第8章 信用管理とその影響

レッスンの学習目標:

Lorem ipsum dolor sit amet、consectetur adipiscing elit。ウト・エリート・テルス、ルクトゥス・ネク・ウラムコーペル・マティス、プルヴィナー・ダピブス・レオ。

信用管理入門

効果的なクレジット管理には、利用可能なさまざまなタイプのクレジットを理解し、クレジット コストを比較し、クレジット決定が個人の財務に与える影響を認識することが含まれます。この章では、不正確な請求明細の特定、クレジット コストの比較、クレジットの使用の影響など、クレジット管理の複雑さについて説明します。

8.1 Identifying and Contesting Incorrect Billing Statements

消費者は請求書に不正確な点がないか注意深く確認する必要があります。 請求明細書に誤りがあることに気づいた場合、消費者はまず請求会社に連絡して解決を図る必要があります。満足できない場合は、消費者保護団体などの消費者擁護機関に苦情を申し立てることができます。 ベタービジネスビューロー(BBB)、商工会議所、フロリダ州農業消費者サービス局、連邦取引委員会(FTC). これらの組織は調停サービスを提供し、必要に応じてさらなる法的措置に関する指導も提供します。

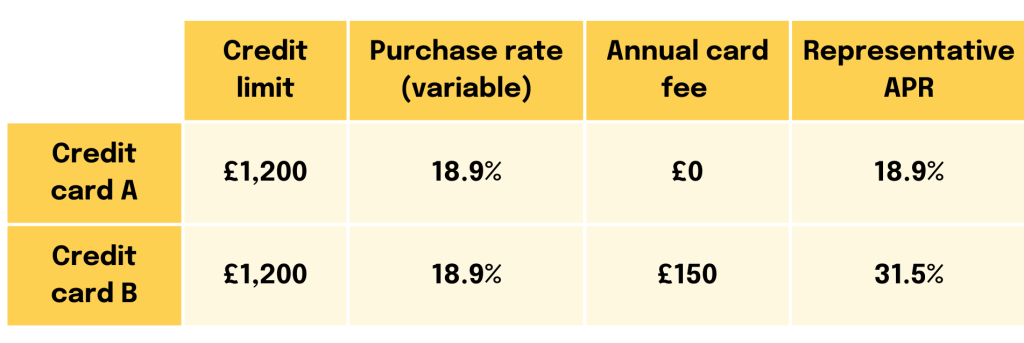

8.2 Comparing Credit Costs

の 年率(APR) そして 初期費用、延滞料、未払い手数料は、信用コストを比較する際に重要な要素です。APRは、金利やその他の手数料を含む借入コストを包括的に示し、消費者がさまざまな信用ソースを効果的に比較できるようにします。たとえば、クレジットカード A はクレジットカード B に比べて APR は低いものの延滞料金が高く、ユーザーの習慣に応じて全体的なクレジット コストに影響を与える可能性があります。

低金利でのクレジット

金融機関は新規顧客を獲得するために低い導入金利を提供する場合があります。魅力的ではありますが、 これらの利率は導入期間後に大幅に上昇する可能性があり、利率が上昇する前に残高を返済できない消費者にとってはコストの上昇につながる可能性があります。

形: The Difference Between Interest Rate and APR

説明:

This graphic illustrates the important distinction between a loan’s 金利 and its 年率(APR). It visually explains that the interest rate is just one part of the borrowing cost, while the APR represents the total cost. The image shows that the APR is a broader measure because it includes both the interest rate and any additional lender fees.

重要なポイント:

- の 金利 is the direct cost of borrowing the money and is calculated as a percentage of the principal only.

- の 年率(APR) provides a more complete picture of a loan’s cost, as it includes the interest rate plus any associated fees, such as origination fees or closing costs.

- Because it includes extra fees, a loan’s APR is typically higher than its advertised interest rate.

- When comparing different loan offers, looking at the 4月 allows for a more accurate, “apples-to-apples” comparison of the true cost of each option.

情報の応用:

- When you are shopping for a loan, such as a mortgage or car loan, you should always compare the 4月 offered by different lenders, not just the interest rate.

- Focusing on the APR helps you understand the 借入総費用 and avoid loans that may have a low interest rate but high hidden fees.

