제8장 신용관리와 시사점

수업 학습 목표:

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elittellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

신용 관리 소개

효과적인 신용 관리에는 다양한 유형의 신용을 이해하고, 신용 비용을 비교하는 방법, 신용 결정이 개인 재정에 미치는 영향을 인식하는 것이 포함됩니다. 이 장에서는 잘못된 청구서 식별, 신용 비용 비교, 신용 사용의 의미를 포함하여 신용 관리의 복잡성을 살펴봅니다.

8.1 Identifying and Contesting Incorrect Billing Statements

소비자는 청구서 내용을 주의 깊게 검토하여 부정확한 내용이 없는지 확인해야 합니다. 잘못된 청구서를 식별할 때 소비자는 먼저 청구 회사에 연락하여 해결을 시도해야 합니다. 만족스럽지 않으면 소비자 옹호 기관(예: 우수기업협회(BBB), 상공회의소, 플로리다 농무부 및 소비자 서비스부, 연방거래위원회(FTC). 이러한 조직은 중재 서비스를 제공할 수 있으며, 필요한 경우 추가 법적 조치에 대한 지침을 제공할 수 있습니다.

8.2 Comparing Credit Costs

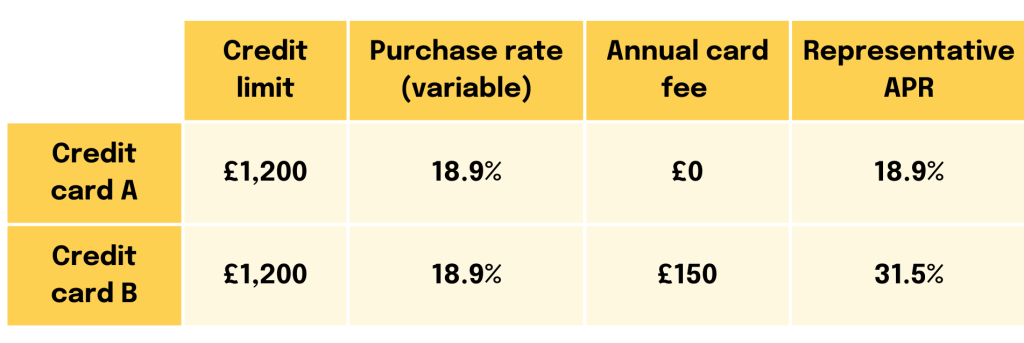

그만큼 연이율(APR) 그리고 초기 수수료, 연체 수수료, 미납 수수료는 신용 비용을 비교할 때 중요한 요소입니다. APR은 이자율 및 기타 비용을 포함한 차용 비용을 포괄적으로 살펴보고 소비자가 다양한 신용 출처를 효과적으로 비교할 수 있도록 합니다.예를 들어, 신용카드 A는 신용카드 B에 비해 연이율(APR)은 낮지만 연체료는 높을 수 있으며, 이는 사용자의 습관에 따라 신용의 전체 비용에 영향을 미칩니다.

낮은 소개 금리로 신용을 얻으세요

금융 기관은 신규 고객을 유치하기 위해 낮은 소개 금리를 제공할 수 있습니다. 매력적이면서도, 이러한 금리는 소개 기간 이후 상당히 증가할 수 있으며, 금리가 오르기 전에 잔액을 갚지 못하는 소비자에게 더 높은 비용으로 이어질 가능성이 있습니다.

수치: The Difference Between Interest Rate and APR

설명:

This graphic illustrates the important distinction between a loan’s 이자율 and its 연이율(APR). It visually explains that the interest rate is just one part of the borrowing cost, while the APR represents the total cost. The image shows that the APR is a broader measure because it includes both the interest rate and any additional lender fees.

주요 시사점:

- 그만큼 이자율 is the direct cost of borrowing the money and is calculated as a percentage of the principal only.

- 그만큼 연이율(APR) provides a more complete picture of a loan’s cost, as it includes the interest rate plus any associated fees, such as origination fees or closing costs.

- Because it includes extra fees, a loan’s APR is typically higher than its advertised interest rate.

- When comparing different loan offers, looking at the APR allows for a more accurate, “apples-to-apples” comparison of the true cost of each option.

정보의 응용:

- When you are shopping for a loan, such as a mortgage or car loan, you should always compare the APR offered by different lenders, not just the interest rate.

- Focusing on the APR helps you understand the 총 차입 비용 and avoid loans that may have a low interest rate but high hidden fees.

- This knowledge is essential for making an informed financial decision and selecting the most affordable loan, potentially saving you a significant amount of money over time.

8.3 Secured vs. Unsecured Loans and credit cards

보안됨 대출은 담보가 필요하고 일반적으로 대출 기관의 위험이 낮아져 이자율이 낮습니다. 자동차 대출이나 모기지와 같이 지불이 이루어지지 않으면 자산을 잃을 위험이 있습니다. 반면에, 무담보 대출, 대부분의 신용카드와 마찬가지로 담보가 필요하지 않지만 이자율이 더 높습니다.

