محليًا: تحليل الشركات الأوروبية

أهداف تعلم الدرس:

- Learn about the income statement under IFRS. You will understand how revenues, نفقات، و صافي الدخل are reported, along with the inclusion of other comprehensive income (OCI). This helps investors assess a company’s profitability and financial performance.

- Understand the balance sheet under IFRS. The balance sheet provides a snapshot of a company’s أصول, الإلتزامات، و عدالة, offering insights into the company’s financial position. Learn about the distinctions between current and non-current items and how they reflect a company’s liquidity and solvency.

- Explore the cash flow statement under IFRS. The cash flow statement outlines how cash is generated and used across operating, الاستثمار، و financing activities. You will learn how this statement helps assess a company’s liquidity and its ability to generate cash to fund operations and investments.

- Gain insights into the overall structure and application of IFRS in European financial reporting. Understanding IFRS helps ensure transparency and comparability, making it easier to analyze financial statements and make informed investment decisions across borders.

مقدمة

Understanding the core financial concepts is essential for any investor. Financial statements provide critical insights into a company’s financial health and performance, helping investors evaluate profitability, liquidity, and growth potential. This section will introduce the fundamental financial statements—بيان الدخل, الميزانية العمومية، و cash flow statement—and explain how to analyze these documents. We will also discuss key financial data points that investors use to assess a company’s performance.

22.1 Financial Statements

When analyzing European companies, it’s essential to understand that their financial statements are typically prepared according to the International Financial Reporting Standards (IFRS), a global accounting framework that ensures transparency and comparability across borders. In Europe, IFRS is mandatory for all publicly listed companies, providing investors with consistent and clear financial information. This section introduces how financial statements in Europe adhere to IFRS, ensuring high-quality reporting.

IFRS and Income Statement

Under IFRS, the بيان الدخل (also called the statement of comprehensive income) follows a structured approach, similar to financial statements globally, but with some unique European nuances. The income statement provides detailed insight into a company’s revenues, costs, and overall profitability.

- Revenue Recognition: Under IFRS, revenue is recognized when control of a product or service is transferred to the customer. European companies must adhere to these rules, ensuring that revenues are reported accurately based on performance obligations, not just when payments are received.

- مصاريف التشغيل: Expenses are classified by either their nature (e.g., wages, materials) or their function (e.g., cost of sales, administrative expenses). This flexibility allows European companies to present their income statements in a way that best reflects their operational structure.

- Other Comprehensive Income: IFRS emphasizes the importance of other comprehensive income (OCI), which includes gains or losses not reflected in the net income, such as foreign exchange differences or revaluation of financial instruments. This is particularly relevant for European companies operating in multiple currencies.

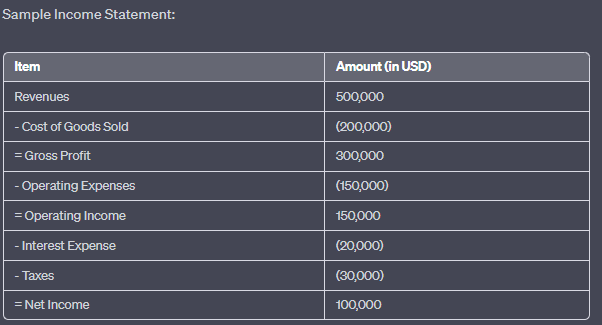

شكل: نموذج بيان الدخل

وصف:

The image presents a sample income statement, breaking down the financial performance of a company over a specific period. It starts with the total revenues and subtracts various expenses to arrive at the net income. The statement showcases the following items:

الإيرادات: $500,000

تكلفة البضائع المباعة: $(200,000)

إجمالي الربح: $300,000

مصاريف التشغيل: $(450,000)

الدخل التشغيلي: $150,000

مصاريف الفائدة: $(20,000)

الضرائب: $(30,000)

صافي الدخل: $100,000

الماخذ الرئيسية:

- الإيرادات:إجمالي المبلغ الذي جلبته الشركة قبل أي نفقات.