- This knowledge is essential for making an informed financial decision and selecting the most affordable loan, potentially saving you a significant amount of money over time.

8.3 Secured vs. Unsecured Loans and credit cards

保護された ローンには担保が必要で、一般的には自動車ローンや住宅ローンなどの貸し手のリスクが低いため金利が低くなりますが、支払いが行われない場合には資産を失うリスクがあります。対照的に、 無担保ローン、 ほとんどのクレジットカードと同様に、担保は必要ありませんが、金利は高くなります。

担保付きクレジットカード 必要 現金預金 担保として機能するため、貸し手にとってはリスクの低い選択肢となり、信用を構築または再構築したい消費者にとっては貴重なツールとなります。 無担保クレジットカード 頭金は必要ありませんが、資格については消費者の信用履歴に依存することがよくあります。

8.4 Factors Influencing Borrowing Costs

頭金 融資総額が減るため、月々の支払額が減ったり、融資期間が短くなったりします。頭金が多額な借り手は貸し手にとってリスクが少なくなり、融資条件がより有利になることがよくあります。

クレジットカード:コストとメリット

クレジットカード 利便性はありますが、特にクレジット スコアが低いユーザーにとっては、金利や手数料が高くなる場合があります。即時購入が可能になりますが、慎重に管理しないと、金利や手数料による長期的なコストがメリットを上回る可能性があります。

クレジットカード 猶予期間, 利息計算 方法、および 関連手数料 借入コストに直接影響します。猶予期間により、借り手は利息を支払わずに残高を返済できるため、賢く利用すれば大きなメリットが得られます。

8.5 Consumer Protection Laws

法律としては、 貸金業法(TILA) そしてその クレジットカード法 貸し手が信用条件を明確に開示し、消費者を不公正な慣行から保護することを確実にする。 貸付法では、貸し手に対して信用条件の完全な開示を義務付けており、差別的貸付、不当なマーケティング、不公平な債権回収慣行から消費者を保護しています。 消費者は、十分な情報に基づいた決定を下すために、クレジットを申請する際にはこれらの開示内容を徹底的に検討する必要があります。

詐欺の防止と対処

詐欺から身を守るために、消費者は定期的に自分の口座を監視し、オンライン バンキングには安全な方法を使用し、疑わしい行為があればすぐに報告する必要があります。詐欺の場合には、金融機関と関係当局に速やかに連絡することが重要です。

8.6 Free Annual Credit Reports

Equifax、Experian、TransUnion などの組織によって管理されている信用レポートは、信用力の評価において重要な役割を果たします。信用スコアに影響を与える要因には、支払い履歴、信用利用、信用履歴の長さなどがあります。信用レポートを定期的に確認し、不正確な点を異議申し立てすることが、健全な信用スコアを維持する鍵となります。

消費者は、主要な信用調査機関から毎年 1 通の無料信用レポートを受け取る権利があります。信用レポートを定期的に確認すると、借入コストや信用取得能力に影響する可能性のあるエラーを特定するのに役立ちます。

8.7 Student Loans Comparison

PLUS ローン、民間学生ローン、直接補助ローンまたは無補助ローンなど、さまざまな種類の学生ローンを比較することは、延期期間中に発生する利息などの長期的なコストを理解する上で非常に重要です。

さまざまな学生ローンの微妙な違いを理解することは、教育資金の戦略に大きな影響を与える可能性があります。さまざまな種類の学生ローンの利子発生ポリシーと資格基準の詳細は次のとおりです。

直接補助ローン

- 利息の発生: 米国教育省は、学生が少なくとも半日制で学校に通っている間、学校を卒業してから最初の 6 か月間 (猶予期間)、および延期期間中に利子を支払います。

- 資格: 経済的必要性が証明された学部生が対象.

直接無補助ローン

- 利息の発生: 利子は、学生にローンが支払われた時点から発生します。学生はすべての利子を支払う責任がありますが、在学中に利子の支払いを延期することもできます。延期された利子は資本化され、ローンの元金に加算されます。

- 資格: 学部生、大学院生、専門学生が対象で、経済的必要性を証明する必要はありません。

学部学生向け親ローン(PLUS)ローン

- 利息の発生: 利息は支払い後すぐに発生します。補助金はなく、借り手がすべての利息の支払いを負担します。

- 資格: 扶養されている学部生の親、大学院生、専門学生も対象です。資格は経済的必要性に基づいていませんが、信用調査が必要です。信用履歴が悪い借り手には保証人が必要になる場合があります。

民間学生ローン

- 利息の発生: Policies vary by lender, but typically, interest starts accruing immediately upon disbursement. Some private loans offer deferment options where interest continues to accrue but payments are not required until later.

