Benefit (DB) Plans: In DB plans, employees are promised a specific monthly payout during retirement based on factors like their salary and years of service. These plans are less common today but provide a stable and predictable income stream.

- Παράδειγμα: In the U.S., 401(k) plans are a popular defined contribution retirement savings option, while defined benefit pension plans, like those in the public sector, are becoming rarer in many countries.

- Defined Contribution (DC) Plans: In DC plans, individuals and sometimes their employers make regular contributions to a retirement fund that is invested in financial markets. The retirement income from these plans depends on the value of the investments at retirement.

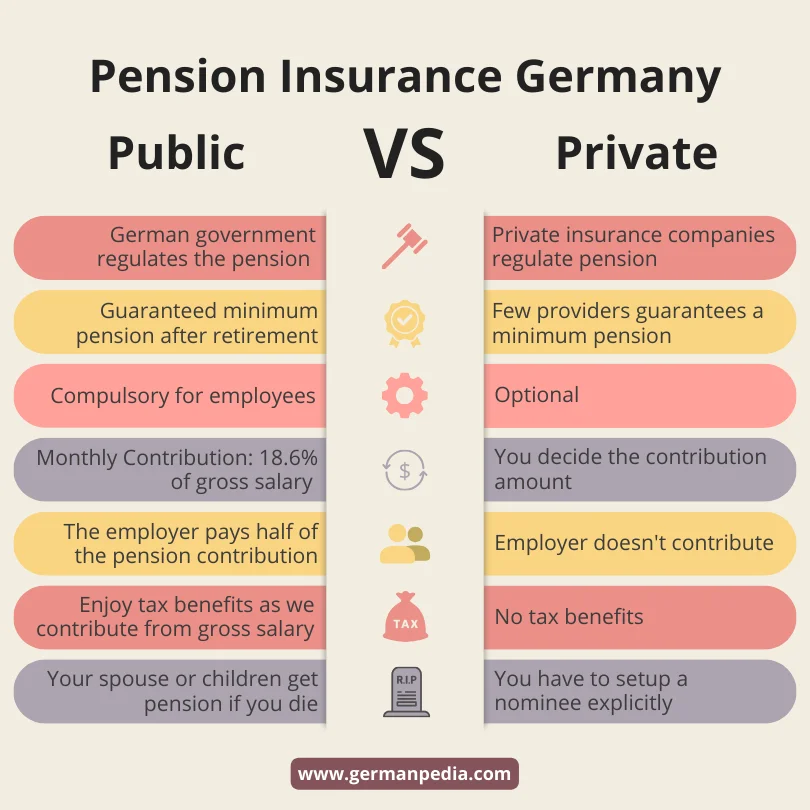

Figure: Pension Insurance Germany: Public vs Private

Περιγραφή:

The figure compares public and private pension insurance systems in Germany. Public pensions are regulated by the government, provide a guaranteed minimum pension, and are compulsory for employees. Employers share the contribution cost, and the contributions are tax-advantaged. In contrast, private pensions are managed by private companies, with contributions being optional, decided by the individual, and lacking tax benefits. Unlike public pensions, employers do not contribute to private pensions, and beneficiaries need to set up a nominee explicitly.

Βασικά συμπεράσματα:

- Public pensions are mandatory for employees and managed by the government, ensuring a guaranteed minimum pension.

- Private pensions offer flexibility in contribution amounts but come without the employer’s financial support.

- Tax benefits are available for public pensions, making them more cost-effective for contributors.

- Private pensions require users to set up nominees explicitly, unlike public systems where family members may receive benefits automatically.

Εφαρμογή πληροφοριών:

Understanding the differences between public and private pension systems can help individuals decide the best option for their retirement planning. Public pensions offer security and tax benefits, while private pensions provide flexibility and personalized contributions. Investors should consider their long-term goals, tax situation, and contribution preferences when selecting a pension plan.

C. Leveraging Home Equity

For many retirees, their home is one of their most significant financial assets. Leveraging home equity can be an effective way to supplement retirement income, especially for those who have paid off their mortgage or own valuable property.

