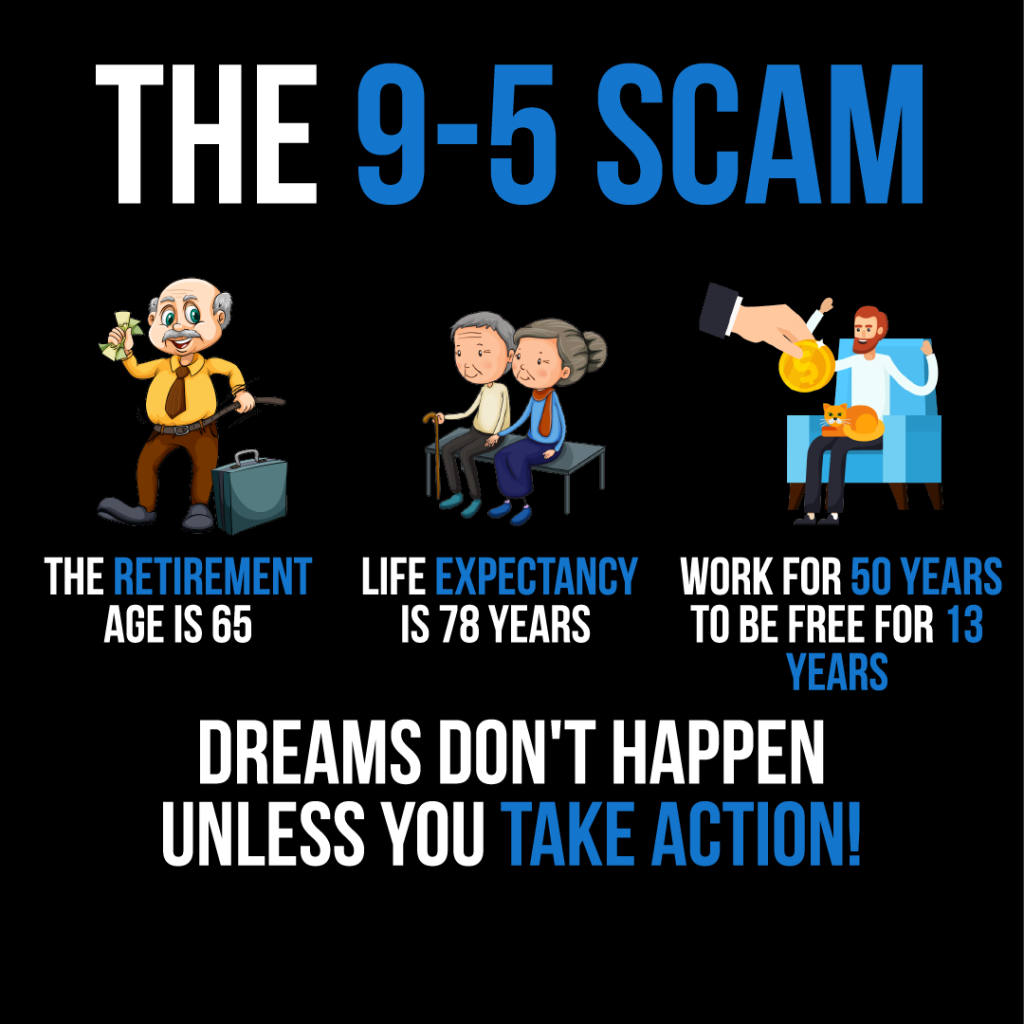

Figure: The infographic titled "The 9-5 Scam" presents a critical view of traditional work life. It points out that with a life expectancy of 78 years and a retirement age of 65, one would work for 50 years only to be free for 13 years. The message "Dreams don't happen unless you take action!" suggests that relying solely on a 9-5 job may not be the most effective path to fulfilling one's dreams. This visual is a call to action for individuals to take proactive steps towards their goals, possibly implying the pursuit of alternative income streams or early retirement strategies. For practical use, users should consider their long-term life and financial goals and explore various ways to achieve them beyond the conventional employment paradigm. Source: Custom Infographic

13.1 Understanding Social Security

社会保障基金: Social Security is funded through payroll taxes collected under the Federal Insurance Contributions Act (FICA). Both employees and employers contribute to this fund, which then provides benefits to retirees, disabled individuals, and survivors of deceased workers. Each paycheck has a deduction (typically 6.2% from the employee and 6.2% from the employer) funding future benefits. Understanding the funding method is crucial because changes in the workforce or tax rates could affect Social Security’s long-term sustainability.

这 average Social Security benefit for a retired worker in 2023 is approximately $1,827 per month, but this varies depending on lifetime earnings and the age at which benefits are claimed.

Typical sources of retirement income also include annuities, real estate rental income, reverse mortgages, and health savings accounts (HSAs) for medical expenses.

退休后的多种收入来源: Relying on a single source of retirement income, like Social Security may not be sufficient for a comfortable retirement. A diversified income strategy incorporating employer-sponsored plans and personal investments can offer a way to maintain financial security and flexibility during retirement.

雇主赞助的退休计划: Participating in these plans is critical, like a 401(k). Many employers offer a match to your contributions, which is essentially free money for your retirement fund. Maximizing your contribution to receive the full employer match can significantly impact your retirement savings. Employees should strive to contribute at least enough to receive the full employer match — otherwise, they are leaving free money on the table.

健康储蓄账户(HSA) are another valuable tool for retirement planning. HSAs allow tax-free savings for medical expenses in retirement, reducing the financial burden of healthcare costs.

Taxable vs Tax-Deferred vs Tax-Advantaged Accounts:

Taxable accounts (like brokerage accounts) do not offer any upfront tax benefits.

Tax-deferred accounts (like Traditional IRAs and 401(k)s) allow contributions to grow tax-free until retirement when withdrawals are taxed as income.

Tax-advantaged accounts (like Roth IRAs) involve paying taxes upfront, but earnings and qualified withdrawals are tax-free.”

Retirement vs Estate Planning:

Retirement planning focuses on ensuring financial independence during retirement by building savings through Social Security, employer plans, and personal investments.

Estate planning addresses how your assets will be distributed after your death and includes tools like wills, trusts, and beneficiary designations.

13.4 Estate Planning Tools:

Figure: A symbolic representation of retirement savings with a golden egg nestled securely, suggesting the importance of building a financial nest egg for the future.

将要: Legal document directing asset distribution after death.

生前遗嘱: Outlines healthcare wishes if incapacitated.

Trust: Allows assets to be managed and distributed without going through probate court.

Annuities and Pensions: Can provide income streams to support heirs. Understanding these tools ensures your wishes are honored and can reduce taxes or legal fees for your heirs