보증된 신용 카드 요구하다 현금 입금 담보 역할을 하므로 대출 기관에게는 위험이 낮은 옵션이 되고 신용을 구축하거나 재구축하려는 소비자에게는 귀중한 도구가 됩니다. 무담보 신용 카드 보증금을 요구하지 않으나, 자격을 갖추려면 소비자의 신용 기록에 따라 결정되는 경우가 많습니다.

8.4 Factors Influencing Borrowing Costs

선불금 총 자금 조달 금액을 줄여 월 상환액이 낮아지거나 대출 기간이 단축됩니다. 상당한 선불금을 가진 차용인은 대출자에게 덜 위험하며, 종종 더 유리한 대출 조건을 제공합니다.

신용카드: 비용과 혜택

신용 카드 편리함을 제공하지만, 특히 신용 점수가 낮은 사용자에게는 높은 이자율과 수수료가 부과될 수 있습니다. 즉시 구매가 가능하지만, 신중하게 관리하지 않으면 이자와 수수료로 인한 장기적 비용이 혜택보다 더 클 수 있습니다.

신용 카드 유예 기간, 이자 계산 방법 및 관련 수수료 대출 비용에 직접 영향을 미칩니다. 유예 기간은 대출인이 이자를 내지 않고 잔액을 상환할 수 있게 해주며, 현명하게 사용하면 상당한 이점을 제공합니다.

8.5 Consumer Protection Laws

다음과 같은 법률 진실대출법(TILA) 그리고 신용카드법 대출 기관이 신용 조건을 명확하게 공개하고 소비자를 불공정 관행으로부터 보호하도록 보장합니다. 대출법은 대출 기관이 신용 조건을 모두 공개하도록 요구하며, 이를 통해 소비자를 차별적인 대출, 부당한 마케팅, 불공정한 채무 징수 관행으로부터 보호합니다. 소비자는 신용을 신청할 때 이러한 공개 내용을 철저히 검토하여 정보에 입각한 결정을 내려야 합니다.

사기 예방 및 해결

사기를 방지하기 위해 소비자는 정기적으로 계좌를 모니터링하고, 온라인 뱅킹을 위한 안전한 방법을 사용하고, 의심스러운 활동이 있으면 즉시 보고해야 합니다. 사기의 경우 금융 기관과 관련 당국에 즉시 연락하는 것이 중요합니다.

8.6 Free Annual Credit Reports

Equifax, Experian, TransUnion과 같은 기관에서 관리하는 신용 보고서는 신용 평가에서 중요한 역할을 합니다. 신용 점수에 영향을 미치는 요인에는 지불 내역, 신용 사용률, 신용 내역 기간이 포함됩니다. 신용 보고서를 정기적으로 확인하고 부정확한 사항에 대해 이의를 제기하는 것은 건강한 신용 점수를 유지하는 데 중요합니다.

소비자는 주요 신용 보고 기관 각각에서 매년 무료 신용 보고서를 한 번 받을 자격이 있습니다. 신용 보고서를 정기적으로 확인하면 대출 비용과 신용 획득 능력에 영향을 미칠 수 있는 오류를 식별하는 데 도움이 됩니다.

8.7 Student Loans Comparison

PLUS 대출, 민간 학생 대출, 직접 보조 대출 또는 비보조 대출 등 다양한 유형의 학자금 대출을 비교하는 것은 연기 기간 동안 발생하는 이자를 포함한 장기적 비용을 이해하는 데 중요합니다.

다양한 학자금 대출의 미묘한 차이를 이해하는 것은 귀하의 교육 자금 조달 전략에 상당한 영향을 미칠 수 있습니다. 다양한 유형의 학자금 대출에 대한 이자 발생 정책과 자격 기준에 대한 세부 내용은 다음과 같습니다.

직접 보조 대출

- 이자 발생: 미국 교육부는 학생이 최소한 반나절 이상 학교에 다니는 동안, 학교를 떠난 후 처음 6개월 동안(유예 기간), 그리고 연기 기간 동안 이자를 지급합니다.

- 적임: 재정적 필요성이 입증된 학부생에게 제공 가능.

직접 무보조 대출

- 이자 발생: 이자는 대출금이 학생에게 지급되는 시점부터 발생합니다. 학생은 모든 이자를 지불해야 하지만, 재학 중 이자 지불을 연기할 수 있으며, 그러면 원금으로 환산되어 대출 원금에 추가됩니다.

- 적임: 학부생, 대학원생, 전문가 학생이 이용할 수 있습니다. 재정적 필요성을 입증할 필요는 없습니다.

