第14章 不動産と住宅所有

レッスンの学習目標:

Lorem ipsum dolor sit amet、consectetur adipiscing elit。ウト・エリート・テルス、ルクトゥス・ネク・ウラムコーペル・マティス、プルヴィナー・ダピブス・レオ。

不動産と住宅所有には、契約の理解、住宅購入の決定に対する経済状況の影響、賃貸と購入の金銭的影響などが含まれます。ここでは、不動産購入の複雑な決定を個人が理解できるように、これらの側面について考察します。

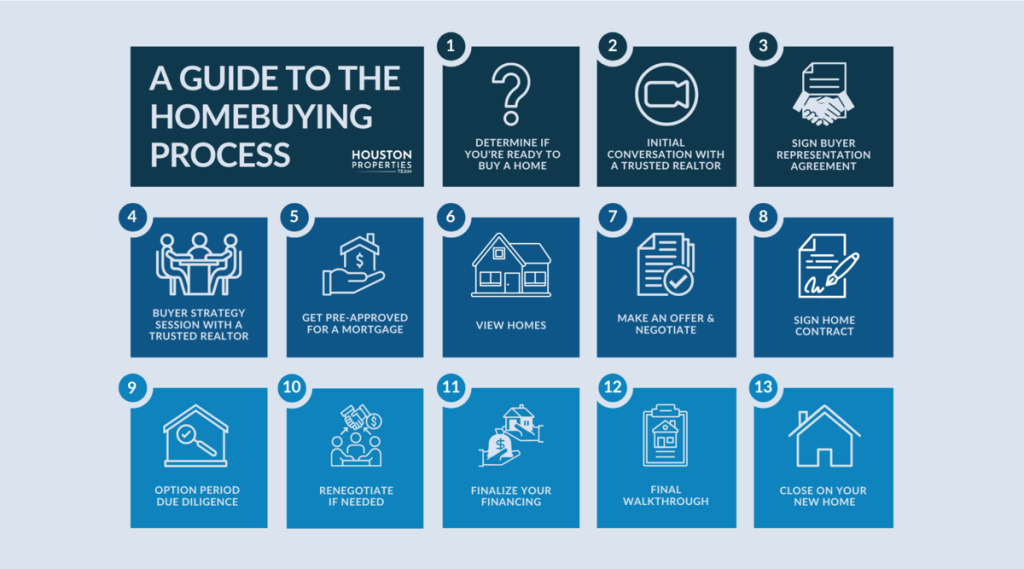

形: A Guide to the Homebuying Process

説明:

This infographic provides a step-by-step visual guide to the homebuying process, outlining the journey from the initial thought of buying to finally receiving the keys. It breaks down the complex process into manageable stages, such as financial preparation, house hunting, and the final closing. The purpose is to demystify the experience for potential homebuyers so they know what to expect.

重要なポイント:

- The homebuying process starts long before you look at houses; the first step is financial preparation, which includes getting pre-approved for a mortgage to set your budget.

- A crucial phase after finding a home and having an offer accepted is the 適当な注意 period, which involves a home inspection to assess the property’s condition.

- The process involves several key professionals, including a real estate agent, a loan officer, and an inspector, who guide you through the various stages.

- The final step is the closing, where all legal documents are signed, funds are transferred, and ownership of the property officially passes to you.

情報の応用:

- This guide acts as a valuable checklist for prospective homebuyers, helping you understand each step and stay organized throughout the purchasing journey.

- By knowing what’s coming next, you can proactively prepare your finances and documents, leading to a smoother and less stressful transaction.

- This knowledge empowers you to make more confident and informed financial decisions at every stage, from choosing the right loan to negotiating the final sale price.

14.1 Understanding Contracts

主な利用規約:

- 契約契約書には、デジタル形式か紙形式かを問わず、期間、解約条項、支払条件、紛争解決方法などの重要な条件が含まれます。これらの条件を理解することは、お客様の権利と責任を守るために不可欠です。

不動産取引であれ、Web アプリケーション契約であれ、契約には、関係するすべての当事者の義務と権利を規定するいくつかの重要な条項が含まれます。その内訳は次のとおりです。

1. Duration

Definition: Specifies how long the contract remains valid. It includes the start and end dates, and may outline renewal conditions (automatic or optional).

