Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elittellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

미국에서의 은퇴 계획은 은퇴 소득의 다면적인 원천과 은퇴 계획에서 사회 보장의 역할을 이해하는 것을 포함합니다. 사회 보장 및 기타 소득원을 포함하여 미국에서의 은퇴 계획과 관련된 주요 측면에 대한 탐구입니다.

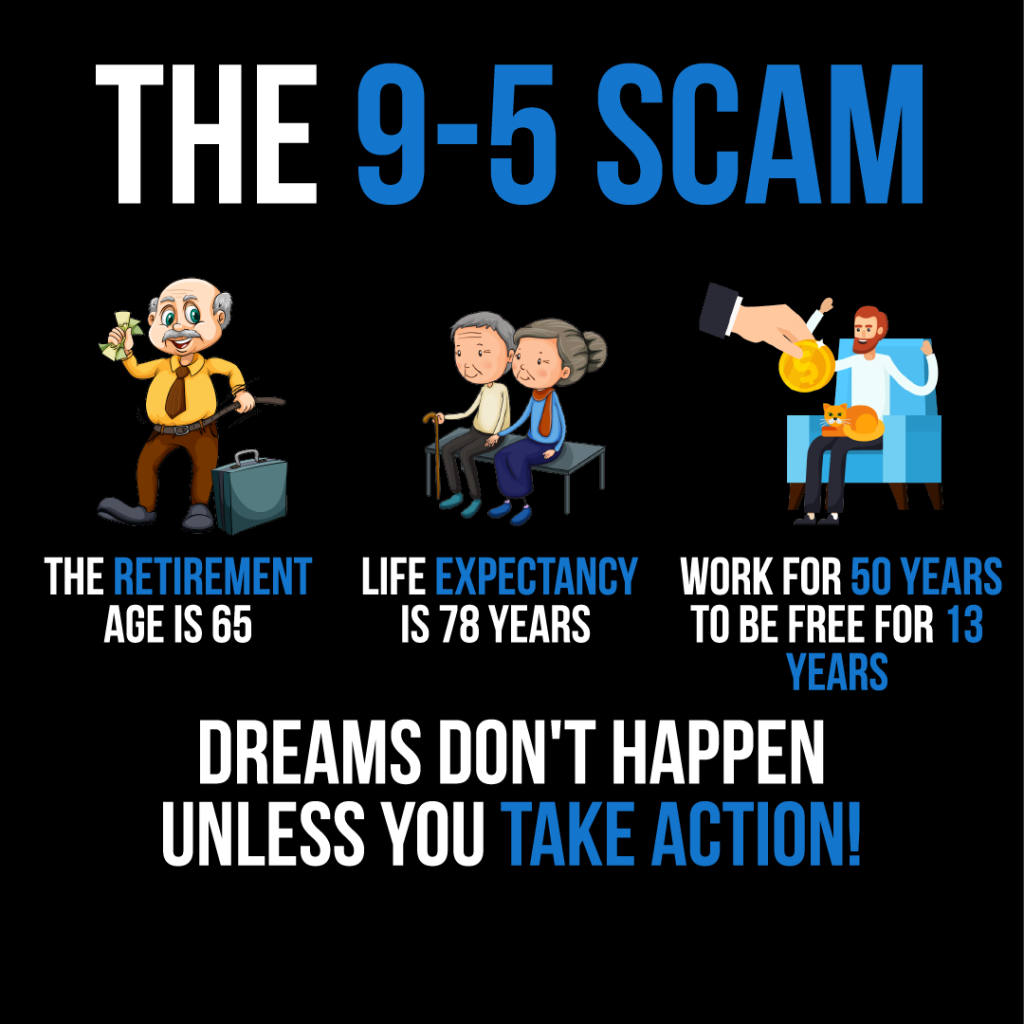

Figure: The infographic titled "The 9-5 Scam" presents a critical view of traditional work life. It points out that with a life expectancy of 78 years and a retirement age of 65, one would work for 50 years only to be free for 13 years. The message "Dreams don't happen unless you take action!" suggests that relying solely on a 9-5 job may not be the most effective path to fulfilling one's dreams. This visual is a call to action for individuals to take proactive steps towards their goals, possibly implying the pursuit of alternative income streams or early retirement strategies. For practical use, users should consider their long-term life and financial goals and explore various ways to achieve them beyond the conventional employment paradigm. Source: Custom Infographic