학부생을 위한 부모 대출(PLUS) 대출

- 이자 발생: 이자는 지급 즉시 발생하기 시작합니다. 보조금은 없으며, 대출인은 모든 이자 지불에 대한 책임이 있습니다.

- 적임: 부양받는 학부생의 부모, 대학원생 및 전문대생에게 제공됩니다. 자격은 재정적 필요에 따라 결정되지 않지만 신용 검사가 필요합니다. 신용 기록이 좋지 않은 대출자는 보증인이 필요할 수 있습니다.

사립 학자금 대출

- 이자 발생: Policies vary by lender, but typically, interest starts accruing immediately upon disbursement. Some private loans offer deferment options where interest continues to accrue but payments are not required until later.

- 적임: Determined by the private lender, usually based on creditworthiness. Students often need a cosigner with good credit to qualify for the best interest rates.

주요 고려 사항:

- 이자 발생 및 자본화: 이자가 어떻게 발생하는지, 언제 자본화되는지(대출 원금 잔액에 추가되는지)를 이해하는 것은 장기 차용 비용을 관리하는 데 중요합니다. 보조 연방 대출은 학생이 학교에 다니는 동안 이자가 발생하지 않는다는 이점을 제공하며, 이는 상당한 절감으로 이어질 수 있습니다.

- 자격 요건: 연방 대출은 일반적으로 연방 학생 지원 무료 신청서(FAFSA)를 작성하여 자격을 확인해야 합니다. 민간 대출은 자체 신청 절차가 있으며 소득 증빙, 신용 검사 및 공동 서명자가 필요할 수 있습니다.

- 올바른 대출 선택: 원금과 이자를 포함한 대출의 총 비용과 대출과 관련된 모든 수수료를 고려하세요. 연방 대출은 고정 이자율과 소득 기반 상환 계획 및 용서 프로그램에 대한 액세스와 같은 혜택을 제공하는데, 이는 일반적으로 민간 대출에서는 제공되지 않습니다.

Navigating student loans requires careful consideration of both immediate needs and future financial implications, making an understanding of each type of loan’s specifics essential for sound financial planning in pursuit of education.

8.8 Deferred Student Loan Payment

학자금 대출의 연기 지불은 차용인이 재정적 어려움, 추가 교육 등록 또는 실업과 같은 특정 조건에서 상환을 연기할 수 있는 기능으로, 즉각적인 구제책과 장기적인 재정적 영향을 모두 가질 수 있습니다. 학자금 대출 상환 연기의 잠재적 결과는 다음과 같습니다.

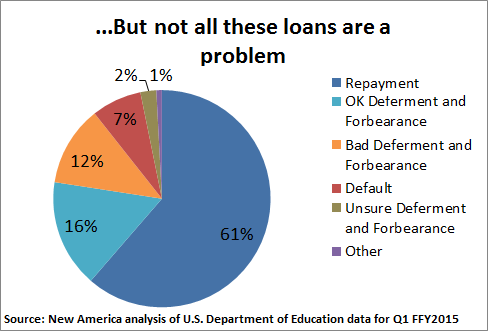

Figure: Student Loan Deferment vs. Forbearance

설명:

This image compares two common options for temporarily pausing student loan payments: deferment 그리고 forbearance. It visually breaks down the key differences between these two programs, with a strong focus on how the 관심 that accumulates on the loan is handled. The goal is to help borrowers understand the financial implications of each choice before deciding.

주요 시사점:

- Both deferment 그리고 forbearance are official ways to pause your student loan payments if you are facing financial difficulty.

- The most important difference is in how accrued interest is treated. With deferment on certain types of federal loans (subsidized loans), the government may pay the interest for you.

- With forbearance, you are always responsible for paying the interest that accrues during the pause, regardless of your loan type.

- This unpaid interest is often capitalized at the end of the forbearance period, meaning it is added to your principal loan balance, increasing the total amount you will have to repay.

정보의 응용:

- If you are unable to make your student loan payments, it is critical to understand these options to choose the least costly one for your situation.

- You should always check if you qualify for deferment first, as it can save you a significant amount of money in interest payments.

- While pausing payments offers short-term relief, it’s vital to understand the long-term cost, as capitalized interest from forbearance can make your loan more expensive over time.

단기적 이점

- 즉각적인 재정적 구제: 지불 연기는 일시적으로 재정적 어려움을 겪고 있는 사람들에게 꼭 필요한 여유를 제공하여 주거, 식량, 의료비와 같은 즉각적인 필요에 자원을 할당할 수 있게 해줍니다.

- 채무 불이행 방지: 공식적으로 대출을 연기함으로써 차용인은 대출 불이행을 피할 수 있으며, 이를 통해 신용 점수를 유지하고 대출 불이행과 관련된 엄중한 처벌을 피하는 데 도움이 됩니다.

