第 8 章:信用管理及影响

课程学习目标:

Lorem ipsum dolor sit amet,consectetur adipiscing elit。 Ut elit tellus,luctus nec ullamcorper mattis,pulvinar dapibus leo。

信用管理概论

有效的信用管理包括了解各种可用的信用类型、如何比较信用成本以及认识到信用决策对个人财务的影响。本章探讨了信用管理的复杂性,包括识别错误的账单、比较信用成本以及使用信用的影响。

8.1 Identifying and Contesting Incorrect Billing Statements

消费者必须仔细检查账单中是否存在错误。 当发现账单不正确时,消费者应首先联系账单公司尝试解决。如果不满意,他们可以将投诉上报给消费者权益保护机构,例如 商业改进局 (BBB)、商会、佛罗里达州农业和消费者服务部以及联邦贸易委员会 (FTC). 这些组织可以提供调解服务,并在必要时提供进一步法律行动的指导。

8.2 Comparing Credit Costs

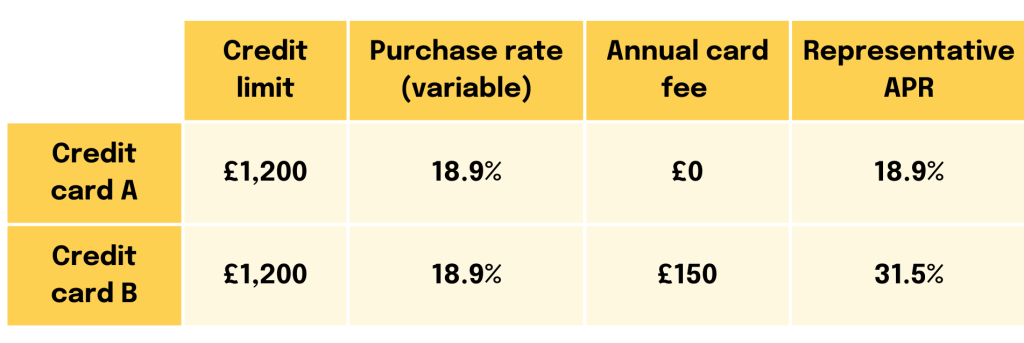

这 年利率(APR) 和 初始费用、滞纳金和未付款费用是比较信贷成本时的关键因素。APR 全面了解借贷成本,包括利率和其他费用,让消费者能够有效地比较不同的信贷来源例如,与信用卡 B 相比,信用卡 A 可能提供较低的 APR,但提供较高的逾期付款费用,从而根据用户的习惯影响总体信贷成本。

低利率信贷

金融机构可能会提供较低的介绍利率来吸引新客户。虽然这很有吸引力, 这些利率在介绍期之后可能会大幅增加,可能会导致无法在利率上升前还清余额的消费者承担更高的成本。

数字: The Difference Between Interest Rate and APR

描述:

This graphic illustrates the important distinction between a loan’s 利率 and its 年利率(APR). It visually explains that the interest rate is just one part of the borrowing cost, while the APR represents the total cost. The image shows that the APR is a broader measure because it includes both the interest rate and any additional lender fees.

要点:

- 这 利率 is the direct cost of borrowing the money and is calculated as a percentage of the principal only.

- 这 年利率(APR) provides a more complete picture of a loan’s cost, as it includes the interest rate plus any associated fees, such as origination fees or closing costs.

- Because it includes extra fees, a loan’s APR is typically higher than its advertised interest rate.

- When comparing different loan offers, looking at the 4月 allows for a more accurate, “apples-to-apples” comparison of the true cost of each option.

信息应用:

- When you are shopping for a loan, such as a mortgage or car loan, you should always compare the 4月 offered by different lenders, not just the interest rate.

- Focusing on the APR helps you understand the 总借贷成本 and avoid loans that may have a low interest rate but high hidden fees.

- This knowledge is essential for making an informed financial decision and selecting the most affordable loan, potentially saving you a significant amount of money over time.