- 資格: Determined by the private lender, usually based on creditworthiness. Students often need a cosigner with good credit to qualify for the best interest rates.

重要な考慮事項:

- 利息の発生と資本化: 利子がどのように発生し、いつ元金に加算されるか(ローンの元金残高に加算されるか)を理解することは、借入の長期コストを管理する上で重要です。補助金付きの連邦ローンは、学生が在学している間は利子が発生しないという利点があり、大幅な節約につながります。

- 資格要件: 連邦ローンの場合、資格を判断するために連邦学生援助無料申請書 (FAFSA) を完了することが一般的に必要です。民間ローンの場合は独自の申請手続きがあり、収入証明、信用調査、場合によっては共同署名者が必要になることがあります。

- 適切なローンの選択: 元金と利息、および借入に関連する手数料を含むローンの総費用を考慮してください。連邦ローンには、固定金利や所得連動型返済プランや返済免除プログラムへのアクセスなどのメリットがありますが、これらは民間ローンでは通常利用できません。

Navigating student loans requires careful consideration of both immediate needs and future financial implications, making an understanding of each type of loan’s specifics essential for sound financial planning in pursuit of education.

8.8 Deferred Student Loan Payment

学生ローンの延払いは、経済的困難、進学、失業などの特定の状況下で借り手が返済を延期できる機能であり、即時の救済と長期的な経済的影響の両方をもたらす可能性があります。学生ローンの支払いを延ばすことで起こり得る結果は次のとおりです。

Figure: Student Loan Deferment vs. Forbearance

説明:

This image compares two common options for temporarily pausing student loan payments: deferment そして forbearance. It visually breaks down the key differences between these two programs, with a strong focus on how the 興味 that accumulates on the loan is handled. The goal is to help borrowers understand the financial implications of each choice before deciding.

重要なポイント:

- Both deferment そして forbearance are official ways to pause your student loan payments if you are facing financial difficulty.

- The most important difference is in how accrued interest is treated. With deferment on certain types of federal loans (subsidized loans), the government may pay the interest for you.

- With forbearance, you are always responsible for paying the interest that accrues during the pause, regardless of your loan type.

- This unpaid interest is often capitalized at the end of the forbearance period, meaning it is added to your principal loan balance, increasing the total amount you will have to repay.

情報の応用:

- If you are unable to make your student loan payments, it is critical to understand these options to choose the least costly one for your situation.

- You should always check if you qualify for deferment first, as it can save you a significant amount of money in interest payments.

- While pausing payments offers short-term relief, it’s vital to understand the long-term cost, as capitalized interest from forbearance can make your loan more expensive over time.

短期的な利益

- 即時の経済的救済: 支払いを延期することで、一時的な経済的困難に直面している個人に重要な余裕が生まれ、住宅費、食費、医療費などの当面のニーズにリソースを割り当てることが可能になります。

- 債務不履行の回避: ローンの支払いを正式に延期することで、借り手はローンの債務不履行を回避し、信用スコアを維持し、ローンの債務不履行に伴う厳しい罰則を回避することができます。

長期的な影響

- 利息の発生: ほとんどの種類の学生ローンでは、返済が行われていなくても、延期期間中は利息が発生し続けます。つまり、借入総額が増加し、借り手はローンの期間中により多くの金額を支払うことになります。

- 返済期間の延長: 支払いを延期すると、ローンの返済にかかる時間が長くなり、借り手の長期的な財務目標に影響を与え、住宅の購入や退職後の貯蓄などの重要な目標が遅れる可能性があります。

- 借入総コストの増加: 猶予期間中に累積した利息は、無補助ローンの元本残高に加算され、ローンの期間中の返済総額が大幅に増加する可能性があります。

- 免除プログラムの資格への影響: 公的サービスローン免除 (PSLF) などのプログラムを通じてローン免除を目指している借り手の場合、延期期間は適格な支払いにカウントされず、免除までの時間が延長される可能性があります。