장기적 결과

- 이자 발생: 대부분의 학자금 대출 유형에 대해 지불이 이루어지지 않더라도 연기 기간 동안 이자가 계속 발생합니다. 즉, 총 빚이 늘어나고 대출인은 대출 기간 동안 더 많은 금액을 지불하게 됩니다.

- 상환 기간 연장: 지불을 연기하면 대출 상환에 걸리는 시간이 연장되어 차용인의 장기적인 재정 목표에 영향을 미칠 수 있으며 주택 구입이나 은퇴를 위한 저축 등의 이정표 달성이 늦어질 수 있습니다.

- 대출 총 비용 증가: 보조되지 않는 대출의 경우, 연기 기간 동안 누적된 이자가 대출 원금 잔액에 추가되어 대출 기간 동안 상환해야 할 총 금액이 상당히 늘어날 수 있습니다.

- 면제 프로그램 자격에 미치는 영향: 공공 서비스 대출 면제(PSLF)와 같은 프로그램을 통해 대출 면제를 받기 위해 노력하는 차용인의 경우, 연기 기간은 자격 지급액에 포함되지 않아 면제까지 걸리는 시간이 연장될 수 있습니다.

예시 시나리오

알렉스는 연방 학자금 대출에 $30,000을 가지고 있으며, 이자율은 5%입니다. 그는 재정적 어려움으로 인해 1년 동안 대출을 연기하기로 결정했습니다. 이 해 동안 그의 대출은 $1,500($30,000의 5%)의 이자가 발생하며, 이는 보조되지 않는 대출이 있는 경우 원금 잔액에 추가됩니다. 그가 지불을 재개할 때 그의 새로운 잔액은 $31,500이며, 그는 이 더 높은 금액에 대한 이자를 지불해야 하며, 이로 인해 대출 비용이 증가합니다.

8.9 Strategies to Mitigate Negative Consequences

- 이자 지급: 가능하다면 연기 기간 동안 이자를 지불하면 이자가 원금에 추가되는 것을 방지하여 대출 잔액이 늘어나는 것을 막을 수 있습니다.

- 더 짧은 연기 기간: 필요한 기간 동안만 연기를 활용하면 시간이 지남에 따라 이자가 누적되므로 재정적 영향을 최소화하는 데 도움이 될 수 있습니다.

- 대체 상환 계획 탐색: 소득 기반 상환 계획은 상환을 연기할 필요 없이 매월 지불하는 금액을 낮추고 20~25년 후에 대출을 면제받을 수 있습니다.

학자금 대출 상환을 연기하는 것은 재정적 어려움을 관리하는 데 도움이 되는 단기 전략이 될 수 있지만, 대출인은 전반적인 재정 건강에 미치는 장기적인 영향을 고려하고 이에 따라 계획을 세우는 것이 필수적입니다.

8.10 Credit Influence on Mortgage Rates and Payments

담보 대출은 주택담보대출과 마찬가지로 일반적으로 무담보 대출보다 이자율이 낮습니다. 주택담보대출 상환액은 대출 금액, 이자율, 상환 기간에 따라 영향을 받습니다. 조정 가능 금리 주택담보대출(ARM) 초기 이자율은 낮을 수 있지만, 이자율이 상승하면 향후 지급액이 더 높아질 수 있습니다. 고정금리 모기지 일정한 이자율로 안정성을 제공합니다. 대출 조건, 금액, 이자율에 따라 주택담보대출 옵션을 비교하는 것은 가장 저렴한 옵션을 찾는 데 필수적입니다.

8.11 Credit Reports and Scores

신용 보고서와 점수를 통해 평가된 신용도는 차입 비용에 상당한 영향을 미칩니다. 집주인, 고용주, 보험 회사도 이 정보를 의사 결정 과정에 사용합니다. 긍정적인 신용 기록을 유지하는 것은 재정 건강에 매우 중요합니다.

8.12 Alternative Financial Services

급여대출과 유사한 서비스는 자금에 대한 빠른 접근을 제공하지만 비용이 많이 듭니다. 이러한 서비스의 의미, 특히 이로 인해 발생할 수 있는 부채의 순환을 이해하는 것은 금융 지식에 필수적입니다.

급여대출 vs. 은행대출

급여대출과 은행대출의 차이는 조건과 비용에 있습니다. 급여대출은 일반적으로 훨씬 더 높은 이자율과 수수료를 가지고 있어, 은행대출에 비해 같은 빌린 금액에 대해 더 많은 상환 금액을 가져옵니다.

급여대출 예시:

존이 긴급 차량 수리를 위해 $500이 필요하다고 가정해 보겠습니다. 그는 급여대출업체에 도움을 요청했고, 급여대출업체는 그에게 $500을 즉시 제공했습니다. 이 조건은 $75 서비스 수수료와 함께 2주 내에 상환해야 합니다. 연이율(APR)로 계산하면 이 대출의 이자는 390%를 초과합니다. 존이 2주 내에 대출을 상환할 수 없다면, 그는 또 다른 급여대출을 받아야 할 수 있으며, 추가 수수료가 발생하고 잠재적으로 부채 주기로 이어질 수 있습니다.