8.3 Secured vs. Unsecured Loans and credit cards

安全 贷款需要抵押品,由于贷方风险较低,通常利率较低,例如汽车贷款或抵押贷款,如果不付款,则存在失去资产的风险。相比之下, 无抵押贷款, 与大多数信用卡一样,不需要抵押品,但利率较高。

担保信用卡 需要一个 现金存款 作为抵押品,这对贷方来说是一种低风险选择,对希望建立或重建信用的消费者来说是一种有价值的工具。 无担保信用卡 不需要押金,但通常取决于消费者的信用记录来确定是否符合资格。

8.4 Factors Influencing Borrowing Costs

首付款 减少融资总额,从而降低每月还款额或缩短贷款期限。支付大量首付的借款人对贷款人的风险较小,通常可获得更优惠的贷款条件。

信用卡:成本与效益

信用卡 信用卡虽然方便快捷,但利息和费用较高,尤其是对于信用评分较低的用户。虽然信用卡可以实现即时购买,但如果管理不善,利息和费用带来的长期成本可能会超过其收益。

信用卡 宽限期, 利息计算 方法,以及 相关费用 直接影响借贷成本。宽限期允许借款人偿还余额而不产生利息,如果使用得当,将带来显著的优势。

8.5 Consumer Protection Laws

诸如 诚实借贷法案 (TILA) 和 信用卡法案 确保贷方明确披露信贷条款并保护消费者免受不公平行为的侵害。 贷款法要求贷款人全面披露信用条款,保护消费者免受歧视性贷款、滥用营销和不公平的债务催收行为的侵害。 消费者在申请信贷时应彻底审查这些披露,以便做出明智的决定。

预防和应对欺诈

为了防止欺诈,消费者应定期监控其账户,使用安全的网上银行方式,并立即报告任何可疑活动。在发生欺诈时,及时联系金融机构和相关部门至关重要。

8.6 Free Annual Credit Reports

信用报告由 Equifax、Experian 和 TransUnion 等机构维护,在信用评估中发挥着至关重要的作用。影响信用评分的因素包括付款历史、信用利用率和信用历史长度。定期检查信用报告并对不准确的信息提出异议是保持良好信用评分的关键。

消费者每年可从各大信用报告机构获得一份免费信用报告。定期检查信用报告有助于发现可能影响借贷成本和获得信贷能力的错误。

8.7 Student Loans Comparison

比较不同类型的学生贷款,例如 PLUS 贷款、私人学生贷款和直接补贴或非补贴贷款,对于了解长期成本(包括延期期间产生的利息)至关重要。

了解不同学生贷款的细微差别可以极大地影响您的教育融资策略。以下是各种学生贷款的利息累积政策和资格标准的细分:

直接补贴贷款

- 利息累积: 美国教育部将在学生至少半日制上学期间、离开学校后的前六个月(宽限期)以及延期期间支付利息。

- 合格:适用于有经济需要的本科生.

直接无补贴贷款

- 利息累积: 利息从贷款发放给学生时起开始计算。学生有责任支付全部利息,但他们可以选择在校期间推迟支付利息,这些利息随后将资本化并添加到贷款本金中。

- 合格:适用于本科生、研究生和专业学生;无需证明经济需要。

本科生家长贷款(PLUS)

- 利息累积:利息在发放后立即开始累积。没有补贴,借款人负责支付所有利息。

- 合格:面向受赡养本科生的家长以及研究生和专业学生。申请资格不取决于经济需求,但需要进行信用检查。信用记录不良的借款人可能需要担保人。

私人学生贷款

- 利息累积: Policies vary by lender, but typically, interest starts accruing immediately upon disbursement. Some private loans offer deferment options where interest continues to accrue but payments are not required until later.

- 合格: Determined by the private lender, usually based on creditworthiness. Students often need a cosigner with good credit to qualify for the best interest rates.

主要考虑因素:

- 利息累积及资本化: 了解利息如何累积以及何时资本化(添加到贷款本金余额中)对于管理长期借贷成本至关重要。联邦补贴贷款的好处是学生在校期间不累积利息,这可以节省大量资金。

- 资格要求: 联邦贷款通常需要填写联邦学生援助免费申请表 (FAFSA) 来确定申请资格。私人贷款有自己的申请流程,可能需要提供收入证明、信用检查,甚至可能需要共同签名人。

- 选择正确的贷款: 考虑贷款的总成本,包括本金和利息,以及与借贷相关的任何费用。联邦贷款提供固定利率、收入驱动的还款计划和减免计划等福利,而这些福利在私人贷款中通常不提供。

Navigating student loans requires careful consideration of both immediate needs and future financial implications, making an understanding of each type of loan’s specifics essential for sound financial planning in pursuit of education.