シナリオ例

アレックスは、金利が 5% の連邦学生ローンを $30,000 借りています。彼は経済的困難のため、ローンを 1 年間延期することにしました。この 1 年間、彼のローンには $1,500 ($30,000 の 5%) の利息が発生します。これは、彼が無利子ローンを返済している場合、彼の元本残高に加算されます。彼が返済を再開すると、彼の新しい残高は $31,500 となり、この高い金額に対して利息を支払うことになり、ローンのコストが増加します。

8.9 Strategies to Mitigate Negative Consequences

- 利息の支払い: 可能であれば、延期中に利息を支払うことで、利息が元本に加算されるのを防ぎ、ローン残高の増加を抑えることができます。

- より短い延期期間: 必要な期間のみ延期を利用すると、時間の経過とともに利息が発生するため、財務上の影響を最小限に抑えることができます。

- 代替返済プランの検討: 所得連動型返済プランでは、延期する必要なく月々の支払額が低くなり、20~25年後にローンの返済が免除される可能性があります。

学生ローンの支払いを延期することは、経済的困難を管理するための有用な短期戦略となり得ますが、借り手は全体的な財務状況への長期的な影響を考慮し、それに応じて計画を立てることが不可欠です。

8.10 Credit Influence on Mortgage Rates and Payments

住宅ローンなどの担保付きローンは、通常、無担保ローンよりも金利が低くなります。 住宅ローンの支払いは、ローン金額、金利、返済期間によって影響を受けます。 変動金利住宅ローン(ARM) 当初の金利は低くなるかもしれませんが、金利が上昇すると将来の支払額が増加する可能性があります。 固定金利住宅ローン 一定の金利で安定性を提供します。 最も手頃なオプションを見つけるには、ローンの条件、金額、金利に基づいて住宅ローンのオプションを比較することが不可欠です。

8.11 Credit Reports and Scores

信用レポートとスコアを通じて評価される信用力は、借入コストに大きな影響を与えます。家主、雇用主、保険会社も意思決定プロセスでこの情報を使用します。良好な信用履歴を維持することは、財務の健全性にとって非常に重要です。

8.12 Alternative Financial Services

ペイデイローンや類似のサービスは、すぐに資金を調達できるものの、コストが高くなります。こうしたサービスがもたらす負債のサイクルなど、こうしたサービスの影響を理解することは、金融リテラシーにとって非常に重要です。

ペイデイローンと銀行ローン

ペイデイローンと銀行ローンの違いは、条件と費用にあります。ペイデイローンは通常、金利と手数料がはるかに高く、銀行ローンと比較して同じ借入額に対する返済額が大きくなります。

ペイデイローンの例:

ジョンが緊急の自動車修理のために $500 を必要としているとします。彼はペイデイ ローン業者に頼り、$500 を即座に借り入れます。条件は 2 週間以内に $75 のサービス料金を支払って返済することです。年率 (APR) で計算すると、このローンの利子は 390% を超えます。ジョンが 2 週間以内にローンを返済できない場合、別のペイデイ ローンを借りる必要があるかもしれません。その場合、追加料金が発生し、借金のサイクルに陥る可能性があります。

銀行ローンの例:

一方、サラが同様の緊急事態で $500 を必要とする場合、口座を持っている銀行から個人ローンを選択するかもしれません。銀行は、1 年間の返済期間で APR 10% (2023 年 4 月の最終更新時点での個人ローンの高値) のローンを彼女に提供します。1 年間で、彼女は約 $27.29 の利息を支払うことになりますが、これはペイデイローンのコストよりも大幅に低い金額です。

比較分析:

- 金利と手数料: ペイデイローンの APR は、銀行ローンに比べて非常に高くなります。この例では、ペイデイローンの APR が高金利の個人向け銀行ローンのほぼ 10 倍になる可能性があることを示しています。

- 返済期間: ペイデイローンの返済期間は通常非常に短く(通常 2 週間)、一方、銀行ローンの返済期間はより長いため、毎月の支払いがより管理しやすくなります。

- 借金のサイクル: ペイデイローンは、コストが高く、返済期間が短いため、借金の悪循環に陥ることがあります。期限内に返済できない借り手は、追加のローンを借りて、さらに手数料を負担することになり、借金の悪循環に陥るおそれがあります。