은행 대출 사례:

반면, 사라가 비슷한 긴급 상황에 $500이 필요하다면, 그녀는 계좌가 있는 은행에서 개인 대출을 선택할 수 있습니다. 은행은 그녀에게 10%(2023년 4월 마지막 업데이트 당시 개인 대출에 대한 높은 추정치)의 APR과 1년 상환 기간의 대출을 제공합니다. 1년 동안 그녀는 약 $27.29의 이자를 지불할 것이며, 이는 급여일 대출 비용보다 상당히 낮습니다.

비교 분석:

- 이자율 및 수수료: 급여대출은 은행 대출에 비해 APR이 엄청나게 높습니다. 이 예는 급여대출의 APR이 고금리 개인 은행 대출보다 거의 10배 높을 수 있음을 보여줍니다.

- 상환 기간: 급여대출은 일반적으로 상환기간이 매우 짧습니다(대개 2주). 반면, 은행 대출은 상환기간이 길어서 매달 상환하는 것이 더 쉽습니다.

- 부채의 순환: 급여대출은 비용이 높고 상환 기간이 짧기 때문에 부채의 악순환으로 이어질 수 있습니다. 제때 상환할 수 없는 차용인은 추가 대출을 받아 더 많은 수수료를 부담하게 되고, 이는 부채의 악순환에 빠질 수 있습니다.

- 신용에 미치는 영향: 일반 은행 대출은 신용 기관에 보고되어 제때 상환하면 신용을 쌓는 데 도움이 될 수 있습니다. 반면, 급여일 대출은 대출이 회수되지 않는 한 신용 기관에 보고되지 않기 때문에 일반적으로 신용을 쌓지 않습니다.

이 비교는 급여대출이 재정적 긴급 상황에 대한 빠른 해결책처럼 보일 수 있지만, 더 관리하기 쉬운 조건과 더 낮은 이자율을 제공하는 전통적인 은행 대출보다 비용이 훨씬 더 많이 드는 경우가 많다는 것을 보여줍니다. 대출인은 급여대출을 선택하기 전에 모든 대안을 고려하고 조건과 잠재적인 장기적 영향을 이해해야 합니다.

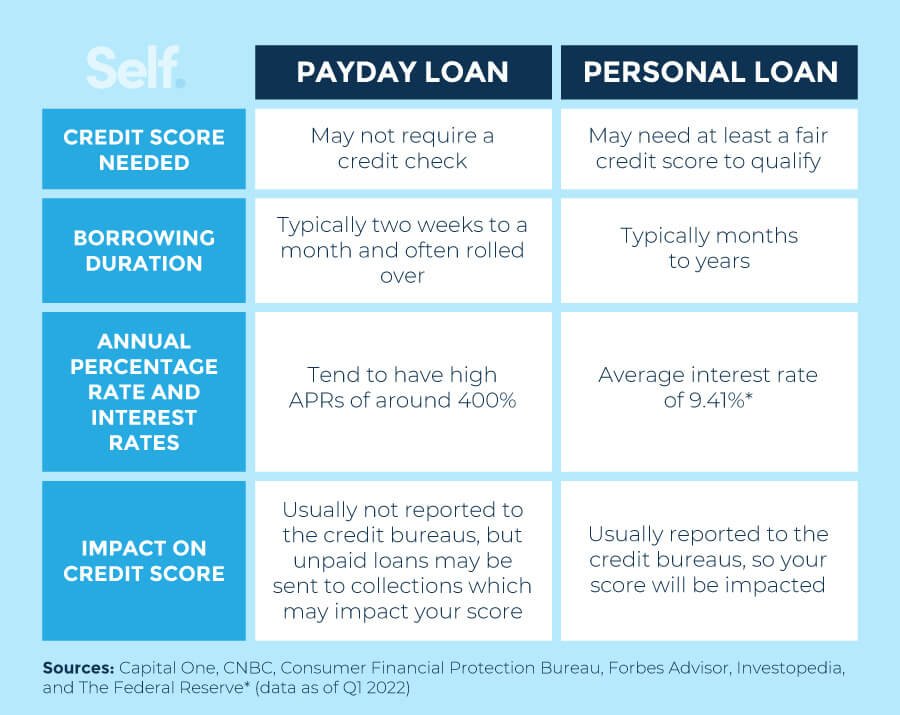

Figure: Payday Loans vs. Personal Loans

설명:

This image provides a side-by-side comparison of payday loans 그리고 personal loans, highlighting the critical differences between these two ways of borrowing money. It focuses on key features such as interest rates, loan amounts, and repayment terms to illustrate their respective costs and benefits. The graphic is designed to help individuals understand which option is safer and more affordable for their financial needs.