例:

A cell phone contract might state: “This agreement begins on January 1, 2025, and remains in effect until December 31, 2026. The contract will automatically renew for another 12 months unless canceled in writing 30 days prior to the expiration date.”

2. Termination

Definition: Outlines how and when either party may end the agreement before the official end date, including any penalties or notice requirements.

例:

In a rental lease agreement: “The tenant may terminate the lease with 60 days’ written notice and payment of a $500 early termination fee. The landlord may terminate for non-payment of rent or lease violations with 30 days’ notice.”

3. Payment Terms

Definition: Describes the amounts owed, when payments are due, acceptable payment methods, and consequences for late or missed payments.

例:

A freelance graphic designer contract might read: “The client agrees to pay $2,000 in two installments: 50% upfront, and 50% upon project completion. Late payments incur a 5% penalty after 10 business days.”

4. Dispute Resolution

Definition: Identifies the process to follow if disagreements arise, such as mediation, arbitration, or litigation, and the location where disputes will be settled.

例:

A software subscription agreement may state: “Any disputes arising from this agreement will be resolved through binding arbitration in the state of California. The parties waive their right to a jury trial.”

5. Privacy and Sharing of Personal Information

Definition: Explains how your personal data is collected, used, stored, and whether it’s shared with third parties. Must comply with data protection laws like GDPR (EU) or CCPA (California).

例:

A budgeting app’s privacy policy might say: “We collect your name, email address, and banking data to provide our services. We do not sell your information to third parties. You can request data deletion under the CCPA.”

⚠️ Tip: Always read these clauses before agreeing, especially in digital contracts like signing up for apps or services. Your data may be shared with partners for marketing or analytics purposes.

6. Privacy Policies and Data Sharing Terms

Definition: These terms clarify how a company collects, stores, uses, and potentially shares personal information. They often reference compliance with regulations like the General Data Protection Regulation (GDPR) in Europe or the California Consumer Privacy Act (CCPA) in the U.S.

例:

When signing up for a social media app, you might see:

“By using our services, you agree to our privacy policy. We collect data such as your location, browsing history, and contacts. This data may be shared with advertisers to personalize your experience. You may opt out of data sharing in your settings, and request deletion of your data at any time.”

現実のシナリオ: 人気の予算管理アプリをダウンロードする前に、ジェイミーは利用規約を徹底的に読み、個人の財務データが安全に保たれるようにプライバシー ポリシーに重点を置いています。

14.2 Economic and Labor Market Conditions

住宅決定への影響:

- 景気の低迷や労働市場の変化は収入の安定性に大きく影響し、個人が賃貸を選択するか購入するかに影響を及ぼします。雇用の安定は重要な考慮事項になります。

- 技術の進歩は、新たなキャリアの機会を生み出す一方で、特定の仕事を時代遅れにし、長期的な住宅の決定に影響を与える可能性があります。

- 経済の低迷は、個人の教育、経験、雇用形態、民族、性別に応じて不均衡な影響を及ぼします。

- 教育や経験の少ない人、臨時労働者やギグワーカー、特定の民族グループは、失業率が高くなる可能性があります。

- 経済の回復力は、多くの場合、高い教育レベル、専門的なスキルセット、および景気循環の影響を受けにくい産業と相関関係にあります。

現実のシナリオ: 大手テクノロジー企業が人員削減を発表した後、アレックスは頭金を貯めていたにもかかわらず、就職の見通しが不透明な中で住宅所有よりも経済的な柔軟性を優先し、賃貸生活を続けることにしました。

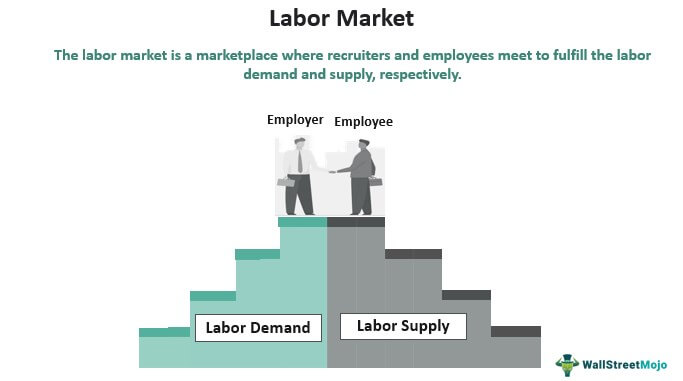

形: Understanding the Labor Market

説明:

This image provides a clear and simple definition of the labor market, the system where employment and wages are determined. It visually represents the two core components: the supply of labor, which comes from individuals seeking work, and the demand for labor, which comes from businesses looking to hire. The graphic explains that the interaction between these two forces sets the price of labor, which is the wage level.