- 信用への影響: 通常の銀行ローンは、期日通りに返済すれば信用調査機関に報告されるため、信用を築くのに役立ちます。対照的に、ペイデイローンは、ローンが回収されない限り、信用調査機関に必ずしも報告されないため、通常は信用を築きません。

この比較から、ペイデイローンは緊急の財政難に対する即効薬のように思えるかもしれませんが、より扱いやすい条件と低い金利を提供する従来の銀行ローンよりもはるかに高いコストがかかることが多いことがわかります。借り手は、ペイデイローンを選択する前に、すべての代替案を検討し、条件と潜在的な長期的影響を理解する必要があります。

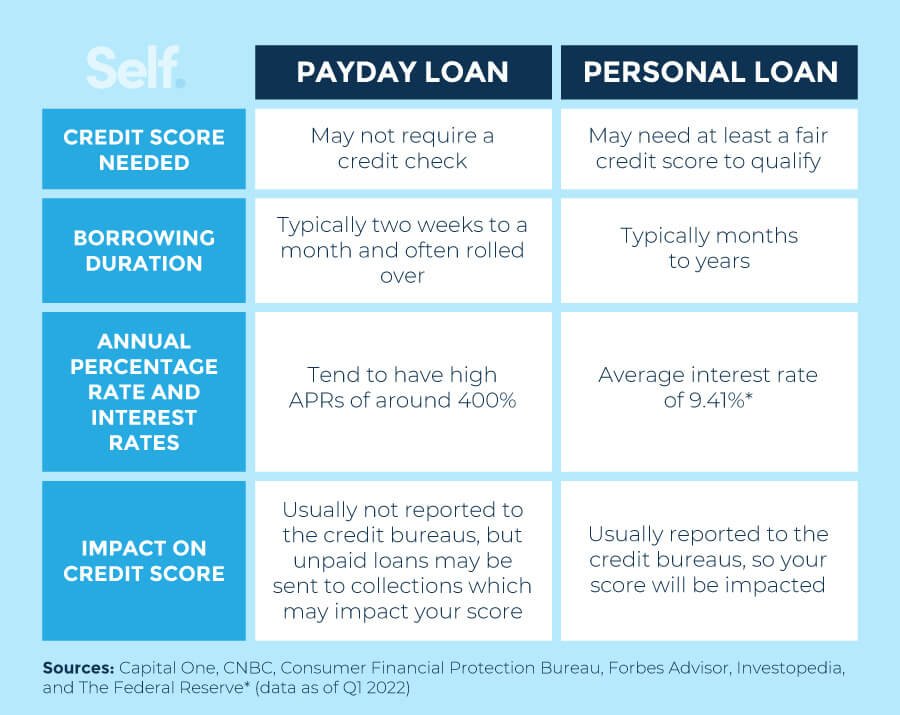

Figure: Payday Loans vs. Personal Loans

説明:

This image provides a side-by-side comparison of payday loans そして personal loans, highlighting the critical differences between these two ways of borrowing money. It focuses on key features such as interest rates, loan amounts, and repayment terms to illustrate their respective costs and benefits. The graphic is designed to help individuals understand which option is safer and more affordable for their financial needs.

重要なポイント:

- The most significant difference is the cost: Payday loans are known for having extremely high APRs (Annual Percentage Rates), often 300% or more, while personal loans offer much lower and more manageable interest rates.

- Repayment schedules are very different. Payday loans require full repayment in a very short term (usually by your next payday), whereas personal loans are repaid in predictable monthly installments over several months or years.

- Loan amounts vary significantly. Payday loans are for small, short-term needs (typically under $500), while personal loans can provide access to much larger sums of money.

- While payday loans are often easier to obtain for those with poor credit, personal loans from reputable lenders are a much more structured and less risky form of credit.

情報の応用:

- This comparison clearly shows that payday loans should be avoided whenever possible, as their high costs can quickly lead to a dangerous debt cycle.

- If you need to borrow money, a personal loan from a bank or credit union is almost always a more responsible and cost-effective financial decision.

