Local: analyzing European companies

Lernziele der Lektion:

- Learn about the income statement under IFRS. You will understand how revenues, Kosten, Und net income are reported, along with the inclusion of other comprehensive income (OCI). This helps investors assess a company’s profitability and financial performance.

- Understand the balance sheet under IFRS. The balance sheet provides a snapshot of a company’s assets, liabilities, Und equity, offering insights into the company’s financial position. Learn about the distinctions between current and non-current items and how they reflect a company’s liquidity and solvency.

- Explore the cash flow statement under IFRS. The cash flow statement outlines how cash is generated and used across operating, Investieren, Und financing activities. You will learn how this statement helps assess a company’s liquidity and its ability to generate cash to fund operations and investments.

- Gain insights into the overall structure and application of IFRS in European financial reporting. Understanding IFRS helps ensure transparency and comparability, making it easier to analyze financial statements and make informed investment decisions across borders.

Einführung

Understanding the core financial concepts is essential for any investor. Financial statements provide critical insights into a company’s financial health and performance, helping investors evaluate profitability, liquidity, and growth potential. This section will introduce the fundamental financial statements—Gewinn- und Verlustrechnung, Bilanz, Und cash flow statement—and explain how to analyze these documents. We will also discuss key financial data points that investors use to assess a company’s performance.

22.1 Financial Statements

When analyzing European companies, it’s essential to understand that their financial statements are typically prepared according to the International Financial Reporting Standards (IFRS), a global accounting framework that ensures transparency and comparability across borders. In Europe, IFRS is mandatory for all publicly listed companies, providing investors with consistent and clear financial information. This section introduces how financial statements in Europe adhere to IFRS, ensuring high-quality reporting.

IFRS and Income Statement

Under IFRS, the Gewinn- und Verlustrechnung (also called the statement of comprehensive income) follows a structured approach, similar to financial statements globally, but with some unique European nuances. The income statement provides detailed insight into a company’s revenues, costs, and overall profitability.

- Revenue Recognition: Under IFRS, revenue is recognized when control of a product or service is transferred to the customer. European companies must adhere to these rules, ensuring that revenues are reported accurately based on performance obligations, not just when payments are received.

- Betriebskosten: Expenses are classified by either their nature (e.g., wages, materials) or their function (e.g., cost of sales, administrative expenses). This flexibility allows European companies to present their income statements in a way that best reflects their operational structure.

- Other Comprehensive Income: IFRS emphasizes the importance of other comprehensive income (OCI), which includes gains or losses not reflected in the net income, such as foreign exchange differences or revaluation of financial instruments. This is particularly relevant for European companies operating in multiple currencies.

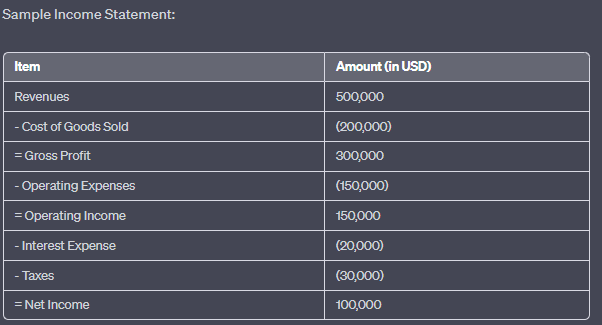

Figur: Beispiel einer Gewinn- und Verlustrechnung

Beschreibung:

The image presents a sample income statement, breaking down the financial performance of a company over a specific period. It starts with the total revenues and subtracts various expenses to arrive at the net income. The statement showcases the following items:

Umsatzerlöse: 1.040.500.000

Kosten der verkauften Waren: $(200.000)

Bruttogewinn: $300.000

Betriebskosten: $(450.000)

Betriebsergebnis: $150.000

Zinsaufwand: $(20.000)

Steuern: $(30.000)

Nettoeinkommen: $100.000

Wichtige Erkenntnisse:

- EinnahmenDer Gesamtbetrag der Einnahmen des Unternehmens vor Abzug aller Kosten.

- Kosten der verkauften Waren (COGS): Die direkten Kosten, die der Herstellung der verkauften Waren zuzurechnen sind.