- Downsizing: One of the simplest ways to access home equity is by downsizing—selling a larger home and moving into a smaller, less expensive one. This can free up capital to be used for retirement expenses while reducing ongoing costs like property taxes and maintenance.

- Reverse Mortgages: A reverse mortgage is another option for retirees to unlock the value of their home without having to sell it. In a reverse mortgage, the homeowner receives a loan against the value of the home, which is repaid when the home is sold or after the homeowner passes away. This allows retirees to use the equity in their home as a source of income while continuing to live in it.

- Παράδειγμα: In the United States, Home Equity Conversion Mortgages (HECMs) are a popular type of reverse mortgage available to those aged 62 and older.

- Παράδειγμα: In the United States, Home Equity Conversion Mortgages (HECMs) are a popular type of reverse mortgage available to those aged 62 and older.

- Renting Out Part of the Home: For those who prefer to stay in their home, renting out a portion of the property, such as a basement apartment or spare room, can generate additional income. This approach allows homeowners to stay in a familiar place while offsetting living costs.

- Equity Release Schemes: In some countries, equity release schemes offer retirees the chance to sell part or all of their home while continuing to live in it. These schemes provide a lump sum or regular payments in exchange for ownership of the home upon the retiree’s death or relocation.

- Global Example: In Αυστραλία, reverse mortgages και equity release schemes have become increasingly popular as more retirees seek to use their property to supplement income without having to sell it outright.

- Global Example: In Αυστραλία, reverse mortgages και equity release schemes have become increasingly popular as more retirees seek to use their property to supplement income without having to sell it outright.

Figure: Different Ways to Leverage Equity to Improve Your Mortgage Allocations

Περιγραφή:

The image illustrates five methods to utilize home equity to enhance mortgage management. These options include refinancing the mortgage, obtaining a home equity loan, using a home equity line of credit (HELOC), opting for a cash-out refinance, and selling the property to downsize. Each method offers unique benefits depending on individual financial goals and situations.

Βασικά συμπεράσματα:

- Refinancing your mortgage can help lower monthly payments or reduce the loan term.

- Home equity loans provide a lump sum for significant expenses, using home equity as collateral.

- HELOCs (Home Equity Lines of Credit) offer flexible borrowing, similar to a credit card, based on home equity.

- Cash-out refinancing allows homeowners to take out more than the mortgage balance, with the difference paid in cash.

- Selling and downsizing can free up equity, reducing mortgage obligations and living expenses.

Εφαρμογή πληροφοριών:

Leveraging equity can help homeowners manage debt, finance home improvements, or invest in other opportunities. Understanding these options allows individuals to make informed financial decisions based on their current needs and future plans. Each strategy has specific benefits, helping users utilize home equity effectively.

Βασικές πληροφορίες μαθήματος:

- Estimating retirement expenses involves planning for both expected and unexpected costs, such as healthcare and lifestyle changes. Knowing how much income will be needed helps users set savings targets and create a realistic budget for retirement.

- Public pensions provide a basic level of income, but they may not be enough to cover all retirement needs. Private pensions offer more flexibility and can supplement public benefits, making it easier to maintain your desired standard of living.

- Leveraging home equity through methods like downsizing or reverse mortgages can provide extra income during retirement. These options allow retirees to use the value of their home to support their lifestyle without selling the property outright.

- Choosing the right pension withdrawal method is crucial for ensuring that savings last throughout retirement. Annuities offer stable income, while lump-sum withdrawals provide immediate access to funds. Users should select the option that best fits their financial needs and risk tolerance.

- Integrating sustainable investment options into pension plans can align financial goals with ethical values. Understanding Environmental, Social, and Governance (ESG) factors allows retirees to invest in socially responsible funds while still aiming for financial growth.

Τελική δήλωση: Effective retirement planning combines careful expense estimation, diverse income sources, and strategic use of assets like home equity. By understanding these key aspects, individuals can achieve a more secure, fulfilling, and sustainable retirement.