- Understanding the true cost of debt, particularly the 4月, is a critical skill for making smart borrowing choices and protecting your long-term financial health.

8.13 Barriers to Being Banked

銀行を利用することに対する障壁、つまり個人が従来の銀行サービスを利用しない理由は多面的であり、財務状況や金融機会へのアクセスに重大な影響を及ぼす可能性があります。主な障壁とそれぞれの詳細は次のとおりです。

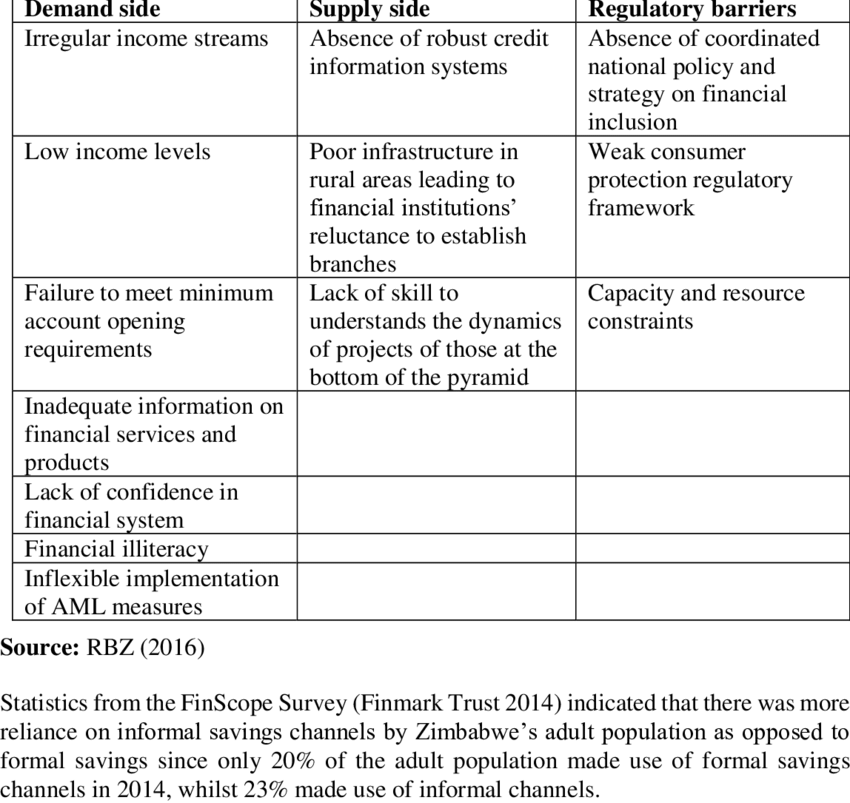

形: Major Barriers to Financial Inclusion in Zimbabwe

説明:

This table, from a formal research publication, lists the key obstacles that prevent people across Zimbabwe from accessing and using formal financial services. The figure categorizes these challenges, highlighting issues such as high transaction costs, lack of trust in the banking system, and low levels of financial literacy. It provides a structured overview of why achieving full financial inclusion remains difficult.

重要なポイント:

- Financial inclusion faces multiple complex barriers, ranging from economic to social and educational issues.

- High service costs and bank fees are a primary obstacle, making financial services unaffordable for many low-income individuals.

- A significant portion of the population may lack the formal documentation, such as a national ID or proof of income, required to open a bank account.

- Low levels of financial literacy (a lack of understanding of financial products) and a general distrust in financial institutions are also major hindrances.

情報の応用:

- Understanding these barriers is essential for anyone interested in finance or investing in emerging markets.

- This knowledge helps investors identify both the risks and the opportunities in a region; for example, a fintech company that solves the documentation problem could unlock a massive new market.

- It highlights the global importance of creating accessible and appropriate financial products that cater to the needs of underserved populations.

