Local: analyzing European companies

Цілі навчання:

- Learn about the income statement under IFRS. You will understand how revenues, витрати, та net income are reported, along with the inclusion of other comprehensive income (OCI). This helps investors assess a company’s profitability and financial performance.

- Understand the balance sheet under IFRS. The balance sheet provides a snapshot of a company’s assets, liabilities, та equity, offering insights into the company’s financial position. Learn about the distinctions between current and non-current items and how they reflect a company’s liquidity and solvency.

- Explore the cash flow statement under IFRS. The cash flow statement outlines how cash is generated and used across operating, інвестування, та financing activities. You will learn how this statement helps assess a company’s liquidity and its ability to generate cash to fund operations and investments.

- Gain insights into the overall structure and application of IFRS in European financial reporting. Understanding IFRS helps ensure transparency and comparability, making it easier to analyze financial statements and make informed investment decisions across borders.

вступ

Understanding the core financial concepts is essential for any investor. Financial statements provide critical insights into a company’s financial health and performance, helping investors evaluate profitability, liquidity, and growth potential. This section will introduce the fundamental financial statements—звіт про доходи, баланс, та cash flow statement—and explain how to analyze these documents. We will also discuss key financial data points that investors use to assess a company’s performance.

22.1 Financial Statements

When analyzing European companies, it’s essential to understand that their financial statements are typically prepared according to the International Financial Reporting Standards (IFRS), a global accounting framework that ensures transparency and comparability across borders. In Europe, IFRS is mandatory for all publicly listed companies, providing investors with consistent and clear financial information. This section introduces how financial statements in Europe adhere to IFRS, ensuring high-quality reporting.

IFRS and Income Statement

Under IFRS, the звіт про доходи (also called the statement of comprehensive income) follows a structured approach, similar to financial statements globally, but with some unique European nuances. The income statement provides detailed insight into a company’s revenues, costs, and overall profitability.

- Revenue Recognition: Under IFRS, revenue is recognized when control of a product or service is transferred to the customer. European companies must adhere to these rules, ensuring that revenues are reported accurately based on performance obligations, not just when payments are received.

- Операційні витрати: Expenses are classified by either their nature (e.g., wages, materials) or their function (e.g., cost of sales, administrative expenses). This flexibility allows European companies to present their income statements in a way that best reflects their operational structure.

- Other Comprehensive Income: IFRS emphasizes the importance of other comprehensive income (OCI), which includes gains or losses not reflected in the net income, such as foreign exchange differences or revaluation of financial instruments. This is particularly relevant for European companies operating in multiple currencies.

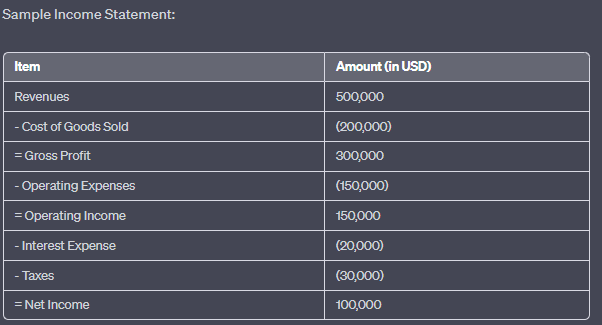

Малюнок: Зразок звіту про доходи

опис:

The image presents a sample income statement, breaking down the financial performance of a company over a specific period. It starts with the total revenues and subtracts various expenses to arrive at the net income. The statement showcases the following items:

Доходи: $500,000

Собівартість проданих товарів: $ (200 000)

Валовий прибуток: $300,000

Операційні витрати: $ (450 000)

Операційний дохід: $150,000

Відсоткові витрати: $(20 000)

Податки: $ (30 000)

Чистий прибуток: $100,000

Ключові висновки:

- ДоходиЗагальна сума грошей, залучених компанією, до будь-яких витрат.

- Собівартість реалізованої продукції (COGS): Прямі витрати, пов'язані з виробництвом проданих товарів.

- Валовий прибутокПрибуток, який компанія отримує після вирахування собівартості реалізованої продукції (COGS) від її загального доходу.

- Операційні витратиВитрати, пов'язані з щоденною діяльністю бізнесу.

- Операційний дохідПрибуток від господарської діяльності (до вирахування відсотків та податків).

- Відсоткові витратиВартість позикових коштів.

- ПодаткиСума, що сплачується уряду на основі оподатковуваного доходу компанії.

- Чистий прибутокЗагальний прибуток компанії після вирахування всіх витрат з доходів.

Застосування інформації:

Звіт про прибутки та збитки – це фундаментальний фінансовий документ, який надає інвесторам та зацікавленим сторонам уявлення про прибутковість компанії за певний період. Аналізуючи звіт про прибутки та збитки, можна зрозуміти потоки доходів компанії, структуру витрат та загальний фінансовий стан. Ці дані є вирішальними для прийняття обґрунтованих інвестиційних рішень та оцінки операційної ефективності компанії.