8.8 Deferred Student Loan Payment

延期偿还学生贷款是一种允许借款人在某些条件下(例如经济困难、继续深造或失业)推迟偿还贷款的功能,它既可以带来即时的救济,又可以带来长期的财务影响。以下是延期偿还学生贷款的潜在后果:

Figure: Student Loan Deferment vs. Forbearance

描述:

This image compares two common options for temporarily pausing student loan payments: deferment 和 forbearance. It visually breaks down the key differences between these two programs, with a strong focus on how the 兴趣 that accumulates on the loan is handled. The goal is to help borrowers understand the financial implications of each choice before deciding.

要点:

- Both deferment 和 forbearance are official ways to pause your student loan payments if you are facing financial difficulty.

- The most important difference is in how accrued interest is treated. With deferment on certain types of federal loans (subsidized loans), the government may pay the interest for you.

- With forbearance, you are always responsible for paying the interest that accrues during the pause, regardless of your loan type.

- This unpaid interest is often capitalized at the end of the forbearance period, meaning it is added to your principal loan balance, increasing the total amount you will have to repay.

信息应用:

- If you are unable to make your student loan payments, it is critical to understand these options to choose the least costly one for your situation.

- You should always check if you qualify for deferment first, as it can save you a significant amount of money in interest payments.

- While pausing payments offers short-term relief, it’s vital to understand the long-term cost, as capitalized interest from forbearance can make your loan more expensive over time.

短期利益

- 立即的财务救济:延期付款可以为面临暂时财务困难的个人提供必要的喘息空间,使他们能够将资源分配到住房、食品或医疗费用等紧急需求上。

- 避免违约:通过正式延期贷款,借款人可以避免拖欠贷款,这有助于维持他们的信用评分并避免与贷款违约相关的严厉处罚。

长期后果

- 利息累积:对于大多数类型的学生贷款,即使没有付款,利息在延期期间仍会继续累积。这意味着总欠款金额将增加,借款人最终将在贷款期限内支付更多款项。

- 延长还款期:延期还款会延长还清贷款的时间,可能会影响借款人的长期财务目标,并推迟买房或储蓄退休等重大事件。

- 增加借贷总成本:延期期间累积的利息会增加无补贴贷款的本金余额,这可以显著增加贷款期限内偿还的总金额。

- 对减免计划资格的影响:对于通过公共服务贷款减免 (PSLF) 等计划争取贷款减免的借款人,延期期限可能不计入合格付款,从而延长减免时间。

示例场景

Alex 有 $30,000 的联邦学生贷款,利率为 5%。由于经济困难,他决定将贷款延期一年。在这一年中,他的贷款将产生 $1,500 的利息($30,000 中的 5%),如果他有无补贴贷款,这些利息将添加到他的本金余额中。当他恢复还款时,他的新余额为 $31,500,他将为这笔更高的金额支付利息,从而增加他的贷款成本。

8.9 Strategies to Mitigate Negative Consequences

- 利息支付:如果可能的话,在延期期间支付利息可以防止利息被资本化(添加到本金余额中),从而防止贷款余额增长。

- 缩短延期期限:仅在必要时使用延期,有助于最大限度地减少财务影响,因为利息会随着时间的推移而累积。

- 探索替代还款计划:收入驱动的还款计划可能提供较低的每月还款额,无需延期,并可在 20-25 年后获得贷款减免。

推迟偿还学生贷款可能是应对财务困难的一种有用的短期策略,但借款人必须考虑其对其整体财务状况的长期影响并制定相应的计划。

8.10 Credit Influence on Mortgage Rates and Payments

有担保贷款(例如抵押贷款)的利率通常低于无担保贷款。 抵押贷款还款额受贷款金额、利率和还款期限的影响。 可调利率抵押贷款(ARM) 可能会提供较低的初始利率,但如果利率上升,可能会导致未来的支付额更高。 固定利率抵押贷款 通过固定利率提供稳定性。 根据贷款条款、金额和利率比较抵押贷款选项对于找到最实惠的选项至关重要。

8.11 Credit Reports and Scores

通过信用报告和信用评分评估的信用度对借贷成本有重大影响。房东、雇主和保险公司也会在决策过程中使用这些信息。保持良好的信用记录对于财务健康至关重要。

8.12 Alternative Financial Services

发薪日贷款和类似服务可快速获得资金,但成本较高。了解这些服务的影响,包括它们可能造成的债务周期,对于金融知识至关重要。

发薪日贷款与银行贷款

发薪日贷款与银行贷款的区别在于期限和费用。发薪日贷款的利率和费用通常要高得多,因此与银行贷款相比,相同借款额的还款额要高得多。

发薪日贷款示例:

假设约翰需要 $500 来紧急修理汽车。他向发薪日贷款人求助,发薪日贷款人立即向他提供了 $500。贷款条款要求他在两周内偿还贷款,并收取 $75 的服务费。如果按年利率 (APR) 计算,这笔贷款的利息将超过 390%。如果约翰无法在两周内偿还贷款,他可能需要再申请一笔发薪日贷款,从而产生额外费用,并可能导致债务循环。

银行贷款示例:

相比之下,如果 Sarah 需要 $500 来应对类似的紧急情况,她可能会选择从她有账户的银行获得个人贷款。银行向她提供一笔年利率为 10% 的贷款(截至我上次更新(2023 年 4 月),这是个人贷款的高估值),还款期限为一年。一年下来,她将支付约 $27.29 的利息,远低于发薪日贷款的成本。

比较分析:

- 利率及费用: 与银行贷款相比,发薪日贷款的年利率极高。示例显示,发薪日贷款的年利率几乎是高利率个人银行贷款的十倍。

- 还款期限: 发薪日贷款的还款期限通常很短(通常是两周),而银行贷款的期限较长,使得每月还款更加容易管理。

- 债务周期: 发薪日贷款成本高、还款期限短,可能导致债务循环。无法按时还款的借款人可能会借入更多贷款,从而产生更多费用,从而使他们陷入债务循环。

- 对信用的影响: 如果按时还款,常规银行贷款可以帮助建立信用,这要归功于向信用机构报告。相比之下,发薪日贷款通常不会建立信用,因为除非贷款进入催收程序,否则它们并不总是向信用机构报告。

这一比较表明,尽管发薪日贷款似乎是解决财务紧急情况的快速方法,但它们的成本往往比传统银行贷款高得多,后者提供更易于管理的条款和更低的利率。借款人在选择发薪日贷款之前,应考虑所有替代方案,并了解条款和潜在的长期影响。

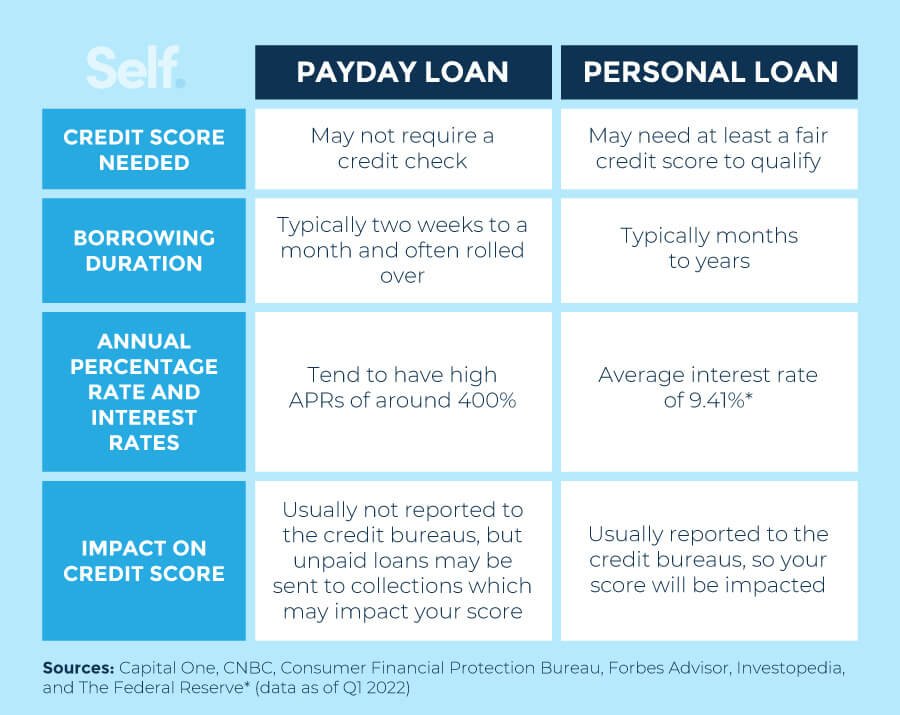

Figure: Payday Loans vs. Personal Loans

描述:

This image provides a side-by-side comparison of payday loans 和 personal loans, highlighting the critical differences between these two ways of borrowing money. It focuses on key features such as interest rates, loan amounts, and repayment terms to illustrate their respective costs and benefits. The graphic is designed to help individuals understand which option is safer and more affordable for their financial needs.