- تكلفة البضائع المباعة (COGS): التكاليف المباشرة المنسوبة إلى إنتاج البضائع المباعة.

- إجمالي الربح:الربح الذي تحققه الشركة بعد خصم تكاليف البضائع المباعة من إجمالي إيراداتها.

- مصاريف التشغيل:التكاليف المرتبطة بالعمليات اليومية للشركة.

- الدخل التشغيلي:الربح من العمليات التجارية (قبل الفوائد والضرائب).

- مصاريف الفائدة:تكلفة اقتراض الأموال.

- الضرائب:المبلغ المدفوع للحكومة بناءً على الدخل الخاضع للضريبة للشركة.

- صافي الدخل:الربح الإجمالي للشركة بعد خصم كافة النفقات من الإيرادات.

تطبيق المعلومات:

بيان الدخل وثيقة مالية أساسية تُقدم للمستثمرين وأصحاب المصلحة نظرةً ثاقبةً على ربحية الشركة خلال فترة زمنية محددة. من خلال تحليل بيان الدخل، يُمكن فهم مصادر إيرادات الشركة، وهيكل تكاليفها، ووضعها المالي العام. تُعدّ هذه البيانات بالغة الأهمية لاتخاذ قرارات استثمارية مدروسة وتقييم الكفاءة التشغيلية للشركة.

22.2 IFRS and Balance Sheet (Statement of Financial Position)

ال الميزانية العمومية, known under IFRS as the statement of financial position, provides a snapshot of a company’s assets, liabilities, and equity. IFRS requires companies to clearly differentiate between current and non-current items to offer a transparent view of a company’s financial health.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

- الإلتزامات: Under IFRS, liabilities are also divided into حاضِر (due within a year) and non-current. European companies must report their obligations, including debt, leases, and pensions, in this format, providing clear insights into their short-term and long-term obligations.

- Shareholders’ Equity: The shareholders’ equity section under IFRS is structured to show both contributed capital (from shareholders) and retained earnings (profits that have been reinvested into the business). European firms must also disclose other reserves, including revaluation reserves and foreign currency translation adjustments.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

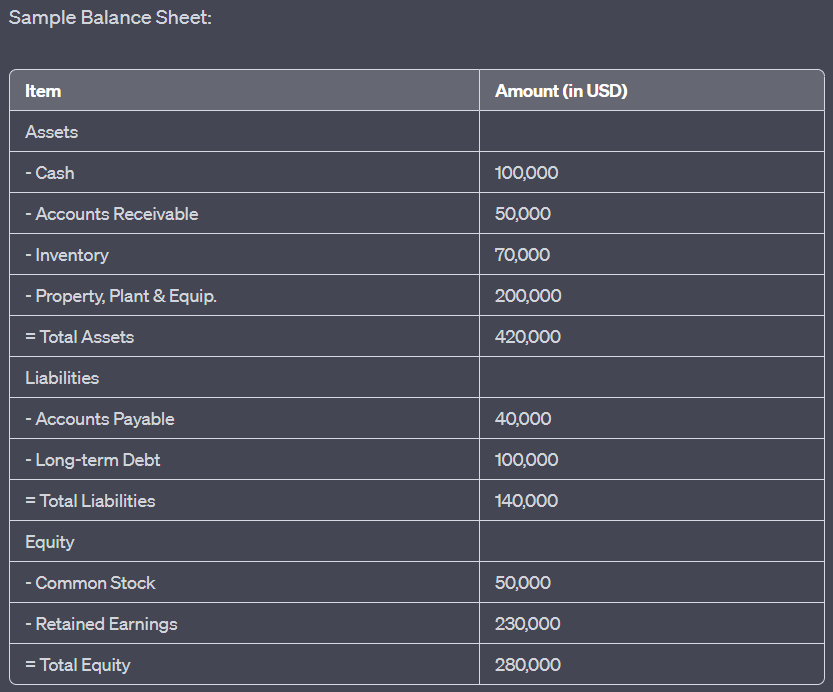

شكل: Sample Balance Sheet

وصف:

The image displays a sample balance sheet, which provides a snapshot of a company’s financial position at a specific point in time. It categorizes the company’s resources (assets) and the claims against those resources (liabilities and equity). The balance sheet showcases the following items:

- أصول: إجمالي $420,000، بما في ذلك النقد ($400,000)، والحسابات المدينة ($50,000)، والمخزون ($70,000)، والممتلكات والمصانع والمعدات ($200,000).