22.2 IFRS and Balance Sheet (Statement of Financial Position)

The баланс, known under IFRS as the statement of financial position, provides a snapshot of a company’s assets, liabilities, and equity. IFRS requires companies to clearly differentiate between current and non-current items to offer a transparent view of a company’s financial health.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

- Зобов'язання: Under IFRS, liabilities are also divided into поточний (due within a year) and non-current. European companies must report their obligations, including debt, leases, and pensions, in this format, providing clear insights into their short-term and long-term obligations.

- Shareholders’ Equity: The shareholders’ equity section under IFRS is structured to show both contributed capital (from shareholders) and retained earnings (profits that have been reinvested into the business). European firms must also disclose other reserves, including revaluation reserves and foreign currency translation adjustments.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

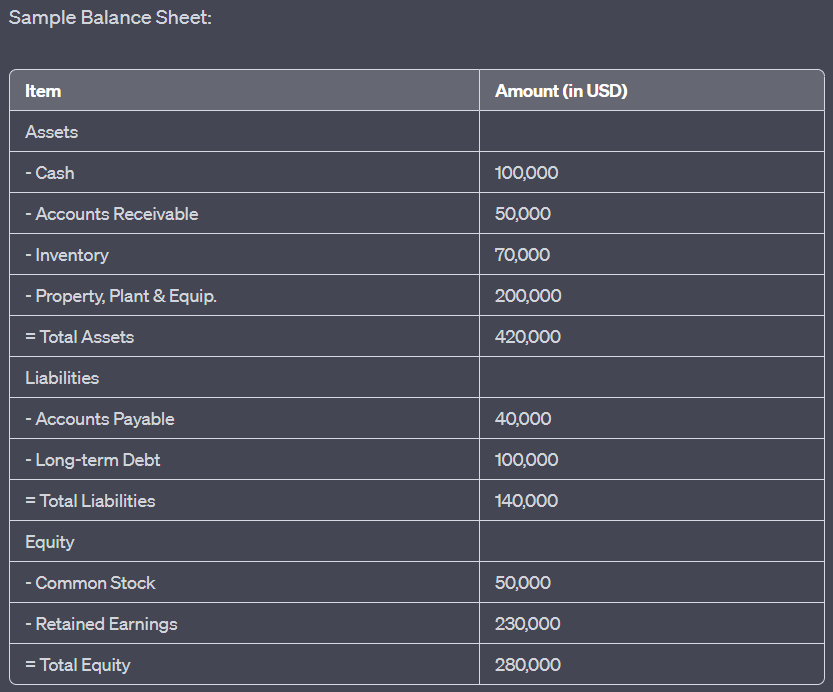

Малюнок: Sample Balance Sheet

опис:

The image displays a sample balance sheet, which provides a snapshot of a company’s financial position at a specific point in time. It categorizes the company’s resources (assets) and the claims against those resources (liabilities and equity). The balance sheet showcases the following items:

- Активи: Загальна сума $420 000, включаючи готівку ($400 000), дебіторську заборгованість ($50 000), запаси ($70 000) та основні засоби ($200 000).

- Зобов'язання: Загальна сума $140 000, включаючи кредиторську заборгованість ($40 000) та довгострокову заборгованість ($400 000).

- Акціонерний капітал: Загальна сума $280 000, включаючи звичайні акції ($50 000) та нерозподілений прибуток ($230 000).

Ключові висновки:

- Активи: Ресурси, що належать компанії та мають економічну цінність.

- Зобов'язанняЗобов'язання компанії перед зовнішніми організаціями.

- Акціонерний капітал: Представляє частку власності в компанії, включаючи кошти, інвестовані акціонерами, та накопичений прибуток.

- Фундаментальне бухгалтерське рівняння: Активи = Зобов'язання + Власний капітал.

\(\textbf{Accounting Equation:}\)

\[ \displaystyle \text{Assets} = \text{Liabilities} + \text{Equity} \]

\(\textbf{Legend:}\)

\(\text{Assets}\) = Total assets

\(\text{Liabilities}\) = Total liabilities

\(\text{Equity}\) = Total equity

Застосування інформації:

A balance sheet is a foundational financial statement that offers insights into a company’s financial health. By analyzing the balance sheet, stakeholders can assess the company’s liquidity, solvency, and overall financial stability. This information is vital for investors, creditors, and other stakeholders to make informed decisions related to the company’s financial position

22.3 IFRS and Cash Flow Statement

The cash flow statement under IFRS follows a similar structure to other global standards but places particular emphasis on transparency in how cash is generated and used by the company. European companies use this statement to report cash flows from operating, investing, and financing activities.

- Операційна діяльність: IFRS allows for flexibility in reporting cash flows from operating activities, either through the direct method (showing cash receipts and payments) or the indirect method (starting with net income and adjusting for non-cash items). Most European companies opt for the indirect method.

- Investing and Financing Activities: Cash flows related to investments in assets or securities and activities such as issuing shares or repaying debt are reported here. European companies must clearly distinguish these transactions to show how they are funding their growth and managing their financial obligations.

- Foreign Exchange Impacts: Given that many European companies operate across multiple countries and currencies, IFRS requires the inclusion of cash flow impacts due to changes in foreign exchange rates, providing investors with a clearer understanding of how currency movements affect a company’s cash position.

