ადგილობრივი: ევროპული კომპანიების ანალიზი

გაკვეთილის სწავლის მიზნები:

- Learn about the income statement under IFRS. You will understand how revenues, ხარჯებიდა net income are reported, along with the inclusion of other comprehensive income (OCI). This helps investors assess a company’s profitability and financial performance.

- Understand the balance sheet under IFRS. The balance sheet provides a snapshot of a company’s assets, liabilitiesდა კაპიტალი, offering insights into the company’s financial position. Learn about the distinctions between current and non-current items and how they reflect a company’s liquidity and solvency.

- Explore the cash flow statement under IFRS. The cash flow statement outlines how cash is generated and used across operating, ინვესტირებადა financing activities. You will learn how this statement helps assess a company’s liquidity and its ability to generate cash to fund operations and investments.

- Gain insights into the overall structure and application of IFRS in European financial reporting. Understanding IFRS helps ensure transparency and comparability, making it easier to analyze financial statements and make informed investment decisions across borders.

შესავალი

Understanding the core financial concepts is essential for any investor. Financial statements provide critical insights into a company’s financial health and performance, helping investors evaluate profitability, liquidity, and growth potential. This section will introduce the fundamental financial statements—შემოსავლის ანგარიშგება, ბალანსიდა cash flow statement—and explain how to analyze these documents. We will also discuss key financial data points that investors use to assess a company’s performance.

22.1 Financial Statements

When analyzing European companies, it’s essential to understand that their financial statements are typically prepared according to the International Financial Reporting Standards (IFRS), a global accounting framework that ensures transparency and comparability across borders. In Europe, IFRS is mandatory for all publicly listed companies, providing investors with consistent and clear financial information. This section introduces how financial statements in Europe adhere to IFRS, ensuring high-quality reporting.

IFRS and Income Statement

Under IFRS, the შემოსავლის ანგარიშგება (also called the statement of comprehensive income) follows a structured approach, similar to financial statements globally, but with some unique European nuances. The income statement provides detailed insight into a company’s revenues, costs, and overall profitability.

- Revenue Recognition: Under IFRS, revenue is recognized when control of a product or service is transferred to the customer. European companies must adhere to these rules, ensuring that revenues are reported accurately based on performance obligations, not just when payments are received.

- ოპერაციული ხარჯები: Expenses are classified by either their nature (e.g., wages, materials) or their function (e.g., cost of sales, administrative expenses). This flexibility allows European companies to present their income statements in a way that best reflects their operational structure.

- Other Comprehensive Income: IFRS emphasizes the importance of other comprehensive income (OCI), which includes gains or losses not reflected in the net income, such as foreign exchange differences or revaluation of financial instruments. This is particularly relevant for European companies operating in multiple currencies.

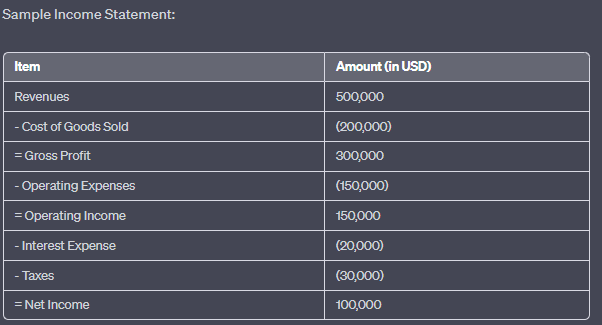

ფიგურა: შემოსავლების ანგარიშგების ნიმუში

აღწერა:

The image presents a sample income statement, breaking down the financial performance of a company over a specific period. It starts with the total revenues and subtracts various expenses to arrive at the net income. The statement showcases the following items:

შემოსავლები: $500,000

გაყიდული საქონლის ღირებულება: $ (200,000)

მთლიანი მოგება: $300,000

ოპერაციული ხარჯები: $ (450,000)

საოპერაციო შემოსავალი: $150,000

საპროცენტო ხარჯი: $(20,000)

გადასახადები: $(30,000)

წმინდა შემოსავალი: $100,000

ძირითადი დასკვნები:

- შემოსავლებიკომპანიის მიერ შემოტანილი თანხის მთლიანი ოდენობა ნებისმიერ ხარჯამდე.

- გაყიდული საქონლის ღირებულება (COGS): გაყიდული საქონლის წარმოებასთან დაკავშირებული პირდაპირი ხარჯები.