주요 시사점:

- The most significant difference is the cost: Payday loans are known for having extremely high APRs (Annual Percentage Rates), often 300% or more, while personal loans offer much lower and more manageable interest rates.

- Repayment schedules are very different. Payday loans require full repayment in a very short term (usually by your next payday), whereas personal loans are repaid in predictable monthly installments over several months or years.

- Loan amounts vary significantly. Payday loans are for small, short-term needs (typically under $500), while personal loans can provide access to much larger sums of money.

- While payday loans are often easier to obtain for those with poor credit, personal loans from reputable lenders are a much more structured and less risky form of credit.

정보의 응용:

- This comparison clearly shows that payday loans should be avoided whenever possible, as their high costs can quickly lead to a dangerous debt cycle.

- If you need to borrow money, a personal loan from a bank or credit union is almost always a more responsible and cost-effective financial decision.

- Understanding the true cost of debt, particularly the APR, is a critical skill for making smart borrowing choices and protecting your long-term financial health.

8.13 Barriers to Being Banked

은행 서비스를 받는 데 대한 장벽, 또는 개인이 전통적인 은행 서비스를 이용하지 않는 이유는 다각적이며 재정 건강과 재정 기회에 대한 접근성에 상당한 영향을 미칠 수 있습니다. 다음은 주요 장애물과 각 장애물에 대한 세부 정보입니다.

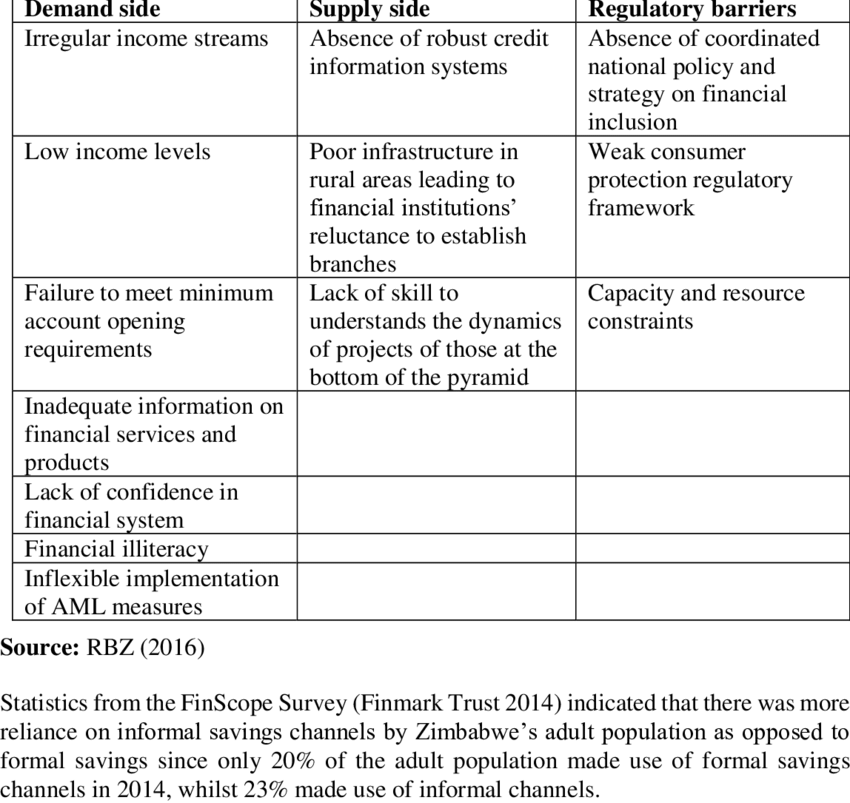

수치: Major Barriers to Financial Inclusion in Zimbabwe

설명:

This table, from a formal research publication, lists the key obstacles that prevent people across Zimbabwe from accessing and using formal financial services. The figure categorizes these challenges, highlighting issues such as high transaction costs, lack of trust in the banking system, and low levels of financial literacy. It provides a structured overview of why achieving full financial inclusion remains difficult.

주요 시사점:

- Financial inclusion faces multiple complex barriers, ranging from economic to social and educational issues.

- High service costs and bank fees are a primary obstacle, making financial services unaffordable for many low-income individuals.

- A significant portion of the population may lack the formal documentation, such as a national ID or proof of income, required to open a bank account.

- Low levels of financial literacy (a lack of understanding of financial products) and a general distrust in financial institutions are also major hindrances.

정보의 응용:

- Understanding these barriers is essential for anyone interested in finance or investing in emerging markets.

- This knowledge helps investors identify both the risks and the opportunities in a region; for example, a fintech company that solves the documentation problem could unlock a massive new market.

- It highlights the global importance of creating accessible and appropriate financial products that cater to the needs of underserved populations.