要点:

- The most significant difference is the cost: Payday loans are known for having extremely high APRs (Annual Percentage Rates), often 300% or more, while personal loans offer much lower and more manageable interest rates.

- Repayment schedules are very different. Payday loans require full repayment in a very short term (usually by your next payday), whereas personal loans are repaid in predictable monthly installments over several months or years.

- Loan amounts vary significantly. Payday loans are for small, short-term needs (typically under $500), while personal loans can provide access to much larger sums of money.

- While payday loans are often easier to obtain for those with poor credit, personal loans from reputable lenders are a much more structured and less risky form of credit.

信息应用:

- This comparison clearly shows that payday loans should be avoided whenever possible, as their high costs can quickly lead to a dangerous debt cycle.

- If you need to borrow money, a personal loan from a bank or credit union is almost always a more responsible and cost-effective financial decision.

- Understanding the true cost of debt, particularly the 4月, is a critical skill for making smart borrowing choices and protecting your long-term financial health.

8.13 Barriers to Being Banked

获得银行服务的障碍,或者说个人不使用传统银行服务的原因是多方面的,可能会严重影响财务健康和获得金融机会的机会。以下是主要障碍及其详细信息:

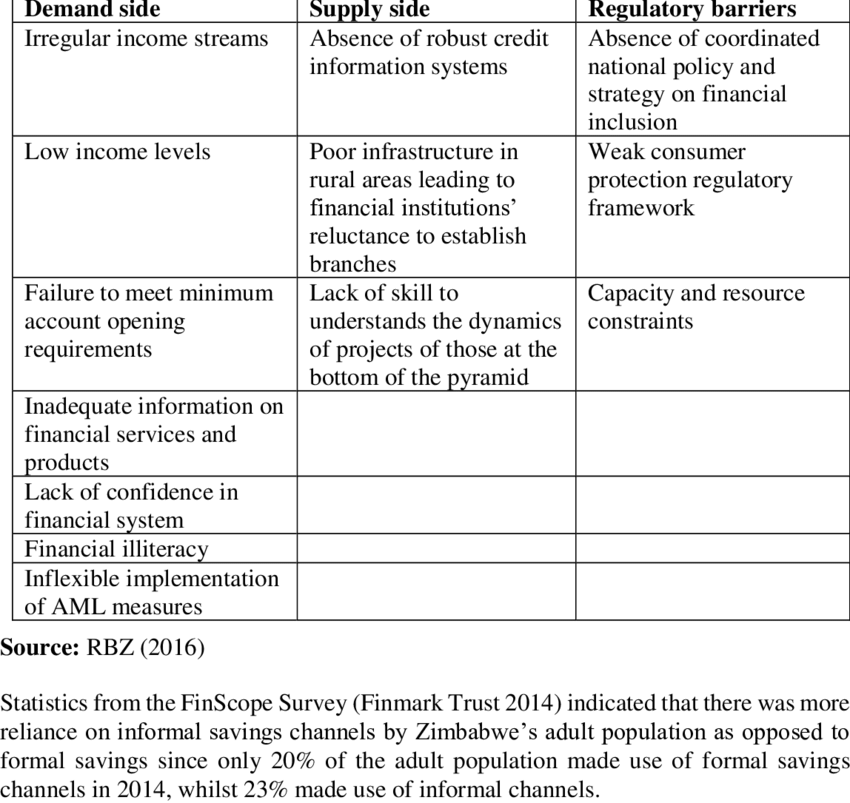

数字: Major Barriers to Financial Inclusion in Zimbabwe

描述:

This table, from a formal research publication, lists the key obstacles that prevent people across Zimbabwe from accessing and using formal financial services. The figure categorizes these challenges, highlighting issues such as high transaction costs, lack of trust in the banking system, and low levels of financial literacy. It provides a structured overview of why achieving full financial inclusion remains difficult.

要点:

- Financial inclusion faces multiple complex barriers, ranging from economic to social and educational issues.

- High service costs and bank fees are a primary obstacle, making financial services unaffordable for many low-income individuals.

