Local: analyzing European companies

Malengo ya Somo:

- Learn about the income statement under IFRS. You will understand how revenues, gharama, na net income are reported, along with the inclusion of other comprehensive income (OCI). This helps investors assess a company’s profitability and financial performance.

- Understand the balance sheet under IFRS. The balance sheet provides a snapshot of a company’s assets, liabilities, na equity, offering insights into the company’s financial position. Learn about the distinctions between current and non-current items and how they reflect a company’s liquidity and solvency.

- Explore the cash flow statement under IFRS. The cash flow statement outlines how cash is generated and used across operating, kuwekeza, na financing activities. You will learn how this statement helps assess a company’s liquidity and its ability to generate cash to fund operations and investments.

- Gain insights into the overall structure and application of IFRS in European financial reporting. Understanding IFRS helps ensure transparency and comparability, making it easier to analyze financial statements and make informed investment decisions across borders.

Utangulizi

Understanding the core financial concepts is essential for any investor. Financial statements provide critical insights into a company’s financial health and performance, helping investors evaluate profitability, liquidity, and growth potential. This section will introduce the fundamental financial statements—taarifa ya mapato, mizania, na cash flow statement—and explain how to analyze these documents. We will also discuss key financial data points that investors use to assess a company’s performance.

22.1 Financial Statements

When analyzing European companies, it’s essential to understand that their financial statements are typically prepared according to the International Financial Reporting Standards (IFRS), a global accounting framework that ensures transparency and comparability across borders. In Europe, IFRS is mandatory for all publicly listed companies, providing investors with consistent and clear financial information. This section introduces how financial statements in Europe adhere to IFRS, ensuring high-quality reporting.

IFRS and Income Statement

Under IFRS, the taarifa ya mapato (also called the statement of comprehensive income) follows a structured approach, similar to financial statements globally, but with some unique European nuances. The income statement provides detailed insight into a company’s revenues, costs, and overall profitability.

- Revenue Recognition: Under IFRS, revenue is recognized when control of a product or service is transferred to the customer. European companies must adhere to these rules, ensuring that revenues are reported accurately based on performance obligations, not just when payments are received.

- Gharama za Uendeshaji: Expenses are classified by either their nature (e.g., wages, materials) or their function (e.g., cost of sales, administrative expenses). This flexibility allows European companies to present their income statements in a way that best reflects their operational structure.

- Other Comprehensive Income: IFRS emphasizes the importance of other comprehensive income (OCI), which includes gains or losses not reflected in the net income, such as foreign exchange differences or revaluation of financial instruments. This is particularly relevant for European companies operating in multiple currencies.

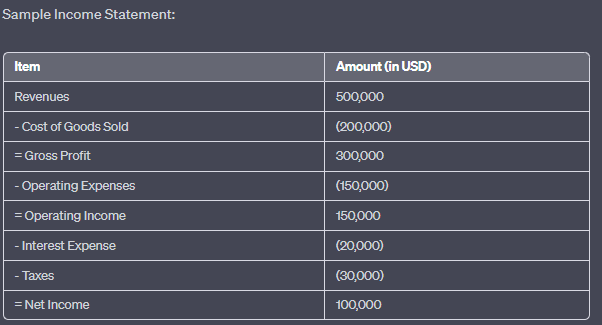

Kielelezo: Mfano wa Taarifa ya Mapato

Maelezo:

The image presents a sample income statement, breaking down the financial performance of a company over a specific period. It starts with the total revenues and subtracts various expenses to arrive at the net income. The statement showcases the following items:

Mapato: $500,000

Gharama ya Bidhaa Zinazouzwa: $(200,000)

Faida ya Jumla: $300,000

Gharama za Uendeshaji: $(450,000)

Mapato ya Uendeshaji: $150,000

Gharama ya Riba: $(20,000)

Ushuru: $(30,000)

Mapato halisi: $100,000

Mambo muhimu ya kuchukua:

- Mapato: Jumla ya pesa inayoletwa na kampuni kabla ya matumizi yoyote.

- Gharama ya Bidhaa Zinazouzwa (COGS): Gharama za moja kwa moja zinazotokana na uzalishaji wa bidhaa zinazouzwa.