重要なポイント:

- の labor market is the broad term for the interaction between workers (supply) and employers (demand).

- の “price” of labor is the wage, which tends to increase when demand for workers is high and the supply of qualified workers is low.

- Key metrics used to analyze the health of the labor market include the 失業率 そしてその labor force participation rate.

- A “tight” labor market, where there are more job openings than available workers, generally gives more bargaining power to employees.

情報の応用:

- The health of the labor market is a critical indicator of the overall health of the economy, making it essential information for investors and policymakers.

- As an individual, understanding labor market trends can help you make informed career choices by identifying industries and skills that are in high demand.

- For investors, positive labor market news, such as strong job growth, often signals a growing economy, which can be beneficial for corporate profits and the 株式市場.

14.3 Renting vs. Buying

財務および個人的な考慮事項:

- 若い成人は、住宅所有に伴う長期的な金銭的負担や維持管理の責任を避け、柔軟性のある賃貸を好むかもしれません。

- 賃貸と購入のコストとメリットを比較するには、月々の支払い、住宅の潜在的な価値上昇、個人のライフスタイルの好みを分析する必要があります。

賃貸か購入かの決定は、経済状況、ライフスタイルの好み、長期計画によって左右されます。比較すると次のようになります。

- レンタルの短期的なコストとメリット:

- 初期費用が低い(保証金と頭金)。

- 動きやすい柔軟性。

- メンテナンス費用はかかりません。

- 購入の長期的なコストとメリット:

- 不動産価値が上昇する可能性。

- 時間の経過とともに資産価値が高まります。

- 住宅ローン利子の税控除の可能性

現実のシナリオ: サラは、自分の住む街で賃貸と購入を比較しています。彼女は、毎月の住宅ローンの支払いは賃貸よりも高くなるかもしれないが、住宅資産価値が増加する可能性があることから、長期的には購入が経済的に健全な決定であると計算しています。

In some cases, individuals may encounter rent-to-own agreements, especially for homes or furniture. While renting-to-own offers flexibility and the chance to eventually own the property or item, it often results in paying significantly more over time compared to buying outright.

Buying a home directly builds equity and may lead to long-term financial stability, while renting (or rent-to-own) provides short-term flexibility but little or no ownership benefits until all payments are made.

賃貸契約の主な用語

1. Lease Term: Duration of the rental agreement

- 意味: Specifies the length of time the tenant agrees to rent the property.

- 例:

A lease agreement states: “This lease shall begin on August 1, 2025, and end on July 31, 2026.”

This indicates a 12-month lease term during which both the landlord and tenant are bound by the lease conditions.

2. Security Deposit: Funds held by the landlord as insurance against damage or unpaid rent

- 意味: A refundable amount paid upfront to cover potential property damage or lease violations.

- 例:

Upon signing a lease, John pays $1,200 as a security deposit in addition to his first month’s rent. When he moves out, the landlord inspects the apartment. Because John left a hole in the wall and didn’t clean the carpets, the landlord keeps $300 to cover the repairs and refunds the remaining $900.

3. Grace Period: Time allowed after the due date for rent payments without penalty

- 意味: A short period during which late payments are accepted without a fee.

- 例:

A lease states: “Rent is due on the 1st of each month. A 5-day grace period is provided before late fees are applied.”

If Maria pays her rent on the 4th, she avoids a penalty; if she pays on the 6th, she owes a $50 late fee.

4. Eviction: Legal process by which a tenant is removed for violating lease terms

- 意味: The formal removal of a tenant from the rental property due to non-payment or other breaches.

- 例:

After failing to pay rent for two months and ignoring multiple notices, David receives an official eviction notice from the landlord. The court sets a hearing, and eventually David is legally required to vacate the property within 10 days.