- الإلتزامات: إجمالي قدره $140,000، يشمل الحسابات الدائنة ($40,000) والديون طويلة الأجل ($400,000).

- عدالة: إجمالي $280,000، مع الأسهم العادية ($50,000) والأرباح المحتجزة ($230,000).

الماخذ الرئيسية:

- أصول: الموارد المملوكة للشركة والتي لها قيمة اقتصادية.

- الإلتزامات:الالتزامات المترتبة على الشركة تجاه الجهات الخارجية.

- عدالة: يمثل حصة الملكية في الشركة، بما في ذلك الأموال المستثمرة من قبل المساهمين والأرباح المتراكمة.

- المعادلة المحاسبية الأساسية: الأصول = الخصوم + حقوق الملكية.

\(\textbf{Accounting Equation:}\)

\[ \displaystyle \text{Assets} = \text{Liabilities} + \text{Equity} \]

\(\textbf{الأسطورة:}\)

\(\text{Assets}\) = Total assets

\(\text{Liabilities}\) = Total liabilities

\(\text{Equity}\) = Total equity

تطبيق المعلومات:

A balance sheet is a foundational financial statement that offers insights into a company’s financial health. By analyzing the balance sheet, stakeholders can assess the company’s liquidity, solvency, and overall financial stability. This information is vital for investors, creditors, and other stakeholders to make informed decisions related to the company’s financial position

22.3 IFRS and Cash Flow Statement

ال cash flow statement under IFRS follows a similar structure to other global standards but places particular emphasis on transparency in how cash is generated and used by the company. European companies use this statement to report cash flows from operating, investing, and financing activities.

- الأنشطة التشغيلية: IFRS allows for flexibility in reporting cash flows from operating activities, either through the direct method (showing cash receipts and payments) or the indirect method (starting with net income and adjusting for non-cash items). Most European companies opt for the indirect method.

- Investing and Financing Activities: Cash flows related to investments in assets or securities and activities such as issuing shares or repaying debt are reported here. European companies must clearly distinguish these transactions to show how they are funding their growth and managing their financial obligations.

- Foreign Exchange Impacts: Given that many European companies operate across multiple countries and currencies, IFRS requires the inclusion of cash flow impacts due to changes in foreign exchange rates, providing investors with a clearer understanding of how currency movements affect a company’s cash position.

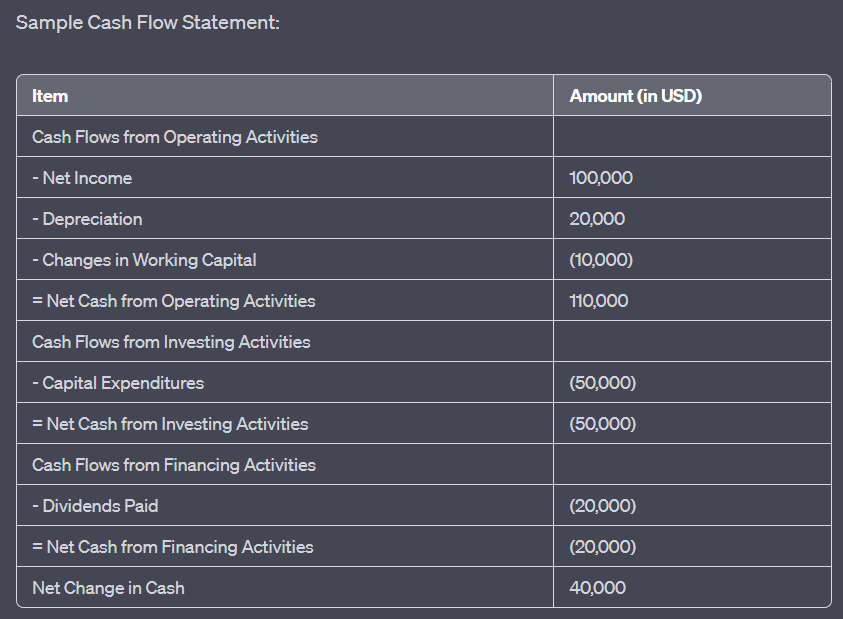

شكل: Sample Cash Flow Statement

وصف:

The image illustrates a sample cash flow statement, which provides a detailed account of the cash inflows and outflows for a company over a specific period. The statement is segmented into three main categories: Operating Activities, Investing Activities, and Financing Activities. The key items include:

التدفقات النقدية من الأنشطة التشغيلية: صافي الدخل ($100,000)، والإهلاك ($20,000)، والتغيرات في رأس المال العامل (-$10,000)، مما أدى إلى صافي النقد من الأنشطة التشغيلية بقيمة $110,000.

التدفقات النقدية من أنشطة الاستثمار: النفقات الرأسمالية (-$50,000)، مما أدى إلى صافي النقد من أنشطة الاستثمار بمقدار -$50,000.

التدفقات النقدية من أنشطة التمويل: تم دفع أرباح الأسهم (-$20,000)، مما أدى إلى صافي النقد من أنشطة التمويل بمبلغ -$20,000.

إجمالي التغيير الصافي في النقد هو $40,000.

الماخذ الرئيسية:

- الأنشطة التشغيلية:يعكس النقد الناتج أو المستخدم في العمليات التجارية الأساسية.

- أنشطة الاستثمار:يمثل النقد المستخدم في الاستثمارات في الأصول أو المستلم من بيع الأصول.

- أنشطة التمويل:يعرض التدفقات النقدية من أو إلى مصادر التمويل الخارجية، مثل المقرضين والمساهمين.

- يوفر صافي التغير في النقد صورة سريعة للزيادة أو النقصان الإجمالي في المركز النقدي للشركة خلال الفترة.

تطبيق المعلومات:

The cash flow statement is an essential financial tool that offers insights into a company’s liquidity and its ability to generate and use cash effectively. By analyzing the cash flow statement, stakeholders can understand how a company manages its cash resources, which is crucial for assessing its financial health and making informed investment decisions.

خاتمة

In Europe, financial statements are prepared according to IFRS, ensuring a high level of consistency, transparency, and comparability across countries and industries. The بيان الدخل, الميزانية العمومية، و cash flow statement under IFRS provide investors with the detailed information needed to assess the financial health of European companies. IFRS’s global standards ensure that European companies’ financial reports meet international expectations, making it easier for investors to analyze and compare firms operating in different regions.

معلومات الدرس الرئيسية:

- The income statement shows a company’s profitability. The income statement provides a breakdown of a company’s revenues, تكلفة البضائع المباعة (COGS), operating expenses، و صافي الدخل. By analyzing this statement, investors can evaluate how efficiently a company is generating profits and managing costs. Revenue recognition under IFRS ensures accurate reporting based on performance obligations.

- The balance sheet offers a snapshot of a company’s financial position. It categorizes a company’s أصول, الإلتزامات، و عدالة. By examining these elements, investors can assess a company’s السيولة (ability to meet short-term obligations), solvency (ability to meet long-term obligations), and الصحة المالية. The fundamental accounting equation ل assets = liabilities + equity is key to understanding this statement.

- The cash flow statement tracks how cash is used. The statement divides cash flows into operating, الاستثمار، و financing activities. By analyzing this statement, investors can understand how the company generates cash from its operations, how it funds investments, and how it manages external financing. Positive cash flow from operating activities signals a strong cash position.

كلمة الختام:

Financial statements under IFRS provide essential insights into a company’s financial health and performance. By analyzing the بيان الدخل, الميزانية العمومية، و cash flow statement, investors can make well-informed decisions based on transparency, consistency, and detailed reporting, helping them assess the company’s profitability, liquidity, and long-term sustainability.