Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Retirement planning in the United States involves understanding the multifaceted sources of retirement income and the role of Social Security in retirement planning. Here’s an exploration of key aspects related to retirement planning in the U.S., including Social Security and other income sources.

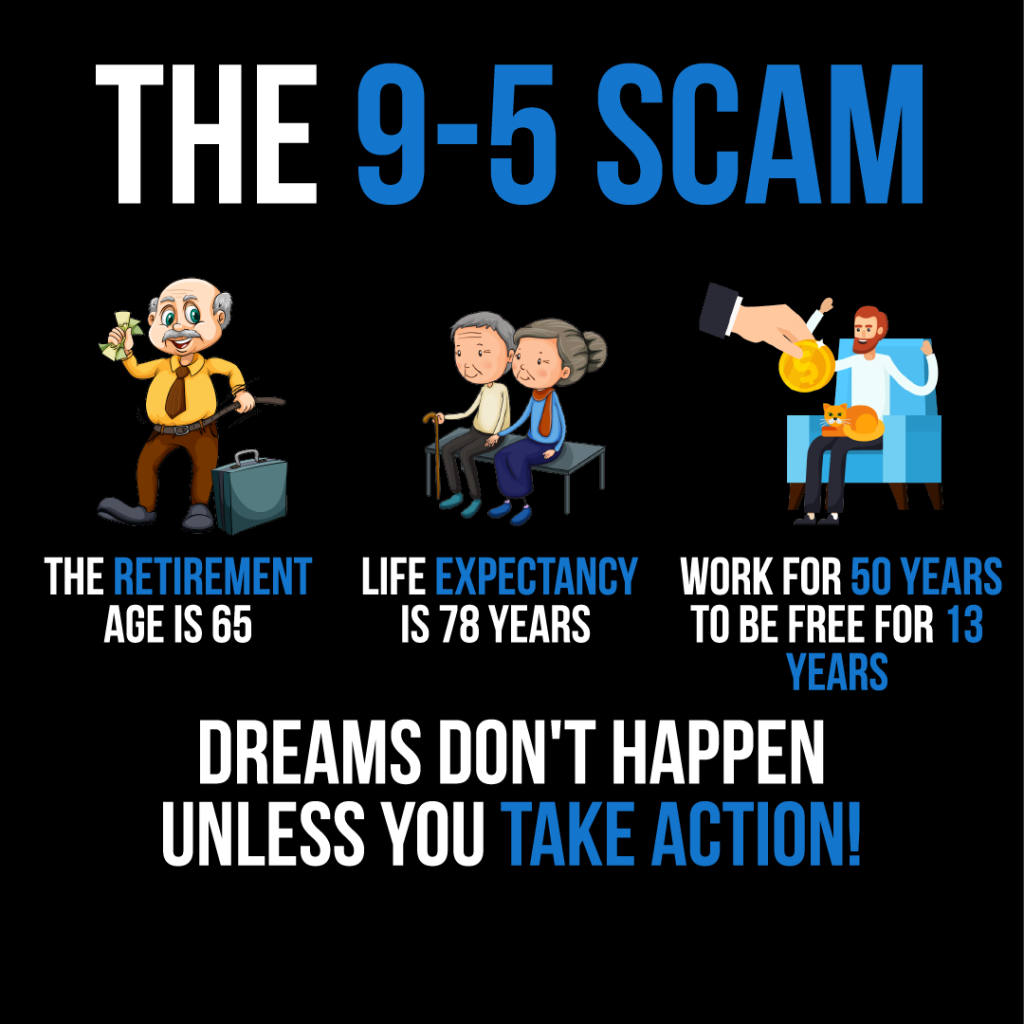

Figure: The infographic titled "The 9-5 Scam" presents a critical view of traditional work life. It points out that with a life expectancy of 78 years and a retirement age of 65, one would work for 50 years only to be free for 13 years. The message "Dreams don't happen unless you take action!" suggests that relying solely on a 9-5 job may not be the most effective path to fulfilling one's dreams. This visual is a call to action for individuals to take proactive steps towards their goals, possibly implying the pursuit of alternative income streams or early retirement strategies. For practical use, users should consider their long-term life and financial goals and explore various ways to achieve them beyond the conventional employment paradigm. Source: Custom Infographic

13.1 Understanding Social Security

Social Security Funding: Social Security is funded through payroll taxes collected under the Federal Insurance Contributions Act (FICA). Both employees and employers contribute to this fund, which then provides benefits to retirees, disabled individuals, and survivors of deceased workers. Each paycheck has a deduction (typically 6.2% from the employee and 6.2% from the employer) funding future benefits. Understanding the funding method is crucial because changes in the workforce or tax rates could affect Social Security’s long-term sustainability.

Benefits Provided: Social Security offers a safety net to retirees, providing a monthly income based on their earnings during their working years. The amount of benefit received depends on the age at retirement and the individual’s earnings record.

El average Social Security benefit for a retired worker in 2023 is approximately $1,827 per month, but this varies depending on lifetime earnings and the age at which benefits are claimed.

Example Activity: Design a promotional flyer highlighting the benefits of Social Security. The flyer could illustrate how early retirement at 62 might result in lower benefits compared to full retirement age benefits, and how delaying benefits up to age 70 can increase the monthly benefit amount. Include visuals or charts to display the difference in benefits for various income levels.

13.2 Diversifying Retirement Income

Different Sources of Retirement Income:

Social Security: A foundational source of income for many retirees, providing benefits based on your earnings history.