- BruttogewinnDer Gewinn, den ein Unternehmen nach Abzug der Herstellungskosten von seinen Gesamteinnahmen erzielt.

- BetriebskostenDie Kosten, die im Zusammenhang mit dem täglichen Geschäftsbetrieb anfallen.

- BetriebsergebnisDer Gewinn aus der Geschäftstätigkeit (vor Zinsen und Steuern).

- ZinsaufwandDie Kosten für die Aufnahme von Krediten.

- SteuernDer an die Regierung zu zahlende Betrag basiert auf dem steuerpflichtigen Einkommen des Unternehmens.

- NettoeinkommenDer Gesamtgewinn des Unternehmens, nachdem alle Ausgaben von den Einnahmen abgezogen wurden.

Anwendung der Informationen:

Die Gewinn- und Verlustrechnung ist ein grundlegendes Finanzdokument, das Investoren und Stakeholdern Einblicke in die Rentabilität eines Unternehmens über einen bestimmten Zeitraum bietet. Durch die Analyse der Gewinn- und Verlustrechnung lassen sich die Umsatzströme, die Kostenstruktur und die allgemeine Finanzlage des Unternehmens verstehen. Diese Daten sind entscheidend für fundierte Investitionsentscheidungen und die Beurteilung der betrieblichen Effizienz des Unternehmens.

22.2 IFRS and Balance Sheet (Statement of Financial Position)

Der Bilanz, known under IFRS as the statement of financial position, provides a snapshot of a company’s assets, liabilities, and equity. IFRS requires companies to clearly differentiate between current and non-current items to offer a transparent view of a company’s financial health.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

- Verbindlichkeiten: Under IFRS, liabilities are also divided into current (due within a year) and non-current. European companies must report their obligations, including debt, leases, and pensions, in this format, providing clear insights into their short-term and long-term obligations.

- Shareholders’ Equity: The shareholders’ equity section under IFRS is structured to show both contributed capital (from shareholders) and retained earnings (profits that have been reinvested into the business). European firms must also disclose other reserves, including revaluation reserves and foreign currency translation adjustments.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

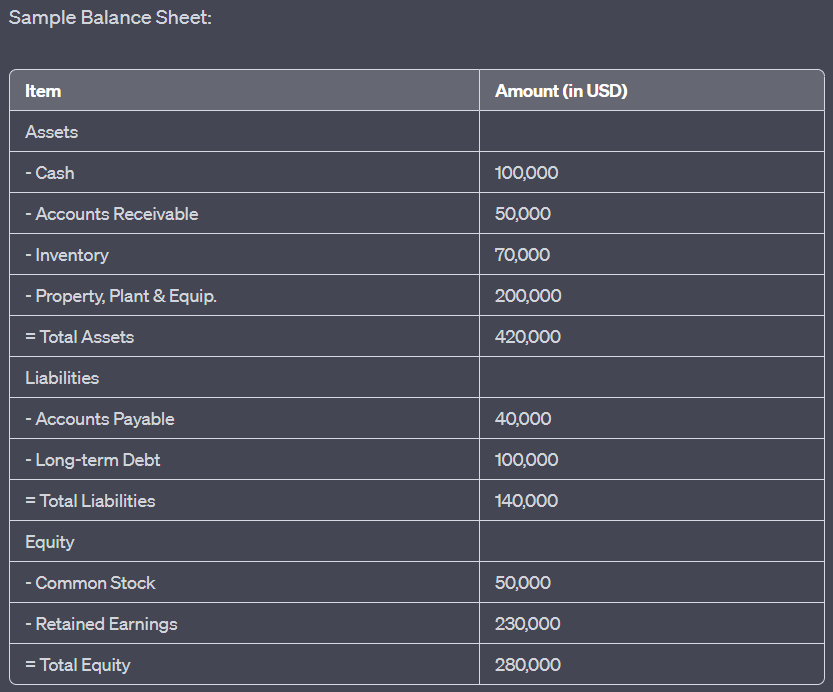

Figur: Sample Balance Sheet

Beschreibung:

The image displays a sample balance sheet, which provides a snapshot of a company’s financial position at a specific point in time. It categorizes the company’s resources (assets) and the claims against those resources (liabilities and equity). The balance sheet showcases the following items:

- Vermögenswerte: In der Summe $420.000, einschließlich Bargeld ($400.000), Forderungen aus Lieferungen und Leistungen ($50.000), Vorräte ($70.000) und Sachanlagen ($200.000).