- 은행 서비스 접근성 부족

- 지리적 장벽: 일부 지역, 특히 농촌이나 서비스가 부족한 도시 지역에는 은행 지점이 부족하여 주민들이 은행 서비스를 이용하기 어려울 수 있습니다.

- 디지털 격차: 인터넷 접속이나 디지털 리터러시가 부족하면 개인이 온라인 뱅킹 서비스를 이용하지 못할 수 있는데, 이는 현대 뱅킹에 점점 더 중요해지고 있는 서비스입니다.

- High Fees

- 은행 계좌를 이용하지 않는 많은 사람은 월 유지 수수료, 최소 잔액 요구 사항, 대체 계좌 수수료 등 은행 계좌 유지에 따르는 높은 비용을 큰 장애물로 꼽습니다.

- 금융기관에 대한 불신

- 주요 은행과 관련된 잘 알려진 스캔들과 함께 역사적 차별 관행은 특정 인구 사이에서 이러한 기관에 대한 불신으로 이어졌습니다. 이러한 회의주의는 전통적인 은행과의 관계를 낙담시킬 수 있습니다.

- 필요한 문서가 부족합니다

- 은행 계좌를 개설하려면 일반적으로 정부에서 발급한 신분증, 주소 증명, 때로는 사회보장번호가 필요합니다. 이민자, 청소년 및 기타 사람들은 이러한 서류가 없어 은행 서비스를 이용할 수 없습니다.

- 개인정보 보호 문제

- 일부 개인은 개인정보 보호 문제나 정부 감사에 대한 두려움 때문에 은행 계좌 개설에 필요한 개인 정보를 공유하고 싶어하지 않습니다. 특히 불법 체류자의 경우가 그렇습니다.

- 비공식 경제 참여

- 비공식 경제에서 일하는 개인은 세금을 피하기 위해, 또는 수입이 일정하지 않고 예측 불가능하여 은행 계좌를 유지하기 어렵기 때문에 현금으로만 거래하는 것을 선호할 수 있습니다.

- 인식된 무관함

- 일부 사람들은 은행 계좌를 갖는 데 개인적인 이점이 없다고 생각합니다. 저축이나 투자의 필요성이 전혀 없이 월급을 받고 살아가는 경우가 있고, 수표 현금화나 송금 수표와 같은 대체 금융 서비스를 사용하여 재정을 관리하기도 합니다.

장벽을 줄이기 위한 솔루션과 노력

금융 기관, 정부 기관 및 비영리 단체는 다양한 이니셔티브를 통해 이러한 장벽을 줄이기 위해 노력하고 있습니다.

- 저렴 또는 무비용 은행 상품: 수수료가 낮거나 전혀 없고 최소 잔액 요구 사항이 없는 기본적인 은행 계좌를 제공합니다.

- 금융 지식 향상 및 교육 프로그램: 개인이 은행 업무의 이점을 이해하고 계좌를 효과적으로 관리하는 방법을 돕습니다.

- 모바일 및 인터넷 뱅킹 솔루션: 서비스가 부족한 지역이나 이동성 문제가 있는 개인을 위한 뱅킹 서비스 접근성 확대

- Bank On Programs: 도시, 은행, 비영리 단체 간의 협업을 통해 접근 가능한 은행 상품을 만들고 금융 포용성을 높입니다.

이러한 장벽을 해소함으로써 더 많은 개인이 공식 금융 시스템에 통합될 수 있고, 이들에게 재정적 성장, 안정성 및 더 넓은 경제에 참여할 수 있는 기회가 제공될 수 있습니다.

8.14 Managing Credit and Debt

좋은 신용 기록을 유지하려면 부채를 책임감 있게 관리하고, 적시에 지불하고, 신용 조회의 영향을 이해해야 합니다. 신용 사용에 대한 전략적 접근 방식은 높은 신용 점수를 개선하고 유지하여 소비자의 재정적 미래에 도움이 될 수 있습니다.

요약하자면, 신용을 현명하게 관리하려면 다양한 신용 상품의 약관을 이해하고, 대출 결정이 미치는 영향을 인식하며, 정보에 입각한 관리와 부정확한 사항에 대한 이의 제기를 통해 신용을 적극적으로 보호해야 합니다.

Comparing Borrowing $1,000 Across Credit Options

When a consumer borrows $1,000, the total repayment amount can vary greatly depending on the credit source, interest rate, and fees involved. A careful comparison of options illustrates the real cost of credit:

- 신용 카드: A standard credit card might have an 18% Annual Percentage Rate (APR) with no annual fee. If a borrower only makes minimum payments over one year, the total amount repaid could be approximately $1,180.

- Personal Loan from a Bank: A personal loan could have a 10% APR and a $25 origination fee. Repaying over one year would cost approximately $1,125, a lower total cost compared to using a credit card.