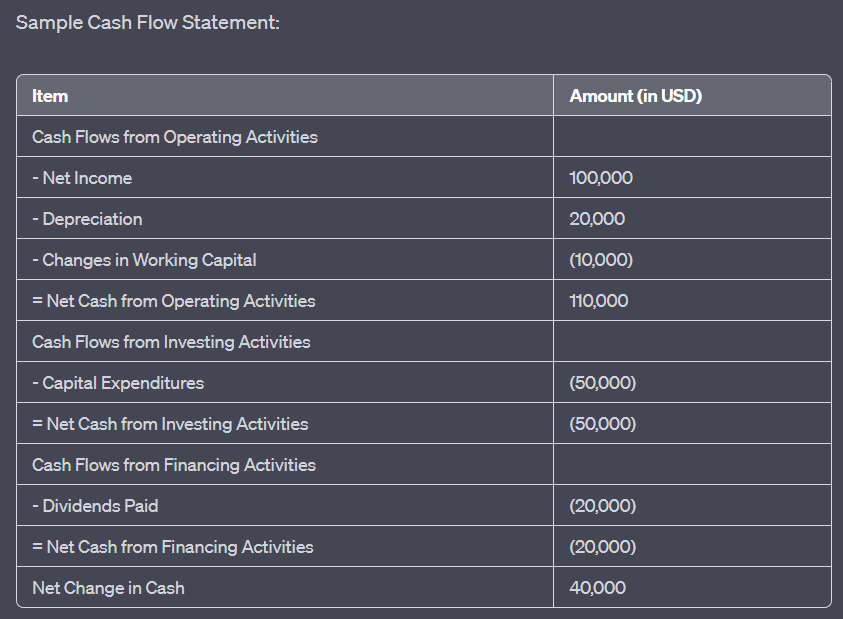

Малюнок: Sample Cash Flow Statement

опис:

The image illustrates a sample cash flow statement, which provides a detailed account of the cash inflows and outflows for a company over a specific period. The statement is segmented into three main categories: Operating Activities, Investing Activities, and Financing Activities. The key items include:

Рух грошових коштів від операційної діяльності: чистий прибуток ($100 000), амортизація ($20 000) та зміни оборотного капіталу (-$10 000), що призводить до чистого руху грошових коштів від операційної діяльності у розмірі $110 000.

Грошові потоки від інвестиційної діяльності: Капітальні витрати (-$50,000), що призводять до чистого грошового потоку від інвестиційної діяльності у розмірі -$50,000.

Грошові потоки від фінансової діяльності: Виплачені дивіденди (-$20,000), що призводить до чистого грошового потоку від фінансової діяльності у розмірі -$20,000.

Загальна чиста зміна готівки становить $40,000.

Ключові висновки:

- Операційна діяльністьВідображає грошові кошти, отримані або використані в основних бізнес-операціях.

- Інвестиційна діяльністьЯвляє собою готівку, використану для інвестицій в активи або отриману від продажу активів.

- Фінансування діяльностіДемонструє грошові потоки від або до зовнішніх джерел фінансування, таких як кредитори та акціонери.

- Чиста зміна грошових коштів дає уявлення про загальне збільшення або зменшення грошової позиції компанії за певний період.

Застосування інформації:

The cash flow statement is an essential financial tool that offers insights into a company’s liquidity and its ability to generate and use cash effectively. By analyzing the cash flow statement, stakeholders can understand how a company manages its cash resources, which is crucial for assessing its financial health and making informed investment decisions.

Висновок

In Europe, financial statements are prepared according to IFRS, ensuring a high level of consistency, transparency, and comparability across countries and industries. The звіт про доходи, баланс, та cash flow statement under IFRS provide investors with the detailed information needed to assess the financial health of European companies. IFRS’s global standards ensure that European companies’ financial reports meet international expectations, making it easier for investors to analyze and compare firms operating in different regions.

Ключова інформація про урок:

- The income statement shows a company’s profitability. The income statement provides a breakdown of a company’s revenues, cost of goods sold (COGS), operating expenses, та net income. By analyzing this statement, investors can evaluate how efficiently a company is generating profits and managing costs. Revenue recognition under IFRS ensures accurate reporting based on performance obligations.

- The balance sheet offers a snapshot of a company’s financial position. It categorizes a company’s assets, liabilities, та equity. By examining these elements, investors can assess a company’s liquidity (ability to meet short-term obligations), solvency (ability to meet long-term obligations), and фінансове здоров'я. The fundamental accounting equation of assets = liabilities + equity is key to understanding this statement.

- The cash flow statement tracks how cash is used. The statement divides cash flows into operating, інвестування, та financing activities. By analyzing this statement, investors can understand how the company generates cash from its operations, how it funds investments, and how it manages external financing. Positive cash flow from operating activities signals a strong cash position.

Заключне слово:

Financial statements under IFRS provide essential insights into a company’s financial health and performance. By analyzing the звіт про доходи, баланс, та cash flow statement, investors can make well-informed decisions based on transparency, consistency, and detailed reporting, helping them assess the company’s profitability, liquidity, and long-term sustainability.