- მთლიანი მოგებამოგება, რომელსაც კომპანია იღებს მთლიანი შემოსავლიდან ხარჯთაღრიცხვის გამოკლების შემდეგ.

- ოპერაციული ხარჯები: ბიზნესის ყოველდღიურ საქმიანობასთან დაკავშირებული ხარჯები.

- საოპერაციო შემოსავალი: ბიზნეს ოპერაციებიდან მიღებული მოგება (პროცენტებისა და გადასახადების გადახდამდე).

- საპროცენტო ხარჯი: სახსრების სესხების ღირებულება.

- გადასახადები: კომპანიის დასაბეგრი შემოსავლის საფუძველზე მთავრობისთვის გადახდილი თანხა.

- წმინდა შემოსავალიკომპანიის მთლიანი მოგება შემოსავლებიდან ყველა ხარჯის გამოკლების შემდეგ.

ინფორმაციის გამოყენება:

მოგება-ზარალის ანგარიშგება არის ფუნდამენტური ფინანსური დოკუმენტი, რომელიც ინვესტორებსა და დაინტერესებულ მხარეებს აძლევს წარმოდგენას კომპანიის მომგებიანობის შესახებ კონკრეტულ პერიოდში. მოგება-ზარალის ანგარიშგების ანალიზით, შესაძლებელია კომპანიის შემოსავლების ნაკადების, ხარჯების სტრუქტურისა და საერთო ფინანსური მდგომარეობის გაგება. ეს მონაცემები გადამწყვეტია ინფორმირებული საინვესტიციო გადაწყვეტილებების მისაღებად და კომპანიის ოპერაციული ეფექტურობის შესაფასებლად.

22.2 IFRS and Balance Sheet (Statement of Financial Position)

ის ბალანსი, known under IFRS as the statement of financial position, provides a snapshot of a company’s assets, liabilities, and equity. IFRS requires companies to clearly differentiate between current and non-current items to offer a transparent view of a company’s financial health.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

- ვალდებულებები: Under IFRS, liabilities are also divided into მიმდინარე (due within a year) and non-current. European companies must report their obligations, including debt, leases, and pensions, in this format, providing clear insights into their short-term and long-term obligations.

- Shareholders’ Equity: The shareholders’ equity section under IFRS is structured to show both contributed capital (from shareholders) and retained earnings (profits that have been reinvested into the business). European firms must also disclose other reserves, including revaluation reserves and foreign currency translation adjustments.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

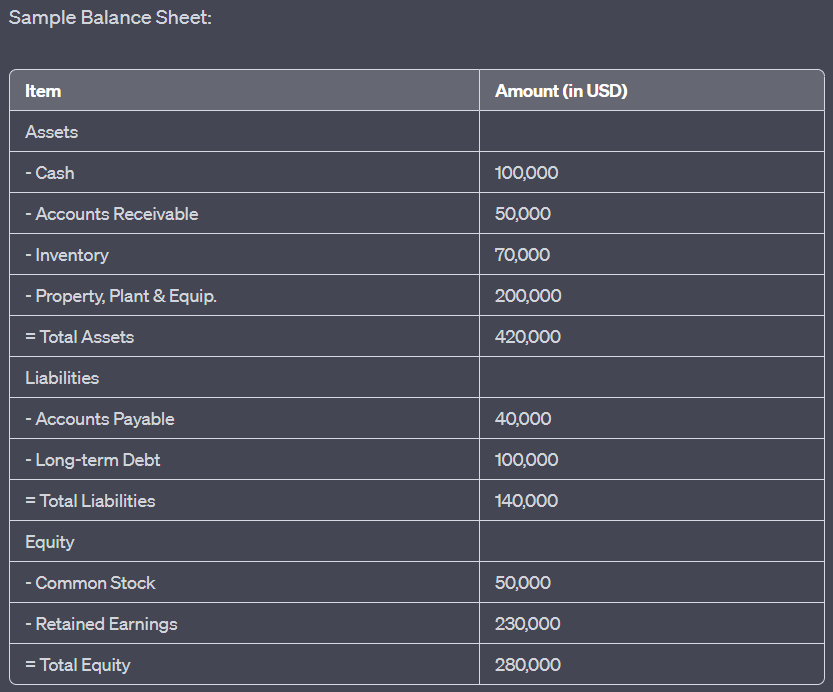

ფიგურა: Sample Balance Sheet

აღწერა:

The image displays a sample balance sheet, which provides a snapshot of a company’s financial position at a specific point in time. It categorizes the company’s resources (assets) and the claims against those resources (liabilities and equity). The balance sheet showcases the following items:

- აქტივები: სულ $420,000, მათ შორის ნაღდი ფული ($400,000), დებიტორული დავალიანება ($50,000), მარაგები ($70,000) და ძირითადი საშუალებები ($200,000).