- A significant portion of the population may lack the formal documentation, such as a national ID or proof of income, required to open a bank account.

- Low levels of financial literacy (a lack of understanding of financial products) and a general distrust in financial institutions are also major hindrances.

信息应用:

- Understanding these barriers is essential for anyone interested in finance or investing in emerging markets.

- This knowledge helps investors identify both the risks and the opportunities in a region; for example, a fintech company that solves the documentation problem could unlock a massive new market.

- It highlights the global importance of creating accessible and appropriate financial products that cater to the needs of underserved populations.

- 无法获得银行服务

- 地理障碍:在某些地区,特别是农村或服务不足的城市社区,银行分支机构可能很少,这使得居民难以获得银行服务。

- 数字鸿沟:缺乏互联网接入或数字素养会阻碍个人使用网上银行服务,而网上银行服务对现代银行业来说已变得越来越重要。

- High Fees

- 许多没有银行账户的个人认为,维持银行账户的高成本(例如每月维护费、最低余额要求和透支费)是重大障碍。

- 对金融机构的不信任

- 历史上的歧视行为,以及涉及大型银行的广为人知的丑闻,导致某些群体对这些机构不信任。这种怀疑态度可能会阻碍人们参与传统银行业务。

- 缺乏必要的文件

- 开立银行账户通常需要政府签发的身份证明、地址证明,有时还需要社会安全号码。移民、年轻人和其他人士可能缺乏这些文件,因此无法享受银行服务。

- 隐私问题

- 由于隐私问题或害怕政府审查,一些人,尤其是无证件人群,不愿意分享开设银行账户所需的个人信息。

- 非正规经济参与

- 在非正规经济中工作的个人可能更喜欢以现金形式进行交易以避免征税,或者因为他们的收入不稳定且不可预测,这使得维持银行账户变得更加困难。

- 感知无关性

- 有些人并不认为拥有银行账户对个人有什么好处,要么是因为他们靠薪水度日,显然不需要储蓄或投资,要么是因为他们使用支票兑现或汇票等替代金融服务来管理他们的财务。

减少障碍的解决方案和努力

金融机构、政府机构和非营利组织正在努力通过各种举措减少这些障碍:

- 低成本或无成本银行产品:提供无费用或低费用且无最低余额要求的基本银行账户。

- 金融知识和教育计划:帮助个人了解银行业务的好处以及如何有效地管理账户。

- 移动和网上银行解决方案:扩大服务不足地区或行动不便的个人获得银行服务的机会。

- 银行计划:城市、银行和非营利组织之间的合作,旨在创造可访问的银行产品并提高金融包容性。

通过解决这些障碍,更多的个人可以融入正规金融体系,为他们提供金融增长、稳定和参与更广泛经济的机会。

8.14 Managing Credit and Debt

保持良好的信用记录包括负责任地管理债务、及时还款以及了解信用查询的影响。战略性地使用信用可以提高和保持较高的信用评分,有利于消费者的财务未来。

总之,明智的管理信用需要了解各种信用产品的条款和条件,认识到借贷决策的影响,并通过明智的管理和对不准确的争议来积极保护个人信用。

Comparing Borrowing $1,000 Across Credit Options

When a consumer borrows $1,000, the total repayment amount can vary greatly depending on the credit source, interest rate, and fees involved. A careful comparison of options illustrates the real cost of credit:

- 信用卡: A standard credit card might have an 18% Annual Percentage Rate (APR) with no annual fee. If a borrower only makes minimum payments over one year, the total amount repaid could be approximately $1,180.

- Personal Loan from a Bank: A personal loan could have a 10% APR and a $25 origination fee. Repaying over one year would cost approximately $1,125, a lower total cost compared to using a credit card.

- 发薪日贷款: A payday lender might charge a $75 fee for a two-week $500 loan, rolled over once. Borrowing $1,000 could quickly escalate to $1,650 or more due to excessive fees and very short repayment periods.

🔹 Key takeaway:

Consumers must look beyond just the interest rate; initial fees, repayment terms, and hidden costs greatly influence the true cost of borrowing.

8.15 Understanding Grace Periods, Interest Methods, and Fees

这 borrowing cost of using credit cards depends heavily on several factors:

- 宽限期: A period (typically 21–30 days) during which a borrower can pay off a new balance without incurring interest. Missing this period results in full interest charges.