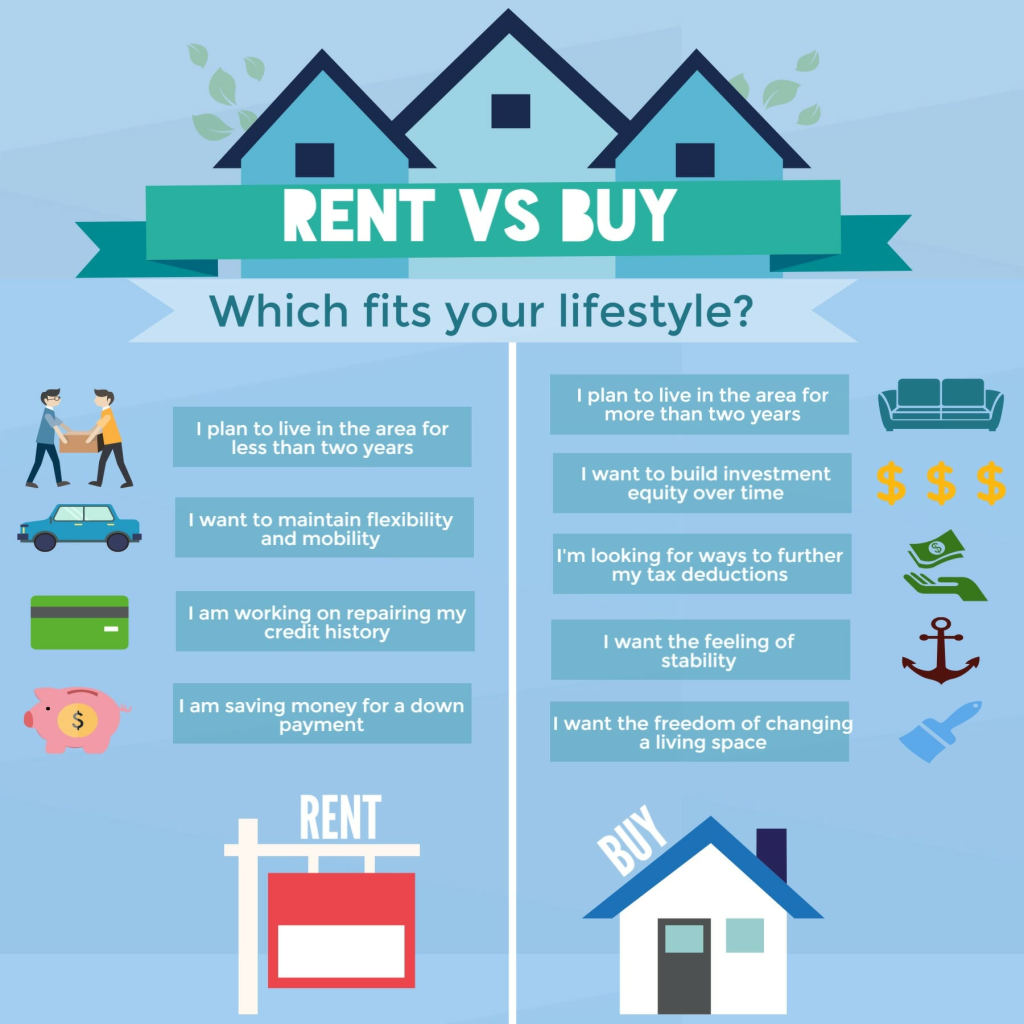

形: Renting vs. Buying a Home: A Comparison

説明:

This image provides a side-by-side comparison of the pros and cons of renting versus buying a home. It breaks down the key differences between the two choices, focusing on factors like cost, responsibility, and financial benefits. The goal is to provide a balanced overview to help individuals make an informed decision that suits their lifestyle and financial situation.

重要なポイント:

- The main advantage of renting is flexibility, as it’s easier to move, and you are not responsible for maintenance costs or property taxes.

- The primary benefit of buying a home is building equity, which is a form of forced savings that helps you grow your net worth over time.

- Homeownership comes with significant additional costs beyond the mortgage payment, including repairs, insurance, and property taxes.

- The “rent vs. buy” decision is not purely financial; it is also a major lifestyle choice that depends on your long-term goals, career stability, and personal preferences.

情報の応用:

- This framework provides a clear checklist of factors to consider when you are making the major financial decision of whether to rent or buy.