- Verbindlichkeiten: In der Summe $140.000, bestehend aus Verbindlichkeiten aus Lieferungen und Leistungen ($40.000) und langfristigen Schulden ($400.000).

- Eigenkapital: In der Summe $280.000, davon Stammaktien ($50.000) und Gewinnrücklagen ($230.000).

Wichtige Erkenntnisse:

- Vermögenswerte: Ressourcen, die sich im Besitz des Unternehmens befinden und einen wirtschaftlichen Wert besitzen.

- VerbindlichkeitenVerpflichtungen, die das Unternehmen gegenüber externen Stellen hat.

- Eigenkapital: Stellt die Eigentumsanteile am Unternehmen dar, einschließlich der von den Aktionären investierten Gelder und der einbehaltenen Gewinne.

- The fundamental accounting equation: Assets = Liabilities + Equity.

\(\textbf{Buchhaltungsgleichung:}\)

\[ \displaystyle \text{Vermögen} = \text{Verbindlichkeiten} + \text{Eigenkapital} \]

\(\textbf{Legende:}\)

\(\text{Vermögen}\) = Gesamtvermögen

Verbindlichkeiten = Gesamtverbindlichkeiten

Eigenkapital = Gesamtes Eigenkapital

Anwendung der Informationen:

A balance sheet is a foundational financial statement that offers insights into a company’s financial health. By analyzing the balance sheet, stakeholders can assess the company’s liquidity, solvency, and overall financial stability. This information is vital for investors, creditors, and other stakeholders to make informed decisions related to the company’s financial position

22.3 IFRS and Cash Flow Statement

Der cash flow statement under IFRS follows a similar structure to other global standards but places particular emphasis on transparency in how cash is generated and used by the company. European companies use this statement to report cash flows from operating, investing, and financing activities.

- Operative Tätigkeiten: IFRS allows for flexibility in reporting cash flows from operating activities, either through the direct method (showing cash receipts and payments) or the indirect method (starting with net income and adjusting for non-cash items). Most European companies opt for the indirect method.

- Investing and Financing Activities: Cash flows related to investments in assets or securities and activities such as issuing shares or repaying debt are reported here. European companies must clearly distinguish these transactions to show how they are funding their growth and managing their financial obligations.

- Foreign Exchange Impacts: Given that many European companies operate across multiple countries and currencies, IFRS requires the inclusion of cash flow impacts due to changes in foreign exchange rates, providing investors with a clearer understanding of how currency movements affect a company’s cash position.

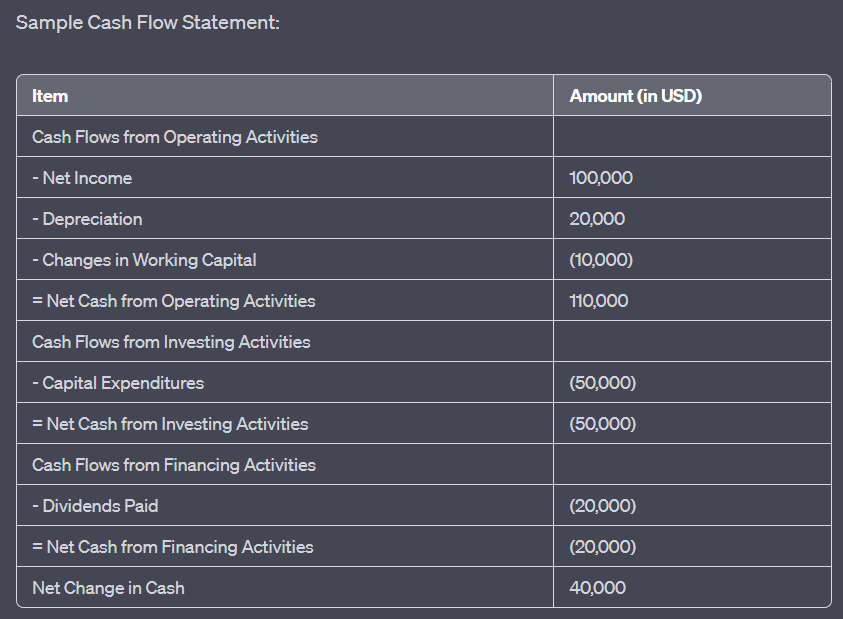

Figur: Sample Cash Flow Statement

Beschreibung:

The image illustrates a sample cash flow statement, which provides a detailed account of the cash inflows and outflows for a company over a specific period. The statement is segmented into three main categories: Operating Activities, Investing Activities, and Financing Activities. The key items include:

Cashflows aus laufender Geschäftstätigkeit: Jahresüberschuss ($100.000), Abschreibungen ($20.000) und Veränderungen des Nettoumlaufvermögens (-$10.000), was zu einem Netto-Cashflow aus laufender Geschäftstätigkeit von $110.000 führt.

Cashflows aus Investitionstätigkeiten: Die Investitionsausgaben (-$50.000) führen zu einem Netto-Cashflow aus Investitionstätigkeit von -$50.000.

Cashflows aus Finanzierungstätigkeiten: Ausgezahlte Dividenden (-$20.000), was zu einem Netto-Cashflow aus Finanzierungstätigkeiten von -$20.000 führt.

Die gesamte Nettoveränderung der liquiden Mittel beträgt $40.000.

Wichtige Erkenntnisse:

- Operative Tätigkeiten: Spiegelt die im Rahmen des Kerngeschäfts generierten oder verwendeten liquiden Mittel wider.

- Investitionstätigkeiten: Stellt Barmittel dar, die für Investitionen in Vermögenswerte verwendet oder aus dem Verkauf von Vermögenswerten erhalten wurden.

- Finanzierungsaktivitäten: Zeigt die Geldflüsse von oder zu externen Finanzierungsquellen wie Kreditgebern und Aktionären.

- Die Nettoveränderung der liquiden Mittel bietet eine Momentaufnahme der allgemeinen Zunahme oder Abnahme der liquiden Mittel des Unternehmens im betrachteten Zeitraum.

Anwendung der Informationen:

The cash flow statement is an essential financial tool that offers insights into a company’s liquidity and its ability to generate and use cash effectively. By analyzing the cash flow statement, stakeholders can understand how a company manages its cash resources, which is crucial for assessing its financial health and making informed investment decisions.

Abschluss

In Europe, financial statements are prepared according to IFRS, ensuring a high level of consistency, transparency, and comparability across countries and industries. The Gewinn- und Verlustrechnung, Bilanz, Und cash flow statement under IFRS provide investors with the detailed information needed to assess the financial health of European companies. IFRS’s global standards ensure that European companies’ financial reports meet international expectations, making it easier for investors to analyze and compare firms operating in different regions.

Wichtige Unterrichtsinformationen:

- The income statement shows a company’s profitability. The income statement provides a breakdown of a company’s revenues, cost of goods sold (COGS), operating expenses, Und net income. By analyzing this statement, investors can evaluate how efficiently a company is generating profits and managing costs. Revenue recognition under IFRS ensures accurate reporting based on performance obligations.

- The balance sheet offers a snapshot of a company’s financial position. It categorizes a company’s assets, liabilities, Und equity. By examining these elements, investors can assess a company’s liquidity (ability to meet short-term obligations), solvency (ability to meet long-term obligations), and finanzielle Gesundheit. The fundamental accounting equation von assets = liabilities + equity is key to understanding this statement.

- The cash flow statement tracks how cash is used. The statement divides cash flows into operating, Investieren, Und financing activities. By analyzing this statement, investors can understand how the company generates cash from its operations, how it funds investments, and how it manages external financing. Positive cash flow from operating activities signals a strong cash position.

Schlusserklärung:

Financial statements under IFRS provide essential insights into a company’s financial health and performance. By analyzing the Gewinn- und Verlustrechnung, Bilanz, Und cash flow statement, investors can make well-informed decisions based on transparency, consistency, and detailed reporting, helping them assess the company’s profitability, liquidity, and long-term sustainability.