- Payday Loan: A payday lender might charge a $75 fee for a two-week $500 loan, rolled over once. Borrowing $1,000 could quickly escalate to $1,650 or more due to excessive fees and very short repayment periods.

🔹 Key takeaway:

Consumers must look beyond just the interest rate; initial fees, repayment terms, and hidden costs greatly influence the true cost of borrowing.

8.15 Understanding Grace Periods, Interest Methods, and Fees

그만큼 borrowing cost of using credit cards depends heavily on several factors:

- Grace Period: A period (typically 21–30 days) during which a borrower can pay off a new balance without incurring interest. Missing this period results in full interest charges.

- Interest Calculation Methods:

- Average Daily Balance: Most common; interest is calculated on the average balance owed each day during the billing cycle.

- Previous Balance: Interest is based only on the outstanding balance from the previous month.

- Adjusted Balance: Payments made during the billing cycle are subtracted before interest is calculated, usually favoring the borrower.

- Average Daily Balance: Most common; interest is calculated on the average balance owed each day during the billing cycle.

- Fees:

- Late Payment Fee: Charged if payment is not made by the due date.

- Over-limit Fee: Charged if spending exceeds the credit limit.

- Annual Fee: Some credit cards charge a yearly fee simply for ownership.

- Late Payment Fee: Charged if payment is not made by the due date.

🔹 예:

A cardholder who misses the grace period on a $2,000 balance with an APR of 20% could pay an extra $400 annually in interest.

8.16 Soft vs. Hard Credit Inquiries

Credit inquiries affect credit scores differently:

- Soft Inquiry: Checking your own credit, or lenders reviewing your profile for preapproval offers. Soft inquiries do not impact your credit score.

- Hard Inquiry: Occurs when you apply for a new loan or credit card. Hard inquiries can lower your credit score by a few points and stay on the report for about two years.

🔹 조언:

Limit hard inquiries by applying for new credit only when necessary, as multiple hard pulls within a short time can signal risk to lenders.

8.17 Steps to Improve Your Credit Score

Improving and maintaining a good credit score requires consistent financial habits:

- Pay On Time: Payment history makes up 35% of a FICO score.

- Keep Balances Low: Maintain credit utilization below 30% of your credit limit.

- Limit New Credit Applications: Only open new credit accounts when necessary.

- Maintain Older Accounts: Length of credit history accounts for about 15% of your score.

- 신용 유형 다양화: Having a mix of credit types, such as credit cards, auto loans, and mortgages, can boost a score.

🔹 예:

If Laura pays off her balances and avoids opening new accounts for six months, her credit score could rise by 50 points or more, saving her thousands in future interest costs.

8.18 How Employers, Landlords, and Insurers Use Credit Reports

Credit reports aren’t only important for loans:

- Employers: Some employers, especially in financial services or security-sensitive jobs, may check credit reports to gauge responsibility.

- Landlords: Credit history helps landlords assess whether a tenant will reliably pay rent.

- Insurance Companies: Insurers may use credit-based insurance scores to determine auto or home insurance premiums.

🔹 Insight:

Maintaining good credit opens up opportunities not only for better borrowing terms but also for better job prospects and lower living costs.

8.19 The Payday Loan Cycle of Debt

Payday loans, while offering quick cash, often trap borrowers in a cycle of debt:

- High Fees: A $500 payday loan with a $75 fee must be repaid in two weeks. If not repaid, the borrower rolls over the loan, adding another $75.

- Debt Trap: Borrowers might end up paying more in fees than the original loan amount without ever reducing the principal.

🔹 예:

John borrows $500 but rolls the loan over five times, paying $375 in fees—more than half the original loan amount—without reducing the $500 debt.

8.20 Finding Help and Credible Sources on Credit

To protect themselves, consumers should rely on trusted sources:

- 소비자 금융 보호국 (CFPB): Provides free resources on credit rights.

- 연방거래위원회(FTC): Offers advice on combating fraud.

- AnnualCreditReport.com: The only federally authorized site for obtaining a free yearly credit report.

🔹 Tip:

Checking credit reports at least once a year allows consumers to catch and correct errors early, maintaining better credit health.

The Role of Cosigners and Collateral in Loans

Understanding cosigners and collateral can improve loan terms:

- Cosigner: A trusted person who promises to repay if the borrower defaults, often helping borrowers with limited credit histories qualify for better rates.

- Collateral: Assets pledged to secure a loan (e.g., car, home). Secured loans typically offer lower interest rates because the lender can recover the asset if the borrower defaults.

🔹 예:

Mark, a recent college graduate, qualifies for a 5% auto loan instead of a 10% loan because his father cosigned the loan.

결론

Incorporating these deeper insights ensures consumers are fully prepared to manage credit wisely, avoid costly mistakes, and build strong, stable financial futures. Empowered with knowledge, they can navigate the credit landscape confidently and strategically.

주요 수업 정보:

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elittellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.