Employer-sponsored Retirement Plans: Such as 401(k)s and pensions, which are crucial for building a retirement nest egg.

Personal Investments: Including IRAs, stocks, bonds, and other investment vehicles.

Continued Employment Earnings: Part-time work or consulting in retirement can supplement income.

Typical sources of retirement income also include annuities, real estate rental income, reverse mortgages, and health savings accounts (HSAs) for medical expenses.

Multiple Income Sources in Retirement: Relying on a single source of retirement income, like Social Security may not be sufficient for a comfortable retirement. A diversified income strategy incorporating employer-sponsored plans and personal investments can offer a way to maintain financial security and flexibility during retirement.

Employer-Sponsored Retirement Plans: Participating in these plans is critical, like a 401(k). Many employers offer a match to your contributions, which is essentially free money for your retirement fund. Maximizing your contribution to receive the full employer match can significantly impact your retirement savings. Employees should strive to contribute at least enough to receive the full employer match — otherwise, they are leaving free money on the table.

Health Savings Accounts (HSAs) are another valuable tool for retirement planning. HSAs allow tax-free savings for medical expenses in retirement, reducing the financial burden of healthcare costs.

Average Social Security Benefit: As of recent data, the average monthly Social Security benefit for retired workers is about $1,543. However, this amount varies based on your earnings history and the age you begin to collect benefits.

Cifra: Estrategias para ahorrar para la jubilación

Descripción:

La imagen describe varias estrategias para ahorrar para la jubilación:

Ahorra 15% al año: Con el objetivo de ahorrar al menos 15% de sus ingresos anualmente.

Ahorre para los gastos más grandes: Priorice el ahorro para gastos importantes que se producirán durante la jubilación.

Ahorra más de 15% al año: Si es posible, ahorre más del 15% recomendado para crear un fondo de jubilación más sustancial.

Maximice sus cuentas de jubilación: Aproveche al máximo las cuentas de jubilación como 401(k) e IRA.

Invierta ahora a largo plazo: Concéntrese en inversiones a largo plazo para aumentar sus ahorros para la jubilación.

Aproveche las contribuciones de puesta al día: Si tiene 50 años o más, haga contribuciones de actualización a sus cuentas de jubilación.

Presupuesto para una jubilación larga: Planifica tus ahorros considerando un largo periodo de jubilación.

Obtenga ayuda con la planificación de la jubilación: Busque asesoramiento profesional para asegurarse de que está en el camino correcto hacia una jubilación segura.

Conclusiones clave:

Ahorrar una parte sustancial de sus ingresos anualmente es crucial para una jubilación cómoda.

La inversión a largo plazo y la maximización de las contribuciones a la cuenta de jubilación pueden hacer crecer significativamente su fondo de jubilación.

Hacer un presupuesto para una jubilación prolongada y obtener asesoramiento profesional sobre planificación de la jubilación puede ayudar a garantizar la seguridad financiera durante la jubilación.

Application of Information:

Estas estrategias proporcionan un enfoque estructurado hacia el ahorro para la jubilación. Siguiendo estas pautas, las personas pueden trabajar para construir un fondo de jubilación sustancial que los respalde durante sus años de jubilación. Es esencial comenzar a ahorrar e invertir temprano, aprovechar las cuentas de jubilación y considerar buscar asesoramiento profesional para garantizar una jubilación bien planificada y financieramente segura.

13.3 Planning for Retirement

To ensure a comfortable retirement, it’s essential to:

Start saving early to take advantage of compound interest.

Diversify your retirement income sources to reduce risk and increase financial security.

Understand the benefits and limitations of Social Security and plan accordingly to maximize your benefits.

Engage in employer-sponsored retirement plans and strive to contribute enough to get the full employer match.

Consider personal investments and savings plans like IRAs to build additional retirement savings.

Taxable vs Tax-Deferred vs Tax-Advantaged Accounts:

Taxable accounts (like brokerage accounts) do not offer any upfront tax benefits.

Tax-deferred accounts (like Traditional IRAs and 401(k)s) allow contributions to grow tax-free until retirement when withdrawals are taxed as income.

Tax-advantaged accounts (like Roth IRAs) involve paying taxes upfront, but earnings and qualified withdrawals are tax-free.”

Retirement vs Estate Planning:

Retirement planning focuses on ensuring financial independence during retirement by building savings through Social Security, employer plans, and personal investments.

Estate planning addresses how your assets will be distributed after your death and includes tools like wills, trusts, and beneficiary designations.

13.4 Estate Planning Tools:

Figure: A symbolic representation of retirement savings with a golden egg nestled securely, suggesting the importance of building a financial nest egg for the future.

Will: Legal document directing asset distribution after death.

Living Will: Outlines healthcare wishes if incapacitated.

Trust: Allows assets to be managed and distributed without going through probate court.

Annuities and Pensions: Can provide income streams to support heirs. Understanding these tools ensures your wishes are honored and can reduce taxes or legal fees for your heirs

Conclusión

Retirement planning in the USA should include a comprehensive strategy that combines Social Security, employer-sponsored plans, personal investments, and possibly continued employment earnings. Understanding how Social Security is funded and the benefits it provides is crucial, as is the importance of diversifying retirement income to ensure financial stability in your golden years.

Tener un plan de jubilación bien pensado le ayuda a acumular ahorros que le brindarán seguridad financiera y tranquilidad durante sus años de jubilación.

Información clave de la lección:

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.