- Interest Calculation Methods:

- Average Daily Balance: Most common; interest is calculated on the average balance owed each day during the billing cycle.

- Previous Balance: Interest is based only on the outstanding balance from the previous month.

- Adjusted Balance: Payments made during the billing cycle are subtracted before interest is calculated, usually favoring the borrower.

- Average Daily Balance: Most common; interest is calculated on the average balance owed each day during the billing cycle.

- Fees:

- Late Payment Fee: Charged if payment is not made by the due date.

- Over-limit Fee: Charged if spending exceeds the credit limit.

- Annual Fee: Some credit cards charge a yearly fee simply for ownership.

- Late Payment Fee: Charged if payment is not made by the due date.

🔹 例子:

A cardholder who misses the grace period on a $2,000 balance with an APR of 20% could pay an extra $400 annually in interest.

8.16 Soft vs. Hard Credit Inquiries

Credit inquiries affect credit scores differently:

- Soft Inquiry: Checking your own credit, or lenders reviewing your profile for preapproval offers. Soft inquiries do not impact your credit score.

- Hard Inquiry: Occurs when you apply for a new loan or credit card. Hard inquiries can lower your credit score by a few points and stay on the report for about two years.

🔹 建议:

Limit hard inquiries by applying for new credit only when necessary, as multiple hard pulls within a short time can signal risk to lenders.

8.17 Steps to Improve Your Credit Score

Improving and maintaining a good credit score requires consistent financial habits:

- Pay On Time: Payment history makes up 35% of a FICO score.

- Keep Balances Low: Maintain credit utilization below 30% of your credit limit.

- Limit New Credit Applications: Only open new credit accounts when necessary.

- Maintain Older Accounts: Length of credit history accounts for about 15% of your score.

- 多元化信贷类型: Having a mix of credit types, such as credit cards, auto loans, and mortgages, can boost a score.

🔹 例子:

If Laura pays off her balances and avoids opening new accounts for six months, her credit score could rise by 50 points or more, saving her thousands in future interest costs.

8.18 How Employers, Landlords, and Insurers Use Credit Reports

Credit reports aren’t only important for loans:

- Employers: Some employers, especially in financial services or security-sensitive jobs, may check credit reports to gauge responsibility.

- Landlords: Credit history helps landlords assess whether a tenant will reliably pay rent.

- Insurance Companies: Insurers may use credit-based insurance scores to determine auto or home insurance premiums.

🔹 Insight:

Maintaining good credit opens up opportunities not only for better borrowing terms but also for better job prospects and lower living costs.

8.19 The Payday Loan Cycle of Debt

Payday loans, while offering quick cash, often trap borrowers in a cycle of debt:

- High Fees: A $500 payday loan with a $75 fee must be repaid in two weeks. If not repaid, the borrower rolls over the loan, adding another $75.

- Debt Trap: Borrowers might end up paying more in fees than the original loan amount without ever reducing the principal.

🔹 例子:

John borrows $500 but rolls the loan over five times, paying $375 in fees—more than half the original loan amount—without reducing the $500 debt.

8.20 Finding Help and Credible Sources on Credit

To protect themselves, consumers should rely on trusted sources:

- 消费者金融保护局(CFPB): Provides free resources on credit rights.

- 联邦贸易委员会(FTC): Offers advice on combating fraud.

- AnnualCreditReport.com: The only federally authorized site for obtaining a free yearly credit report.

🔹 Tip:

Checking credit reports at least once a year allows consumers to catch and correct errors early, maintaining better credit health.

The Role of Cosigners and Collateral in Loans

Understanding cosigners and collateral can improve loan terms:

- Cosigner: A trusted person who promises to repay if the borrower defaults, often helping borrowers with limited credit histories qualify for better rates.

- Collateral: Assets pledged to secure a loan (e.g., car, home). Secured loans typically offer lower interest rates because the lender can recover the asset if the borrower defaults.

🔹 例子:

Mark, a recent college graduate, qualifies for a 5% auto loan instead of a 10% loan because his father cosigned the loan.

结论

Incorporating these deeper insights ensures consumers are fully prepared to manage credit wisely, avoid costly mistakes, and build strong, stable financial futures. Empowered with knowledge, they can navigate the credit landscape confidently and strategically.

主要课程信息:

Lorem ipsum dolor sit amet,consectetur adipiscing elit。 Ut elit tellus,luctus nec ullamcorper mattis,pulvinar dapibus leo。