- 銀行サービスへのアクセス不足

- 地理的障壁: 一部の地域、特に農村部やサービスが行き届いていない都市部では、銀行支店が不足しており、住民が銀行サービスにアクセスすることが困難になる場合があります。

- デジタル格差: インターネット アクセスやデジタル リテラシーの欠如により、現代の銀行業務にとってますます重要になっているオンライン バンキング サービスに個人が参加できなくなる可能性があります。

- High Fees

- 銀行口座を持たない人の多くは、月々の口座維持費、最低残高要件、当座貸越手数料など、銀行口座の維持にかかる高額なコストが大きな障害になっていると指摘しています。

- 金融機関への不信

- 歴史的に行われてきた差別慣行や、大手銀行を巻き込んだ広く報道されたスキャンダルにより、一部の人々の間でこれらの金融機関に対する不信感が高まっています。この懐疑心は、従来の銀行との関わりを阻む可能性があります。

- 必要な文書の不足

- 銀行口座を開設するには通常、政府発行の身分証明書、住所証明、場合によっては社会保障番号が必要です。移民、若者などはこれらの書類を持っていないため、銀行サービスを利用できない場合があります。

- プライバシーに関する懸念

- 特に不法滞在者の中には、プライバシーに関する懸念や政府の監視を恐れて、銀行口座を開設するために必要な個人情報を共有したくない人もいます。

- 非公式経済への参加

- 非公式経済で働く個人は、課税を回避するため、または収入が不安定で予測不可能なため、銀行口座を維持するのが難しくなるため、現金のみで取引することを好む場合があります。

- 無関係と認識される

- 銀行口座を持つことに個人的なメリットを感じない人もいます。その理由は、給料日前に生活していて貯蓄や投資をする必要がないから、または小切手換金やマネーオーダーなどの代替金融サービスを使って家計を管理しているからです。

障壁を減らすための解決策と取り組み

金融機関、政府機関、非営利団体は、さまざまな取り組みを通じてこれらの障壁を軽減するために取り組んでいます。

- 低コストまたは無料の銀行商品: 手数料が無料または低額で、最低残高要件のない基本的な銀行口座を提供します。

- 金融リテラシーと教育プログラム: 個人が銀行のメリットと口座を効果的に管理する方法を理解できるように支援します。

- モバイルおよびインターネット バンキング ソリューション: サービスが行き届いていない地域や移動に問題のある個人に対する銀行サービスへのアクセスを拡大します。

- Bank On プログラム: 都市、銀行、非営利団体が協力して、アクセスしやすい銀行商品を作成し、金融包摂を拡大します。

これらの障壁に対処することで、より多くの個人が正式な金融システムに統合され、経済成長、安定、そしてより広範な経済への参加の機会が提供されます。

8.14 Managing Credit and Debt

良好な信用履歴を維持するには、責任を持って債務を管理し、期限内に支払いを行い、信用照会の影響を理解することが必要です。信用利用に対する戦略的なアプローチは、高い信用スコアを改善および維持し、消費者の経済的な将来に利益をもたらします。

要約すると、信用を賢く管理するには、さまざまな信用商品の利用規約を理解し、借入決定の影響を認識し、情報に基づいた管理と不正確な点の異議申し立てを通じて自分の信用を積極的に保護することが必要です。

Comparing Borrowing $1,000 Across Credit Options

When a consumer borrows $1,000, the total repayment amount can vary greatly depending on the credit source, interest rate, and fees involved. A careful comparison of options illustrates the real cost of credit:

- クレジットカード: A standard credit card might have an 18% Annual Percentage Rate (APR) with no annual fee. If a borrower only makes minimum payments over one year, the total amount repaid could be approximately $1,180.

- Personal Loan from a Bank: A personal loan could have a 10% APR and a $25 origination fee. Repaying over one year would cost approximately $1,125, a lower total cost compared to using a credit card.

- ペイデイローン: A payday lender might charge a $75 fee for a two-week $500 loan, rolled over once. Borrowing $1,000 could quickly escalate to $1,650 or more due to excessive fees and very short repayment periods.

🔹 Key takeaway:

Consumers must look beyond just the interest rate; initial fees, repayment terms, and hidden costs greatly influence the true cost of borrowing.

8.15 Understanding Grace Periods, Interest Methods, and Fees

の borrowing cost of using credit cards depends heavily on several factors:

- 猶予期間: A period (typically 21–30 days) during which a borrower can pay off a new balance without incurring interest. Missing this period results in full interest charges.

- Interest Calculation Methods:

- Average Daily Balance: Most common; interest is calculated on the average balance owed each day during the billing cycle.

- Previous Balance: Interest is based only on the outstanding balance from the previous month.