- It encourages you to analyze your complete financial picture, including your savings for a down payment and your ability to cover unexpected maintenance costs.

- By weighing these pros and cons against your personal goals and financial stability, you can make a choice that best supports your long-term financial well-being.

14.4 Mortgage Basics

担保付ローンおよび住宅ローン:

- 住宅ローン 担保付きローンであり、購入した住宅が担保となります。クレジットカードローンなどの無担保債務とは異なり、支払いが滞ると差し押さえにつながる可能性があります。

- 固定金利住宅ローンと変動金利住宅ローン (ARM) などの住宅ローンの条件を理解することは重要です。固定金利住宅ローンでは支払いが予測可能ですが、変動金利住宅ローンでは初期金利は低くなりますが、将来的に支払い額が増加するリスクがあります。

- 購入される不動産は通常、 担保 住宅ローンの場合、借り手が支払いを怠った場合、貸し手はローン金額を回収するために不動産を差し押さえる権利を持ちます。

Real-Life Scenario: Considering a stable job and a preference for predictable payments, Chris opts for a 30-year fixed-rate mortgage over an ARM when purchasing a first home, valuing long-term financial stability.

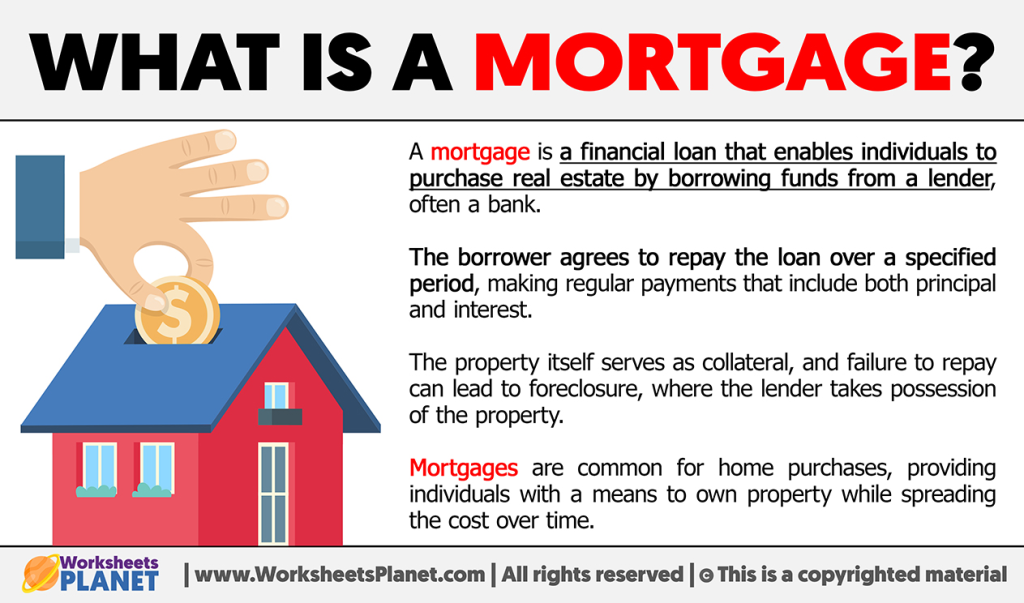

形: What is a Mortgage?

説明:

This image provides a simple, educational overview of what a モーゲージ is, explaining it as a loan used to purchase a home. It likely illustrates the core relationship where a lender provides a large sum of money to a borrower, who then repays it in installments over many years. The goal is to define this fundamental financial concept in an easy-to-understand visual format.

重要なポイント:

- あ モーゲージ is a specific type of long-term loan from a bank or financial institution that helps you buy a house.

- The property you buy with the loan serves as 担保, meaning the lender can take possession of the home if you fail to make your payments.

- Mortgages are typically repaid through regular monthly payments over a long period, commonly 15 to 30 years.

- Each monthly payment consists of two main parts: the principal (the original loan amount) and the 興味 (the cost of borrowing the money).

情報の応用:

- Understanding the concept of a モーゲージ is the foundational first step for anyone aspiring to achieve homeownership.

- This knowledge is critical for assessing your financial readiness to buy a home and for comparing different loan options from various lenders.

- Grasping the long-term commitment of a mortgage helps you make a responsible and well-informed financial decision when purchasing what is likely your largest asset.