- Faida ya Jumla: Faida ambayo kampuni inapata baada ya kupunguza COGS kutoka kwa jumla ya mapato yake.

- Gharama za Uendeshaji: Gharama zinazohusiana na shughuli za kila siku za biashara.

- Mapato ya Uendeshaji: Faida kutokana na shughuli za biashara (kabla ya riba na kodi).

- Gharama ya Riba: Gharama ya fedha za kukopa.

- Kodi: Kiasi kinacholipwa kwa serikali kulingana na mapato ya kampuni yanayotozwa ushuru.

- Mapato halisi: Faida ya jumla ya kampuni baada ya gharama zote kukatwa kutoka kwa mapato.

Utumiaji wa Taarifa:

Taarifa ya mapato ni hati ya kimsingi ya kifedha ambayo huwapa wawekezaji na washikadau maarifa kuhusu faida ya kampuni katika kipindi mahususi. Kwa kuchanganua taarifa ya mapato, mtu anaweza kuelewa mitiririko ya mapato ya kampuni, muundo wa gharama na afya ya kifedha kwa ujumla. Data hii ni muhimu kwa kufanya maamuzi sahihi ya uwekezaji na kutathmini ufanisi wa uendeshaji wa kampuni.

22.2 IFRS and Balance Sheet (Statement of Financial Position)

The mizania, known under IFRS as the statement of financial position, provides a snapshot of a company’s assets, liabilities, and equity. IFRS requires companies to clearly differentiate between current and non-current items to offer a transparent view of a company’s financial health.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

- Madeni: Under IFRS, liabilities are also divided into current (due within a year) and non-current. European companies must report their obligations, including debt, leases, and pensions, in this format, providing clear insights into their short-term and long-term obligations.

- Shareholders’ Equity: The shareholders’ equity section under IFRS is structured to show both contributed capital (from shareholders) and retained earnings (profits that have been reinvested into the business). European firms must also disclose other reserves, including revaluation reserves and foreign currency translation adjustments.

- Asset Classification: European companies report assets as either current or non-current. Current assets include items like cash, receivables, and inventory, while non-current assets encompass long-term investments such as property, plant, and equipment (PPE), as well as intangible assets like goodwill.

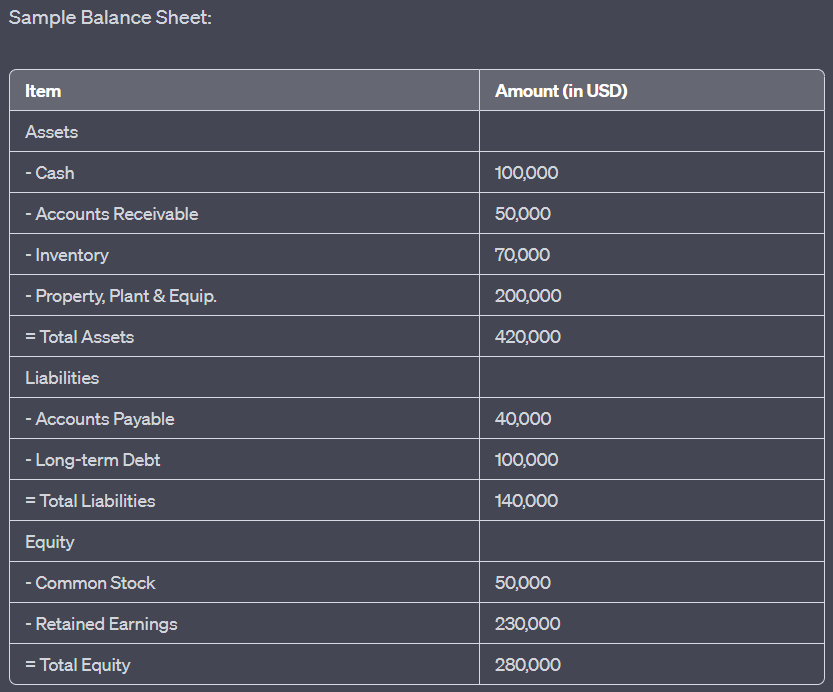

Kielelezo: Sample Balance Sheet

Maelezo:

The image displays a sample balance sheet, which provides a snapshot of a company’s financial position at a specific point in time. It categorizes the company’s resources (assets) and the claims against those resources (liabilities and equity). The balance sheet showcases the following items:

- Mali: Jumla ya $420,000, ikijumuisha Fedha ($400,000), Akaunti Zinazopokelewa ($50,000), Mali ($70,000), na Mali, Mitambo na Vifaa ($200,000).