13.1 Understanding Social Security

사회보장 자금: Social Security is funded through payroll taxes collected under the Federal Insurance Contributions Act (FICA). Both employees and employers contribute to this fund, which then provides benefits to retirees, disabled individuals, and survivors of deceased workers. Each paycheck has a deduction (typically 6.2% from the employee and 6.2% from the employer) funding future benefits. Understanding the funding method is crucial because changes in the workforce or tax rates could affect Social Security’s long-term sustainability.

제공되는 혜택: 사회보장은 은퇴자들에게 안전망을 제공하며, 근무 기간 동안의 수입에 따라 월 소득을 제공합니다. 받는 혜택의 양은 은퇴 연령과 개인의 수입 기록에 따라 달라집니다.

그만큼 average Social Security benefit for a retired worker in 2023 is approximately $1,827 per month, but this varies depending on lifetime earnings and the age at which benefits are claimed.

예시 활동: 사회 보장의 혜택을 강조하는 홍보 전단지를 디자인합니다. 전단지는 62세에 조기 퇴직하면 정년 퇴직 연령 혜택에 비해 혜택이 낮아질 수 있으며, 혜택을 70세까지 연기하면 월 혜택 금액이 늘어날 수 있음을 보여줄 수 있습니다. 다양한 소득 수준에 따른 혜택 차이를 보여주는 시각 자료나 차트를 포함합니다.

13.2 Diversifying Retirement Income

은퇴 소득의 다양한 출처:

사회 보장: 많은 은퇴자들에게 기본적인 소득원으로, 소득 내역에 따른 혜택을 제공합니다.

고용주 후원 연금 계획: 은퇴 자금을 마련하는 데 꼭 필요한 401(k)와 연금 등이 그렇습니다.

개인 투자: IRA, 주식, 채권 및 기타 투자 수단이 포함됩니다.

지속적인 고용 수입: 은퇴 후에 파트타임으로 일하거나 컨설팅을 하면 수입을 보충할 수 있습니다.

Typical sources of retirement income also include annuities, real estate rental income, reverse mortgages, and health savings accounts (HSAs) for medical expenses.

은퇴 시의 다양한 소득원: Relying on a single source of retirement income, like Social Security may not be sufficient for a comfortable retirement. A diversified income strategy incorporating employer-sponsored plans and personal investments can offer a way to maintain financial security and flexibility during retirement.

고용주 후원 연금 계획: Participating in these plans is critical, like a 401(k). Many employers offer a match to your contributions, which is essentially free money for your retirement fund. Maximizing your contribution to receive the full employer match can significantly impact your retirement savings. Employees should strive to contribute at least enough to receive the full employer match — otherwise, they are leaving free money on the table.

건강 저축 계좌(HSA) are another valuable tool for retirement planning. HSAs allow tax-free savings for medical expenses in retirement, reducing the financial burden of healthcare costs.

평균 사회보장 혜택: 최근 데이터에 따르면, 은퇴한 근로자의 평균 월 사회보장 혜택은 약 $1,543입니다. 그러나 이 금액은 귀하의 소득 내역과 혜택을 받기 시작하는 연령에 따라 다릅니다.

수치: 은퇴를 위한 저축 전략

설명:

The image outlines various strategies to save for retirement:

연간 15% 절약: 매년 소득의 최소 15%를 저축하는 것을 목표로 하세요.

가장 큰 비용을 위해 저축하세요: 은퇴 후에 발생할 상당한 비용을 위해 저축을 우선시하세요.

연간 15% 이상 절약: 가능하다면 권장 금액인 15%보다 더 많이 저축하여 더욱 풍성한 은퇴 자금을 마련하세요.

은퇴 계좌를 최대한 활용하세요: 401(k)와 IRA 같은 은퇴 계좌를 최대한 활용하세요.