- ვალდებულებები: სულ $140,000, რომელიც მოიცავს კრედიტორულ დავალიანებას ($40,000) და გრძელვადიან ვალს ($400,000).

- კაპიტალი: სულ $280,000, ჩვეულებრივი აქციებით ($50,000) და გაუნაწილებელი მოგებით ($230,000).

ძირითადი დასკვნები:

- აქტივები: კომპანიის საკუთრებაში არსებული რესურსები, რომლებსაც აქვთ ეკონომიკური ღირებულება.

- ვალდებულებებიკომპანიის ვალდებულებები გარე სუბიექტების წინაშე.

- კაპიტალი: წარმოადგენს კომპანიის საკუთრების წილს, მათ შორის აქციონერების მიერ ინვესტირებულ სახსრებსა და დაგროვილ მოგებას.

- ფუნდამენტური ბუღალტრული განტოლება: აქტივები = ვალდებულებები + საკუთარი კაპიტალი.

\(\textbf{Accounting Equation:}\)

\[ \displaystyle \text{Assets} = \text{Liabilities} + \text{Equity} \]

ლეგენდა:

\(\text{Assets}\) = Total assets

\(\text{Liabilities}\) = Total liabilities

\(\text{Equity}\) = Total equity

ინფორმაციის გამოყენება:

A balance sheet is a foundational financial statement that offers insights into a company’s financial health. By analyzing the balance sheet, stakeholders can assess the company’s liquidity, solvency, and overall financial stability. This information is vital for investors, creditors, and other stakeholders to make informed decisions related to the company’s financial position

22.3 IFRS and Cash Flow Statement

ის cash flow statement under IFRS follows a similar structure to other global standards but places particular emphasis on transparency in how cash is generated and used by the company. European companies use this statement to report cash flows from operating, investing, and financing activities.

- ოპერაციული საქმიანობა: IFRS allows for flexibility in reporting cash flows from operating activities, either through the direct method (showing cash receipts and payments) or the indirect method (starting with net income and adjusting for non-cash items). Most European companies opt for the indirect method.

- Investing and Financing Activities: Cash flows related to investments in assets or securities and activities such as issuing shares or repaying debt are reported here. European companies must clearly distinguish these transactions to show how they are funding their growth and managing their financial obligations.

- Foreign Exchange Impacts: Given that many European companies operate across multiple countries and currencies, IFRS requires the inclusion of cash flow impacts due to changes in foreign exchange rates, providing investors with a clearer understanding of how currency movements affect a company’s cash position.

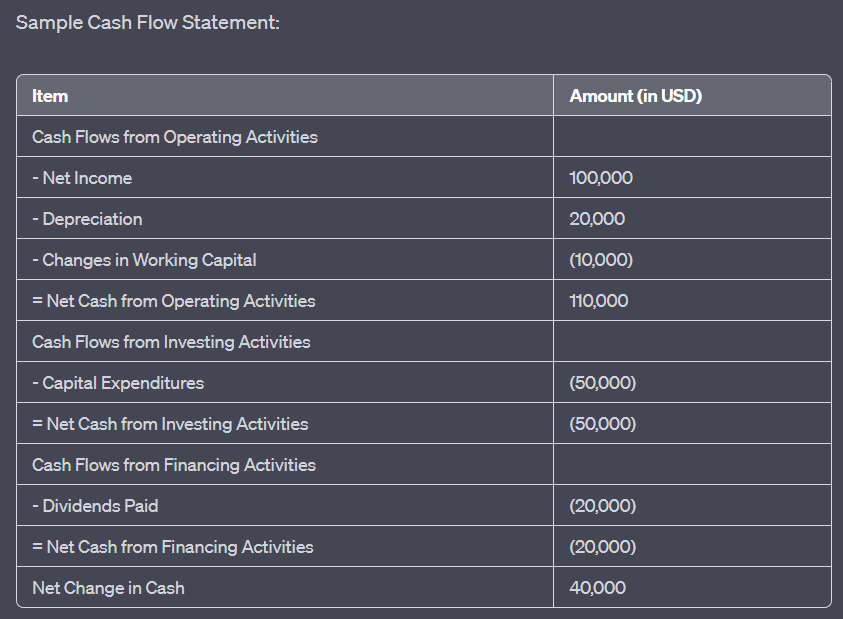

ფიგურა: Sample Cash Flow Statement

აღწერა:

The image illustrates a sample cash flow statement, which provides a detailed account of the cash inflows and outflows for a company over a specific period. The statement is segmented into three main categories: Operating Activities, Investing Activities, and Financing Activities. The key items include:

საოპერაციო საქმიანობიდან მიღებული ფულადი ნაკადები: წმინდა შემოსავალი ($100,000), ცვეთა ($20,000) და საბრუნავი კაპიტალის ცვლილებები (-$10,000), რაც საოპერაციო საქმიანობიდან მიღებულ წმინდა ფულად ნაკადს $110,000-ს შეადგენს.

საინვესტიციო საქმიანობიდან მიღებული ფულადი ნაკადები: კაპიტალური ხარჯები (-$50,000), რამაც საინვესტიციო საქმიანობიდან მიღებული წმინდა ფულადი რესურსი -$50,000-ის ოდენობით გამოიწვია.

ფინანსური საქმიანობიდან მიღებული ფულადი ნაკადები: გადახდილი დივიდენდები (-$20,000), რის შედეგადაც ფინანსური საქმიანობიდან მიღებული წმინდა ფულადი სახსრები -$20,000-ს შეადგენდა.

ნაღდი ფულის საერთო წმინდა ცვლილება 1 TP 4 40,000-ია.

ძირითადი დასკვნები:

- ოპერაციული საქმიანობაასახავს ძირითად ბიზნეს ოპერაციებში გენერირებულ ან გამოყენებულ ფულად რესურსებს.

- საინვესტიციო საქმიანობა: წარმოადგენს აქტივებში ინვესტიციებისთვის გამოყენებულ ან აქტივების გაყიდვიდან მიღებულ ნაღდ ფულს.

- დაფინანსების აქტივობებიაჩვენებს ფულადი ნაკადებს გარე დაფინანსების წყაროებიდან, როგორიცაა კრედიტორები და აქციონერები.

- ნაღდი ფულის წმინდა ცვლილება იძლევა კომპანიის ნაღდი ფულის პოზიციის საერთო ზრდის ან შემცირების სურათს პერიოდის განმავლობაში.

ინფორმაციის გამოყენება:

The cash flow statement is an essential financial tool that offers insights into a company’s liquidity and its ability to generate and use cash effectively. By analyzing the cash flow statement, stakeholders can understand how a company manages its cash resources, which is crucial for assessing its financial health and making informed investment decisions.

დასკვნა

In Europe, financial statements are prepared according to IFRS, ensuring a high level of consistency, transparency, and comparability across countries and industries. The შემოსავლის ანგარიშგება, ბალანსიდა cash flow statement under IFRS provide investors with the detailed information needed to assess the financial health of European companies. IFRS’s global standards ensure that European companies’ financial reports meet international expectations, making it easier for investors to analyze and compare firms operating in different regions.

გაკვეთილის ძირითადი ინფორმაცია:

- The income statement shows a company’s profitability. The income statement provides a breakdown of a company’s revenues, cost of goods sold (COGS), operating expensesდა net income. By analyzing this statement, investors can evaluate how efficiently a company is generating profits and managing costs. Revenue recognition under IFRS ensures accurate reporting based on performance obligations.

- The balance sheet offers a snapshot of a company’s financial position. It categorizes a company’s assets, liabilitiesდა კაპიტალი. By examining these elements, investors can assess a company’s liquidity (ability to meet short-term obligations), solvency (ability to meet long-term obligations), and ფინანსური ჯანმრთელობა. The fundamental accounting equation -ის assets = liabilities + equity is key to understanding this statement.

- The cash flow statement tracks how cash is used. The statement divides cash flows into operating, ინვესტირებადა financing activities. By analyzing this statement, investors can understand how the company generates cash from its operations, how it funds investments, and how it manages external financing. Positive cash flow from operating activities signals a strong cash position.

დასკვნითი განცხადება:

Financial statements under IFRS provide essential insights into a company’s financial health and performance. By analyzing the შემოსავლის ანგარიშგება, ბალანსიდა cash flow statement, investors can make well-informed decisions based on transparency, consistency, and detailed reporting, helping them assess the company’s profitability, liquidity, and long-term sustainability.