- Adjusted Balance: Payments made during the billing cycle are subtracted before interest is calculated, usually favoring the borrower.

- Average Daily Balance: Most common; interest is calculated on the average balance owed each day during the billing cycle.

- Fees:

- Late Payment Fee: Charged if payment is not made by the due date.

- Over-limit Fee: Charged if spending exceeds the credit limit.

- Annual Fee: Some credit cards charge a yearly fee simply for ownership.

- Late Payment Fee: Charged if payment is not made by the due date.

🔹 例:

A cardholder who misses the grace period on a $2,000 balance with an APR of 20% could pay an extra $400 annually in interest.

8.16 Soft vs. Hard Credit Inquiries

Credit inquiries affect credit scores differently:

- Soft Inquiry: Checking your own credit, or lenders reviewing your profile for preapproval offers. Soft inquiries do not impact your credit score.

- Hard Inquiry: Occurs when you apply for a new loan or credit card. Hard inquiries can lower your credit score by a few points and stay on the report for about two years.

🔹 アドバイス:

Limit hard inquiries by applying for new credit only when necessary, as multiple hard pulls within a short time can signal risk to lenders.

8.17 Steps to Improve Your Credit Score

Improving and maintaining a good credit score requires consistent financial habits:

- Pay On Time: Payment history makes up 35% of a FICO score.

- Keep Balances Low: Maintain credit utilization below 30% of your credit limit.

- Limit New Credit Applications: Only open new credit accounts when necessary.

- Maintain Older Accounts: Length of credit history accounts for about 15% of your score.

- クレジットの種類を多様化する: Having a mix of credit types, such as credit cards, auto loans, and mortgages, can boost a score.

🔹 例:

If Laura pays off her balances and avoids opening new accounts for six months, her credit score could rise by 50 points or more, saving her thousands in future interest costs.

8.18 How Employers, Landlords, and Insurers Use Credit Reports

Credit reports aren’t only important for loans:

- Employers: Some employers, especially in financial services or security-sensitive jobs, may check credit reports to gauge responsibility.

- Landlords: Credit history helps landlords assess whether a tenant will reliably pay rent.

- Insurance Companies: Insurers may use credit-based insurance scores to determine auto or home insurance premiums.

🔹 Insight:

Maintaining good credit opens up opportunities not only for better borrowing terms but also for better job prospects and lower living costs.

8.19 The Payday Loan Cycle of Debt

Payday loans, while offering quick cash, often trap borrowers in a cycle of debt:

- High Fees: A $500 payday loan with a $75 fee must be repaid in two weeks. If not repaid, the borrower rolls over the loan, adding another $75.

- Debt Trap: Borrowers might end up paying more in fees than the original loan amount without ever reducing the principal.

🔹 例:

John borrows $500 but rolls the loan over five times, paying $375 in fees—more than half the original loan amount—without reducing the $500 debt.

8.20 Finding Help and Credible Sources on Credit

To protect themselves, consumers should rely on trusted sources:

- 消費者金融保護局 (CFPB): Provides free resources on credit rights.

- 連邦取引委員会(FTC): Offers advice on combating fraud.

- AnnualCreditReport.com: The only federally authorized site for obtaining a free yearly credit report.

🔹 Tip:

Checking credit reports at least once a year allows consumers to catch and correct errors early, maintaining better credit health.

The Role of Cosigners and Collateral in Loans

Understanding cosigners and collateral can improve loan terms:

- Cosigner: A trusted person who promises to repay if the borrower defaults, often helping borrowers with limited credit histories qualify for better rates.

- Collateral: Assets pledged to secure a loan (e.g., car, home). Secured loans typically offer lower interest rates because the lender can recover the asset if the borrower defaults.

🔹 例:

Mark, a recent college graduate, qualifies for a 5% auto loan instead of a 10% loan because his father cosigned the loan.

結論

Incorporating these deeper insights ensures consumers are fully prepared to manage credit wisely, avoid costly mistakes, and build strong, stable financial futures. Empowered with knowledge, they can navigate the credit landscape confidently and strategically.

主なレッスン情報:

Lorem ipsum dolor sit amet、consectetur adipiscing elit。ウト・エリート・テルス、ルクトゥス・ネク・ウラムコーペル・マティス、プルヴィナー・ダピブス・レオ。