지금 장기적으로 투자하세요: 은퇴 자금을 늘리려면 장기 투자에 집중하세요.

캐치업 기여를 활용하세요: 만 50세 이상이시면 은퇴 계좌에 추가 기여를 하세요.

장기 은퇴를 위한 예산: 긴 은퇴 기간을 고려하여 저축을 계획하세요.

은퇴 계획에 대한 도움을 받으세요: 안전한 은퇴 생활을 위해 올바른 길을 가고 있는지 확인하려면 전문가의 조언을 구하세요.

주요 시사점:

편안한 은퇴생활을 위해서는 매년 소득의 상당 부분을 저축하는 것이 중요합니다.

장기 투자와 은퇴 계좌 기여금 극대화를 통해 은퇴 기금을 크게 늘릴 수 있습니다.

장기 은퇴생활을 위해 예산을 세우고 전문적인 은퇴 계획에 대한 조언을 받는 것은 은퇴 기간 동안 재정적 안정을 확보하는 데 도움이 될 수 있습니다.

정보의 응용:

이러한 전략은 은퇴를 위한 저축에 대한 체계적인 접근 방식을 제공합니다. 이러한 지침을 따르면 개인은 은퇴 기간 동안 자신을 지원할 상당한 은퇴 기금을 구축하기 위해 노력할 수 있습니다. 일찍 저축과 투자를 시작하고, 은퇴 계좌를 활용하고, 잘 계획되고 재정적으로 안전한 은퇴를 보장하기 위해 전문가의 조언을 구하는 것이 필수적입니다.

13.3 Planning for Retirement

편안한 은퇴생활을 보장하려면 다음 사항이 필수입니다.

복리의 혜택을 누리려면 일찍부터 저축을 시작하세요.

위험을 줄이고 재정적 안정을 높이려면 은퇴 수입원을 다양화하세요.

사회보장의 혜택과 한계를 이해하고 그에 따라 혜택을 극대화하기 위한 계획을 세우세요.

고용주가 후원하는 퇴직 연금 계획에 참여하고 고용주가 전액 지원하는 금액을 받을 수 있도록 노력하세요.

추가적인 은퇴 자금을 마련하기 위해 IRA와 같은 개인 투자 및 저축 계획을 고려하세요.

Taxable vs Tax-Deferred vs Tax-Advantaged Accounts:

Taxable accounts (like brokerage accounts) do not offer any upfront tax benefits.

Tax-deferred accounts (like Traditional IRAs and 401(k)s) allow contributions to grow tax-free until retirement when withdrawals are taxed as income.

Tax-advantaged accounts (like Roth IRAs) involve paying taxes upfront, but earnings and qualified withdrawals are tax-free.”

Retirement vs Estate Planning:

Retirement planning focuses on ensuring financial independence during retirement by building savings through Social Security, employer plans, and personal investments.

Estate planning addresses how your assets will be distributed after your death and includes tools like wills, trusts, and beneficiary designations.

13.4 Estate Planning Tools:

Figure: A symbolic representation of retirement savings with a golden egg nestled securely, suggesting the importance of building a financial nest egg for the future.

할 것이다: Legal document directing asset distribution after death.

생전의료의향서: Outlines healthcare wishes if incapacitated.

Trust: Allows assets to be managed and distributed without going through probate court.

Annuities and Pensions: Can provide income streams to support heirs. Understanding these tools ensures your wishes are honored and can reduce taxes or legal fees for your heirs

결론

미국의 은퇴 계획에는 사회 보장, 고용주 후원 계획, 개인 투자, 그리고 아마도 계속 고용된 수입을 결합한 포괄적인 전략이 포함되어야 합니다. 사회 보장이 어떻게 자금 조달되고 어떤 혜택을 제공하는지 이해하는 것은 매우 중요하며, 황금기를 보내는 동안 재정적 안정을 보장하기 위해 은퇴 소득을 다양화하는 것도 중요합니다.

잘 고안된 은퇴 계획은 은퇴 후 재정적 안정과 마음의 평화를 제공하는 돈을 모으는 데 도움이 됩니다.

주요 수업 정보:

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elittellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.