- Madeni: Jumla ya $140,000, inayojumuisha Akaunti Zinazolipwa ($40,000) na Deni la Muda Mrefu ($400,000).

- Usawa: Jumla ya $280,000, yenye Hisa ya Kawaida ($50,000) na Mapato Yanayobaki ($230,000).

Mambo muhimu ya kuchukua:

- Mali: Rasilimali zinazomilikiwa na kampuni ambazo zina thamani ya kiuchumi.

- Madeni: Majukumu ambayo kampuni inadaiwa na vyombo vya nje.

- Usawa: Inawakilisha maslahi ya umiliki katika kampuni, ikiwa ni pamoja na fedha zilizowekezwa na wanahisa na faida iliyokusanywa.

- The fundamental accounting equation: Assets = Liabilities + Equity.

\(\textbf{Mlingano wa Uhasibu:}\)

\[ \displaystyle \text{Assets} = \text{Madeni} + \text{Equity} \]

\(\textbf{Legend:}\)

\(\text{Assets}\) = Jumla ya mali

\(\text{Liabilities}\) = Jumla ya madeni

\(\text{Equity}\) = Jumla ya usawa

Utumiaji wa Taarifa:

A balance sheet is a foundational financial statement that offers insights into a company’s financial health. By analyzing the balance sheet, stakeholders can assess the company’s liquidity, solvency, and overall financial stability. This information is vital for investors, creditors, and other stakeholders to make informed decisions related to the company’s financial position

22.3 IFRS and Cash Flow Statement

The cash flow statement under IFRS follows a similar structure to other global standards but places particular emphasis on transparency in how cash is generated and used by the company. European companies use this statement to report cash flows from operating, investing, and financing activities.

- Shughuli za Uendeshaji: IFRS allows for flexibility in reporting cash flows from operating activities, either through the direct method (showing cash receipts and payments) or the indirect method (starting with net income and adjusting for non-cash items). Most European companies opt for the indirect method.

- Investing and Financing Activities: Cash flows related to investments in assets or securities and activities such as issuing shares or repaying debt are reported here. European companies must clearly distinguish these transactions to show how they are funding their growth and managing their financial obligations.

- Foreign Exchange Impacts: Given that many European companies operate across multiple countries and currencies, IFRS requires the inclusion of cash flow impacts due to changes in foreign exchange rates, providing investors with a clearer understanding of how currency movements affect a company’s cash position.

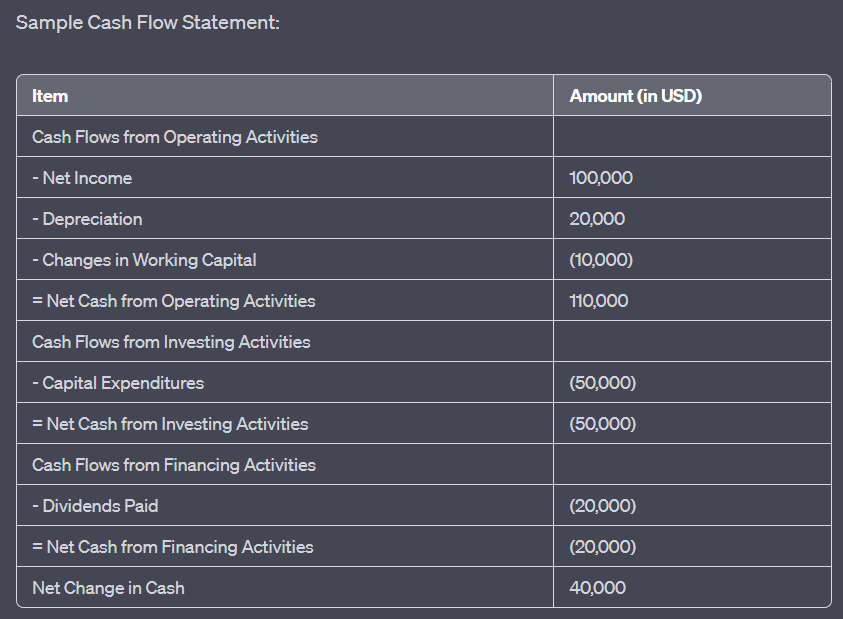

Kielelezo: Sample Cash Flow Statement

Maelezo:

The image illustrates a sample cash flow statement, which provides a detailed account of the cash inflows and outflows for a company over a specific period. The statement is segmented into three main categories: Operating Activities, Investing Activities, and Financing Activities. The key items include:

Mtiririko wa Pesa kutoka kwa Shughuli za Uendeshaji: Mapato Halisi ($100,000), Kushuka kwa Thamani ($20,000), na Mabadiliko ya Mtaji Unaofanya Kazi (-$10,000), na kusababisha Pesa Halisi kutokana na Shughuli za Uendeshaji za $110,000.

Mtiririko wa Pesa kutoka kwa Shughuli za Uwekezaji: Capital Expenditures (-$50,000), inayoongoza kwa Pesa Halisi kutoka kwa Shughuli za Uwekezaji za -$50,000.

Mtiririko wa Pesa kutoka kwa Shughuli za Ufadhili: Gawio Lililolipwa (-$20,000), na kusababisha Pesa Halisi kutokana na Shughuli za Ufadhili wa -$20,000.

Mabadiliko Halisi katika Fedha Taslimu ni $40,000.

Mambo muhimu ya kuchukua:

- Shughuli za Uendeshaji: Huakisi pesa zinazozalishwa au kutumika katika shughuli kuu za biashara.

- Shughuli za Uwekezaji: Inawakilisha pesa taslimu zinazotumika kwa uwekezaji katika mali au kupokea kutokana na mauzo ya mali.

- Shughuli za Ufadhili: Inaonyesha mtiririko wa pesa kutoka au kwenda kwa vyanzo vya ufadhili vya nje, kama vile wakopeshaji na wanahisa.

- Mabadiliko Halisi katika Pesa hutoa mukhtasari wa ongezeko la jumla au kupungua kwa nafasi ya pesa ya kampuni katika kipindi hicho.

Utumiaji wa Taarifa:

The cash flow statement is an essential financial tool that offers insights into a company’s liquidity and its ability to generate and use cash effectively. By analyzing the cash flow statement, stakeholders can understand how a company manages its cash resources, which is crucial for assessing its financial health and making informed investment decisions.

Hitimisho

In Europe, financial statements are prepared according to IFRS, ensuring a high level of consistency, transparency, and comparability across countries and industries. The taarifa ya mapato, mizania, na cash flow statement under IFRS provide investors with the detailed information needed to assess the financial health of European companies. IFRS’s global standards ensure that European companies’ financial reports meet international expectations, making it easier for investors to analyze and compare firms operating in different regions.

Habari Muhimu ya Somo:

- The income statement shows a company’s profitability. The income statement provides a breakdown of a company’s revenues, cost of goods sold (COGS), operating expenses, na net income. By analyzing this statement, investors can evaluate how efficiently a company is generating profits and managing costs. Revenue recognition under IFRS ensures accurate reporting based on performance obligations.

- The balance sheet offers a snapshot of a company’s financial position. It categorizes a company’s assets, liabilities, na equity. By examining these elements, investors can assess a company’s ukwasi (ability to meet short-term obligations), solvency (ability to meet long-term obligations), and afya ya kifedha. The fundamental accounting equation of assets = liabilities + equity is key to understanding this statement.

- The cash flow statement tracks how cash is used. The statement divides cash flows into operating, kuwekeza, na financing activities. By analyzing this statement, investors can understand how the company generates cash from its operations, how it funds investments, and how it manages external financing. Positive cash flow from operating activities signals a strong cash position.

Taarifa ya Kufunga:

Financial statements under IFRS provide essential insights into a company’s financial health and performance. By analyzing the taarifa ya mapato, mizania, na cash flow statement, investors can make well-informed decisions based on transparency, consistency, and detailed reporting, helping them assess the company’s profitability, liquidity, and long-term sustainability.