Key Mortgage Qualification Factors

When applying for a mortgage, two important financial ratios lenders consider are:

- Debt-to-Income (DTI) Ratio:

Measures how much of your monthly income goes toward debt payments.

例: If your total debt payments are $1,800 and your monthly income is $5,000, your DTI = 36%.

Lenders typically prefer a DTI below 36%.

- Loan-to-Value (LTV) Ratio:

Compare the size of your mortgage to the home’s value.

例: If you buy a $250,000 home with a $50,000 down payment, your loan is $200,000. Your LTV = 80%.

A lower LTV reduces lender risk and can help you avoid private mortgage insurance (PMI).

Understanding these ratios can improve your chances of qualifying for better mortgage terms.

14.5 Comparing Mortgage Payments

ローン期間 | 借入金額 | 金利 | 月額支払い |

30年 | $250,000 | 4.0% | $1,193.54 |

15年 | $250,000 | 3.5% | $1,787.21 |

30年 | $350,000 | 4.5% | $1,773.40 |

15年 | $350,000 | 4.0% | $2,584.17 |

計算は説明目的であり、固定金利に基づいています。実際の支払額は、特定のローン条件と変動金利によって異なる場合があります。

これらの例は、ローンの条件、金額、金利の違いが月々の住宅ローンの支払額に大きく影響することを示しています。返済期間が長くなると、通常、月々の支払額は少なくなりますが、ローンの期間全体で支払う利息の合計額は高くなります。

14.6 Homeownership Costs

住宅を所有すると、継続的な費用が発生するため、住宅所有の予算を立てる際には、その費用を考慮する必要があります。これらの費用には、次のようなものがあります。

- 固定資産税: 固定資産税は、不動産の評価額に基づいて地方自治体によって課税されます。税率は居住地によって異なり、時間の経過とともに変更されることもあります。固定資産税は通常、年ごとまたは半年ごとに支払われ、月々の住宅ローンの支払いに含まれることがよくあります。

- 住宅所有者保険: Homeowner’s insurance protects you from financial losses due to damage to your property or personal liability. The cost of homeowner’s insurance depends on factors such as your home’s value, location, and coverage limits. Shop around and compare quotes from multiple insurance providers to find the best policy for your needs. Homeowners’ insurance typically covers damages to the home from events like fire, storms, theft, and certain natural disasters. It also includes liability coverage if someone is injured on the property.

- Renters’ insurance, on the other hand, covers personal belongings inside a rented property, such as clothing, electronics, and furniture, but ない the building structure itself.

Both types of insurance are important for protecting against unexpected losses.

- メンテナンスと修理: 住宅所有者は、所有物件の維持管理と必要な修理を行う責任があります。芝生の手入れ、雨どいの清掃、空調設備の点検などの定期的なメンテナンス作業は、時間が経つにつれて費用がかさみます。さらに、屋根の交換や配管の問題などの予期しない修理には費用がかかることがあります。こうした継続的な費用を予算に組み、予期しない費用に備えて緊急資金を確保しておくことが重要です。

不動産と住宅所有のさまざまな側面を理解することで、情報に基づいた決定を下し、住宅の購入、資金調達、維持という複雑な世界を切り抜けることができます。Simple Financial Community は、あなたの金融の旅をサポートし、住宅所有の目標に最適な選択を行うのに役立つリソースとガイダンスを提供します。

14.7 Tenant and Landlord Rights and Responsibilities

Rental lease agreements outline important rights and obligations:

- Tenants have the right to a safe, habitable living environment and are responsible for timely rent payments and maintaining the property.

- Landlords have the right to collect rent and expect property upkeep, but must handle repairs and maintenance promptly.

Understanding these terms protects both parties and helps prevent legal disputes.

結論

不動産や住宅所有をうまく進めるには、契約、経済状況、個人の状況を慎重に考慮する必要があります。賃貸か購入かの選択、住宅ローンの選択肢の理解、投資ベンチマークの比較など、情報に基づいた決定は、不動産の分野でより大きな満足感と経済的幸福につながります。

主なレッスン情報:

Lorem ipsum dolor sit amet、consectetur adipiscing elit。ウト・エリート・テルス、ルクトゥス・ネク・ウラムコーペル・マティス、プルヴィナー・ダピブス・レオ。